CRZBF - Commerzbank: Walking The Recession Tightrope

Summary

- 28.9% Y/Y underlying revenue growth in Q4, driven by PSBC (+56.1%). 18% Y/Y growth in 2022.

- CET1 of 14.14%, some 4% above pro-forma MDA requirement after expected increases in 2023. 30% Payout in 2022, increased to 50% in 2023.

- Net interest income seen up 0.2-0.8 billion EUR in 2023. Costs targeted 0.2 billion EUR lower.

- I see ROTE of at least 6% in 2023. On track to achieve >7.3% in 2024, with room for further branch optimization.

- Main competitor, Deutsche Bank, shares have lagged Commerzbank substantially, even adjusted for capital surplus. I am more neutral on Commerzbank until the gap closes.

Company Overview

Commerzbank (CRZBF) operates in two main divisions - Private and Small Business Customers ((PSBC)) at 61.6 % of underlying Q4 2022 revenues, of which Polish majority-owned (69.3% Commerzbank stake) subsidiary mBank accounted for 17.6% of underlying Q4 2022 revenues while PSBC Germany made up 44% of underlying Q4 2022 revenues , and Corporate Clients ((CC)) at about 41.4% of underlying Q4 2022 revenues. Totals do not equal 100% due to eliminations/consolidation and group functions.

Operational Overview

Private and Small Business Customers delivered a stunning 56.1% Y/Y underlying revenue growth in Q4, well ahead of the 17.9% 2022 growth rate. Operating return on tangible equity was 18.3% in the quarter, ahead of the 14% for the full year.

The operating return on tangible equity varies over the year as it is not adjusted for compulsory contributions (bank levies) which are primarily in Q1 of each year.

Corporate Clients saw 27% Y/Y underlying revenue growth in Q4, slightly ahead of the 22.8% 2022 growth rate. Operating return on tangible equity was 7.7% in Q4, below the 9.8% achieved for 2022.

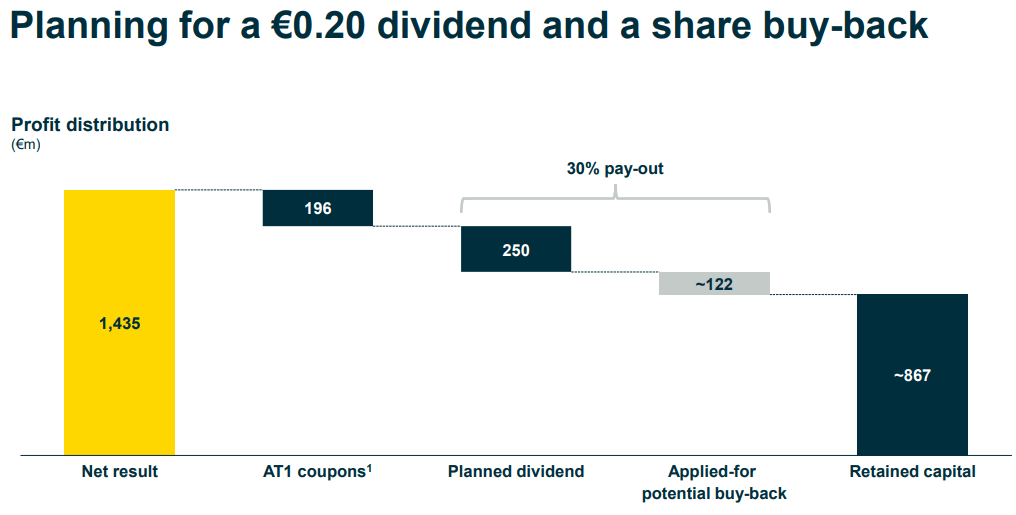

On a consolidated basis, underlying revenues grew 28.9% Y/Y in Q4 and 18% for the full year. Net return on tangible equity was 6.7% in Q4 and 4.9% for 2022. Cost of risk was 17 basis points in 2022, ahead of the 12 bps in 2021. Tangible book per share increased by 0.08 EUR/share Q/Q to 20.28 EUR/share. The Cost/Income ratio was 69% in 2022. The majority of the profit was retained, with a 0.20 EUR/share dividend proposed and a 122 million EUR buyback, for a total payout of 30%:

{kind=link}

Capital Position

The bank further solidified its CET1 capital to 14.14%, up 30 bps Q/Q. The maximum distributable amount requirement (MDA) is set to increase by circa 61 bps in 2023 to about 10.1%, from 9.48% currently. Thus the pro-forma MDA buffer is about 4%.

Having made good progress on its restructuring so far, Commerzbank plans to increase the payout ratio from 30% in 2022 to 50% of profit in 2023.

Quantifying the Capital Surplus

Largest competitor Deutsche Bank ( DB ) expects its MDA requirement to increase to about 11.2 % in 2023. With a CET1 of 13.4% DB therefore is sitting on a pro-forma MDA buffer of about 2.2%.

With its 4% pro-forma MDA buffer, Commerzbank has a 1.8% MDA buffer surplus relative to DB, which can be used for a variety of corporate purposes. For the sake of comparison, I will compute the theoretical effect from Commerzbank deploying its surplus capital on share buybacks.

As of the end of Q4 2022, Commerzbank had CET1 capital of 23.9 billion EUR. The 1.8% surplus therefore represents some 3.04 billion EUR in capital. With a current price/tangible book of about 0.56 the theoretical buyback can create some 2.39 billion EUR in book value.

This would increase the tangible book by about 1.91 EUR/share to 22.19 EUR/share. In that unlikely scenario (it will be quite difficult for the bank to repurchase so much at the current price, setting aside the regulatory and risk hurdles in such an operation) the price/tangible book would improve to about 0.51, still above the 0.44 at Deutsche bank.

All in all, Commerzbank is far safer than DB in the current recessionary environment, but strong price gains have eroded the accretive impact of potential buybacks.

Outlook 2023

The prospects for 2023 are great for Commerzbank, especially on the net interest income ((NII)) front:

{kind=link}

From 6.3 billion EUR in 2022, NII is set to increase to at least 6.5 billion EUR, perhaps even as high as 7.1 billion EUR.

Risk result seen at below 900 million EUR (2022: 876 million EUR) assuming usage of top level adjustments (482 million EUR remaining). These adjustments are provisions for credit losses made by management on a discretionary basis, rather than predicated by actual loan losses.

CET1 seen at around 14%.

Expenses targeted at 6.3 billion EUR (2022: 6.5 billion EUR), however shifting towards a cost/income (C/I) ratio target. For 2024 the C/I target is 60%.

All in all, in 2023 pre-tax income should improve by at least 0.4 billion EUR or 20% (in 2022 pre-tax profit was 2 billion EUR). This should boost the bank's profit by close to 0.3 billion EUR with a ROTE of at least 6% in 2023.

Investment Thesis

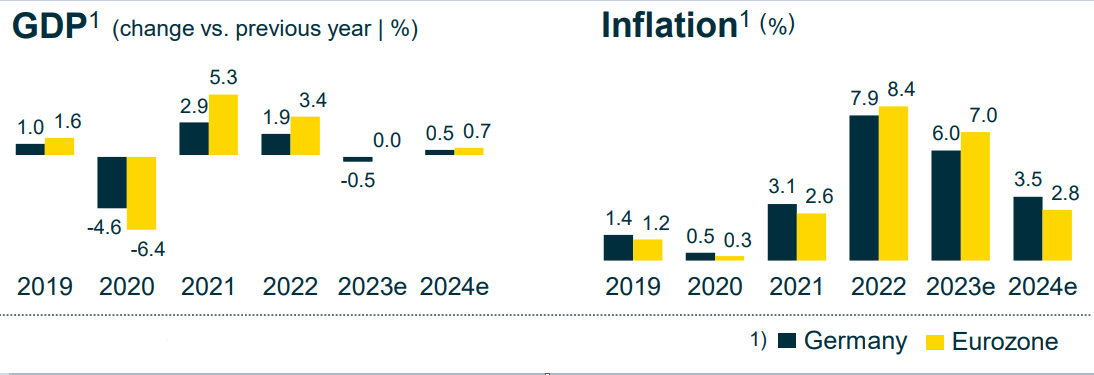

Commerzbank still expects a mild recession Germany in 2023 (-0.5%), with weak growth in 2024 (+0.5%):

{kind=link}

The bank is in a comfortable position to weather the downturn and plans to increase shareholder distributions. However significant outperformance relative to largest domestic peer Deutsche Bank clouds the share price outlook over the immediate future.

Over the long term I would expect Deutsche Bank's relative valuation to improve, which should open the way for further gains at Commerzbank. Furthermore, there is room for additional operational improvement at Commerzbank. The bank ended 2020 with 800 domestic locations (bank branches) and has already cut their number to 450 as of 2022. The new target for 2023 is 400. For comparison, ABN AMRO (AAVMY) operates with 27 bank offices. While the Netherlands has a population some 5 times smaller than Germany, even counting branches in Poland, it is safe to say Commerzbank can cut domestic locations to 150-200 in the coming years.

Commerzbank is making progress on its ROTE target of at least 7.3% for 2024. The strong capital position will shield the bank even in an adverse recessionary outcome. While I see more limited upside in the immediate future, the exit from negative rates in the eurozone has been a gamechanger. Therefore I think the bank is a hold for the medium term and a buy in the long term. I look forward to the bank updating its post-2024 targets.

Thank you for reading.

For further details see:

Commerzbank: Walking The Recession Tightrope