DBC - Commodities (PDBC GSG): Don't Miss The Forest For The Trees

- SPX has seen record negativity (since 2020) last week: Worst back-to-back days, 3 consecutive days of <-1%, 47th day of <2% for the year.

- At the same time, inflation isn't showing any sign of easing, and the Fed is being forced to hike fast and furious; a 75bps hike this week is definitely possible.

- Consumer sentiment is at an all-time low, yield-curve is about to invert (again), and the probability for a recession is now high.

- If there's something strange in your neighborhood. Who you gonna call? Commodities!

- If there's something weird, and it don't look good. Who you gonna call? Commodities!

[ Please note that the bulk of this article was first published on June 13th for subscribers of Macro Trading Factory ("MTF") , as part of our weekly macro/market review. Therefore, whenever there's a reference to time, please have that date in mind]

Prologue

2022 is a rough year for both stocks and bonds.

The S&P 500 is en-route towards the worst first half performance in 90 years.

Deutsche Bank

The aggregate return of stocks (measured by MSCI All-Country World Index) and bonds (measured by Bloomberg Global Bonds Index) is the worst in at least 35 years.

Bloomberg

Correlation between stocks and bonds has turned positive again, meaning that both asset classes tend to lose (or gain) in tandem.

The Fed clearly is determined to fight inflation and Powell doesn't seem like he intends to come for rescue anytime soon.

It's no wonder then that the question many investors are asking themselves these days is where to put their money? Is it smart to keep pushing money into the traditional, most popular, asset classes, or should they look somewhere else?

Bloomberg

Last week we already revealed an area (within the stock market) that we like.

In this article, however, we're putting a spotlight on Commodities, an asset class of its own that you can invest in through stocks, bonds, or ETFs.

You may buy either operating entities/businesses that benefit from higher commodity prices, or focus on commodity prices themselves.

YTD Performance

Charles Schwab

- Only one sector is up - Energy ( XLE )

- Four sectors are down more than 20%: Real Estate ( XLRE ), Technology ( XLK ), Communication Services ( XLC ) and Consumer Discretionary ( XLY )

Charles Schwab

For the first time since March 2020, the S&P 500 was down at least 1% for 3 consecutive days.

The index hasn't been down (at least 1%) 4 in a row since Dec. 2018, but looking at SPX futures right now, we are due to make another (small/negative) history today.

Bloomberg

This market-breadth table doesn't include this morning’s pre-market action:

Charles Schwab

13 Years A Tech Bull

Nasdaq 100 ( NDX ) Annual Total Returns (since GFC):

- 2009: +55%

- 2010: +20%

- 2011: +4%

- 2012: +18%

- 2013: +37%

- 2014: +19%

- 2015: +10%

- 2016: +7%

- 2017: +33%

- 2018: +0.04%

- 2019: +39%

- 2020: +49%

- 2021: +27%

- 2022 YTD: -27%

If you think Tech is having a rough year, take a look at Retail.

MSCI World Retail Index is headed for its first annual drop since 2008.

Bloomberg

While Nasdaq 100 components slammed this past week...

Yahoo Finance

... Chinese stocks were holding up nicely.

Yahoo Finance

Inflation: Out of Control

CPI at +8.6% Y/Y is the highest inflation the US has seen in 41 years.

True Insights

The average US gasoline price crossed $5/gallon last week; up 52% YTD.

True Insights

Average of utility costs, gasoline, food at home, and electricity components of May CPI inflation surged by 25.7% Y/Y (just slightly off the peak in 1980).

Charles Schwab

Pygmalion Effect

Following a couple of months in which inflation expectations have eased, they are on the rise again.

Saxo

According to the University of Michigan sentiment survey , inflation expectations for the next 5-10 years have gone up in May to 3.3% (from 3% in April).

That's not only the highest level since 2008, but it's also a worrying sign because expectations usually determine outcome. If consumers now think that inflation is getting out of control - they will adjust consumption/savings accordingly.

The Daily Shot

Jefferies: “In order to re-anchor inflation expectations, Jefferies expects the Fed to lift 75bp at this week’s FOMC.”

Inversion, Again

US Treasury 2-year yield is at its highest level since 2007.

Bloomberg

The US yield-curve is about to invert again.

US Treasury 10-2 year yield spread is just a hair (1bps) from inverting.

The Daily Shot

Reminder: In many cases, an inversion is the promo for a recession.

The last two times consumer credit growth accelerated alongside collapsing sentiment? 2000 and 2008.

Bloomberg

Deutsche Bank strategists, who are among the most bearish on the economic outlook, now see a peak Fed funds rate of 4.125% in mid-2023.

If they're correct, we expect the entire yield-curve to invert.

Fortune Telling

The good news is that we already know (with a very high degree of certainty) how this tightening cycle is going to end.

BofA

The bad news is that a recession is very likely part of the near-future path.

Compound

Earnings

US companies are warning of earnings misses at a historically high rate and there are signs that the pace could accelerate, but Wall Street analysts don't seem to be listening too closely, yet.

SPX is expected to report Y/Y earnings growth of 4.0% for Q2 2022, which would be the lowest growth since Q4 2020 (3.8%).

FactSet

Dollar strength often leads to a global corporate earnings contraction, and the current inflation adds more pressure to profit margins that are due to squeeze.

The Fed remains the Fed, and Powell remains Powell, so you can count on the "soft landing" narrative to turn into the same old "transitory"/"nobody could see a recession coming" nonsense in no time.

Crescat Capital

Even those who are making record profits are doing so while taking much more risk.

Trafigura, the giant commodity-trading house, posted its highest-ever net income ($2.7B) for the first half of any fiscal year.

That's great, but when you see how much more (value-at-) risk the company took in order to get to this result you understand how tough it's to make money these days, even within the most lucrative areas (commodities), without taking an enormous risk.

Bloomberg

Heading South

High yield corporate bonds tend to be terribly sensitive to liquidity. They tell us when the conditions are great for stocks, and more importantly they tell us when liquidity is in short supply.

MFP

RBC's Lori Calvasina : If this year's 3900 low on the S&P gets broken and the index then dips under 3,850, "we see potential downside in the S&P 500 to a little over 3,200. That would represent a 32% drawdown in the S&P 500 from the early January 2022 high"

Contrary to the bearish views, Ned Davis Research actually expects the second half of 2022 to be way better.

NDR

Only time will tell, but looking at the chart, the SPX is trading way closer to the lower band (than to the upper band) of the (red-lines) channel, and the trend (orange-lines) points to further weakness.

Y-Charts, Author

We would be surprised if the index won't test the lower end (~3800) soon, and frankly - we don't see any level of support before previous highs (shortly before or after the pandemic erupted), or even lower (~3200).

Y-Charts, Author

Another leg of 10%, even 20% (which would take us to 3120.69), down can't be ruled out and the main problem of this market is that no matter how small (or big) the downside risk is, it's the lack of upside potential that prevents us from turning bullish.

No Refuge

- Everything but Energy ( XLE ) is down this year.

- Everything but Energy and Utilities ( XLU ) is down more than 10%.

- Consumer Discretionary ( XLY ) and Real Estate ( XLRE ) are down over 30%.

Having said that, the place to be in is Commodities.

You get a protection against the risks of inflation, supply-chain disruptions, food protectionism, and geo-political/cross-border tensions/tariffs.

As we always say: Macro Trumps Micro!

Reading the market/book (as a whole) correctly is way more important than picking the (exact) right stock/page.

True Insights

Can this be a protection against a recession? Unlikely, but it surely is a better and safer place to be than growth/tech stocks that provide a protection against nothing these days.

Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF ( PDBC )

PDBC focuses on commodity prices, not commodity-related businesses. As such, there are no periodical earnings reports, financial statements, or all sorts of valuations/metrics related to a single stock of an operating company.

The ETF invests in derivatives across the various segments of the Commodities arena (Energy, Agriculture, Precious Metals, Base Metals)

Per the fund's manager , PDBC "seeks to achieve its investment objective by investing in commodity-linked futures and other financial instruments that provide economic exposure to a diverse group of the world's most heavily traded commodities. The Fund seeks to provide long-term capital appreciation using an investment strategy designed to exceed the performance of DBIQ Optimum Yield Diversified Commodity Index Excess Return™ (DBIQ Opt Yield Diversified Comm Index ER) (Benchmark), an index composed of futures contracts on 14 heavily traded commodities across the energy, precious metals, industrial metals and agriculture sectors."

Here are the fund's holdings as of 06/20/2022:

| SECTOR TOTAL | COMMON NAME | NAME | CONTRACTEXPIRY DATE | % OF NET ASSETS |

|---|---|---|---|---|

| SWAP77.40% | ||||

| TRS | ||||

| Pay RBC ENHANCED PS01 ER RBCAPS01 RBC_US_DVPS 7/5/2022 | ||||

| 07/05/2022 | ||||

| 16.73 | ||||

| TRS | ||||

| Pay MACQUARIE INDEX MQCP322E MQCP322E MACQ_US_DVPS 7/5/2022 | ||||

| 07/05/2022 | ||||

| 15.69 | ||||

| TRS | ||||

| Pay MORGAN STANLEY MSCYIZ01 MSCYIZ01 MORG_US_DVPS 7/5/2022 | ||||

| 07/05/2022 | ||||

| 14.12 | ||||

| TRS | ||||

| Pay MANAGED COMMODITY STRATEGY GSEBA001 GSEBA001 GOLD_US_DVPS 7/5/2022 | ||||

| 07/05/2022 | ||||

| 11.50 | ||||

| TRS | ||||

| Pay BOFA MERRILL LYNCH COMMODITY MLBXIVMB EXCESS RETURN STRATEGY MLBXIVMB BAML_US_DVPS 6/6/2022 | ||||

| 06/06/2022 | ||||

| 10.98 | ||||

| TRS | ||||

| Pay CB CIXBICPI CITI_US_DVPS 7/5/2022 | ||||

| 07/05/2022 | ||||

| 8.37 | ||||

| Energy14.28% | ||||

| NY Harbor ULSD | ||||

| NYMEX NY Harbor ULSD Futures | ||||

| 08/31/2022 | ||||

| 4.16 | ||||

| Gasoline | ||||

| NYMEX Reformulated Gasoline Blendstock for Oxygen Blending R | ||||

| 11/30/2022 | ||||

| 3.39 | ||||

| WTI Crude | ||||

| NYMEX Light Sweet Crude Oil Future | ||||

| 11/21/2022 | ||||

| 2.66 | ||||

| Brent Crude | ||||

| ICE Brent Crude Oil Future | ||||

| 09/30/2022 | ||||

| 2.45 | ||||

| Natural Gas | ||||

| NYMEX Henry Hub Natural Gas Futures | ||||

| 04/26/2023 | ||||

| 1.62 | ||||

| Precious Metals1.62% | ||||

| Gold | ||||

| COMEX Gold 100 Troy Ounces Future | ||||

| 08/29/2022 | ||||

| 1.34 | ||||

| Silver | ||||

| COMEX Silver Future | ||||

| 09/28/2022 | ||||

| 0.28 | ||||

| Agriculture4.59% | ||||

| Corn | ||||

| CBOT Corn Future | ||||

| 09/14/2022 | ||||

| 1.27 | ||||

| Soybeans | ||||

| CBOT Soybean Future | ||||

| 11/14/2022 | ||||

| 1.20 | ||||

| Wheat | ||||

| CBOT Wheat Future | ||||

| 07/14/2023 | ||||

| 1.19 | ||||

| Sugar | ||||

| NYBOT CSC Number 11 World Sugar Future | ||||

| 09/30/2022 | ||||

| 0.93 | ||||

| Base Metals2.10% | ||||

| Zinc | ||||

| LME Zinc Future | ||||

| 08/15/2022 | ||||

| 0.77 | ||||

| Aluminium | ||||

| LME Primary Aluminum Future | ||||

| 12/19/2022 | ||||

| 0.68 | ||||

| Copper | ||||

| LME Copper Future | ||||

| 12/19/2022 | ||||

| 0.65 | ||||

| Collateral100.10% | ||||

| Invesco Government & Agency Portfolio | ||||

| AGPXX | ||||

| 33.85 | ||||

| Invesco US Dollar Liquidity Portfolio | ||||

| STUSDIC | ||||

| 18.55 | ||||

| United States Treasury Bill | ||||

| 11/25/2022 | ||||

| 26.27 | ||||

| United States Treasury Bill | ||||

| 09/29/2022 | ||||

| 5.28 | ||||

| United States Treasury Bill | ||||

| 08/18/2022 | ||||

| 3.81 | ||||

| United States Treasury Bill | ||||

| 07/28/2022 | ||||

| 3.18 | ||||

| United States Treasury Bill- When Issued | ||||

| 10/27/2022 | ||||

| 3.16 | ||||

| United States Treasury Bill | ||||

| 12/08/2022 | ||||

| 3.15 | ||||

| United States Treasury Bill | ||||

| 07/21/2022 | ||||

| 1.32 | ||||

| United States Treasury Bill | ||||

| 10/20/2022 | ||||

| 1.32 | ||||

| Cash/Receivables/Payables | ||||

| -CASH- | ||||

| 0.21 |

As you can see below, the price of PDBC did fall off the up-trending channel (green lines) and it's now trading inside the "buy zone" (red box), slightly below the 50-DMA and over 3% above the 200-DMA.

Y-Charts, Author

We would like to see PDBC moving back into the channel, which would also mean breaking-up the 50-DMA again.

That would be marking that the longer-term bullish cycle remains intact.

iShares S&P GSCI Commodity-Indexed Trust ( GSG )

Like PDBC, GSG focuses on commodity prices, not commodity-related operations.

Per the fund's manager , GSG "seeks to track the results of a fully collateralized investment in futures contracts on an index composed of a diversified group of commodities futures."

GSG is more "lazy" than PDBC. The fund is only trading futures on its benchmark - S&P GSCI Total Return Index - and not on specific commodities, as PDBC does.

Perhaps this is the reason that since both funds are available, PDBC has outperformed GSG significantly, with the gap getting wider and wider as time goes by.

Y-Charts

As you can see below, the price of GSG did fall off (though only slightly) the up-trending channel (green lines) and ~1.3% below the 50-DMA.

Nonetheless, it's still trading above the short-term support (red line), and comfortably above the 200-DMA, suggesting the bull move is still very much alive.

Y-Charts, Author

Epilogue

A new commodity bullish cycle started 26 months ago.

During the first 20 months, stocks managed to keep up pace and stay within a reasonable distance from commodities.

However, over the past 6 months, we're witnessing a significant divergence. While the "Commodity Boom" continues, and even accelerated along 2022, stocks are heading south.

Y-Charts, Author

It's funny to see people looking at the still-very-young commodity bull market and ask questions that are completely driven by their own positioning.

Those who are still out wonder whether they've already missed it? Is it too late to jump in?

And those who got in early wonder whether they should already get out? Has the commodity bull market already ended?

Bloomberg

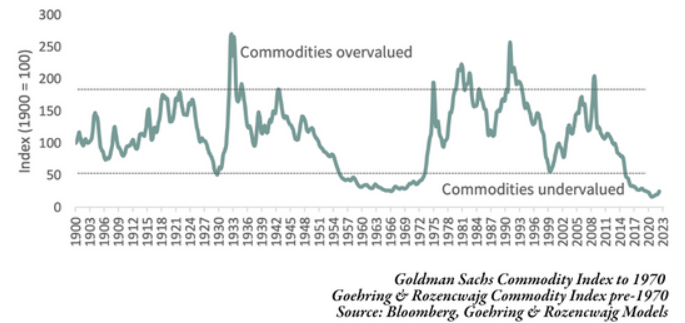

Taking into consideration the jump in many commodity markets over the past 26 months, it is only natural to ask such questions. Nonetheless, the answer to all these questions - no matter on which side of the commodity aisle you stand - is simple: Not only is the current cycle not over, it has barely begun.

{kind=link}

Can we guarantee that the next 26 months will look like the previous 26 months? No, we can't.

Can we promise that Commodities will deliver superior returns (compared to other asset classes) going forward? No, we can't.

But do we feel that this commodity bull market is only in its early stage? Yes, we do.

Incrementum

Don't miss the forest (long-term cycle) for the trees (trough; 26 months ago)!

For further details see:

Commodities (PDBC, GSG): Don't Miss The Forest For The Trees