MBB - Commercial And Multifamily Mortgage Loan Investments For A Fixed Income Portfolio

2023-09-13 08:40:00 ET

Summary

- In a volatile economic environment, core commercial and multifamily mortgage loan investments may provide investors with an attractive credit risk profile, appealing relative value, and diversification benefits.

- From a relative value perspective, CML spreads have historically provided excess returns compared to similarly rated corporate bonds.

- However, the private market nature of core commercial mortgage investments creates both challenges and opportunities for investors.

By Dan Dickman, Managing Director, Portfolio Management

In a volatile economic environment, core commercial and multifamily mortgage loan investments may provide investors with an attractive credit risk profile, appealing relative value, and diversification within a larger fixed income portfolio.

Moreover, these investments may offer high current income returns, limited correlation of returns with other fixed income alternatives, call protection, and the ability for investors to tailor their portfolios to meet specific durational needs.

It is essential for investors to select a well-qualified asset manager to help them reap the potential benefits of investing in commercial and multifamily mortgages, since the asset class can be difficult to navigate.

Potential key benefits of allocating to commercial and multifamily mortgage loan investments:

- Attractive credit risk profile

- Appealing relative value

- Appealing current income returns

- Call protection

- Limited correlation of returns with fixed income alternatives

The asset class

Core commercial and multifamily mortgage loan (“CML”) investments include private mortgage loans secured by first liens on well-leased, income- producing properties such as industrial, retail, office, and multifamily residential properties. Investment sizes range from less than $10 million to more than $100 million per transaction, with terms ranging from less than three years to 30 years or longer. Value-added investments in subordinate debt and bridge loans secured by commercial and multifamily real estate are also available, although here we will focus primarily on core, senior investments. According to the U.S. Federal Reserve (Fed), the total balance of commercial and multifamily real estate debt outstanding in the United States was approximately $5.67 trillion at the end of first quarter 2023 1 . CML investors include commercial banks, asset-backed security issuers, insurance companies, government-sponsored enterprises, finance companies, pension funds and others.

Credit risk

Underwriting metrics for newly originated CML investments remain robust from an historical perspective, buoyed by changes to insurance company risk-based capital ((RBC)) charge requirements adopted by the National Association of Insurance Commissioners (NAIC) in 2013. Banks also progressively tightened lending standards for stabilized commercial and multifamily residential properties each quarter from late 2018 through early 2021 before leveling their underwriting expectations, which remain tight overall. 2

The current RBC rubric from the NAIC mandates different minimum levels of capital for loans with different loan-to-value ("LTV") and debt service coverage ratios ((DSCR)), creating a meaningful economic incentive for insurance company lenders to take a conservative approach toward underwriting. As a result, average credit metrics for core CMLs have been more conservative over the past 10 years. (See Exhibit 1).

Of course, even with the pre-2013 underwriting metrics, insurance companies enjoyed strong credit performance in their CML portfolios, with industry delinquency rates averaging just 1.6% and an average loss upon foreclosure of approximately 20.2% prior to 2013 (and better since that time, as older loans repaid). 3 The result has been minimal loss rates for core CML portfolios.

Exhibit 1: Insurance company fixed-rate CMLs

| Pre-2013 | Post-2013 | |

|---|---|---|

| Average LTV | ||

| 69.6% | ||

| 59.0% | ||

| Average DSCR | ||

| 1.46 | ||

| 2.10 |

Source: The American Council of Life Insurers’ quarterly Commercial Mortgage Commitments reports through Q2 2023.

- Regarding default risk, we believe robust debt service coverage ratios underwritten for core CMLs today allow significant declines in net operating incomes before property income streams can no longer cover debt service payments and operating expenses.

- With regard to the potential severity of core CML losses, we believe today’s low loan-to-value ratios allow significant declines in property values before losses would be realized on defaulted loans.

- Core CML underwriting margins remain strong.

Case Study: Gauging historical portfolio performance

To supplement the analysis of historical credit loss data from the ACLI, we studied the performance of 33 commercial mortgage loan portfolios that Principal Real Estate created and managed. The data set included CMLs originated for each of our non-affiliated core CML clients. However, the study excluded Principal Life Insurance Company data so that the results might better reflect a broad range of strategies employed for various clients. Consisting of loans originated between 1988 and 2022, the data set included 1,425 loans with an original principal balance of $11.24 billion. At year-end 2022, loans with an aggregate balance of $4.63 billion remained outstanding.

The key findings of the study included:

Of the 1,425 loans studied, 25 experienced losses. This equated to 1.75% of all loans originated by loan count.

For the 25 loans that incurred losses, cumulative losses totaled $41.73 million. That resulted in an average loss severity of 26% for loans experiencing losses.

Based on an approximate outstanding term of six years and weighted by loan amount, the average annual portfolio loss rate was 0.062% , or roughly 6 basis points per year.

Case Study is shown for example and illustrate purposes only and is not a prediction of future results.

Relative value

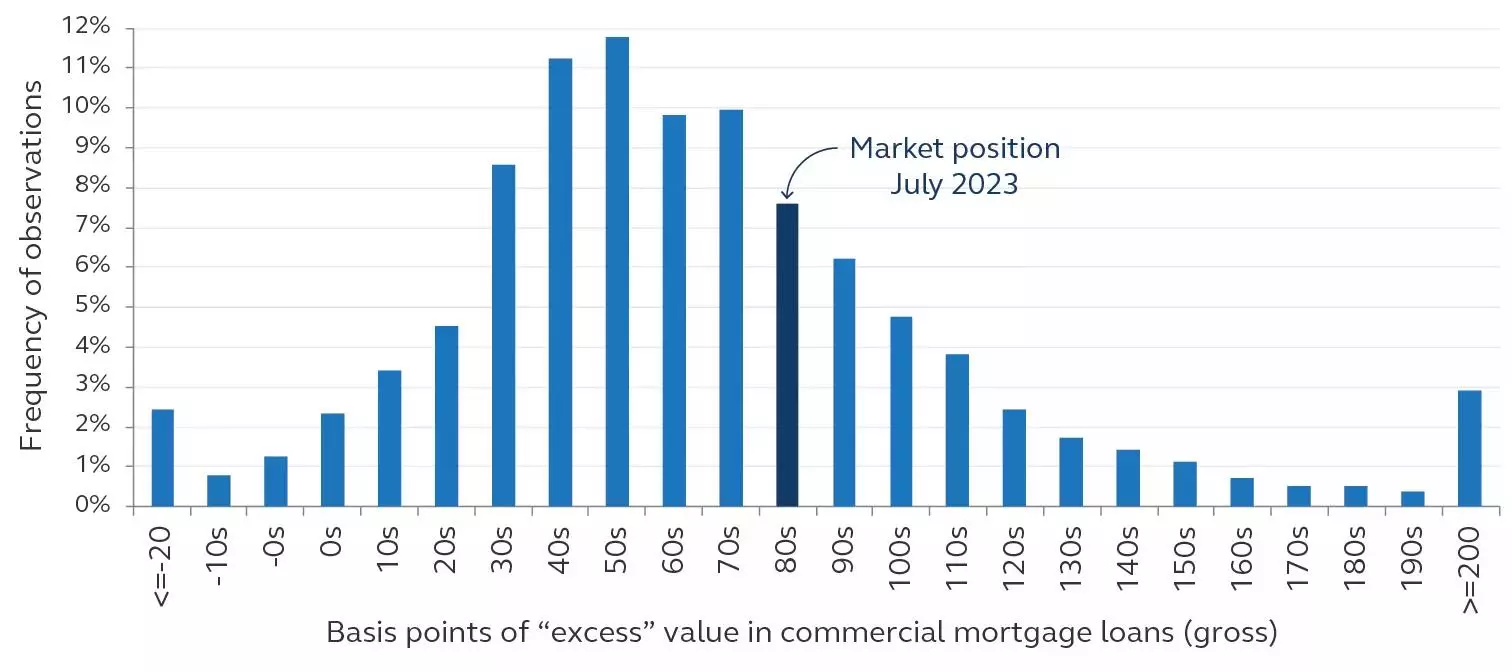

From a relative value perspective, CML spreads have historically provided excess returns compared to similarly rated corporate bonds. 4 To showcase this difference, we examined the differential between Principal Real Estate's market-clearing spread estimates for core CMLs and Bloomberg Barclays corporate bond spread indices. When considering 5- and 10-year terms and a range of credit ratings between AAA and BBB+, on average core CMLs offered approximately 68 basis points (bps) of excess returns relative to comparably rated corporate bonds since the beginning of the year 2000. The spread differential offsets the higher administrative costs and lower liquidity of mortgages compared to corporate bonds, and we believe the differentials make core CML investments attractive from a risk-return perspective.

Exhibit 2: Relative value at market-clearing: CML spread premiums observed since 2000 CML market-clearing spread estimates less Corporate Bond Composite Index

5- & 10-Year terms, BBB+ equivalent & better, classes & times weighted equally, annual effective yield basis

{kind=link}

Source: Barclays, Aladdin, Principal Real Estate, July 2023.

Returns

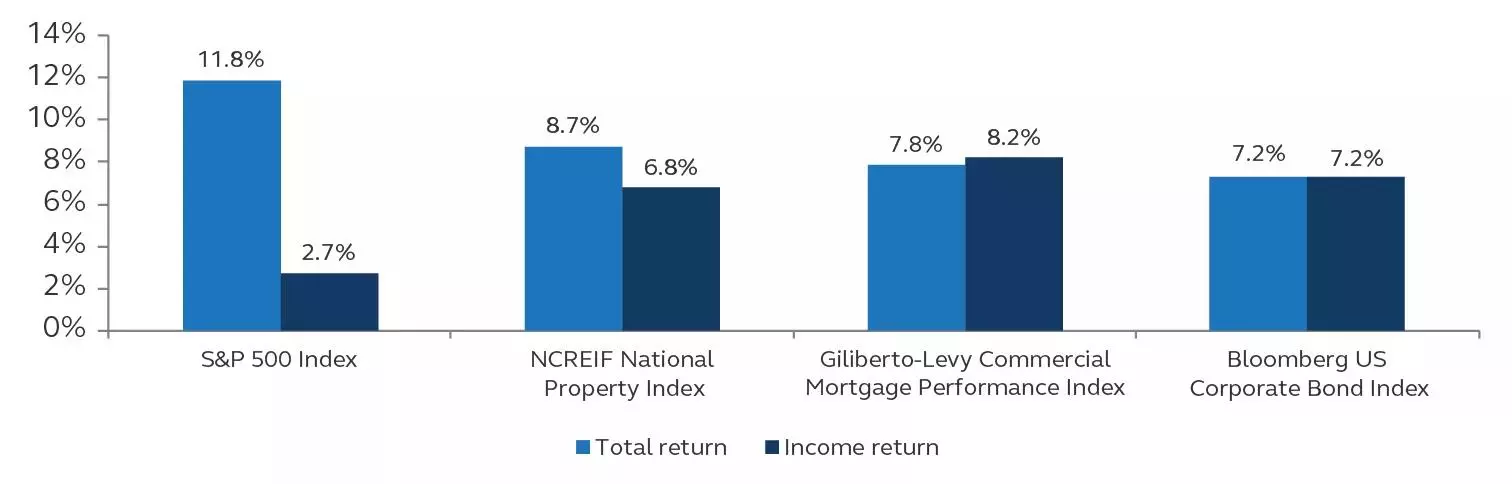

Over the past 44 years, CMLs delivered total returns approaching those of real estate equity and exceeded those of corporate bonds. 5 An analysis of the same data set revealed that CMLs provided a consistently high level of current returns over time, which is an attribute of the asset class particularly appealing to investors with significant current liabilities.

Exhibit 3: Average annual returns - Total return vs. income return

Q4 1978 through Q2 2023

{kind=link}

Source: Bloomberg, S&P, NCREIF, and Giliberto-Levy, Q2 2023. The S&P 500 index represents U.S. equities. The NCREIF National Property Index represents performance of commercial real estate. The Giliberto-Levy Commercial Mortgage Performance Index represents U.S. core commercial real estate loans. The Bloomberg US Corporate Bond Index represents the investment grade U.S. corporate bond market. Please see index descriptions on page 6. Indices are unmanaged and do not take into account fees, expenses, and transaction costs and it is not possible to invest in an index.

Other considerations

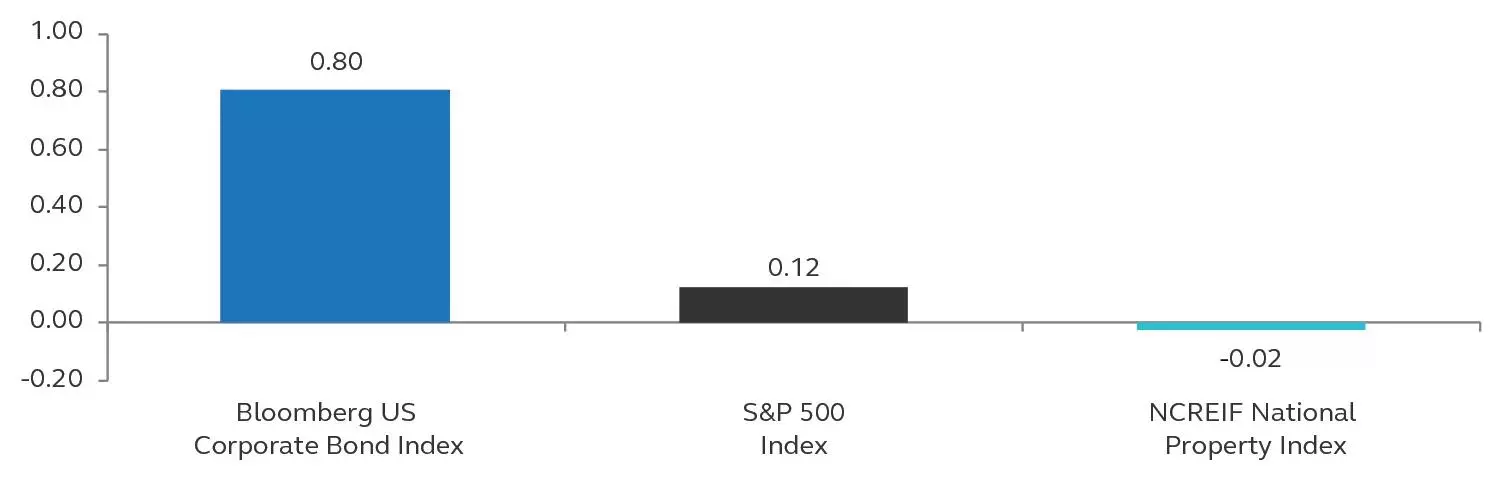

Commercial mortgages provide correlation benefits with other asset classes used by institutional investors. The price appreciation of various fixed income asset classes is driven largely by interest rate levels. To gauge the excess value provided by commercial mortgage investments over bond investments, the primary focus should be on spread differentials and credit loss expectations. However, it is interesting to note that the total returns of these fixed income asset classes are not perfectly correlated (only a 0.80 correlation since the fourth quarter of 1978). Therefore, institutional investors who use core CML investments as a component of their fixed income portfolios may reap the benefits of portfolio diversification.

Exhibit 4: Correlation of quarterly total returns - Giliberto-Levy Commercial Mortgage Performance Index vs. other indices

Q4 1978 through Q2 2023

{kind=link}

Source: Bloomberg, S&P, NCREIF, and Giliberto-Levy, Q2 2023. The Bloomberg US Corporate Bond Index represents the investment grade U.S. corporate bond market. The S&P 500 index represents U.S. equities. The NCREIF National Property Index represents performance of commercial real estate. Please see index descriptions in the disclosure section.

Most commercial and multifamily mortgage investments feature a high degree of call protection, which reduces risk to the investor for a specific amount of time during which the borrower cannot prepay any and/or all of the principal. In the event a borrower prepays a fixed rate loan prior to the final three months of the loan term, most loans require that the borrower pay a yield maintenance prepayment premium (a so-called “make-whole”) to the lender. However, in certain instances, lenders will negotiate more flexible prepayment provisions at the time of loan origination, in exchange for a higher interest rate.

Because of the private nature of the commercial mortgage market, lenders can tailor loan terms to meet their portfolio’s average life and duration needs. Lenders may also specify investment criteria that are suited to their particular credit risk tolerance and yield requirements. For example, many life insurance companies select core senior mortgage programs as foundations to their real estate debt portfolios. Those investors who can tolerate slightly higher risk- return profiles may also consider construction lending, subordinate debt, or bridge lending strategies.

Conclusion

Commercial real estate debt appeals to many investors in today’s market environment as a potential means of enhancing yields and mitigating portfolio level risks associated with their fixed income portfolios. However, the private market nature of core commercial mortgage investments creates both challenges and opportunities for investors. Investors who take affirmative steps to overcome the challenges have the potential for a mix of strong relative value, minimal credit losses, appealing current income returns, and diversification benefits from their commercial mortgage investments. The management-intensive nature of the asset class requires specialized knowledge, expertise, and relationships with the right borrowers and intermediaries. While these may serve as material barriers to market entry, investors can select an investment advisor with the right people, tools, and relationships to help them meet their investment goals.

_______________

1 “Financial Accounts of the United States: Flow of Funds, Balance Sheets, and integrated Macroeconomic Accounts, First Quarter 2023,” Board of Governors of the Federal Reserve System.

2 “Senior Loan Officer Opinion Survey on Bank Lending Practices”, April 2023, Board of Governors of the Federal Reserve System.

3 “Mortgage Loan Portfolio Pro?le”, various editions, American Council of Life Insurers.

4 “Using Principal Real Estate’s proprietary credit risk rating system, a 60% LTV loan for a property with a highly durable cash ?ow stream and favorable property, market, and sponsor attributes might be rated A+/A. A 68% LTV loan for the same property might be rated BBB+. For illustration purpose only, not to be taken as investment advice. Proprietary model output is based upon certain assumptions that may change, are not guaranteed and should not be relied upon as a signi?cant basis for an investment decision.

5 Based on data from Standard & Poor’s, Bloomberg Barclay’s, the National Council of Real Estate Investment Fiduciaries, Giliberto-Levy, and Principal Real Estate Research. For illustration purpose only, not to be taken as investment advice. It is not possible to invest in an index. Past performance does not guarantee future returns.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Commercial And Multifamily Mortgage Loan Investments For A Fixed Income Portfolio