CBSH - Commerce Bancshares: Fantastic Business But A Premium

2023-07-20 10:09:29 ET

Summary

- Commerce Bancshares Inc's share price has dropped over 20% since the start of 2023, but the company's fundamentals remain strong, making it a good option for investors to hold and collect a 2.1% dividend yield.

- Despite challenges from rising interest rates, CBSH has shown strength with increased deposits and loans, a robust return on equity, and an efficiency ratio of 57.2%, indicating efficient growth.

- CBSH maintains a conservative approach by avoiding high-risk assets but will need to carefully manage its available-for-sale securities portfolio to weather the current market efficiently.

Introduction

The financial sector struggled in 2023 as the meltdown of some of the largest banks in the United States and other regional banks came down with the broader sector. The share price of Commerce Bancshares Inc (CBSH) is down over 20% to the start of 2023. This could to some make it out as a very good entry point seeing as the price has decreased so much. But I find the valuation still not to be in the buying territory and would much rather want a valuation around 9x earnings and p/b under 1. CBSH is still far from that.

But the fundamentals of the business are still very strong and I can't see a good enough reason to sell shares in CBSH. Instead, investors are better off holding shares and collecting the 2.1% dividend yield and benefit from the steadily decreasing outstanding shares as CBSH management continues buying them back. As stated, I think CBSH is a hold for now until the valuation compresses into more reasonable territories.

Company Structure

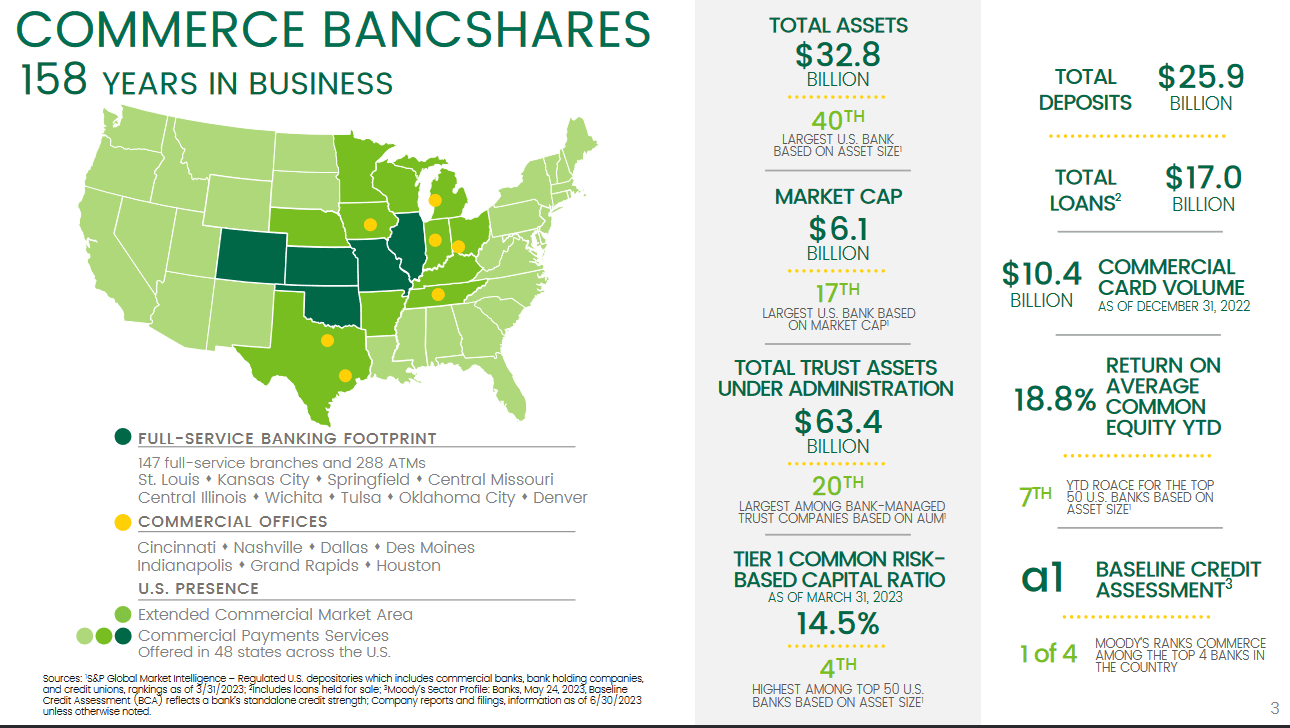

Commerce Bancshares has a very long and rich history of operations as it was founded back in 1865. This makes it one of the oldest in the industry and during the period it has grown its balance sheet at a solid rate. The tangible book value has grown 2.12% YoY in the last 10 years. This is the stability that investors are seeking when viewing CBSH.

{kind=link}

The company has a broad exposure in the United States and total deposits now amount to $25.9 billion and loans at $17 billion. The company operates as a bank holding business that provides retail, mortgage, and banking. But they are also versed in asset management and various individual financial services. The business has been divided into three different segments, those being Consumer, Commercial, and Wealth. The first segment offers banking products and services, consumer deposits, and consumer loans for example. In the second segment, CBSH has its lending and leasing operations located. Lastly, the Wealth segment offers customers trust and estate planning but also portfolio management and leasing services. With a diversified business model, it has netted CBSH a very strong ROE of 17.25% in the last 12 months. I expect similar numbers to be displayed given the experience of the people running the company and the broad exposure the company has two various regions.

{kind=link}

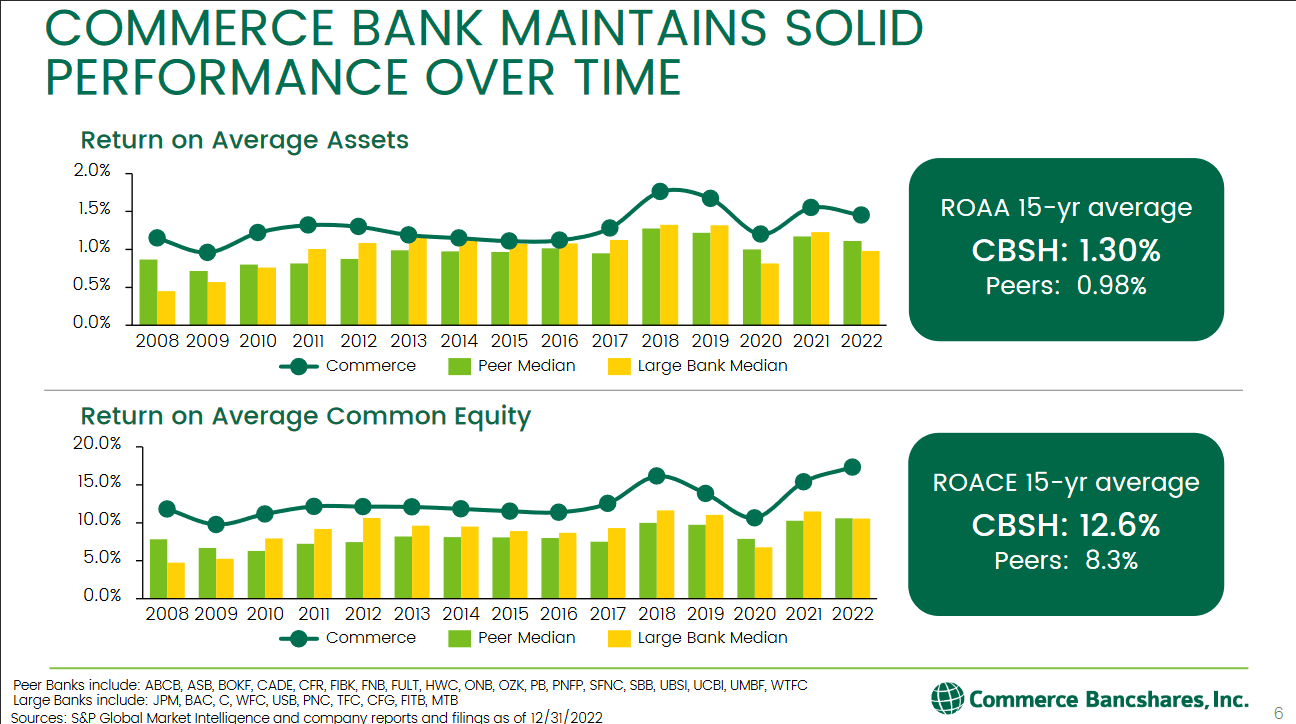

Historically, CBSH has a very strong track record of growth and retention of returns. The ROACE 15-year average is 12.6 for CBSH, whilst the pores are nearly 50% below 8.3% during that period. Assets have also grown consistently over time and CBSH over the last 15 years maintained profitability on it. These results could be the reason that CBSH is trading at the valuation it does currently.

Earnings Results

The recent results from CBSH showed strength as the deposits and loans increased. A beat on both the top and bottom line as well had investors very pleased.

Earnings Results (Seeking Alpha)

The EPS came in at $1.02 and revenues at $397 million. But what caught my attention was the ROA being 1.56%. This is some of the highest returns the company has had historically, and the ROE remained robust too at 18.81%. To further underscore the strength of CBSH right now just looking at the efficiency ratio of 57.2% tells the story that CBSH has been able to grow efficiently in recent months as interest rates continued to rise.

{kind=link}

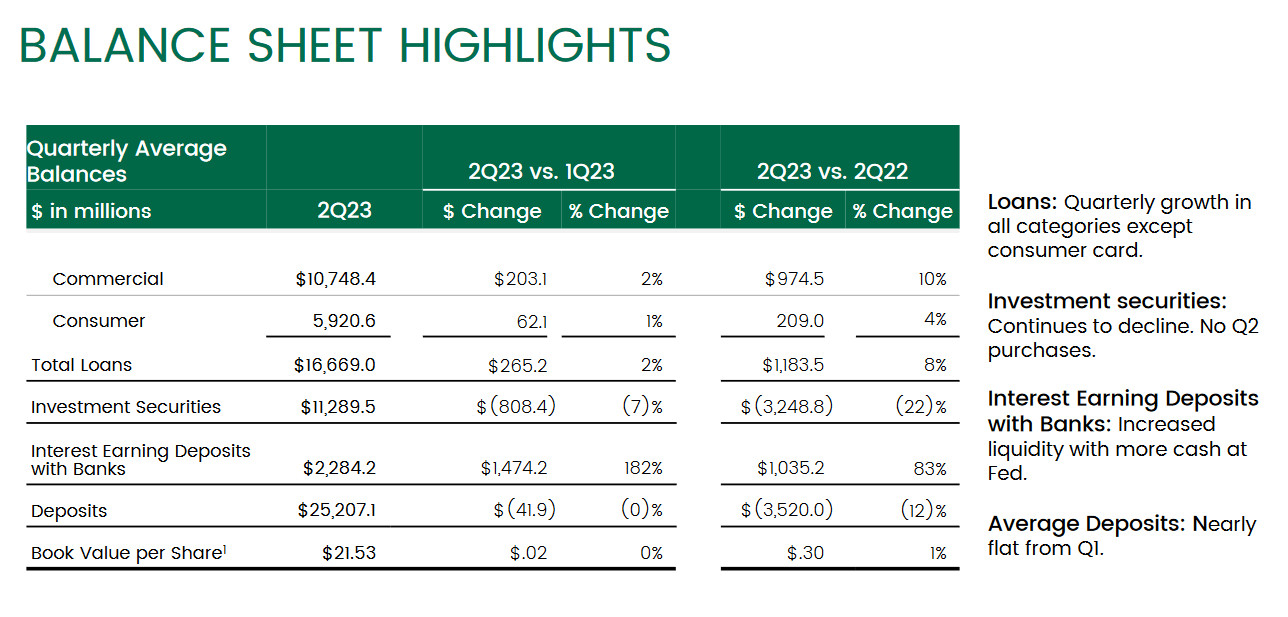

As shown in the balance sheet highlights from the Q2 FY2023 report, the book value per share for CBSH is $21.53. The current share price is still over 2x this and underscores why perhaps right now isn't a solid buying opportunity. But apart from that, the balance sheet saw some solid growth as commercial growth was 10% YoY and interest-earning deposits with banks were 83%. That's a monster result and for the next Q3 report, I think it's highly likely we see more growth as interest rates are still growing and not expected to stop just yet in 2023.

Risk Associated

CBSH maintains a significant available-for-sale ("AFS") securities portfolio, with a concentration in mortgage-backed and asset-backed securities, as well as state and municipal obligations. However, the fixed-rate nature of these securities exposed the company to unrealized losses when interest rates rose last year, creating challenges for its financial performance.

{kind=link}

Despite these challenges, one positive aspect is that CBSH demonstrates a conservative approach by avoiding exposure to high-risk assets such as cryptocurrencies and venture capital investments. Instead, the credit card business represents the only high-risk segment in its portfolio.

To navigate the volatile market conditions, CBSH will need to carefully manage its AFS portfolio, considering potential interest rate fluctuations and adopting risk mitigation strategies. Moreover, as the credit card business presents some inherent risks, the company may need to maintain a vigilant risk management framework to safeguard its financial stability.

Investor Takeaway

For investors that are looking for a solid dividend play and don't relay mind paying a slight premium right now then CBSH might look appealing. The company has grown the dividend for 54 years consistently, and the last 5 years have averaged a 9.27% annual growth.

Dividend Summary (Seeking Alpha)

The payout ratio is still quite low at under 30% leaving more room for growth. But the company is still training at a bit above where I am comfortable buying. An FWD p/e of 13 and a p/b of over 2 is above my preferred valuations. I find however that the quality of CBSH is clearly on display still as the last report beat on estimates. Because of this, I am rating CBSH a hold.

For further details see:

Commerce Bancshares: Fantastic Business But A Premium