CCU - Compania Cervecerias Unidas: Starting To Look Cheap Below 8x EV/EBITDA

2023-10-07 05:01:59 ET

Summary

- The company’s margins are showing improvement in 2023, with H1 EBITDA rising by 8.9% thanks to higher selling prices and a strong Chilean peso.

- In my view, EBITDA for the full year is likely to surpass 500 billion Chilean pesos ($545.4 million) despite the struggles of the wine business.

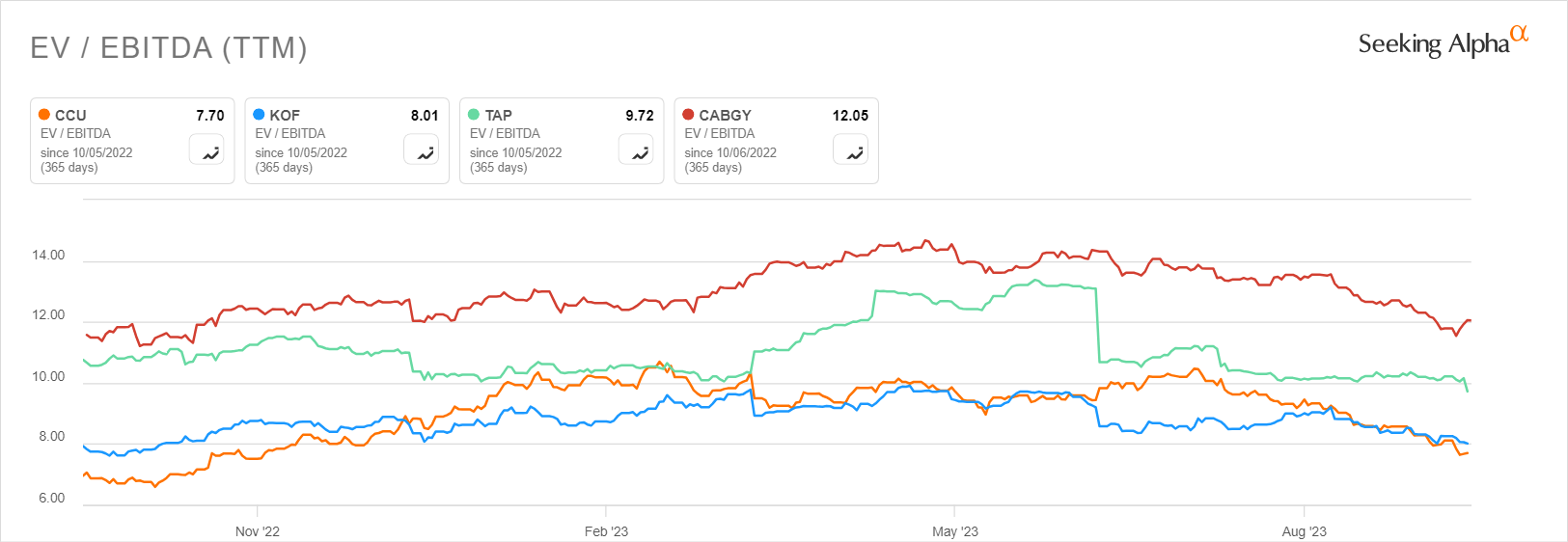

- CCU is trading at an EV/EBITDA ratio of 7.7x on a TTM basis and looks undervalued considering many of its peers are valued at above 9x EV/EBITDA.

Introduction

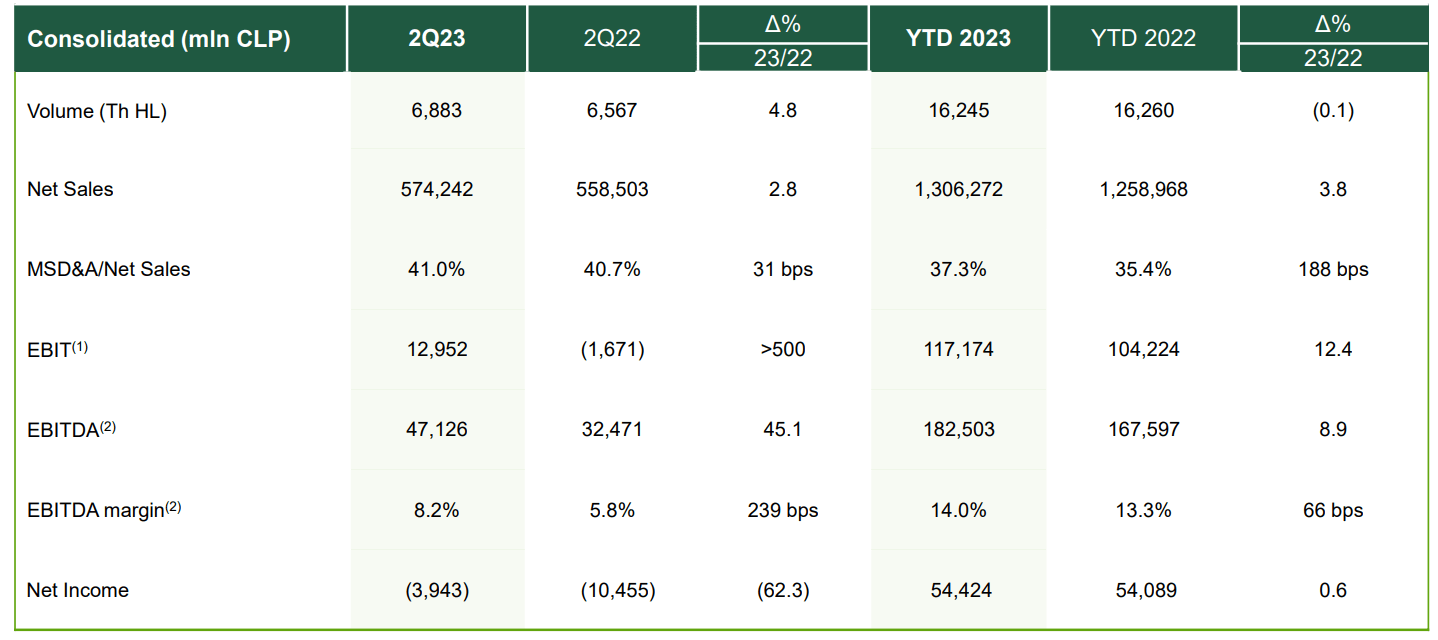

I work as an M&A analyst covering Latin America and over the past few months I've been surprised by the sharp decline in the market valuation of Chilean beverages group Compania Cervecerias Unidas (CCU). The company is currently experiencing headwinds at its wine division, but I think that its financial results for H1 2023 were strong, with net sales inching up by 3.8% year on year and EBITDA rising by 8.9% to 47.1 billion Chilean pesos ($51.4 million). The market capitalization by over a third since late July and I think that CCU is becoming cheap based on fundamentals compared to many of its peers. My rating on the stock is speculative buy. Let's review.

Overview of the business and financials

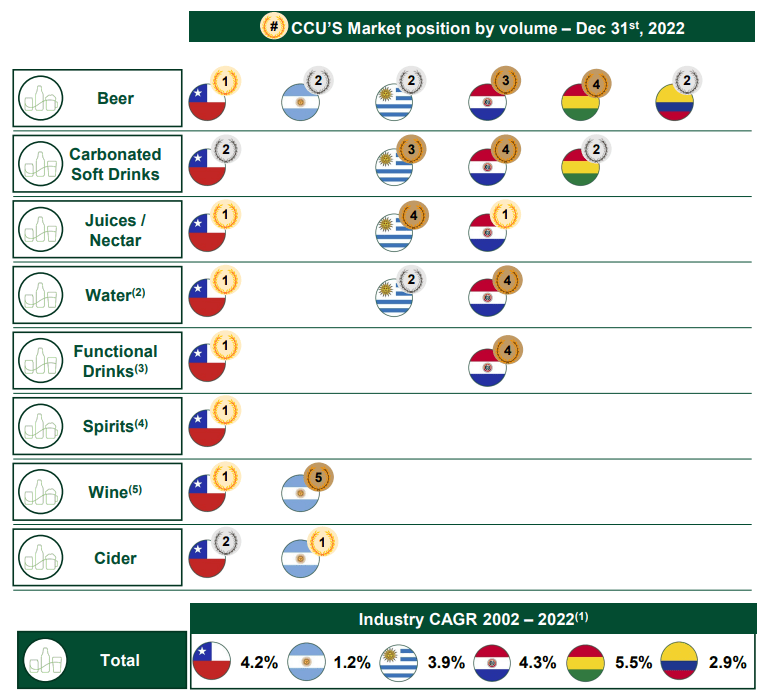

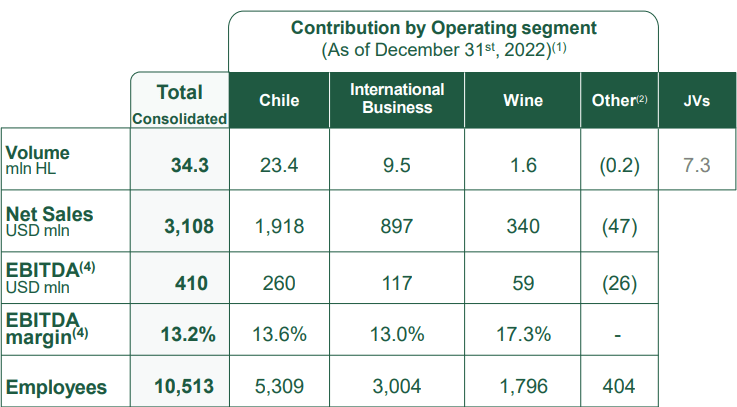

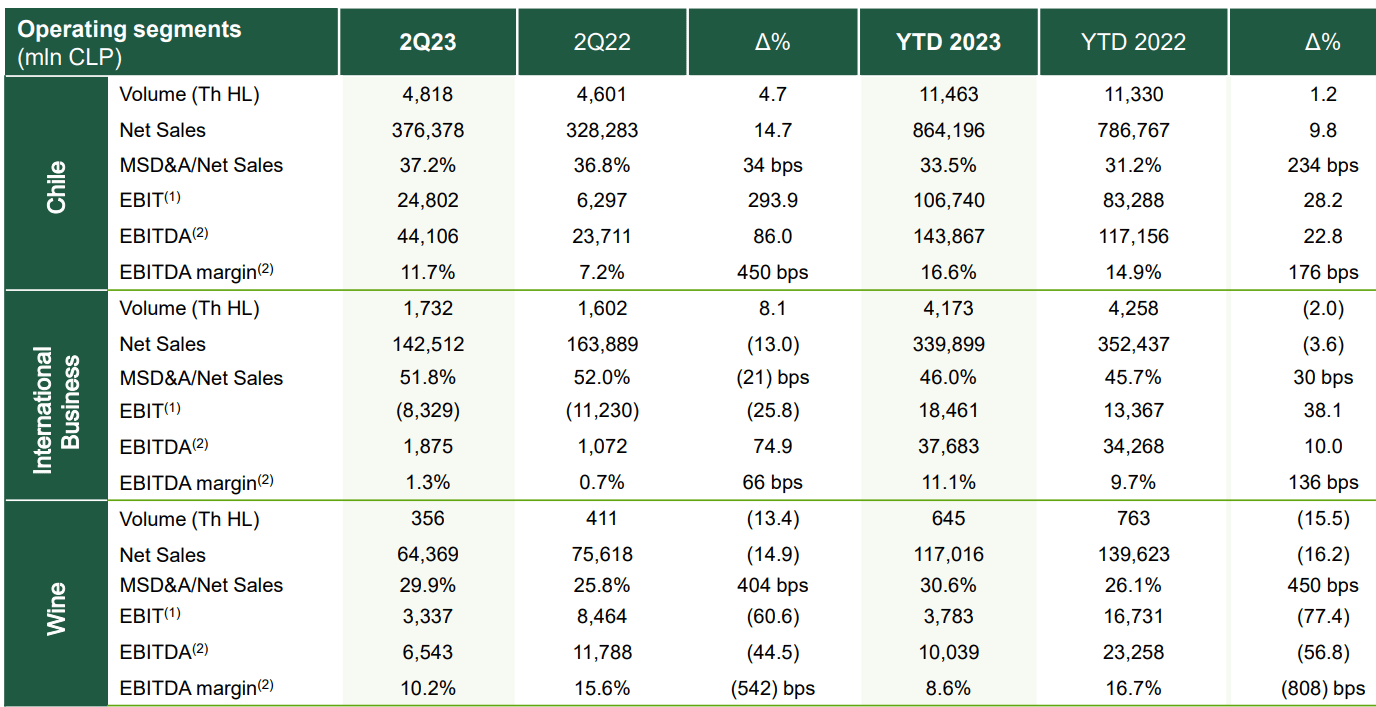

CCU was founded in 1850 and is the largest beer producer in Chile in terms of volume as well as a major player in several Latin American countries, including Argentina, Colombia, Uruguay, Paraguay, and Bolivia. It's also Chile's leading producer of fruit juices, bottled water, tea and energy drinks, spirits, and wine. Chile currently accounts for about two-thirds of net sales as well as EBITDA.

{kind=link}

{kind=link}

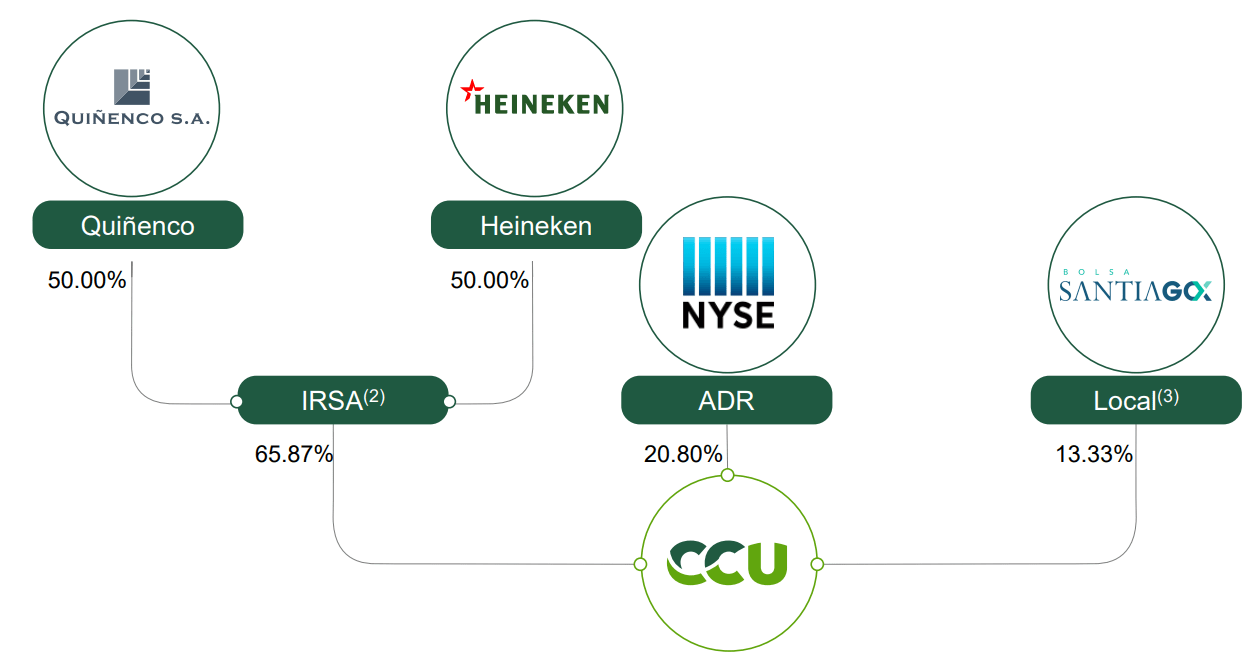

The company's majority shareholder is Inversiones y Rentas with a stake of 65.87% and the latter a 50:50 joint venture company of Dutch brewing giant Heineken ( HEINY ), and Chilean conglomerate Quinenco. CCU's shares are traded on the New York, and Santiago stock exchanges.

{kind=link}

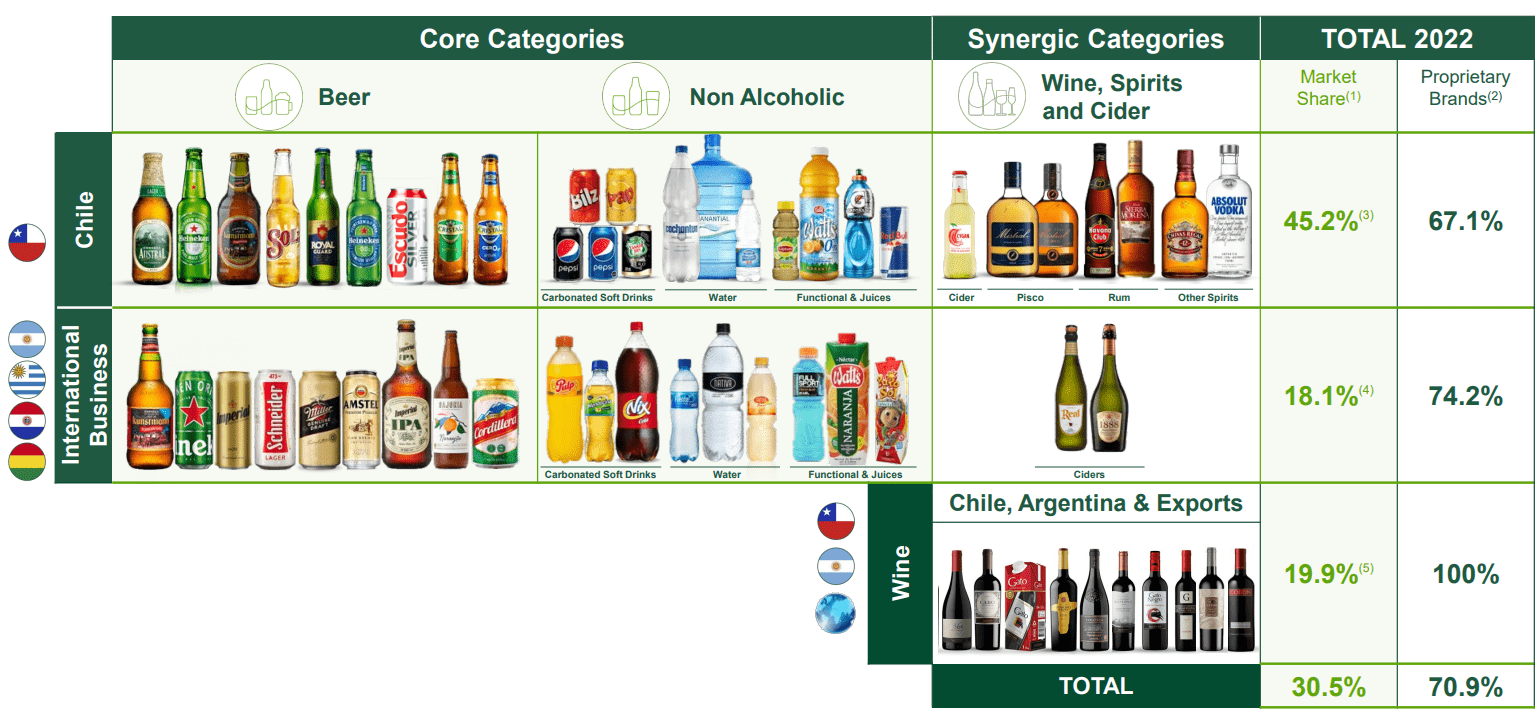

CCU's product portfolio comprises dozens of own brands as well as licensed and imported brands. The company currently has 35 productions plants and 50 distribution centers, and its products are sold across over 400,000 points of sale in Latin America (see slide 11 here ). In addition, it owns 50% of Colombian brewer Central Cervecera de Colombia.

{kind=link}

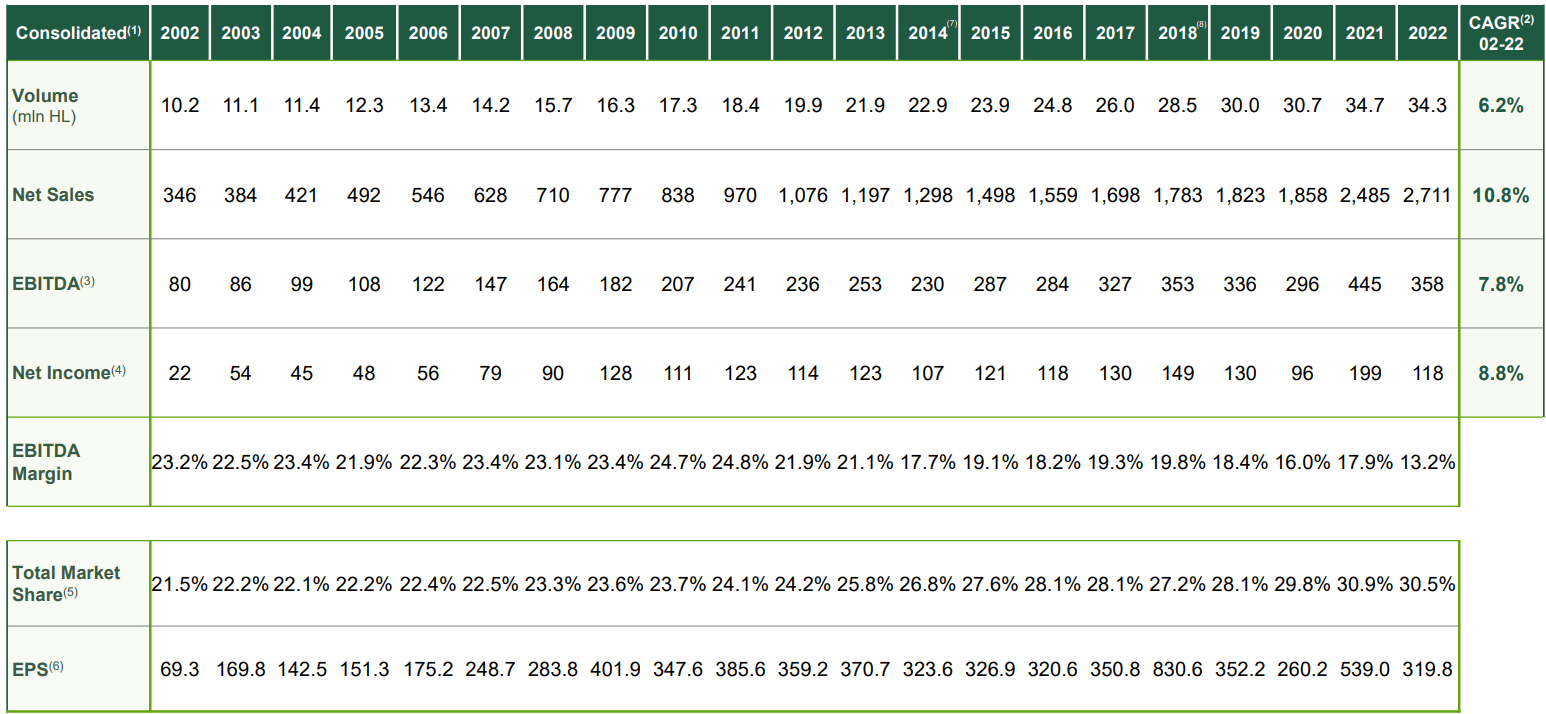

Looking at the financial performance of the business over the past two decades, we can see that the compound annual growth rate ((CAGR)) of net sales was a compelling 10.8% between 2002 and 2022 and there wasn't even a single year in which they decreased. However, it seems that economies of scale are lacking here as both EBITDA and net income had CAGR in the single digits during the period. Note that the numbers in the table below are in billions of Chilean pesos, except EPS which are in Chilean pesos.

{kind=link}

In 2022, EBITDA and net income were under pressure as CCU was unable to fully pass on cost inflation to consumers. Yet, this changed in H1 2023 as the EBITDA margin rose to 14% from 13.3% a year earlier despite volumes remaining flat. In addition, the gross margin expanded by 266 bps to 46.3% thanks to the strong Chilean peso.

{kind=link}

You also have to keep in mind that 2023 is shaping up as a particularly bad year for the Chilean wine sector due to weak demand from China. According to data from Wines of Chile , wine exports from the Latin American country came in at 20 million boxes and $584 million, which translates into a 24% decrease in both volume and value. Looking at the performance of CCU's wine business, volumes went down by 15.5% while net sales dipped by 16.2% year on year in H1 2023. Excluding this segment from CCU's financial results, EBITDA would have increased by 19.5% during the period.

{kind=link}

Overall, I think that 2023 is shaping up as a strong year for CCU as cost inflation is moderating and the company is improving margins thanks to higher selling prices. In my view, EBITDA for the full year is likely to surpass 500 billion Chilean pesos ($545.4 million).

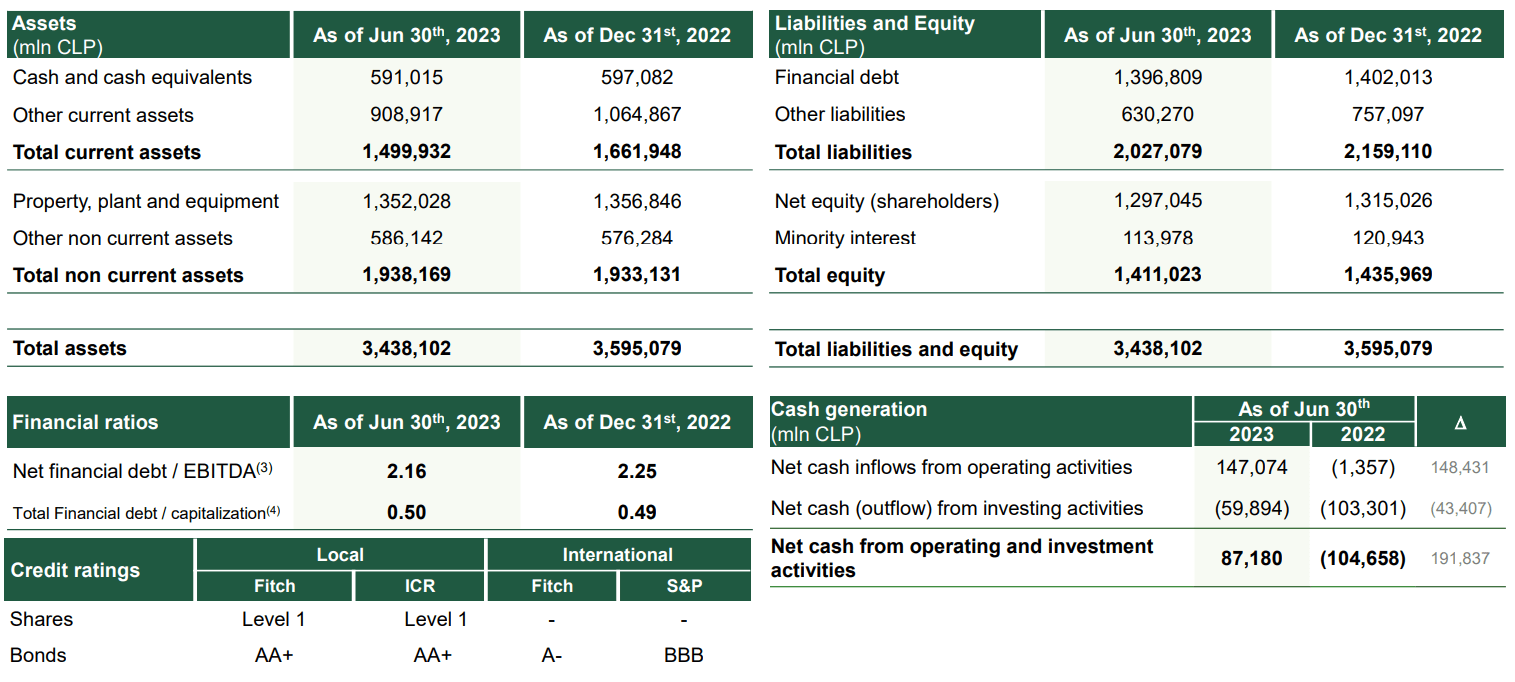

Turning our attention to the balance sheet, there was little change in the structure of assets and liabilities as CCU is limiting CAPEX in a bid to focus on profitable and sustainable growth. Free cash flow during H1 2023 was 87.2 billion pesos ($95.1 million) and the net financial debt/EBITDA ratio improved slightly to 2.16x thanks to the rising EBITDA. Overall, I think that CCU has a strong balance sheet, and its credit rating is unlikely to change in the near future.

{kind=link}

Turning our attention to the valuation, CCU has an enterprise value of $3.72 billion as of the time of writing and the company is trading at an EV/EBITDA ratio of 7.7x on a TTM basis. In my view, CCU should be worth at least 9x EV/adjusted EBITDA considering it has a strong balance sheet and a history of double-digit percentage net sales growth over the past two decades. This level doesn't seem high considering many major players in the beverages industry are trading at higher multiples as of the time of writing.

{kind=link}

Turning our attention to the downside risks, I think that the major one is that I could be wrong about the improvement of EBITDA for the full year. The economies of several countries in Latin America are experiencing macroeconomic headwinds and slow GDP growth and this could translate into lower beverages consumption over the coming months. In addition, the results of CCU could be negatively affected by the strengthening of the US dollar against the Chilean peso. Another risk here is that the wine sector in Chile could continue to struggle in 2024 due to weak demand from China.

Investor takeaway

Last year was tough for CCU as volumes were flat and margins were pressured by cost inflation. Yet, 2023 is shaping up to be better as the company has been successfully increasing selling prices while keeping volumes at the same level, resulting in a significant improvement in EBITDA despite the issues of the wine division. CCU's valuation is down to below 8x EV/EBITDA and I think this creates a buying opportunity as many of its competitors are trading above 9x EV/EBITDA.

For further details see:

Compania Cervecerias Unidas: Starting To Look Cheap Below 8x EV/EBITDA