CBU - Community Bank System: There Are Better Prospects To Consider At This Time

2023-09-18 04:14:10 ET

Summary

- Community Bank System has not experienced a significant recovery since the banking crisis, with shares still down 28.7% from where they were before the crisis.

- The company offers a wide array of services, including traditional banking, employee benefit trust, retirement plan administration, wealth management, and insurance.

- The company's deposits have recently fallen and shares look pricey compared to what else is out there.

Earlier this year, in response to the banking crisis, a number of financial institutions experienced significant downside. Some have posted sizable recoveries and others have still languished. To some investors, buying into the banks that have not really recovered much could make sense, particularly if you hope for a rebound. While I believe this strategy will work out for some banks, I also believe that others that declined we'll continue to underperform for the foreseeable future. One firm that fits into this latter category is Community Bank System ( CBU ). From the end of February through today, units are down 28.7%. However, at the bottom, they were down 31%. This means that, in the months that followed the banking crisis, shareholders have seen virtually nothing in the way of a recovery. In the grand scheme of things, shares are not priced all that bad. In addition, the company has very limited exposure to uninsured deposits. However, the stock is more expensive than many of the other banks that I have looked at and deposits fell in the second quarter of this year. Given these factors, I wouldn't go so far as to rate the bank a ‘sell’, but I would argue that a ‘hold’ rating is appropriate.

Dissecting Community Bank System

Since its founding in 1983, Community Bank System has grown into a rather sizable bank. The company has a $2.36 billion market capitalization as of this writing and, as of the end of its 2022 fiscal year, it boasted 203 full-service branches and 13 drive-thru only locations spread across 42 counties in upstate New York, 6 counties in northeastern Pennsylvania, 12 counties in Vermont, and a single county in western Massachusetts. Through these locations, the institution provides customers a wide array of services. Primarily, it focuses on traditional regional banking activities such as accepting deposits, originating loans, and more. It even does some of these activities through its digital banking operations.

Outside of this, Community Bank System has its hands and other activities as well. For instance, it operates a national practice that provides employee benefit trust, collective investment fund, retirement plan administration, and other related activities such as welfare consulting services and health consulting services, to its customers across the US and Puerto Rico. For some clients, it even offers wealth management services that consist of selling advisory products, on top of getting customers invested in various securities like stocks and bonds. And finally, the company also offers up insurance services, including both personal and commercial lines of insurance, on top of other risk management products and services, to its customers.

{kind=link}

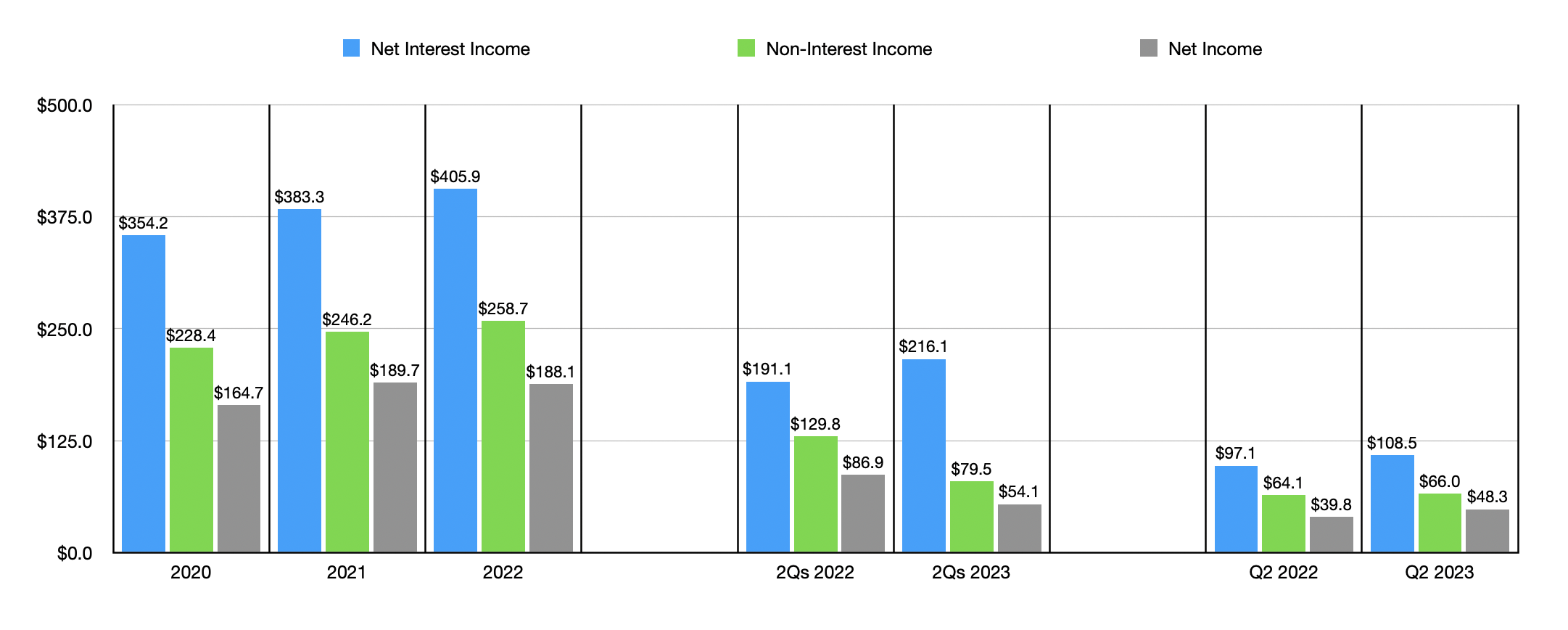

Over the past few fiscal years, management has done a solid job of growing the company's top and bottom lines. Between 2020 and 2022, net interest income expanded from $354.2 million to $405.9 million. Non-interest income also grew, climbing from $228.4 million to $258.7 million. These factors, combined, allowed net income to grow from $164.7 million to $188.1 million. As you can see in the chart above, performance has largely continued to grow into the current fiscal year. The one exception is net income for the second half of this year relative to the same time last year. But that was driven by a $52.3 million loss on the sale of investment securities. So although painful, it should be viewed as a one-time thing.

{kind=link}

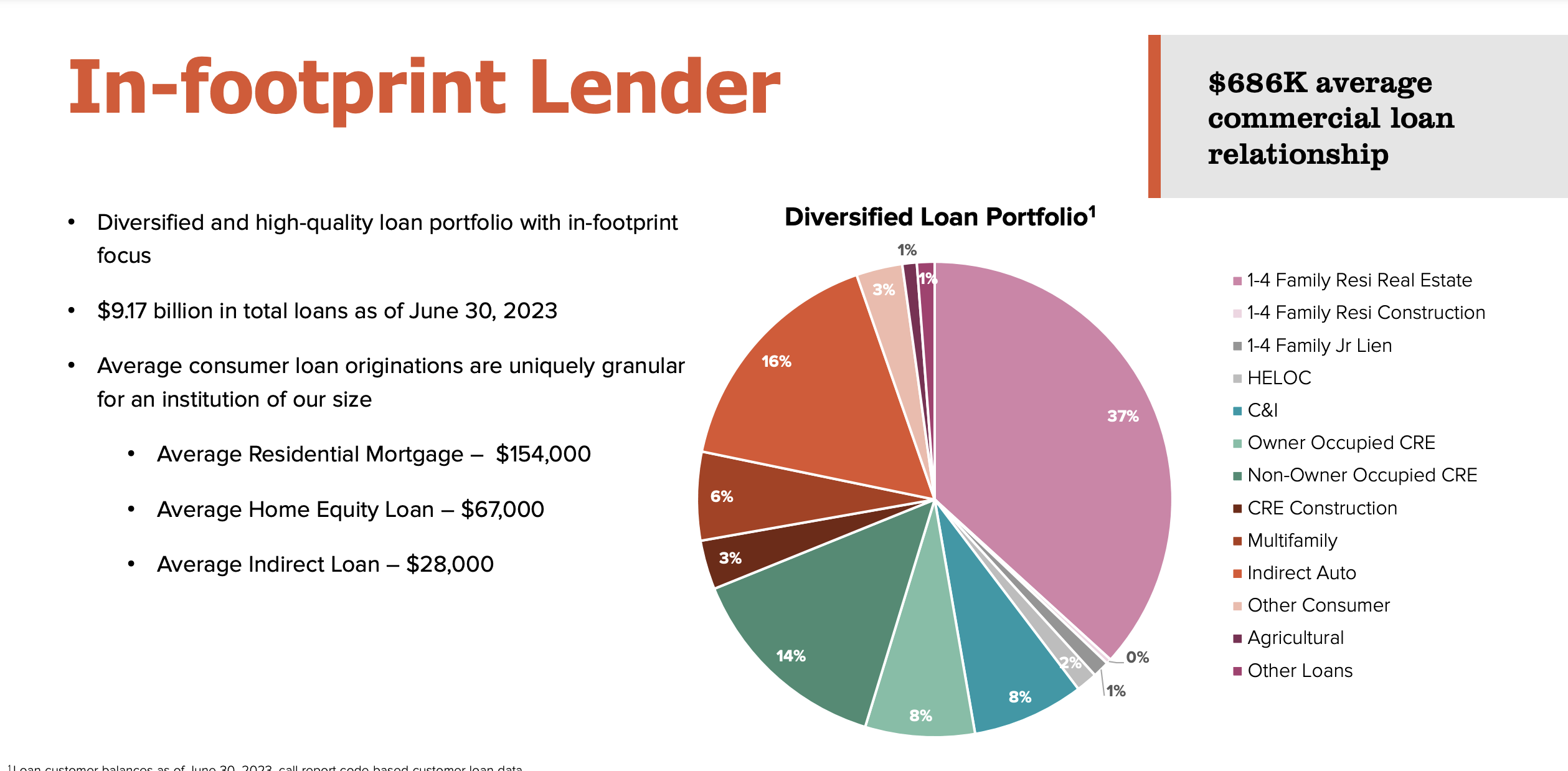

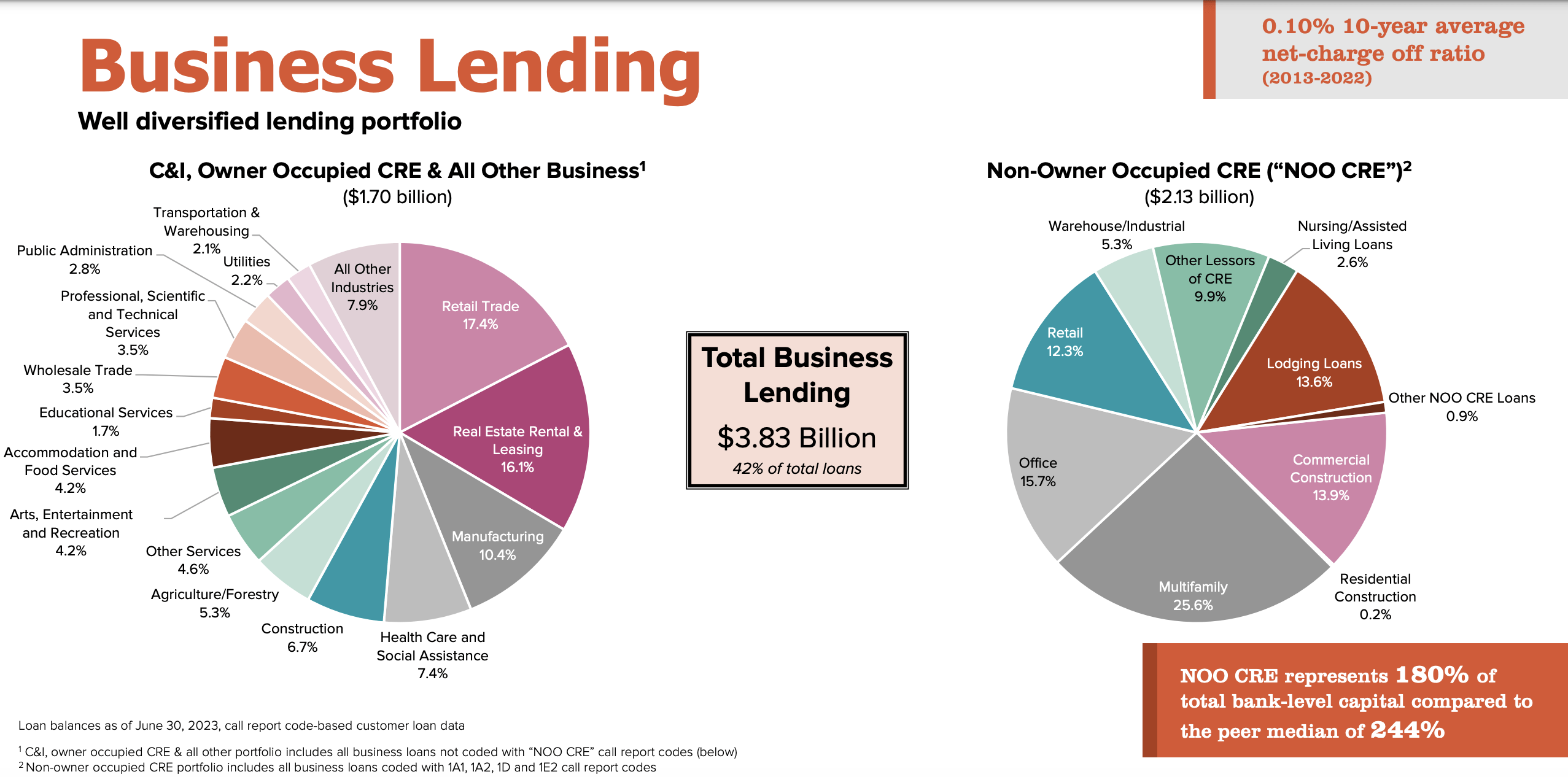

A growth in the company's loan portfolio has made possible the general expansion of its revenue and profits. Loans went from $7.42 billion in 2020 to $8.81 billion in 2022. As of the end of the most recent quarter , they came in even higher at $9.17 billion. Some of this benefit was offset to an extent because, after peaking at $5.31 billion in 2022, investment security values dropped to $4.23 billion by the end of the second quarter this year. I understand that one area that investors are concerned about when it comes to loans is exposure to office properties. Management does not break out this exposure for owner occupied commercial real estate. However, they do break it out for non-owner occupied commercial real estate. About 15.7% of the $2.13 billion of non-owner occupied commercial real estate in the form of office properties. That translates to only 3.6% of the company's entire loan portfolio. Most of its portfolio is dedicated to other things. For instance, about 37% of all loans by value fall under the one to four family residential real estate category. Another 16% falls under indirect automotive loans. That's followed up by 14% in the form of non-owner occupied commercial real estate.

{kind=link}

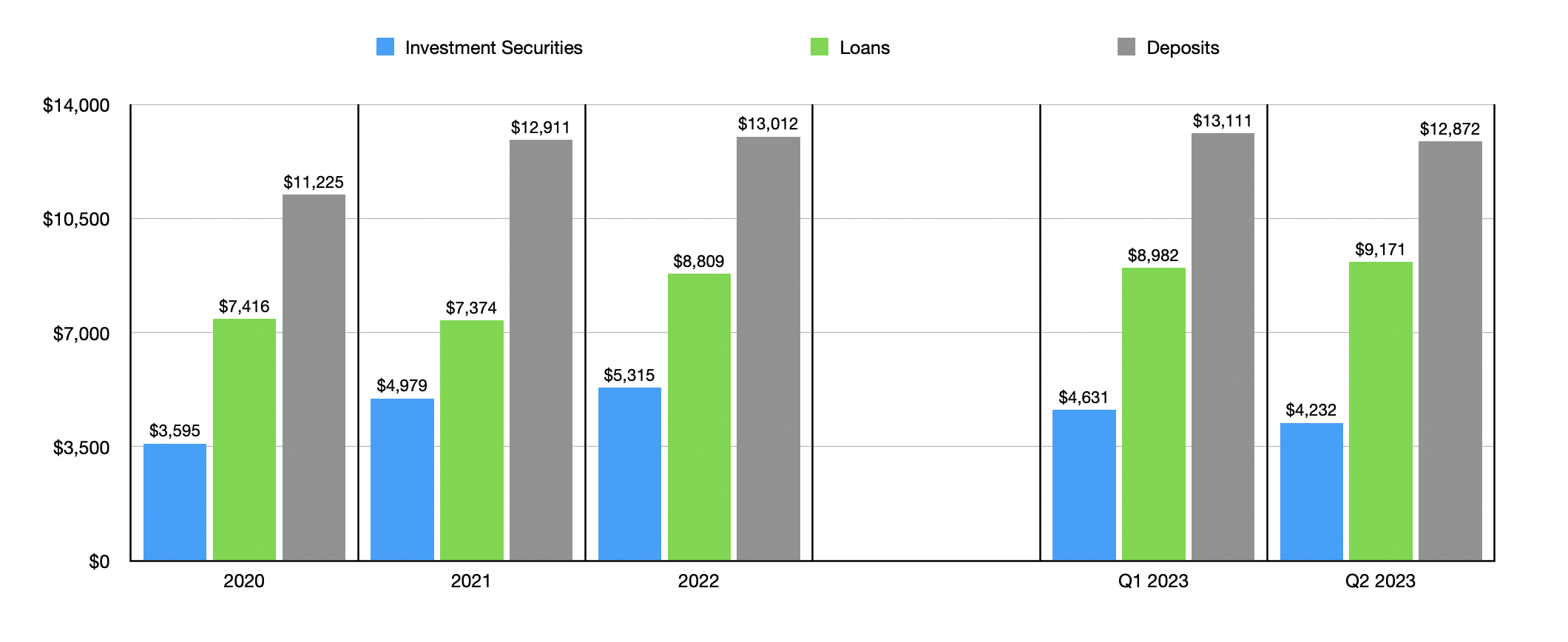

For much of the company's recent history, the value of deposits has managed to grow. That has fueled the loan portfolio growth. Deposits expanded from $11.23 billion in 2020 to $13.01 billion last year. This growth continued through the first quarter when it hit $13.11 billion. But from the end of the first quarter to the end of the second, deposits fell by $238.9 million to $12.87 billion. The good news, at least, is that only 15.9% of the company’s deposits are classified as uninsured. And on top of this, overall debt for the company is a paltry $234 million.

{kind=link}

When it comes to valuing the company, there are a couple of methods that we can use. The first would be the price to earnings approach. On this basis, shares are trading at a multiple of 12.5. In the grand scheme of things, this is not bad. Right now, however, the average price to earnings multiple in the space is about 10.4. So relative to that, the stock is a bit pricey. The other way is by comparing the share price to its book value. But this doesn't yield a satisfactory result either. Shares are trading at $43.53 apiece. By comparison, the book value per share is $30.07, while the tangible book value is $14.14.

Takeaway

All things considered, Community Bank System stock is not a great prospect. But it's also not an awful one. Personally, I believe that there are far better opportunities in the space right now. I understand why the stock has not recovered since shares are already more expensive than what many other players are trading for. The drop in deposits is painful, even though uninsured deposit exposure is attractive. But when you Add all of this together, it makes the company a ‘hold’ prospect in my book.

For further details see:

Community Bank System: There Are Better Prospects To Consider At This Time