CYH - Community Health Systems: Hurdles Still Yet To Pass

2023-04-27 06:46:57 ET

Summary

- Community Health Systems is a mixed operator at this point in time.

- On the one hand, some key business metrics are improving, with respect to operations.

- However, there's still a number of other issues to be addressed with cash flows and margin growth.

- Net-net, I rate CYH a hold.

Investment Summary

After curling off a bottom the question is, are we witnessing a rapid comeback for Community Health Systems, Inc. ( CYH )? Whilst this is promising, to the best of my estimation, it is not at the moment. In my previous CYH publication, I cover some of the major headwinds it must overcome. Many exist still today.

Although, fundamentals are improving somewhat. Even more so when thinking over a long-term basis. It has added 640 new licensed beds since FY'18 (average 128/year) and another 80 surgical and procedure suites (16/year on average) in the same time. The debt levels of 2015–'17 are no longer for this company and management has focused on retiring debt as much as possible, $645mm in H2 last year alone.

However, top-line growth has compressed annually since FY'18 and this presents as a challenge to gain investment. This, with a busy capital structure. $14Bn of assets are held up from negligible equity, not to mention the $11.4Bn in long-term debt liabilities. In my opinion, CYH hasn't recycled capital well over the last 5-years and this has led to a difficult time from the market. My numbers have these trends going forwards, too. Net-net, I believe there's still a ways to go for this name. Rate hold.

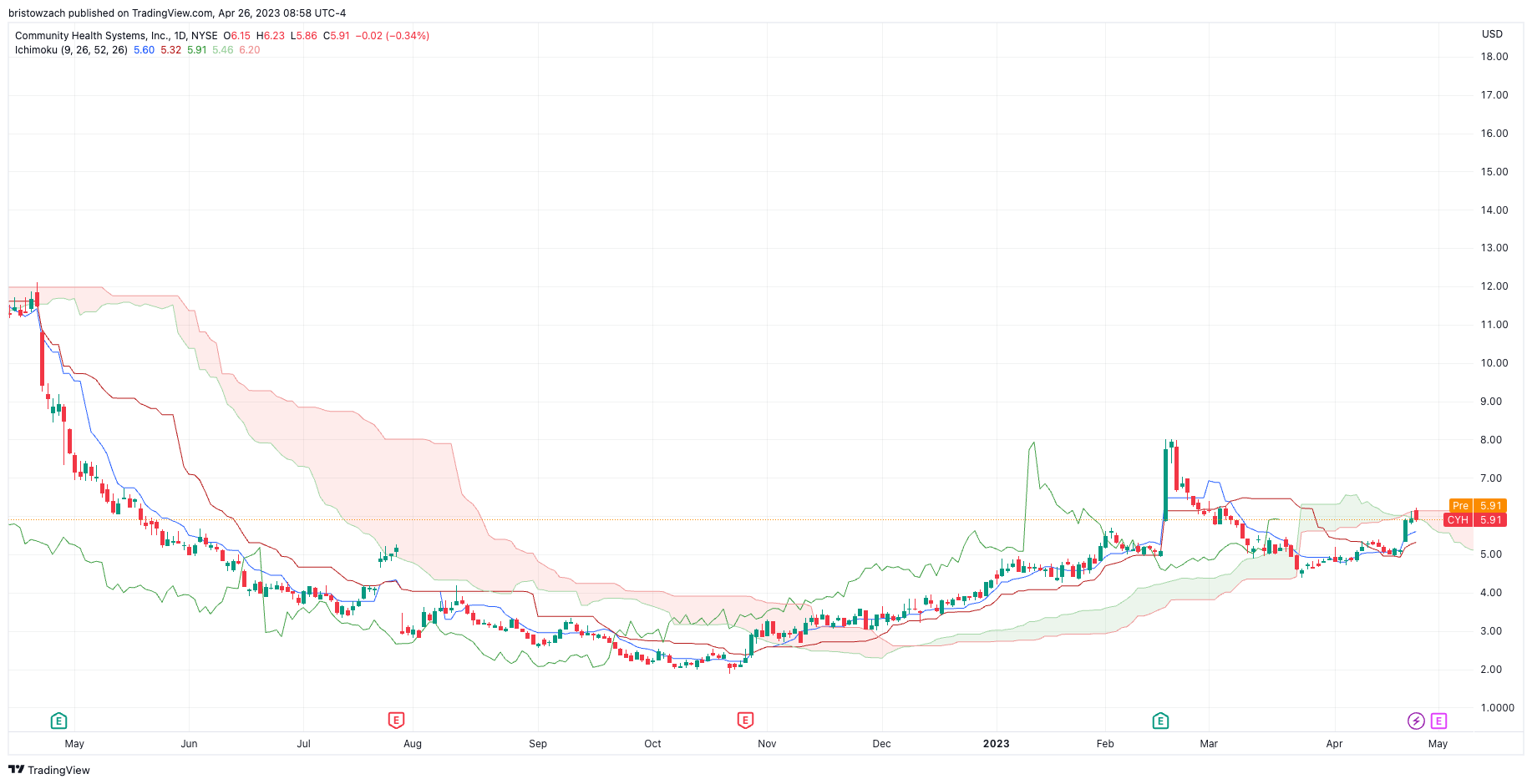

CYH curling up off lows

{kind=link}

Data: TradingView

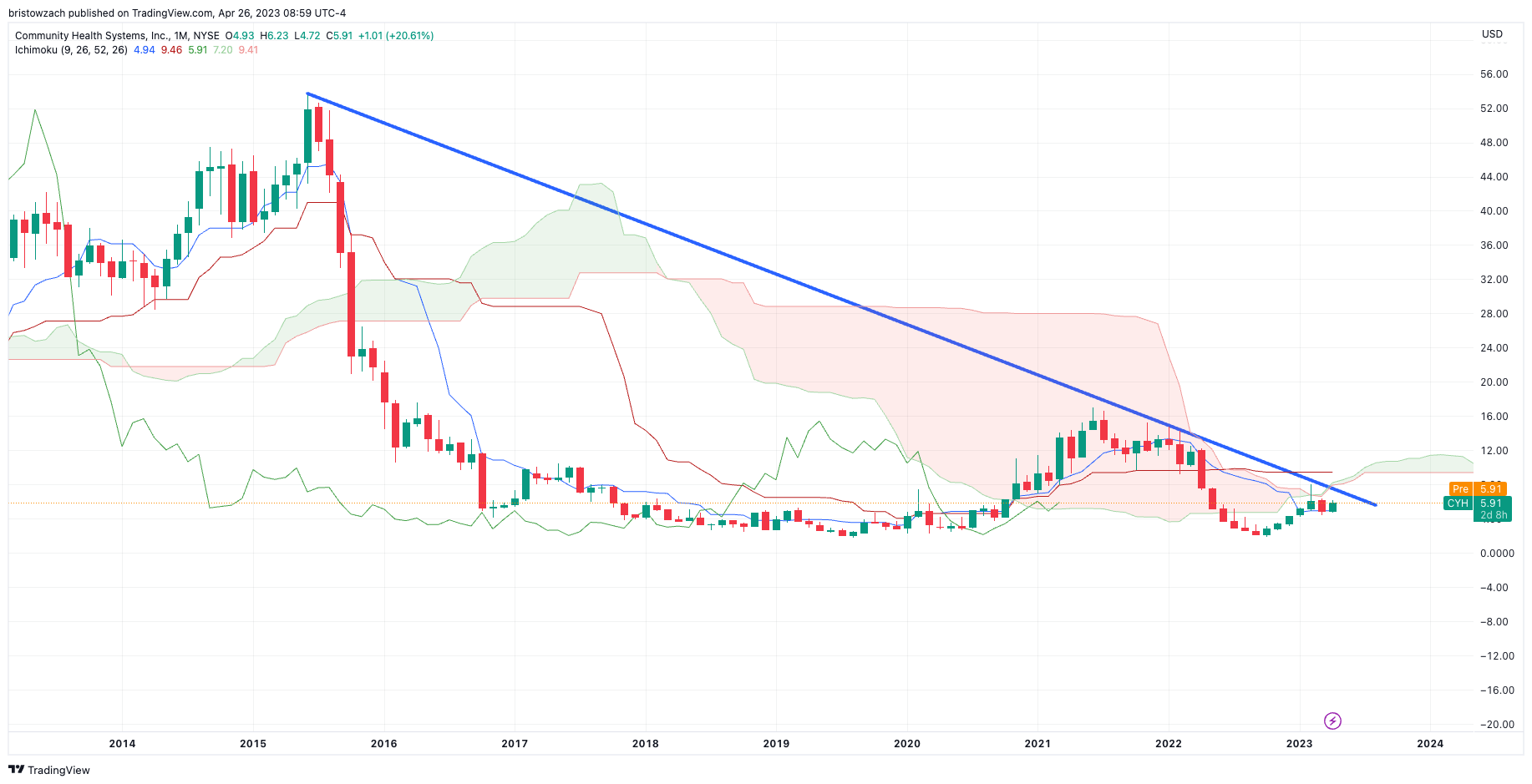

Different story over the long-term, however. Still a long ways to go.

{kind=link}

Data: TradingVIew

Current operations looking healthier

Revenue came in flat at $12.2Bn last year, but this is punitive from the $18–$19Bn revenue peak in 2013/14 for CYH. But this is a much leaner company, with more manageable leverage than 10-years ago. Hence, revenue growth is a factor of concern, as same-store revenues clipped 1.3% last quarter. Still, same-store admissions increased 4% YoY in Q4 and would explain the 8% decrease in net revenue per admission. Moreover, the firm is operating same-store admissions at its pre-pandemic levels.

Meanwhile, same-store surgeries were up 420bps YoY and are now above pre-pandemic range. This backed with 8.7% YoY growth in ED volumes, and these appear to have been unaffected by any pullback in Covid-related revenue. This would serve as an appropriate anchor to work from looking forward, now that we are beyond that era. All of these are certainly positives, but are likely already in the share price.

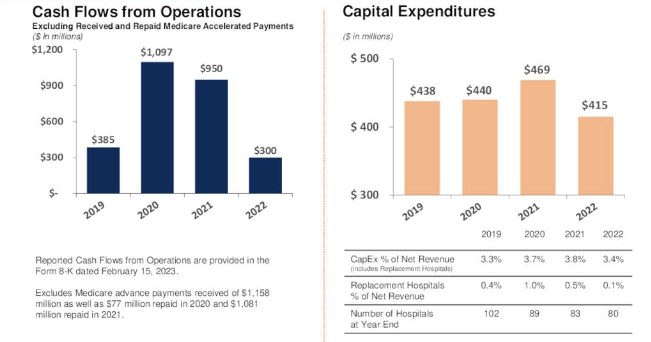

I'd also point out that CYH extinguished $378mm in notes outstanding last quarter, a trend it will be continuing. In the second half, it had retired $645mm of debt and captured a $300mm discount, which is good capital budgeting in my estimation. This is set to result in annualized interest savings of $58mm going forward. Good move, because the balance sheet is a sticking point for me. It has $11.4Bn in long-term liabilities, meaning $3.2Bn in adjusted equity is holding up $14Bn in asset – quite a wide window. Add in all liabilities, the company actually has negative equity of $1.4Bn [Figure 2]. Not something I can see improving quickly, or easily, either. It now has about $7Bn in tangible capital to uphold as well, although it is reasonably productive at 1.7x turnover.

This, and the fact it generated $300mm in annual operating cash flow, factoring in just $20mm of stock-based compensation. Still, this isn't attractive in my opinion. With $300mm in cash flow holding up $12Bn, just 2% of the top-line is backed by cash. Ideally, there'd be closer to 10% to create some operating leverage. Not to mention, the company has only $118mm in cash (0.9% of sales) on the balance sheet, and has accumulated a $3.4Bn deficit since FY'16, a trend I believe will continue in the medium-term. It's important to note that CYH will incur a 450bps YoY increase in the average hourly rate for its employees this year as well. This could be a specific challenge going ahead, if trends continue. Even though it totalled $80mm in labour costs in Q4, there's potential margin pressure from this segment.

Fig. 1

{kind=link}

Data: CYH Investor Presentation

Further, CYH has wound back CapEx to $415mm last year, which may or may not be beneficial. Management say this is to reflect the current operating environment. However, the question beckons at the growth opportunities on CYH's plate, let alone the cash it can generate for owners. There's risk here, in that regard. CapEx and NWC requirements are ~$400mm and $896mm, respectively, suggesting there is room for this to wind back further. It is difficult to foresee any growth in operations with the current capital structure. A bulk of the equity growth is capped by the size of the liabilities, and the company is less capital productive than previous as well. Further, earnings growth continues to be weak, and there looks to be no respite to this in the near future either.

Fig. 2

Data: CYH Investor Presentation

This could be quite the problem, as profitability isn't CYH's strong point anyway. It is strong against the sector, yes – and this is a balancing point But, we're looking at 3% trailing return on capital here, 0.82x asset turnover and single-digit margins, which aren't conducive to unlocking value for shareholders. Last time, I estimated "another 14-15% decline in CYH's post-tax earnings for FY23E" and noted the several divestitures it had completed since 2021. Moreover, shares are looking richly priced versus cash flow. Cash per share is $0.91, and for the providers of capital, the return on assets its 0.3%.

You can't expect a higher multiple when the returns on capital provided to and owned by the business aren't above the hurdle rate. This will require substantial performance to turn around. I don't foresee this happening in the medium-term for CYH. The task is large, and with $118mm in cash on the balance sheet, the risk of issuing further debt is a probability in my opinion. Whether $300mm+ in operating cash flow is sufficient to continue the growth route, we will wait and see. Perhaps a contrarian can see the opposite side, expecting the margins to lift off from here. Not in this report, however.

Fig 3.

Data: Seeking Alpha, CYH profitability

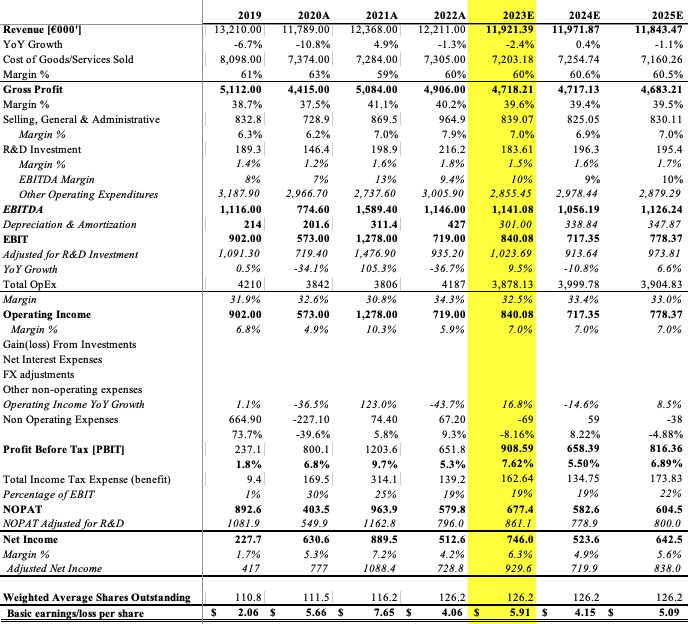

Looking forward, my numbers call for CYH to generate another $11.9–$12Bn at the top-line [see: Appendix 1]. Management say this could be 50/50% volume/rate respectively, and I'd agree.

This would be a generous increase in same-store revenues of 3–4%, but still, going forward, I believe top-line growth will be pressured. Cash collection is low relative to turnover, and I believe CYH could see revenues pull back to a $11.9Bn range more frequently. I'd see 11-12% EBITDA margin on this, and again CFFO making up just 5% of revenues. This is a potential downward spiral as cash interest expense is projected at $780mm at the upper end, and the $600–$700mm in potential operating cash flow would be wiped out on a negative pre-tax earnings margin.

Fig. 4

Data: Author Estimates

Valuation and conclusion

One might say CYH is cheap at 9x forward EBITDA and 1x forward sales, well below the sector. The question is, what are you getting for these kind of multiples. Number 1 is a messy capital structure. Any gains going forward won't be all from the equityholders' capital. Number 2, is that quant ratings for the company are flat as well. I see no major catalyst for the trend below to deviate.

Fig. 5 – CYH Quant Rating

Data: Seeking Alpha

Further, the interest payable for CYH isn't the best use of cash in my opinion, not at the current ranges. In addition, consensus has is to do negative $0.39 in EPS this year, and CYH doesn't have the best track record in beating the Street. Can it rate higher? Sure it can. At 9x forward EBITDA, my numbers have it to potentially hit $7.50, 27% upside potential.

In summary, do I think that CYH is worth a buy right now? I don't. There are more appealing and productive options to place capital to work at this period of time. Keep CYH on the radar though, as it could be an interesting year for the company. A $12.5–$13Bn revenue result could be interesting, but that's a big jump from my estimates. At this point, rate hold.

Appendix 1: FY'23-'25 forecasts

{kind=link}

Data: Author

For further details see:

Community Health Systems: Hurdles Still Yet To Pass