DOC - Community Healthcare Trust's Third Largest Tenant Declares Bankruptcy Poses Risk

2023-06-20 10:59:37 ET

Summary

- GenesisCare filed for Chapter 11 bankruptcy on June 1st, posing a risk to Community Healthcare Trust as their third-largest tenant.

- CHCT has one lease already rejected by GenesisCare, with the company having 120 days to decide on additional leases.

- The bankruptcy proceedings represent a significant risk to CHCT's investors, who should be questioning the lack of information from management.

- Another CHCT tenant Envision Healthcare filed for bankruptcy in May.

In his recent article Community Healthcare's (CHCT) Gravy Train Has A Finite Shelf Life, Dane Bowler laid out how since its IPO, CHCT has invested in properties in tertiary markets with tenants with less than stellar financials. Due to the high yields these properties offered, the market priced CHCT at a premium to NAV for years and ignored the risks. As interest rates rise and labor costs go up, many of the private equity backed health care providers who are tenants of Healthcare REITs are experiencing severe financial strain and the risk of CHCT's strategy are becoming clear. Two significant CHCT tenants recently filed for bankruptcy. On June 1st GenesisCare filed for Chapter 11 Bankruptcy . In addition to GenesisCare, Envision Healthcare filed for bankruptcy in May as I predicted in Envision's Potential Bankruptcy May Trigger A Sell-Off For Community Healthcare Trust And Global Medical REIT . I believe these two filings and the risk they pose to CHCT's results will force investors to reevaluate its premium valuation.

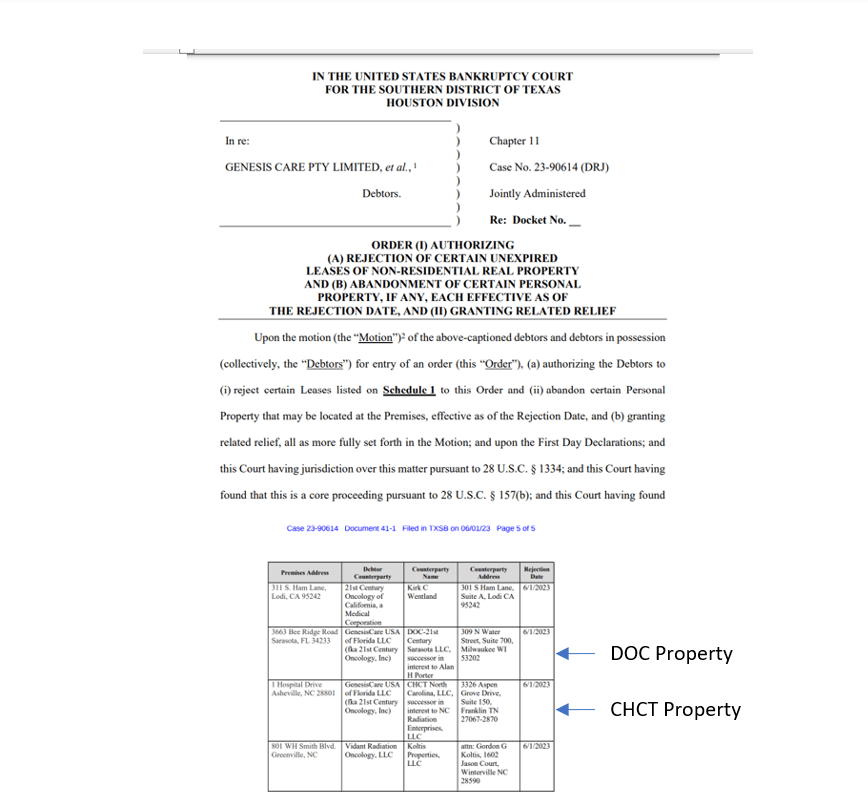

In conjunction with its bankruptcy filing, GenesisCare rejected 8 leases . One of these leases was for a property owned by CHCT. Interestingly, Physicians Realty Trust ( DOC ) also had a lease rejected, but I have no reason to believe DOC has significant exposure to GenesisCare.

Rejected Leases (DEBTORS’ MOTION FOR ENTRY OF AN ORDER (I) AUTHORIZING (A) REJECTION OF CERTAIN UNEXPIRED LEASES OF NON-RESIDENTIAL REAL PROPERTY AND (B) ABANDONMENT OF CERTAIN PERSONAL PROPERTY, IF ANY, EACH EFFECTIVE AS OF THE REJECTION DATE, AND (II) GRANTING RELATED RELIEF)

{kind=link}

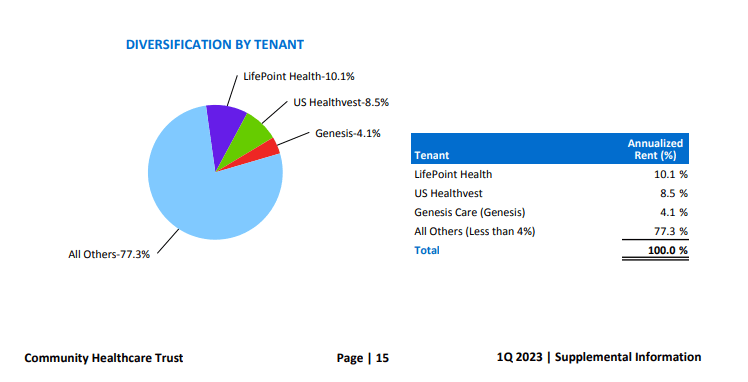

CHCT has a total of nine GenesisCare locations. ( CHCT Property Locations Table 1Q23 Supplemental Financial Disclosure. ) CHCT receives 4.1% of its annualized base rent from GenesisCare which equates to 8.0% of its 2023 Consensus FFO.

{kind=link}

If GenesisCare only rejects one lease from CHCT, its impact on reported results will be minimal. However, it is important to realize that GenesisCare has 120 days to decide which leases it is keeping and which it is rejecting. Given that the Australian parent company is planning to sell the U.S. operations , it is likely they are deferring the decision on which leases to accept, so the future buyer can decide which properties they want. It is also possible that GenesisCare or the future buyer will come back to CHCT and say we will accept a lease, but only with a reduction in the rental rate. An additional wrinkle in this bankruptcy is the decision to file on June 1 st , the day that rent is due. It is possible by filing on June 1 st GenesisCare is trying to make June’s rent a prepetition claim . This would mean that CHCT would need to line up with other unsecured creditors to try to collect June’s rent on any leases that are ultimately rejected. (I believe management should at least let investors know whether they have received June rent from GenesisCare.) While there are a number of ways the bankruptcy process could play out, the proceedings represent a significant risk to CHCT’s investors. CHCT’s investors should be asking why management has not released any information either to reassure investors or to provide clarity on the impact of the bankruptcy filing.

Interestingly, Sila Realty Trust which is a non-traded REIT (fka Carter Validus) filed an 8-K with the SEC June 5th detailing their exposure to the GenesisCare bankruptcy even though none of their leases were rejected. This means they viewed GenesisCare's bankruptcy as a material event for their business. Sila's total exposure to GenesisCare is 5.4% of annual base rents ( Sila Realty Trust 1Q23 Supplemental Financial Disclosure p.15 ) vs. 4.1% for CHCT. Given that CHCT has already had a lease rejected, investors should be questioning, why they do not see the bankruptcy as a material event. Most participants in the REIT industry feel non-traded REITs typically have disclosure that is inferior to public REITs. In this instance, it looks like a non-traded REIT is giving investors more information than CHCT.

Conclusion

I would advise investors with a high risk-tolerance to short CHCT and investors with lower risk tolerance to avoid the stock. Healthcare REITs can trade off significantly when they announce a tenant bankruptcy. As I explained in Envision's Potential Bankruptcy May Trigger A Sell-Off For Community Healthcare Trust And Global Medical REIT when Global Medical Trust ( GMRE ) announced a tenant representing 2.3% of annual base rents was filing for bankruptcy the stock traded off close to 20% over the next week. In GMRE's case, the lease was eventually assumed. I believe the market could have a similar reaction to a CHCT announcement. In gauging the market’s reaction to the potential announcement, it is important to realize that CHCT’s bankrupt tenant represents a greater percentage of annual base rents than was the case for GMRE and CHCT’s tenant has already rejected a lease. Additionally, if the Envision Healthcare bankruptcy needs to be announced as well, investors may begin to see a pattern. An increasing number of bankrupt tenants for CHCT does not support it being valued at a premium to NAV.

The market's recognition of CHCT's exposure to bankrupt tenants will likely occur by their next earnings call in August as they will almost certainly need to add some disclosures in their 10Q to discuss the GenesisCare bankruptcy. It is also possible that CHCT will be forced to issue an 8-K before the next earnings call disclosing the bankruptcy, if GenesisCare rejects more leases.

Risk to Shorting CHCT

It is important for readers to understand that despite the problems I believe CHCT faces due to the bankruptcy of GenesisCare and Envision Healthcare, the stock is very volatile. This means any number of things could cause the stock price to spike temporarily. A short seller without sufficient capital could be forced to liquidate their position at a loss in this scenario. It is easy to envision circumstances where the remainder of GenesisCare’s leases are assumed and there is no need for an announcement. Additionally, CHCT will likely continue to pay its dividend. Not only does the dividend represent a cost to a short seller, I believe the dividend will put a floor on the stock price for some time as there will always be investors who are seeking yield. In other words, I believe someone shorting CHCT needs to have the patience and capital to wait until the market has a clear and informed view of the impact of the Chapter 11 filings for both GenesisCare and Envision Healthcare.

For further details see:

Community Healthcare Trust's Third Largest Tenant Declares Bankruptcy, Poses Risk