CVLT - Commvault Looks To Reduce Costs As Outlook Is Flat

2023-04-21 15:47:53 ET

Summary

- Commvault Systems, Inc. provides a range of storage solutions to businesses worldwide.

- The firm has a strong balance sheet and produces excellent free cash flow.

- However, growth is likely to be flat amid a slowing macroeconomic environment, so I'm on Hold for Commvault Systems, Inc. in the near term.

A Quick Take On Commvault Systems

Commvault Systems, Inc. ( CVLT ) provides a range of on-premises and cloud data storage and recovery technologies.

The company has a strong financial position and produces substantial free cash flow, but growth is likely to be flat in the period ahead.

Accordingly, I’m on Hold for Commvault Systems, Inc. in the near term as I watch the effects of a slowing economy on its trajectory.

Commvault Systems Overview

Tinton, New Jersey-based Commvault was founded in 1988 to provide organizations with data protection, backup and recovery solutions.

The firm is headed by Chief Executive Officer Sanjay Mirchandani, who was previously CEO of Puppet and SVP Asia Pacific Japan for VMware.

The company’s primary offerings include:

-

Backup & recovery

-

Disaster recovery

-

File storage optimization

-

Data governance

-

eDiscovery & compliance

-

Managed services

-

Security.

The firm acquires customers via its direct and inside sales and marketing teams as well as through partner referrals.

CVLT counts more than 100,000 customers and 7,000 ecosystem partners.

Commvault Systems’ Market & Competition

According to a 2022 market research report by MarketsAndMarkets, the global market for cloud storage services was an estimated $78.6 billion in 2022 and is forecast to reach $183.7 billion by 2027.

This represents a forecast CAGR of 18.5% from 2022 to 2027.

The main drivers for this expected growth are growing demand for enterprises for ever larger amounts of data and a rising number of remote-located employees and contractors needing access to relevant data stores.

Also, a key challenge for the industry is to effectively defend against security threats and improve data privacy for corporate and personal data.

Major competitive or other industry participants include:

-

Amazon

-

Alphabet

-

Microsoft

-

Dell EMC

-

iDrive

-

pCloud

-

Dropbox

-

Icedrive

-

NordLocker

-

Others.

Commvault’s Recent Financial Trends

-

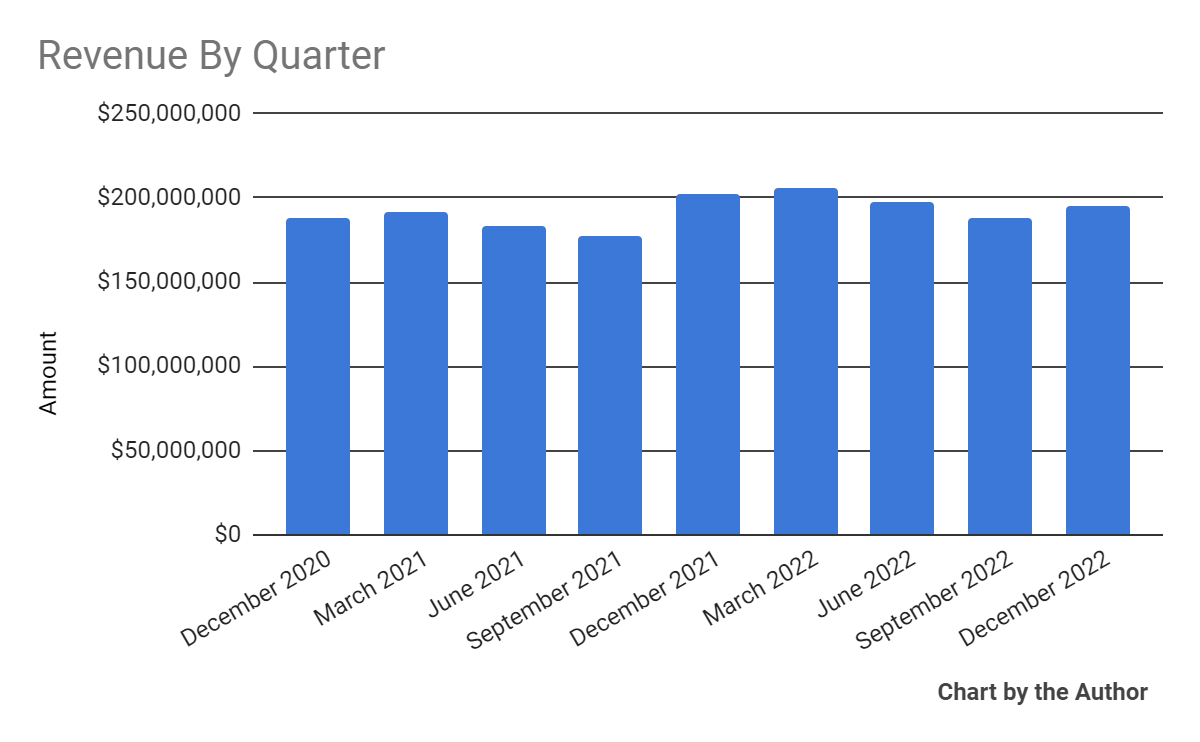

Total revenue by quarter has essentially flatlined recently:

{kind=link}

-

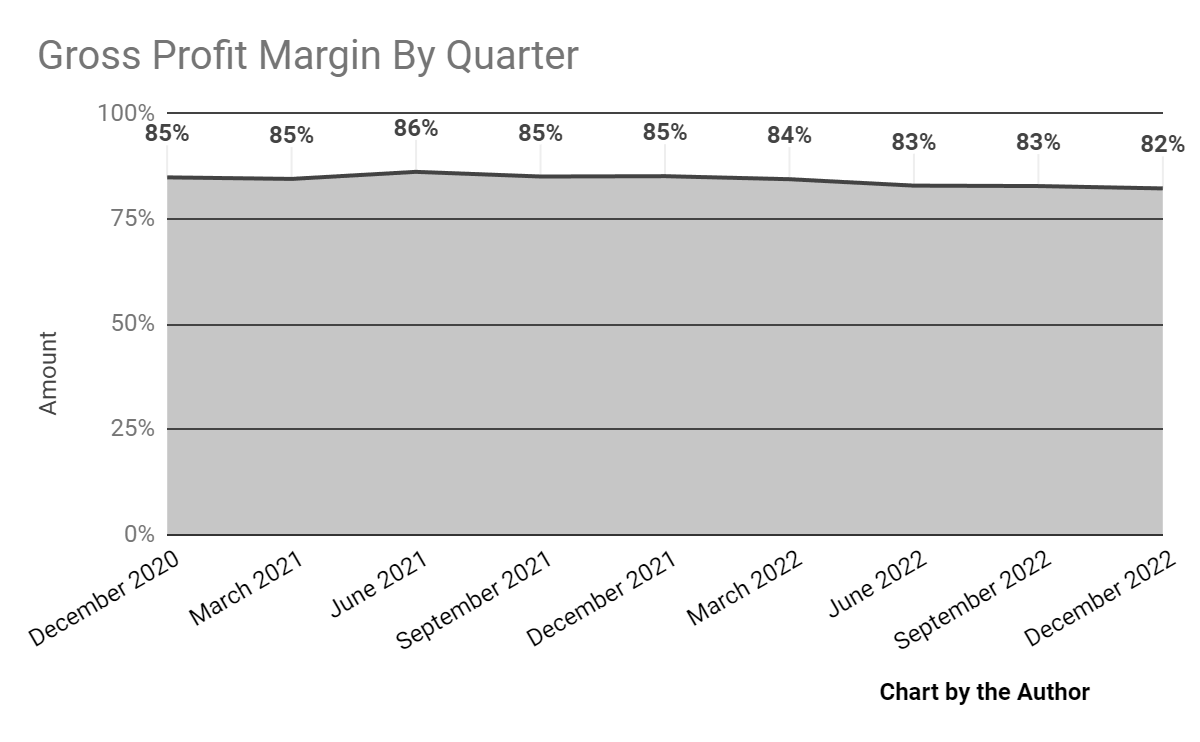

Gross profit margin by quarter has dropped in recent quarters:

{kind=link}

-

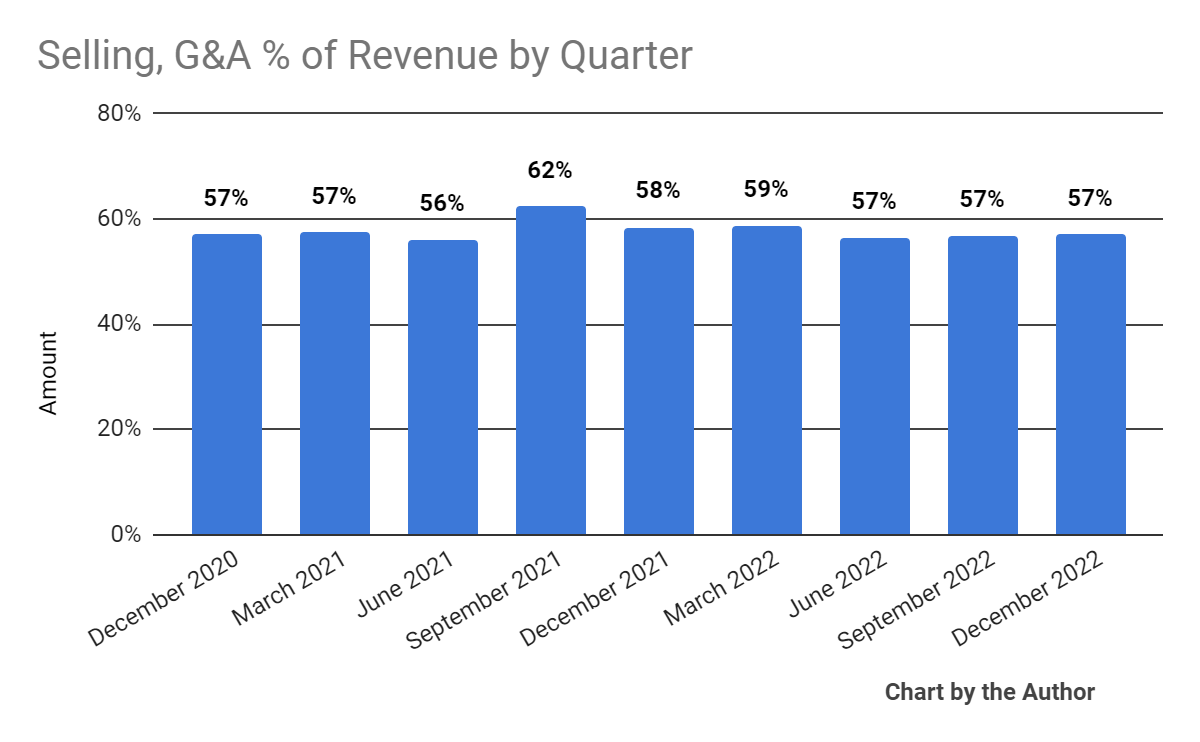

Selling, G&A expenses as a percentage of total revenue by quarter have dropped slightly more recently:

{kind=link}

-

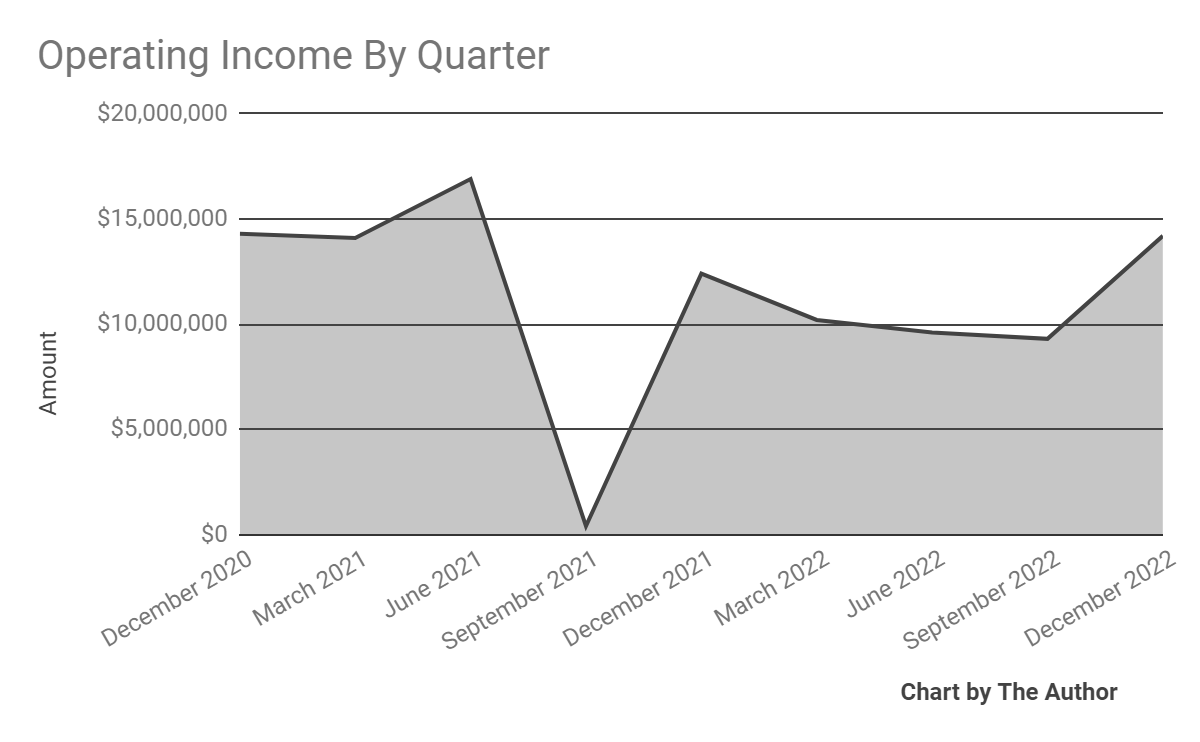

Operating income by quarter has fluctuated markedly in recent quarters:

{kind=link}

-

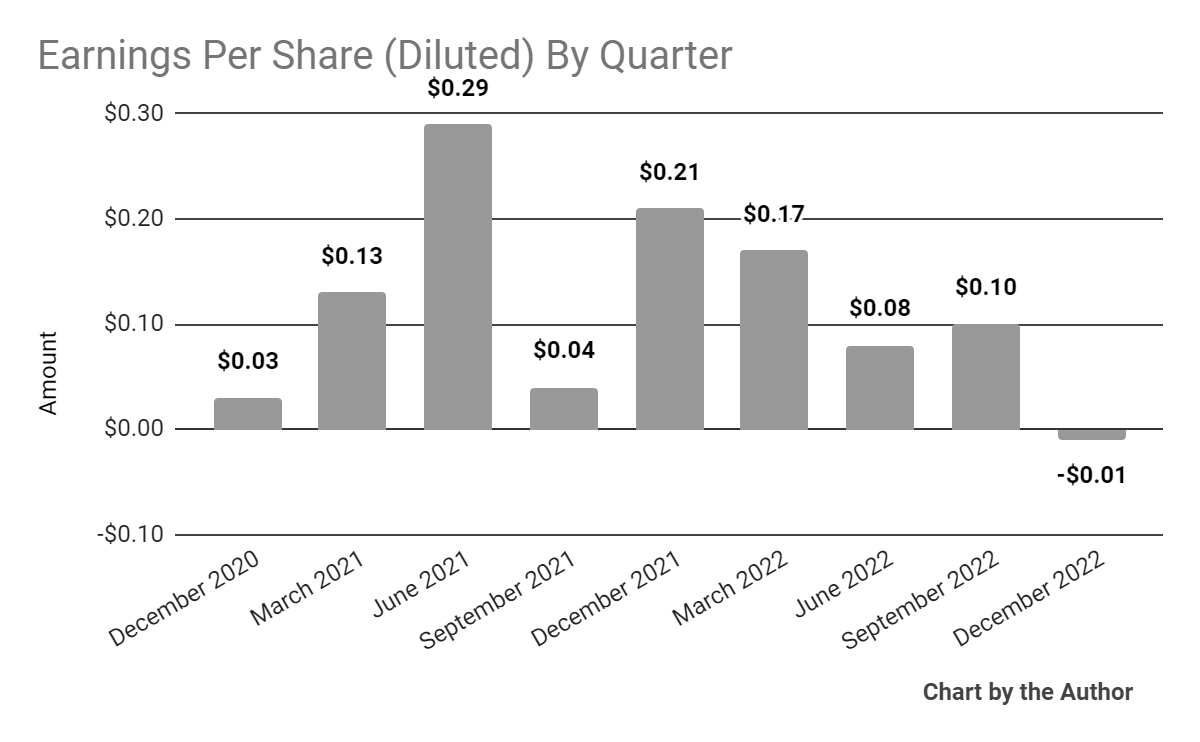

Earnings per share (Diluted) have turned negative in Q4 2022:

{kind=link}

(All data in the above charts is GAAP.)

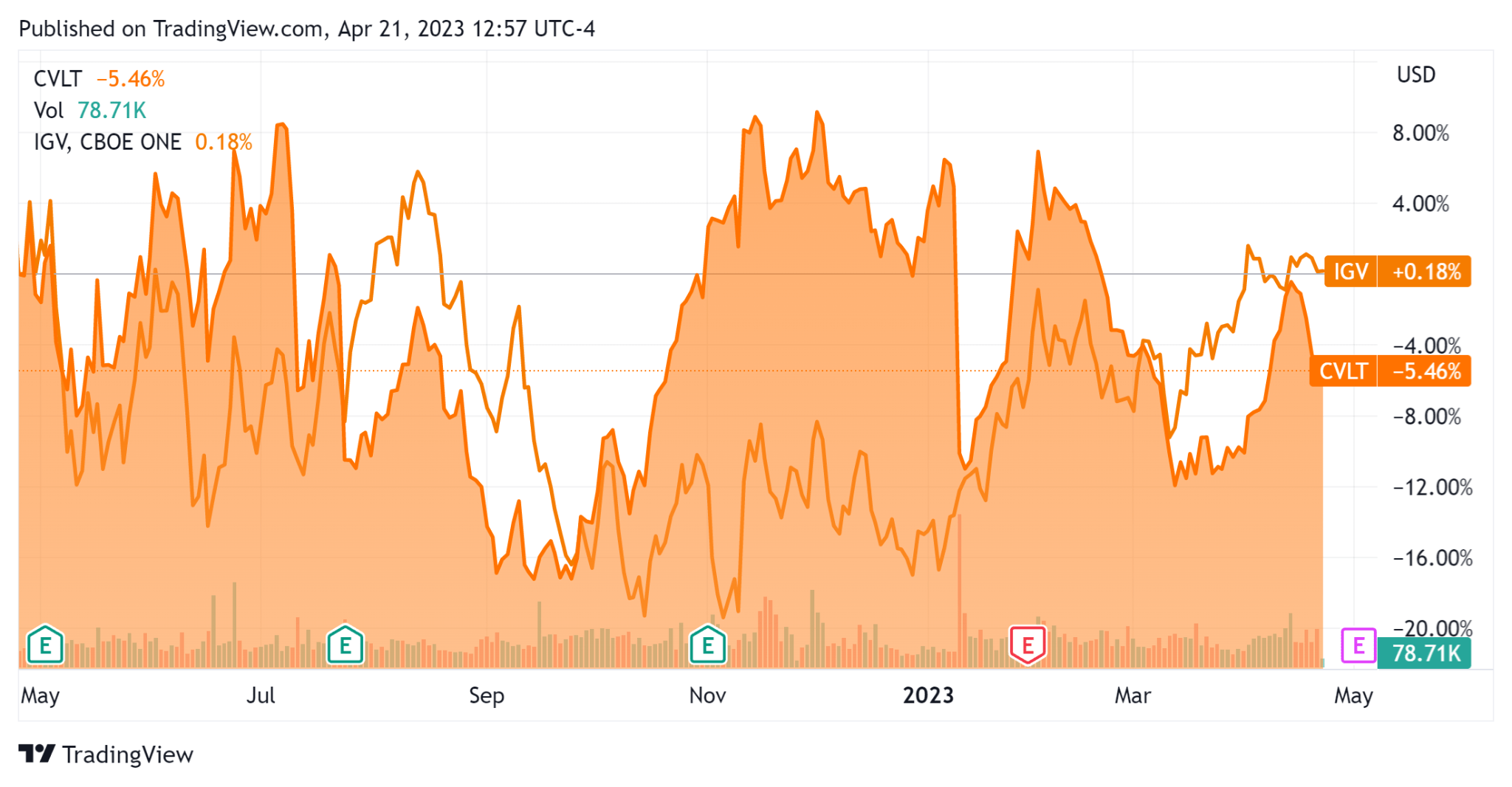

In the past 12 months, CVLT’s stock price has dropped 5.46% vs. the rise of the iShares Expanded Technology-Software ETF ( IGV ) of 0.18%, as the chart indicates below:

{kind=link}

For the balance sheet , the firm ended the quarter with $273.5 million in cash and equivalents and no debt.

Over the trailing twelve months, free cash flow was an impressive $186.8 million, of which capital expenditures accounted for $2.8 million. The company paid a hefty $109.4 million in stock-based compensation in the last four quarters.

Management did not disclose any company retention rate metrics.

Valuation And Other Metrics For Commvault

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 3.0 |

| Enterprise Value / EBITDA |

| 45.1 |

| Price / Sales |

| 3.4 |

| Revenue Growth Rate |

| 4.3% |

| Net Income Margin |

| 2.0% |

| GAAP EBITDA % |

| 6.7% |

| Market Capitalization |

| $2,620,000,000 |

| Enterprise Value |

| $2,360,000,000 |

| Operating Cash Flow |

| $189,570,000 |

| Earnings Per Share (Fully Diluted) |

| $0.34 |

(Source - Seeking Alpha.)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

CVLT’s most recent GAAP Rule of 40 calculation was only 10.9% as of FQ3 2023’s results, so the firm is in need of substantial improvement in this regard, per the table below:

| Rule of 40 - GAAP |

| Calculation |

| Recent Rev. Growth % |

| 4.3% |

| GAAP EBITDA % |

| 6.7% |

| Total |

| 10.9% |

(Source - Seeking Alpha.)

Future Prospects For Commvault

In its last earnings call ( Source - Seeking Alpha ), covering FQ3 2023’s results, management highlighted "delays and deferrals" in customer spending activity, as prospects and existing clients exert greater scrutiny on new spending and sales cycles extend as a result.

Notably, the firm’s enterprise customers were particularly slow in closing deals, with large deal revenue dropping $10 million year-over-year.

By contrast, deals for under $100K in revenue rose by 6%, indicating the lower and middle market segments were performing better than the large enterprise segment.

Leadership also noted that its Metallic product has succeeded in drawing in new customers, with 70% of Metallic’s new additions being customers that are new to Commvault.

Management is continuing to look for ways to cut costs, announcing its intention to sell its headquarters building and lease back a small portion of it.

Looking ahead, the company will likely continue to see slower customer decision-making as many economists are predicting a second-half 2023 recession or meaningful slowdown in the U.S. economy.

Commvault Systems, Inc.'s financial position is quite strong, with significant liquidity, no debt and copious free cash flow.

However, the firm is handing out over $100 million in trailing twelve-months stock-based compensation, diluting shareholders in the process.

Regarding valuation, the market is valuing Commvault Systems, Inc. at an EV/Sales multiple of around 3.0x.

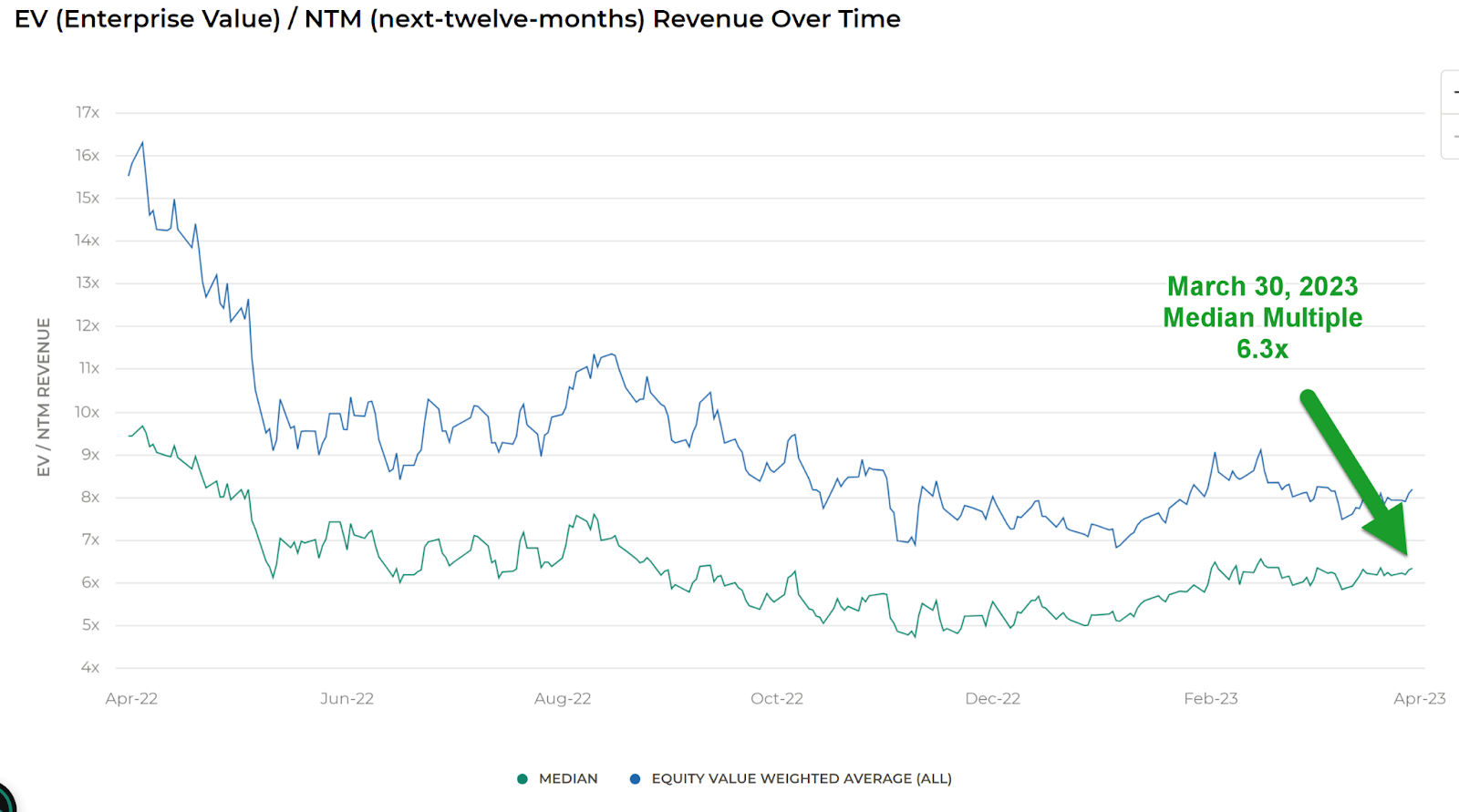

The Meritech Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 6.3x on March 30, 2023, as the chart shows here:

EV/Next 12 Months Revenue Multiple Index (Meritech Capital Index)

{kind=link}

So, by comparison, Commvault Systems, Inc. is currently valued by the market at a substantial discount to the broader Meritech Capital SaaS Index, at least as of March 30, 2023.

The primary risk to the company’s outlook is a macroeconomic slowdown or recession, which will likely reduce its revenue growth potential, which is already flat.

A potential upside catalyst to Commvault Systems, Inc. stock could include an end to interest rate hikes, reducing downward pressure on its valuation multiple.

However, given the slowing macroeconomic conditions, elongating sales cycles, and minimal forward visibility, I’m on Hold for Commvault Systems, Inc. in the near term.

For further details see:

Commvault Looks To Reduce Costs As Outlook Is Flat