CMC - Commercial Metals Company Is A Stable Steel Play

2023-05-05 11:40:45 ET

Summary

- Commercial Metals Company has been able to grow revenues at a good rate over the last several years and tailwinds are suggesting this will continue.

- Deglobalization will benefit CMC as more demand is placed on companies in the US and the products they offer.

- With a strong financial position and good outlook, I will rate the company a buy.

Investment Summary

Commercial Metals Company ( CMC ) is a prominent player in the steel and metal industry, offering a wide range of products and services globally. With four primary business segments, the company caters to different areas of the market, including Americas Recycling, Americas Mills, Americas Fabrication, and International Mills. CMC's Americas Mills segment is responsible for manufacturing and selling a variety of steel products, including rebar, merchant bar, and wire rod.

With deglobalization seeming to be in play, the demand for domestic production which CMC offers I think they will continue seeing revenue increases as a result. It's one of the major tailwinds I see with them going forward in the next several years. Besides relatively steady revenue growth over the next several years, I think the healthy financial state the company is in further fuels a buy case for it.

Deglobalization Is A Tailwind

I mentioned one of the major tailwinds for the company being deglobalization. It seems more and more companies are moving production out of China and into other countries like India or Vietnam.

But besides this companies are also moving back to the US to hedge against global constraints that we saw during the pandemic. This is in the hope of having a more sleek and well-run business model that can be efficient when times are tough. It also then of course increases the demand for business within the country as the close proximity they have is a major benefit. With incentives from the government to increase spending on manufacturing in the US it seems just that is happening.

In the case of CMC the steel production in the country has also been increasing steadily in 2022 with December having a 5% increase from the production levels in November. I think this highlights the momentum in the industry. If you go of what was said in the last earnings report then this holds true also that CMC should continue seeing momentum as a result of both deglobalization and increased spending from recent bills passed. The CEO Barbara R. Smith said the following “We expect current and new industrial projects, as well as growing levels of state and federal infrastructure spending, will support CMC's North America volumes in the quarters ahead”.

Quarterly Result

In the last earnings report , I think CMC managed to perform rather well despite the tough climate we are in and steel prices falling a fair bit from the prices seen 12 months ago. Net sales only increased slightly on a yearly basis, reaching around $2 billion. But what might worry some was the EBITDA seeing an over $300 million decrease as a result of less favorable prices and margins generally taking a hit. What might construe this a little however is the gain the company had of around $273 million as they sold off some assets. With that in mind the shift doesn't seem so extreme and in fact rather seasonal as commodities go in ups and downs all the time.

{kind=link}

The company did manage to maintain a rather strong cash position as it sat at around $600 million. This could have a significant impact on the long-term debt of over $1 billion, something I value quite highly as it means the company is in a generally good financial position.

All in all, it seems the company weathered the storm quite well and I am excited to see how the coming quarters look as more and more demand will be placed on companies in the US.

Valuation & Wrap Up

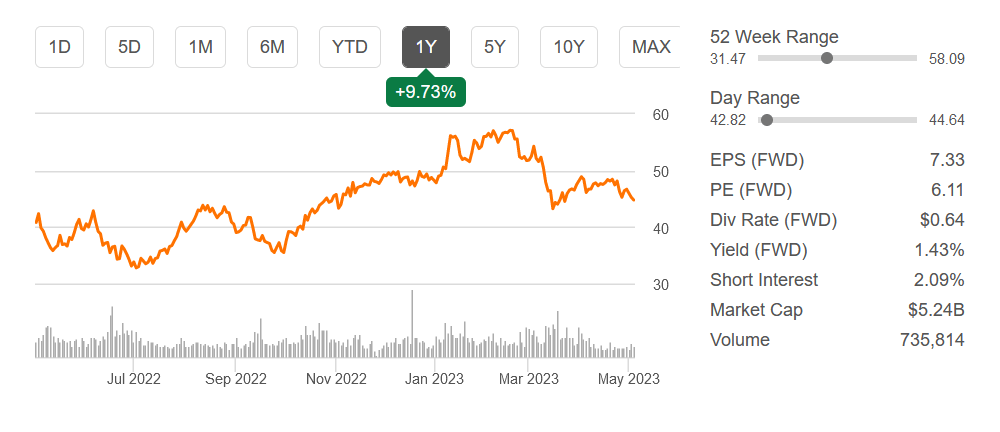

Looking at the valuation of the company it seems to be at a pretty fair price right now. With a forward p/e of just over 6, it's far under the sector's average of 13. It is however increasing slightly as analysts are expecting 2023 to perhaps be a challenging year for the company, primarily for margins.

I don't think it's out of the picture to see more margin compression for the company. But I think the long-term picture remains strong enough that short-term headwinds like that aren't enough to put down a buy case. In the meantime, you as an investor can collect a nice dividend and have your shares increase in value as the company keeps up its share buyback program.

{kind=link}

Besides this, the company sits at a net debt/EBITDA ratio of just 0.59 which is incredibly strong. This makes me think that even if margins take a turn for the worse, debt won't become an issue, and both buybacks and dividends won't be cut.

To conclude, I think CMC offers a stable growth opportunity as revenues will be fueled by an increased demand for domestic production. With a stable financial position, I think the company deserves a buy rating.

For further details see:

Commercial Metals Company Is A Stable Steel Play