CRZBF - Commerzbank: Capital Return And Fee Business Targeted In A Bid To Reach 11.5% RoTE In 2027

2023-12-15 17:17:05 ET

Summary

- In its new strategic plan, Commerzbank targets 8% RoTE in 2024, gradually improving to 11.5% in 2027.

- The bank may distribute about €1.5 billion to get to a capital position comparable with its largest competitor Deutsche Bank.

- The distribution amounts to 11.5% of Commerzbank's market capitalization and is likely to put upward pressure on the share price.

- Elevated interest rate assumptions are the main risk in Commerzbank reaching its 2027 aspirations.

- The undemanding valuation of German banks and a strong capital position make Commerzbank a buy.

Introduction

I last covered Commerzbank ( OTCPK:CRZBF ) back in a February 2023 article here , arguing it was somewhat overvalued compared to its closest peer Deutsche Bank ( DB ). In November, Commerzbank released a new medium-term plan covering the 2024-2027 period (available here ). As a result, in this article, I will provide an update on the bank's plans and see how it stacks up against its crosstown rival DB.

The new strategic plan

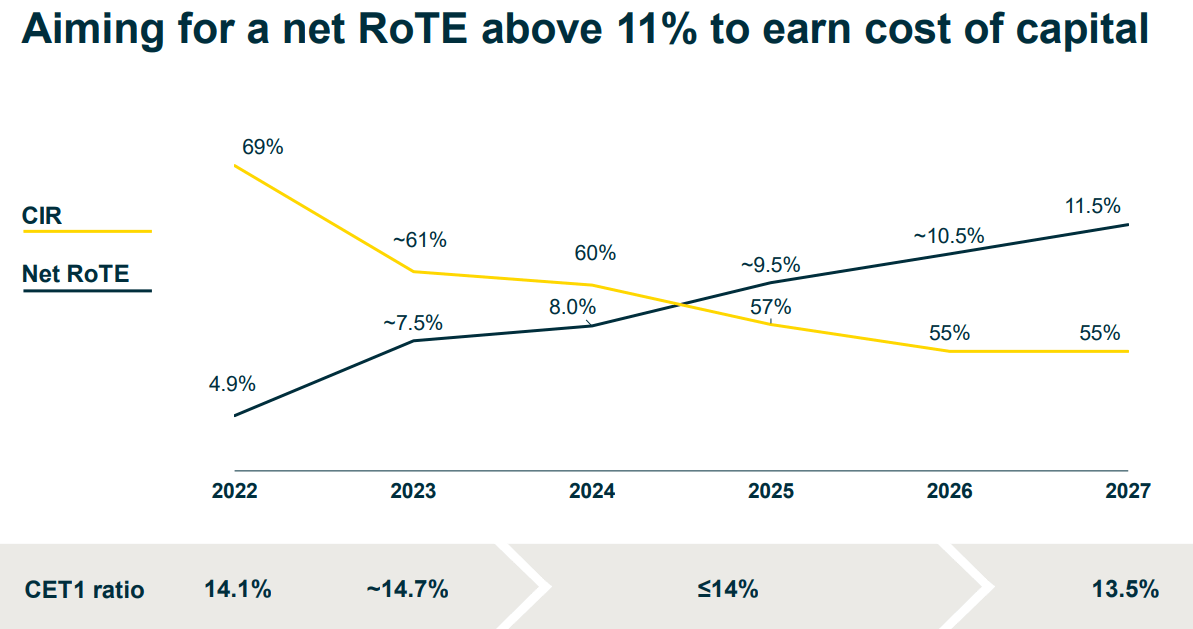

Commerzbank has set itself very ambitious goals in the new strategic plan, with RoTE growing gradually throughout the period:

- 7.5% in 2023

- 8% in 2024

- 9.5% in 2025

- 10.5% in 2026

- 11.5% in 2027

RoTE, CIR and CET1 targets (Commerzbank 2024-2027 Strategic Plan)

{kind=link}

A good portion of the plan actually depends on the return of excess capital to shareholders (i.e. changing the denominator in the RoTE equation). Case in point, the 7.5% RoTE estimate in 2023 is against a CET1 ratio of roughly 14.7%. If the CET1 ratio were at the targeted level of 13.5% in 2027, the RoTE in 2023 would be 8.2%.

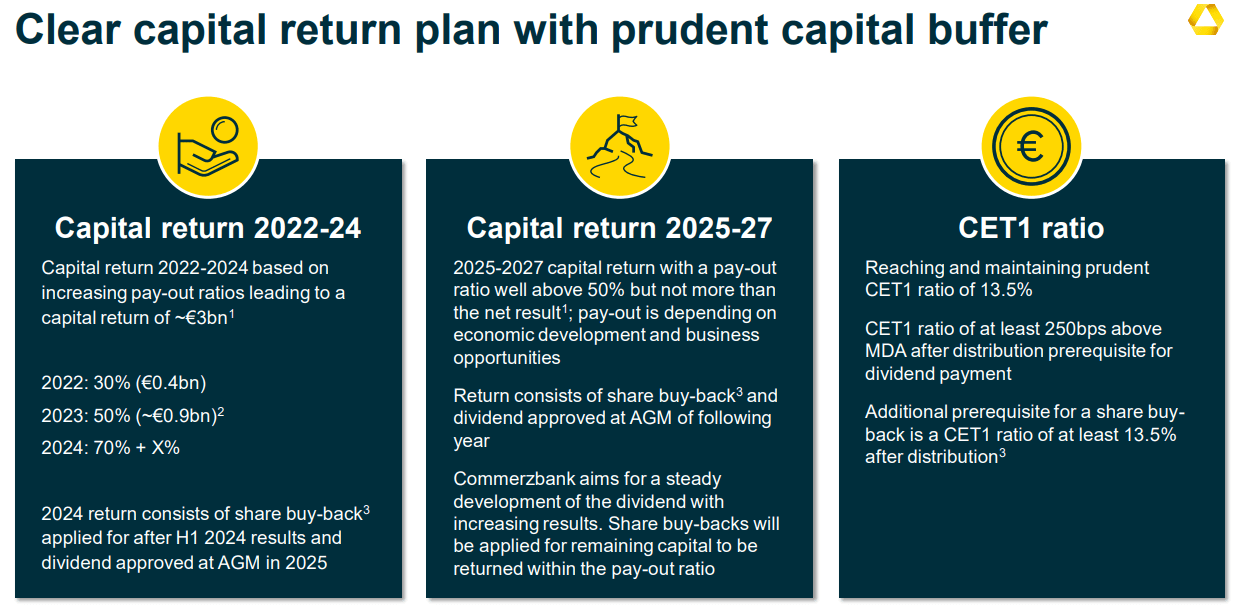

To achieve the lower CET1 capital level, the bank targets a payout of at least 70% in 2024, with a share buyback application to the ECB targeted after the H1 2024 results:

{kind=link}

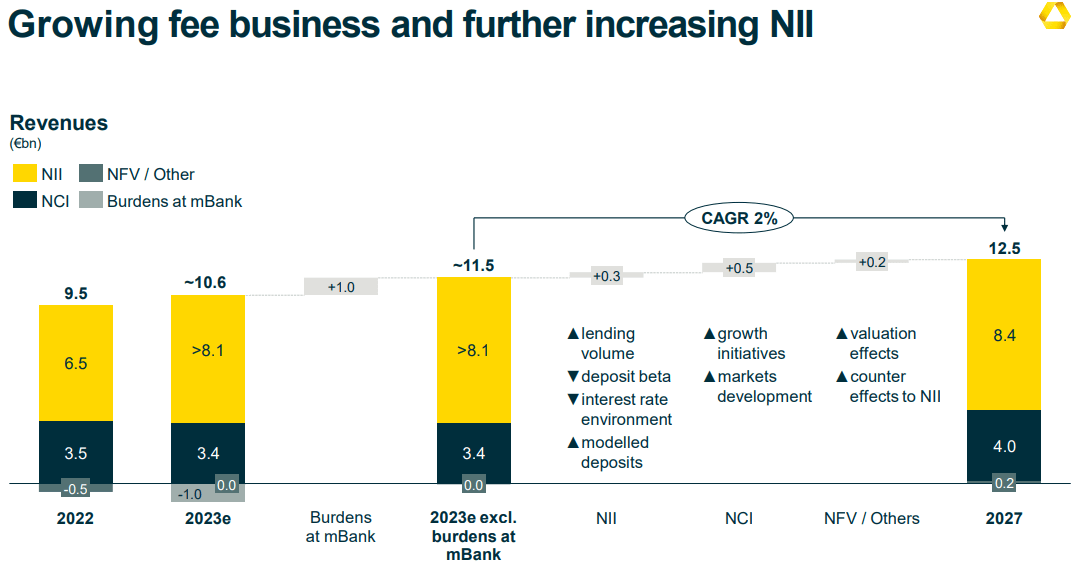

To achieve the remaining growth in RoTE, from pro-forma 8.2% in 2023 with a CET1 of 13.5% (as shown above) to a RoTE of 11.5% in 2027, the bank targets a slight growth in net interest income and 3-4% compound annual growth in fee income:

Revenue expectations 2024-2027 (Commerzbank 2024-2027 Strategic Plan)

{kind=link}

Indeed, from the graph above we can see that roughly half of the €1 billion growth in revenue, from €11.5 billion in 2023 (excluding burdens at Polish subsidiary mBank) to €12.5 billion in 2027, is set to come from higher net commission income ((NCI)).

Capital return effects on tangible book value

Commerzbank's Q3 results presentation is available here . To evaluate the effect of capital return, I will compare Commerzbank's surplus capital position to DB, as shown in the table below:

| Commerzbank |

| Deutsche Bank |

| CET1 Capital Q3 2023 |

| 14.60% |

| 13.94% |

| MDA Requirement 2024 |

| 10.27% |

| 11.16% |

| CET1 Surplus |

| 433 bps |

| 278 bps |

| Tangible book per share Q3 2023 |

| € 21.45 |

| € 27.74 |

| Price/Tangible book |

| 0.49 |

| 0.44 |

Source: Author calculations based on company disclosures

From the table above, we can see that Commerzbank has a roughly 66 basis point surplus relative to DB when it comes to absolute CET 1 capital. Furthermore, due to its lower CET1 requirement, the regulatory surplus is some 155 basis points.

What's more, Commerzbank is applying a 50% payout ratio for 2023, compared to roughly 30% for DB.

At the end of Q3 2023, Commerzbank had a CET1 capital of €25.4 billion. The graph below shows the potential distributions for Commerzbank:

| Type of distribution |

| 66 bps absolute capital surplus |

| € 1.15 billion |

| 155 bps regulatory capital surplus |

| € 2.7 billion |

| 20% difference in payout ratio 2023 |

| € 360 million |

Source: Author calculations based on company disclosures

For the purposes of comparison, I will only use the 66 basis point absolute capital surplus and the 20% higher payout in 2023, while the 155 basis point regulatory capital surplus is a theoretically possible payout scenario but unlikely in my view.

As a result, it is fair to assume that Commerzbank will distribute around €1.5 billion to get to a capital position on par with Deutsche bank. Here is how the capital position table evolves after a distribution at the current price-to-tangible book ratio.

| Commerzbank |

| Deutsche Bank |

| Pro-forma CET1 capital after distribution |

| 13.94% |

| 13.94% |

| Pro-forma tangible book after distribution |

| € 22.71 |

| € 27.74 |

| Pro-forma Price/Tangible book |

| 0.46 |

| 0.44 |

Source: Author calculations based on company disclosures

From the calculation above we see that the tangible book value of Commerzbank should increase by about €1.26/share to €22.71/share as a result of the potential distribution at the current 0.49 price-to-tangible book ratio.

We can also observe that the two banks are almost identically valued from a Price/Tangible perspective, leaving profitability to determine which is the better pick at the moment. On the one hand, Commerzbank targets a slightly lower profitability of 9.5% in 2025 compared to 10% at DB. On the other hand, Commerzbank has a lower capital requirement which makes its shareholder distributions more certain.

All in all, DB seems slightly more attractive from a valuation perspective, largely due to a higher profitability and a larger tangible book discount, especially if price rises in Commerzbank's share price limit the accretive effects of its buyback.

Nevertheless, I reckon Commerzbank is a buy due to the significant upward pressure on the share price from share buybacks and dividends (the €1.5 billion distribution amounts to 11.5% of Commerzbank's market capitalisation), coupled with undemanding absolute valuation of both German banks.

Risks and Assumptions

The main controversial assumption in the 2024-2027 plan is that the ECB deposit rate remains at 4% in 2024 and 2025, before declining to 3.3% in 2027:

Interest rate assumptions (Commerzbank 2024-2027 Strategic Plan)

While the future path of interest rates is highly uncertain, chances are the ECB cuts rates as early as 2024.

Conclusion

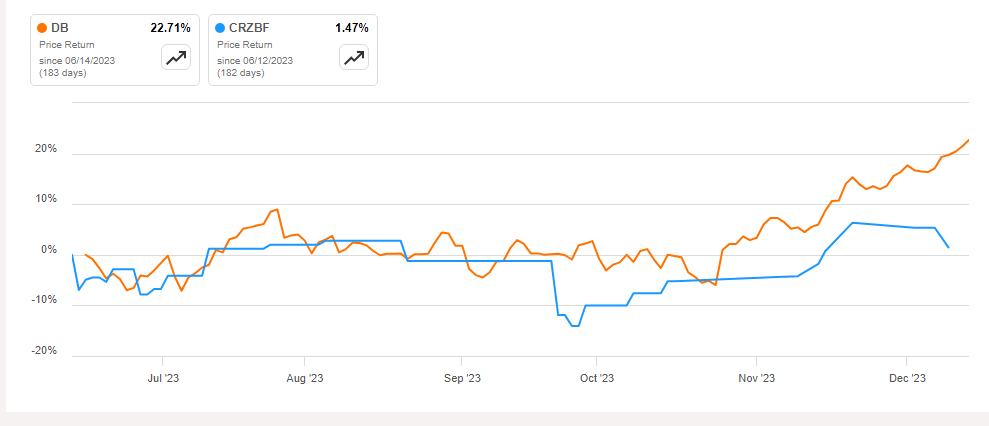

Commerzbank has underperformed its largest competitor DB in recent months:

{kind=link}

As a result, while DB is still marginally more attractive from a profitability perspective, I reckon Commerzbank's higher absolute and relative capital position, plus aggressive capital return plans, coupled with undemanding valuation of both banks, warrant a buy rating on Commerzbank. The main risk for Commerzbank is that the ECB cuts rates at a rapid pace in 2024 and 2025, undermining the bank's net interest income, on which it is more reliant compared to DB.

Thank you for reading.

For further details see:

Commerzbank: Capital Return And Fee Business Targeted In A Bid To Reach 11.5% RoTE In 2027