CVLT - Commvault: Low Conversions Are A Concern

2024-01-19 15:47:39 ET

Summary

- Commvault has reduced its guidance due to lower conversion from perpetual license to subscription, indicating a need to win over customers.

- The company offers data protection solutions and has stable revenue and high gross margins.

- Slowing transition to subscription and lower customer referrals compared to competitors are challenges for Commvault's growth.

Commvault ( CVLT ) has reduced its guidance citing lower conversion in its perpetual license base to subscription. We believe this is symptomatic of a deeper issue with customer feedback. As described below, we think the company is in a dire need of winning over its customers, lest its competitors take Commvault’s cake. Until there is a clear plan from the company on remediating revenue growth, we would not be an owner of the Commvault stock.

Business

Commvault is a leading provider of data protection solutions. The company has had a stable revenue profile and 80%+ gross margins, despite its ongoing transition away from a software to a SAAS (software as a service) company.

Commvault offers the following:

Products:

- Data recovery: Commvault Backup and Recovery (or CBR), Commvault Disaster Recovery (CDR), Commvault Complete Data Protection (combination of CBR and CDR) and Metallic Data Protection as-a-service (or Metallic)

- Data Compliance & Governance: Commvault Data Governance, Commvault File Storage Optimization, and Commvault eDiscovery and Compliance

- Data Storage: Hyperscale X (data protection solutions for small to large enterprises) and Metallic Recovery Reserve (a SAAS based solution that helps to adopt Commvault’s Data recovery and storage products)

- Data Security: Metallic ThreatWise, to provide an early detection system

Support Services

These services help complement the company’s product portfolio

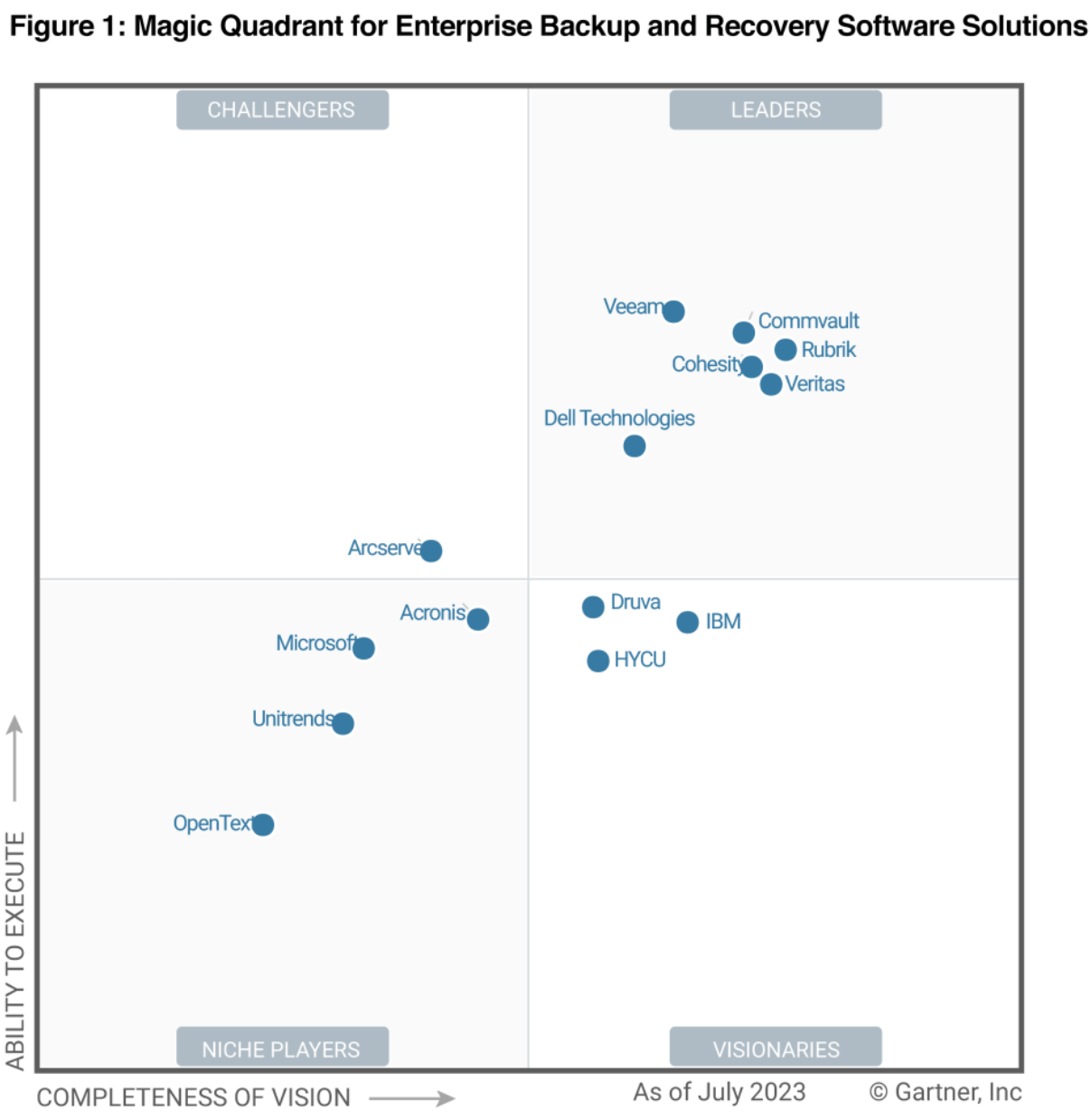

Commvault has over 1,350 patents to its credit and is a leader in the prestigious Gartner Magic Quadrant

{kind=link}

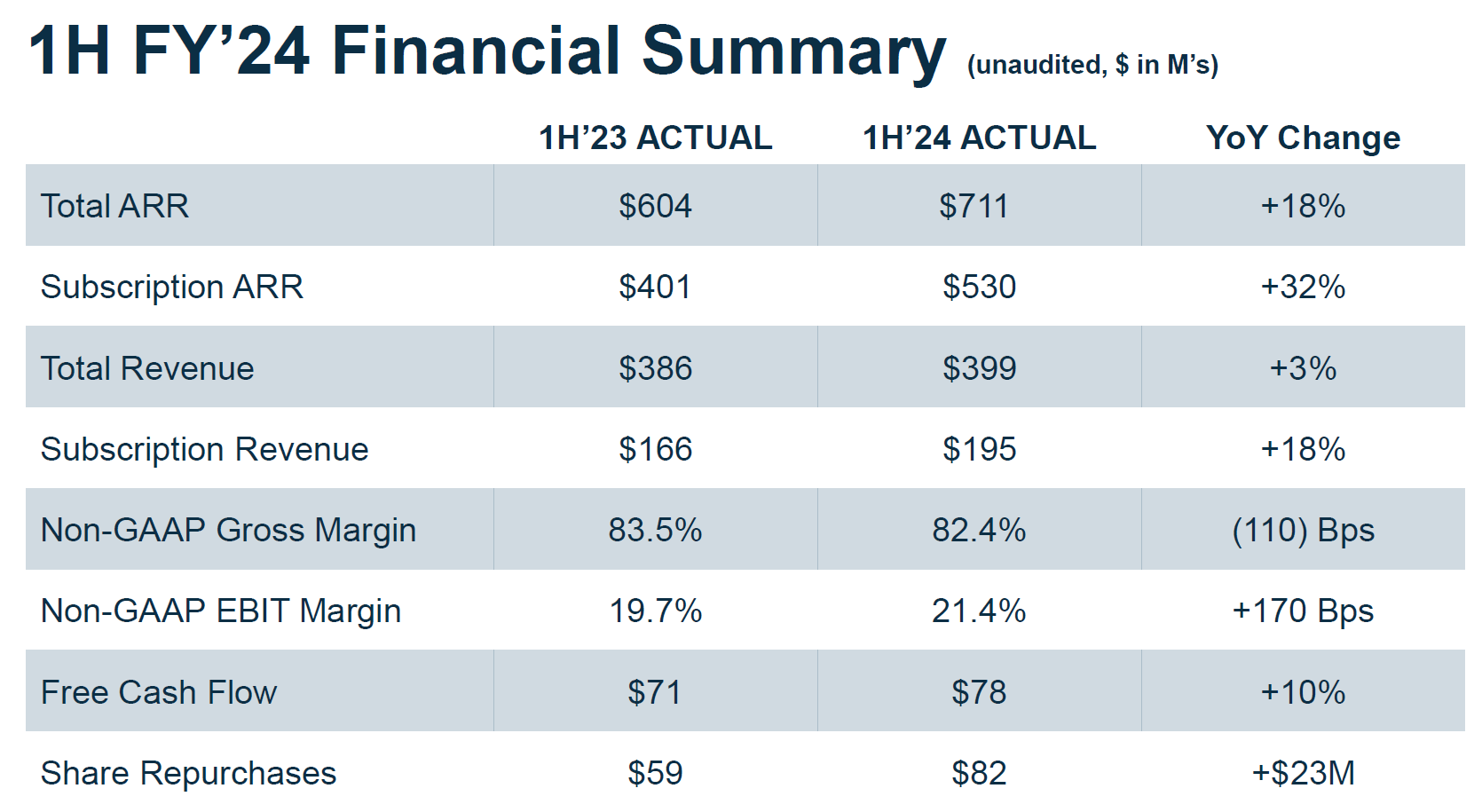

For the latest reported Q2 2024, the company did handsomely on the financial metrics.

{kind=link}

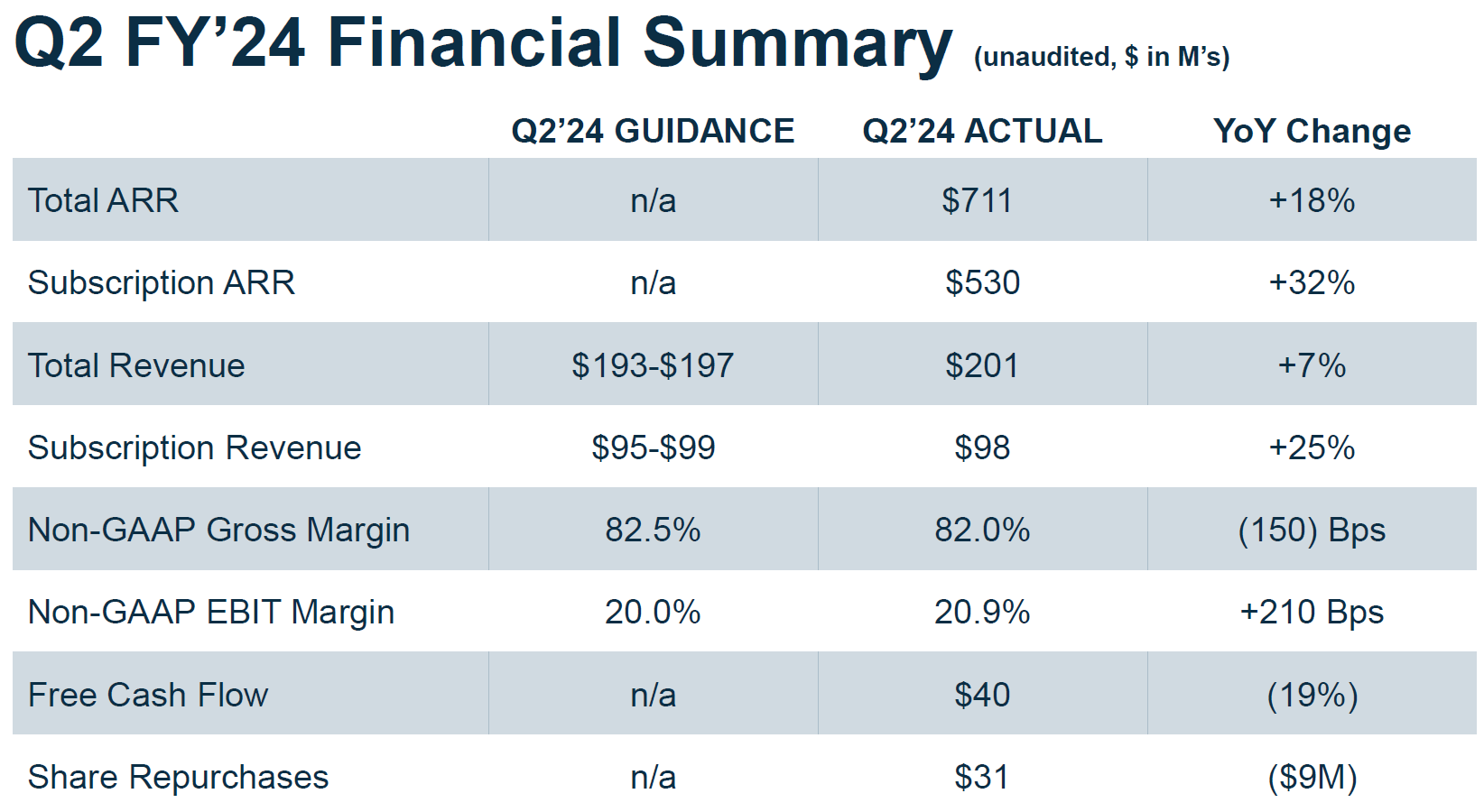

Commvault’s numbers were also ahead of its guidance.

{kind=link}

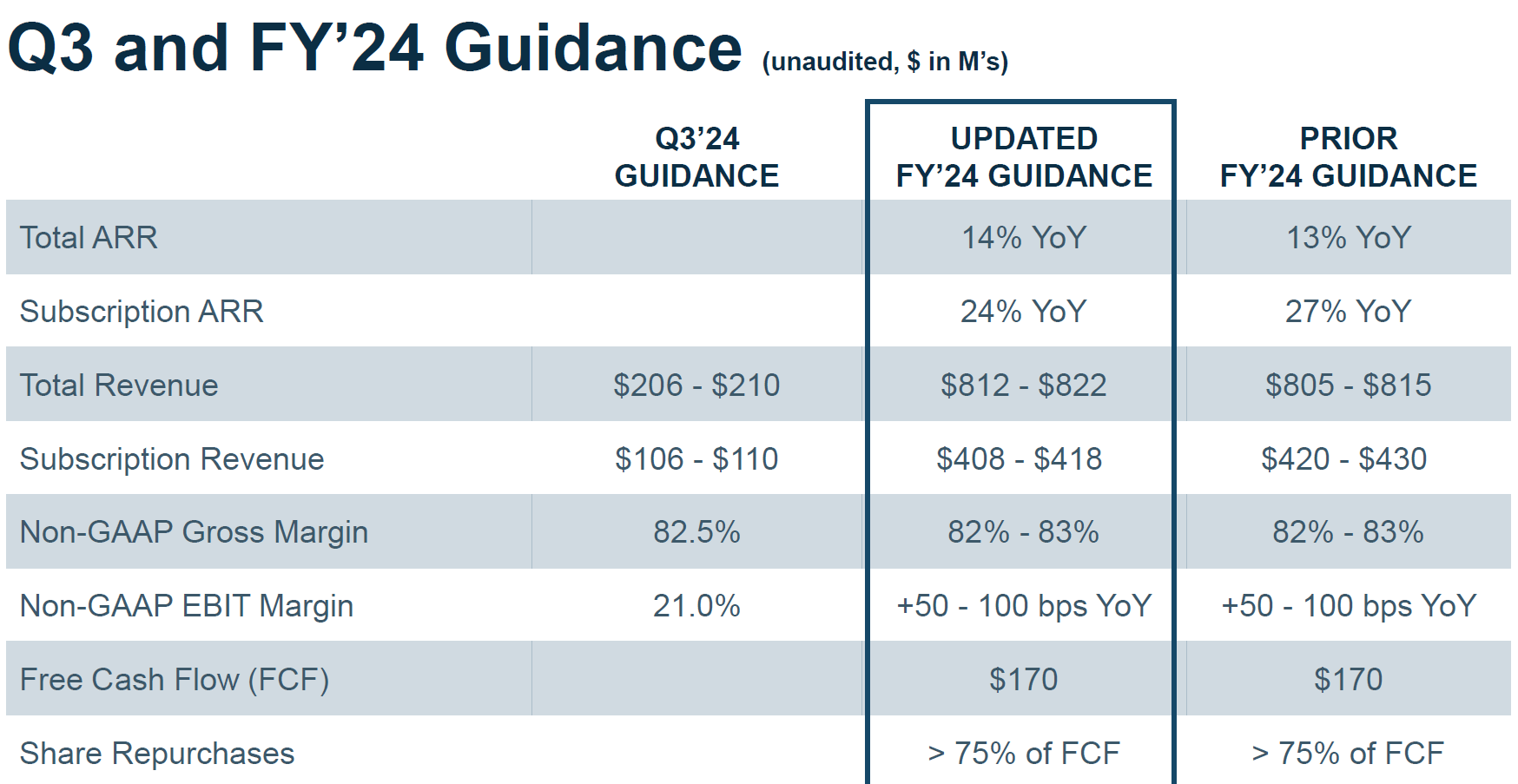

However, the Commvault management revised its guidance to reflect its view on mix shift.

{kind=link}

Our updated guidance reflects a mix shift from subscription revenue due to a lower number of conversions from perpetual support contracts to term software compared to the prior year, as well as continued measured spending for lower multi-year transactions in a relative high interest rate environment.

Source: Q2 2024 Earnings Call on Seeking Alpha

Investment positive: The data backup and recovery markets are poised to growth and Commvault has a reasonable position here

- Backup of enterprise workloads has become indispensable with the growth in data, remote working, and regulations.

- While players in this market offer hardware, a mix of hardware and software and software only solutions, we like Commvault’s high gross margin (80%+) profile.

- The executive team is ex-EMC, Dell, VMWare, and Arthur Anderson LLP

Investment challenge: Slowing transition to subscription

The Commvault management noted that they are seeing fewer conversions of existing perpetual support contracts to term software licenses. Furthermore, the average term of the subscriptions has reduced to two years. Lastly, the number of conversions were half versus the last year. The management attributes the slowness to macro factors and a shift in customer buying patterns.

The combination of these factors is likely to impact revenue in the near term. However, the management believes that the strength in the Metallic business is indicative of the broader positive around the uptake of Commvault’s offerings and hence quarterly variations should not be read too much into.

don't read into this in anything, but we're just looking at the pipeline and being very pragmatic about what the mix shift might be and that's it. I mean business -- we had a very good quarter, and we've raised ARR for the year, and we've raised revenue for the year. So, it's in my mind, as straightforward as a mix shift inside of the customer buying patterns, whether it be interest rate or where they are in their cloud migration journey.

Source: Q2 2024 Earnings Call on Seeking Alpha

While the management commentary looks consistent with the guidance, we find another aspect a bit more challenging.

{kind=link}

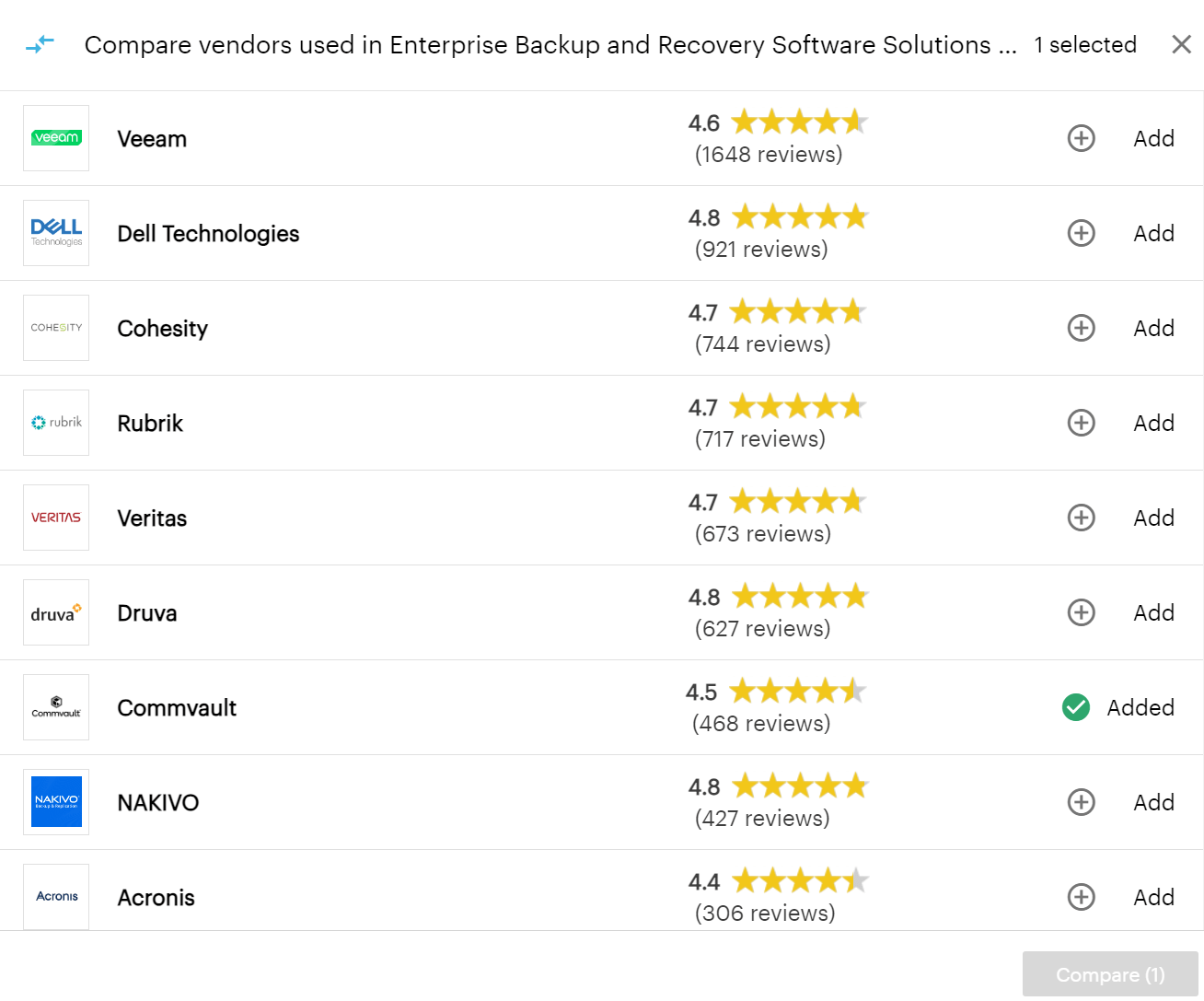

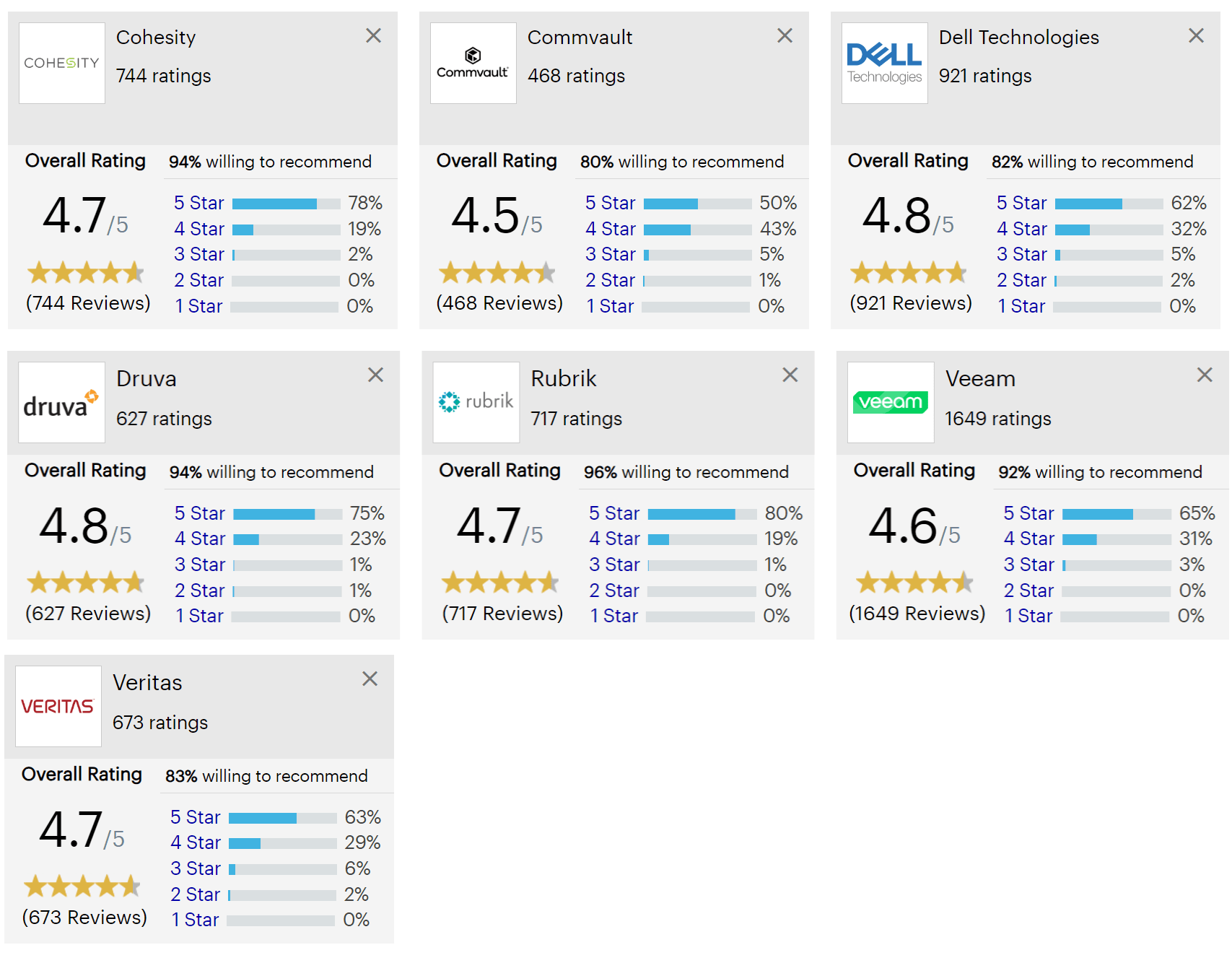

While looking at the comparison of vendors in the Gartner Magic Quadrant, two things stand out:

- Veeam, Dell Technologies, Cohesity, Rubrik, Veritas and Druva not only have higher rating than Commvault but also have a greater number of ratings. We think this points to greater mindshare these companies have been able to capture versus Commvault.

{kind=link}

- Furthermore, Commvault has the lowest percentage of its clients willing to recommend it at 80% or 370 odd reviewers – compared to it, every single peer has more clients willing to recommend. This implies peers are getting better referrals than Commvault, which then has led to reduced conversions.

we're on basically about half of the conversions that we did last year, which is just a transitional in the customer environment

Source: Q2 2024 Earnings Call on Seeking Alpha

We will be looking keenly at the Q3 2024 print and management commentary specifically around the issue of conversions. While the management narrative of Metallic picking up and helping drive growth in view of a declining on-premise base is attractive, we are worried about what customers are saying.

Valuation

The company trades at a P/S of 4.3x which is much lower than the 6-7x for most pure play SAAS companies. Despite Commvault delivering 80%+ gross margins, the valuation appears to be a function of its lower growth (c.5%) versus SAAS peers doing high teens and above.

Based on the investment concern highlighted above, coupled with the fact that the management expects margins to further contract as the transition to subscription follows through and revenues to also be hit in the near term due to the transition, we see limited upside in the stock.

At this point, we would not want to be an owner of the stock.

Outlook

We have highlighted our biggest concern about Commvault’s business: conversions to SAAS not happening due to peers having a greater referral push. In the same breath we would also want to discuss the company having a good management team and a $800 million business. We think while it might take a while, the company should focus on enhancing the customer experience, which then will help the tide on conversions and momentum (with much lower blips).

For further details see:

Commvault: Low Conversions Are A Concern