PPRUF - Compagnie Financière Richemont: Financials And Valuations Look Good Watch For Growth Slowdown

2023-06-22 01:12:31 ET

Summary

- Swiss luxury products stock Richemont's price has increased by 36% since November last year, with improved operating margins and strong sales growth in Asia Pacific as Chinese demand recovers.

- The company's forward price-to-earnings (P/E) ratio looks attractive compared to luxury peers, indicating a potential for further stock price growth.

- However, if sales in key markets like the US and Europe slow down more than expected, Richemont's earnings growth might be negatively impacted. So far though, this risk appears limited.

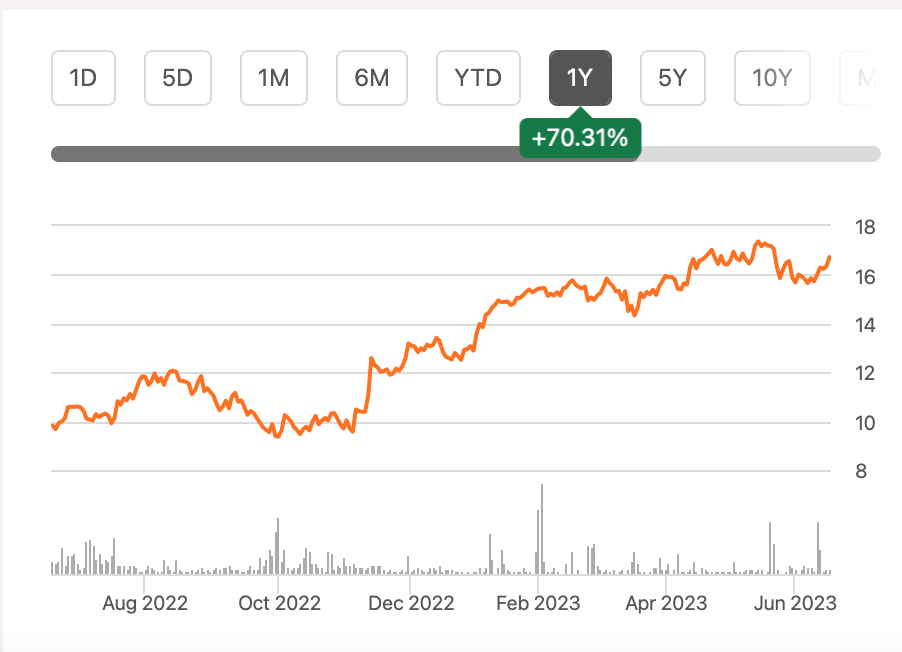

Since the time I upgraded the Swiss luxury products stock Compagnie Financière Richemont (CFRUY) to Buy from Hold in November last year, its price is up by 36%. The impetus for the rating upgrade was the sale of its controlling stake in the e-commerce portal Yoox Net-A-Porter (YNAP). As per my estimates, a notable positive effect on operating margins was likely because of this. At the time, the high inflation and CFRUY’s lagging operating margin compared to luxury peers put it at a particular disadvantage.

{kind=link}

Improved Operating Margins

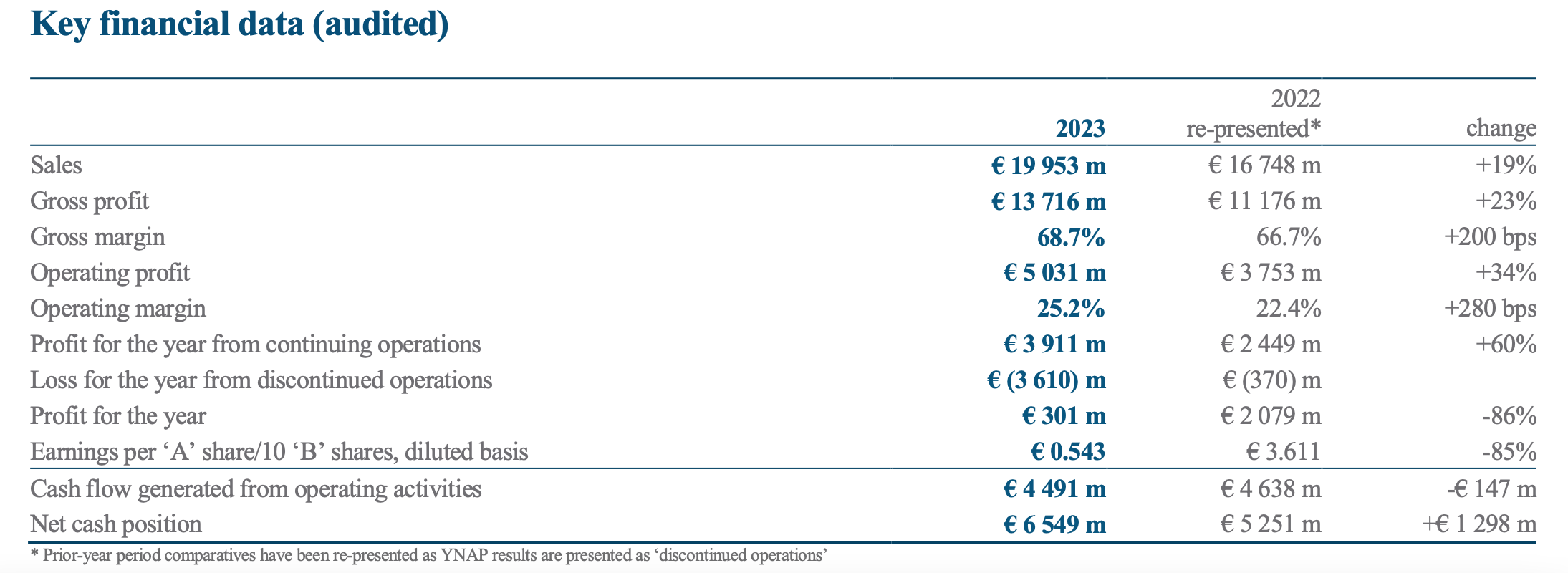

Cut to now , and the Cartier owner's operating margins for FY22 (financial year ending March 31, 2022) have been re-presented as 22.4%, after removing the influence of YNAP. This is just a shade higher than my expectations of around a 4 percentage point increase from the earlier 17.9%.

{kind=link}

But the real story here is the even bigger increase in margins seen for the latest financial year, FY23, at 25.2%. It still lags behind its luxury peers, to be sure. Hermès ( OTCPK:HESAY ) has the highest margins of 41.5% . But Richemont has come quite close to Kering ( OTCPK:PPRUY ) at 27.5% and LVMH ( OTCPK:LVMUY ) at 26.5% , as of their last financial year-end.

The operating margin has been a particularly important differentiator in a time of high inflation since it is a signifier of pricing power. It was hard to see companies with relatively limited ability to pass on costs as being able to retain or improve profitability in the environment. With inflation on the decline now, it is less significant from that perspective. It is still important otherwise, though, as a measure of profitability, which in turn can determine the future trajectory of a stock’s price.

Region wise sales encouraging

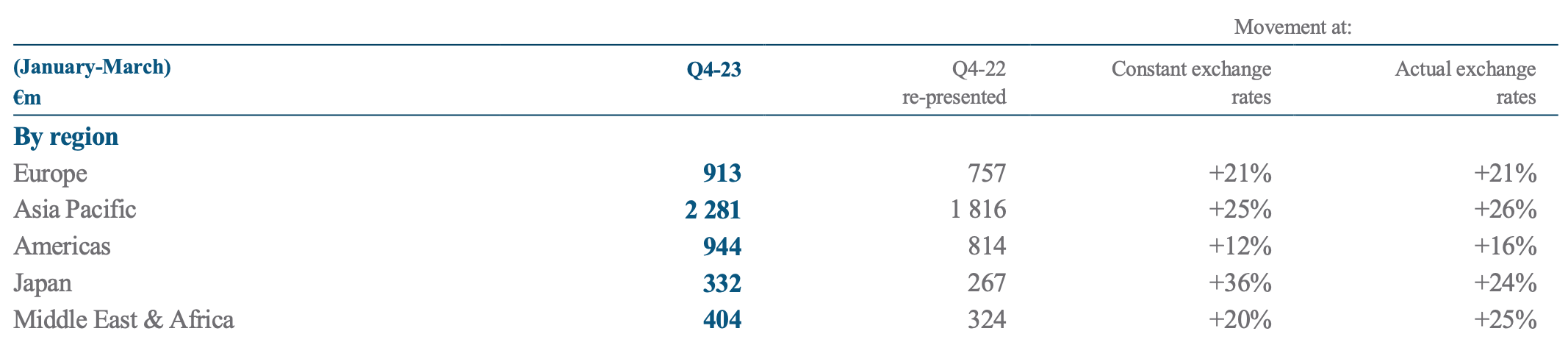

Looking at its latest financials encourages me that Richemont can strengthen its margins further. First, consider its revenue growth, which continued to be healthy at 19% in FY23 on a strong base of FY22 . But the really heartening fact is the recovery in its Asia Pacific [APAC] sales in the final quarter of FY23 (Q4 FY23), which factors in the return of demand from China. Sales to the region rose by a huge 26% year-on-year (YoY). This is particularly significant since APAC was a 40% contributor to the company’s sales in FY23.

Sales across markets (Source: Compagnie Financière Richemont)

{kind=link}

Also, it's notable that its Americas sales have seen healthy growth of 16% in Q4 FY23, even as they slowdown from the full-year growth figure of 27%. But there are two points to note here. One, the gap is wider at market exchange rates. At constant exchange rates growth in Q4 FY23 at 12% is just about slower than the 14% for FY23. Next, Richemont’s sales to the region have grown faster than what LVMH reported recently . LVMH of course has an interest in a bigger number of luxury segments than Richemont, which focuses on jewellery and watches, so they aren’t entirely comparable, but the comparison is still indicative.

The outlook

The key question now is whether Richemont can continue to grow fast. In talking about the outlook, the company’s Chairman, Johann Rupert, points out both risks and opportunities. In terms of risks, he says “Economic volatility and political uncertainty look set to remain features of the trading environment.”. In this context, “fluctuating levels of demand” are mentioned.

In terms of opportunities, he says “I am confident that our Maisons are well positioned to meet strong demand, notably driven by a significant resumption of Chinese travel.”. To me this says that while there are likely drags on growth, there are also balancing factors.

Analysts do, however, anticipate slowing down in revenue growth to 8.9% this year. This is not too bad, though, considering that this is a come-off from particularly strong growth in the past two years. Further, it is still higher than the average growth of 7% seen over the past decade.

Profit projections are also positive. The EPS is expected to increase by over 21.5% to USD 0.88, after declining in FY23 primarily due to the charge for YNAP as it's held for sale.

The market multiples

This yields a forward price-to-earnings (P/E) of 18.7x , which is attractive compared to its luxury peers. LVMH and Hermès are at 24.2x and 51.7x , respectively.

Similarly, even its twelve-month trailing [TTM] reported P/E of 22.1x looks good. For one, it hasn’t increased significantly from the 20x I had estimated it to be after it decided to hive off YNAP. Further, among its peers, it has a higher multiple than only Gucci owner Kering at 17.9x . LVMH and Hermès are far ahead at 31x and 62.3x respectively.

It is worth noting, that it looks competitive even compared to its median P/E of 27.7x over the past 10 years. This alone indicates an over 25% upside to CFRUY, even as it trades at near all-time highs.

The downside

The price upside will play out only assuming that everything goes as projected, though. If sales in the important US and European markets, that account for 44% of its revenues, slow down more than expected, Richemont’s earnings growth might get dented. Signs of a cooling off in demand are limited up to now, but sales to these markets need to be watched going forward to ascertain how FY23 will play out going forward.

What next?

So far though, Richemont is still a Buy for me. There is no doubt that its price looks very high in absolute terms from a historical standpoint. And if some of its key markets weaken significantly this year, both growth and profits can soften.

However, its revenues are likely to be steadied by solid demand from China. Its latest financials already show robust performance in the market in the last quarter of the year. Moreover, its Americas’ sales so far are doing relatively alright too.

Its earnings numbers are set to grow in 2023, which shows up favourably in its forward P/E ratio. Both its forward and TTM P/E look attractive compared to luxury peers and even its own historical levels. These along with its healthy financials indicate that CFRUY can rise further.

For further details see:

Compagnie Financière Richemont: Financials And Valuations Look Good, Watch For Growth Slowdown