BVN - Compania de Minas Buenaventura: A Major Share Price Opportunity Before Further Headwinds

2023-12-18 13:40:43 ET

Summary

- I give a Sell rating for Compañía de Minas Buenaventura S.A.A. due to recent whopping rise in stock price.

- BVN's sales heavily depend on the copper market, which is at risk due to weak near-term conditions and potential recession in the US.

- BVN's financial situation is not solid, and in general the production is not improving.

A “Sell” Rating on Compañía de Minas Buenaventura S.A.A.

This analysis suggests that retail investors take some profit from the investment in Compañía de Minas Buenaventura S.A.A. ( BVN ) – a Lima, Peru-based explorer and miner of copper, gold, and other metals across Peru – following the sharp rise in the stock price that has occurred recently.

Shares are hovering at the upper bound of the 52-week range of $6.45 to $12.73, as shares were trading at $12.50 as of this writing.

{kind=link}

The current high share price is the result of the interest rate break decided by the Federal Reserve after the meeting in mid-December 2023, as this decision increases analysts' expectations of a rosy outlook for the metals mined by BVN. However, according to this analysis, this decision by the Fed, which also expects the rate cutting policy to begin in 2024 (likely sometime in spring 2024), is not enough to completely eliminate the risk of weak near-term conditions for copper which is BVN’s main source of income. BVN depends on the copper market for more than 40% of sales. Further negative impacts are on track for copper demand as the economy in the US is expected to enter recession as early as 2024, while China's support for copper demand may be delayed as the economy is currently struggling with deflation and cannot be confident that it can use the help of its most important trading partners, the US and Europe. The latter economy is also struggling with a slowdown in consumption and investment due to the European Central Bank's hawkish stance on interest rates to combat elevated core inflation.

It must be said that a downturn in the economy will create headwinds for the value of portfolios, and gold - the second most important metal in BVN's portfolio - acting as a hedge, will instead experience strong demand in my view, likely driving the price per ounce significantly up from current levels. The positive impact of an increase in the gold price will be important to BVN's income - a key driver of the share price - but is still not considered sufficient to fully offset the negative fallout for copper stemming from the economic slowdown in western countries and the problems in China's real estate sector.

Gold represents a maximum of 35% of BVN's turnover. BVN produces other metals: silver, lead, and zinc, which together account for the remaining 20% of total turnover.

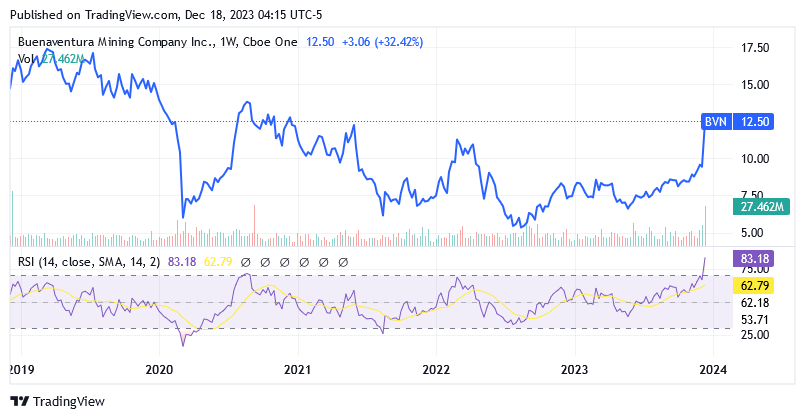

Holding BVN Does not pay in the Medium/Long Term

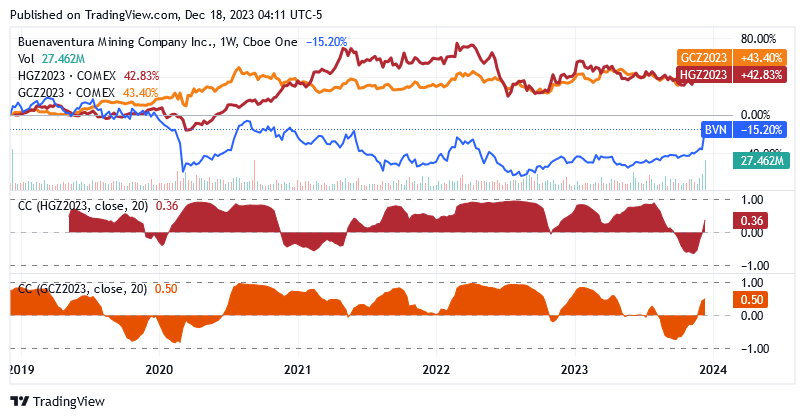

As shown in the chart below, a position in BVN is held with significant risk under a “Buy and Hold” investment approach.

The past 5 years of holding BVN would indicate that this investment returned -15.20%, significantly underperforming the SPDR® S&P 500 ETF Trust ( SPY ) which returned +80.19%, which is the benchmark for the US stock market. It also significantly underperformed the Materials Select Sector SPDR® Fund ETF ( XLB ), which returned +65.96%, which is the benchmark for the entire industry BVN operates in.

{kind=link}

Additionally, this stock pays a very small dividend of $0.073 which was paid for the full year on May 11, 2023.

The graph above also implies that if the retail investor may need the money stored in this stock to cover unforeseen expenses or because he wants to allocate to other securities, he bears the risk of ending up with a significant loss if the share price tumbles. This is quite possible with BVN as shares are exposed to the volatility of the metals markets, but while gold and copper have shown growth over the years through cycles, shares of BVN have instead shown a disappointing performance through cycles.

Gold and copper have been steadily rising for the following reasons: Uncertain global conditions due to increased geopolitical tensions and macroeconomic concerns are supporting increasing demand for gold for hedging purposes; while the demand for copper will continue to grow stronger in the future as a key element for projects promoting the electrification of economic activities and for other green technologies as part of global plans to avoid extreme impacts of climate change.

Based on the chart below: BVN reflects the volatility of copper and gold prices (since the stock price is positively correlated with the metals), but not the steady growth of the metals. This is a strong indication that the market does not have confidence in the portfolio of mineral activities and its growth prospects and is primarily using this stock to exploit the cycles in metal prices.

{kind=link}

As you can see in the lower part of the chart, the dark red area is a graphical representation of the strong positive correlation between BVN stock price and copper futures prices (HGZ2023). The dark yellow area is the graphical representation of the strong positive correlation between BVN stock price and gold futures prices (GCZ2023) over the last 5 years.

The correlation is positive because, in addition to an optimistic mood in the BVN share price, there is usually also an optimistic mood in the futures prices for copper and gold. Instead, if there is a bearish sentiment on the BVN stock price, there will also be a bearish sentiment on the copper and gold futures prices. Correlation measures whether market sentiment tends to converge or diverge between securities, regardless of their performance, which can also vary significantly from security to security. I believe the correlation is positive and strong in both cases because the graph of the correlation coefficient is almost always in the positive part of the “CC” subplot.

Current Peak Is also a Significant Peak (To Profit From) Relative to Recent Years

Against the risk of recession headwinds for copper in the near term that will certainly continue to inhibit steady growth in the share price, and given an insignificant dividend paid annually, I believe investors should sell shares of BVN and take advantage of the great opportunity with the share price near its 52-week high, which is also a significant peak compared to the last 5 years.

{kind=link}

After the divestment, the retail investor may want to allocate the funds in US bonds, which can generate good interest income (compared to the very small dividend paid by BVN), as fixed interest rates have also risen sharply due to the Fed's aggressive hawkish stance against elevated core inflation.

Amid growing distrust over the U.S. economic outlook, the 10-year U.S. Treasury yield has risen slightly since the start of the year as investors moved away in favor of shorter-term Treasury bonds or money market instruments. The 10-year Treasury bond is currently at 3.905%, which poses a higher investment risk than last year, but risk-for-risk, an investment in US bonds will always be better than BVN stock due to any uncertainties associated with the share price and the weak dividend, which is subject, among other things, to factors such as the volatility of the commodity markets.

BVN Operations and Financials for the First 9 Months of 2023: A General Decline in Metal Production and Weak Metal Prices Weigh on Sales and Net Income

As mentioned earlier, BVN's profitability depends on more than 40% on the price of copper and 30-35% on the price of gold. In addition, the company is also engaged in the exploration and mining of lead, zinc and silver.

On average, the price of copper remained unchanged year-on-year at $8,689 per metric tonne, while the price of gold increased 7% year-on-year to $1,925 per ounce in the first 9 months of 2023 . Prices for other metals performed as follows: silver rose 14% to $24.30 per ounce; zinc fell 46% to $2,152 per metric ton and lead fell 3% to $2,030 per metric ton. These metals together account for less than 20% of sales and net income.

Production instead performed in these terms: equity copper production (direct copper operations not from affiliated entities) and equity gold production (direct gold operations not from affiliated entities) amounted to 27,200 metric tonnes and 105,930 ounces respectively in the first nine months of the year 2023, reflecting +35% and -17% year-over-year. Equity silver from direct operations fell 21% year over year to 3.984 million ounces, equity lead from direct operations fell 61% year over year to 4,575 tonnes, and equity zinc from direct operations fell 66% year over year to 7,706 tonnes.

Production in Peru is affected by a) the need for more than-expected effort to access high-grade ore at the Tambomayo mine; b) the suspension of mining and processing of ore storage in late 2022 at the La Zanja mine; c) lower than previously identified treated ore at the Julcani mine; d) the ongoing transition to copper from polymetallic ore at the El Brocal mine. The latter operational event results in an ongoing ramp-up at El Brocal and growth in copper production.

The rise in gold prices and better copper production data were not enough to prevent a 1% year-on-year decline in total revenue to $570 million in the first 9 months of 2023. At the same time, EBITDA from direct operations increased by 27% year-over-year to $121.9 million.

However, for the first nine months of 2023, net profit from direct operations was $42.5 million, down 37.2% year-on-year, as net profit for the first nine months of 2022 was $67.7 million.

The Financial Situation Doesn’t Seem Solid Despite Positive Free Cash Flow

Net cash flows from operating activities were $155.5 million in the first nine months of 2023 compared to $11.2 million in the same period in 2022 and capital expenditures were $145.7 million compared to $93.2 million. Investments were higher due to higher allocations for the Yumpag project, part of the Uchucchacua underground polymetallic mine, which was restarted after operations ceased in 2021. The company is awaiting approval of an updated mine plan for the Uchucchacua mine by Peruvian authorities. Production and transportation to the Uchucchacua processing facility are expected to begin before the end of 2023.

Free cash flow improved to inflows of $9.8 million in the first nine months of 2023 compared to outflows of -$82 million first nine months of 2022.

Buenaventura's cash balance reached $221.8 million in the third quarter of 2023, but this represents a significant decrease from $253.9 million at the end of 2022. Instead, net debt increased to $493.7 million from $484.6 million at the end of 2022 and net debt currently has an average maturity of 2.7 years. The latter data is not favorable, considering that corporate loan interest rates are not expected to decline quickly from 2024, despite the Federal Reserve's rate-cutting policy. This situation creates a risk that BVN may need to raise capital when interest rates in the market are still expensive boding not favorably with its future profitability.

Overall, BVN's balance sheet is not optimal from a financial solvency perspective, as shown by the Altman Z-Score of 1.73 (scroll down to the "Risk" section on this page of Seeking Alpha ), which means that BVN is in a distress zone, suggesting the company could face bankruptcy risk within a few years.

In addition, the debt outstanding in the third quarter of 2023 caused a 12-month interest expense of $50.1 million , which is not covered by the 12-month operating profit, as the latter represents a loss of $40.2 million .

Operating income divided by interest expense forms the interest coverage ratio and investors aim for a minimum acceptable level of 1.5x. This means that any value below 1.5 or negative indicates that the company is unable to generate income to pay the interest expenses incurred due to the debt.

BVN Stock Price: Generous Market Valuation Against the Prospects

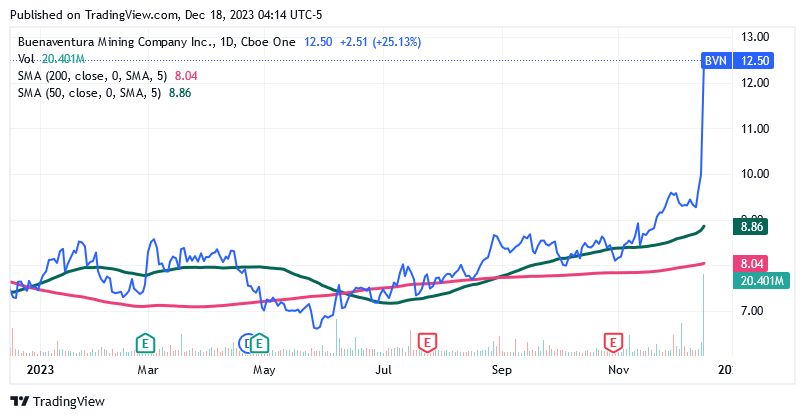

As of this writing shares were trading at $12.50 per unit giving it a market cap of $3.17 billion, and a 12-month dividend yield of 0.58%.

Following the recent sharp rise, shares are trading well above their 200-day simple moving average of $8.04 and well above their 50-day SMA of $8.86. Shares are also well above the $9.59 midpoint in the 52-week range of $6.45 to $12.73.

{kind=link}

For the reasons set out at the top of this article, together with the fact that operations are in general struggling to produce higher volumes of metals and a financial base that does not currently appear to be sound enough to support expectations of a significant upgrade to the mineral portfolio, retail investors may want to profit from historically high valuations and sell some shares.

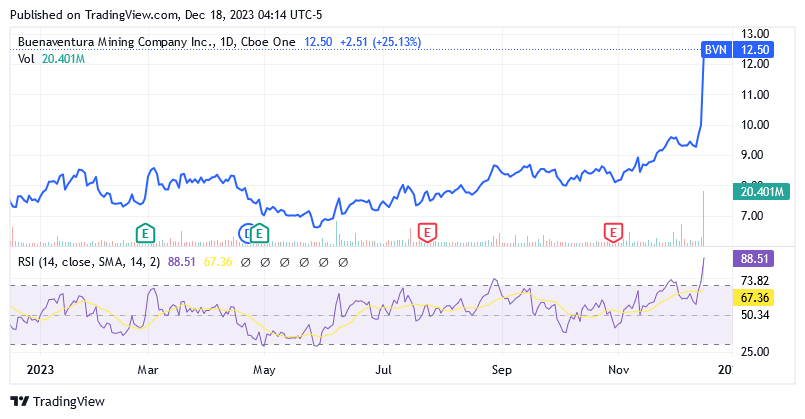

Additionally, the 14-day Relative Strength Indicator at 88.51 signals an overbought level, meaning there is no room technically for further rise from this level in my view.

{kind=link}

BVN also currently has a very high valuation in terms of EV/EBITDA ((TTM)). BVN's ratio stands at 29.86x compared to the industry average of 9.14x, supporting the thesis that current market valuations are seen as levels to exploit and take profits. This ratio is highly valued by investors because it is the best measure to reflect the profitability of capital-intensive industries such as metal mining and exploration activities.

The recession winds will be very favorable for gold as the precious metal serves as a safe haven during events that can cause severe headaches to investors' portfolios, and a possible gold bull market is good for BVN's income and share price. Despite this, BVN is not as well known in the gold production market as it is in base metals production market, and in particular copper production, on which its income is largely dependent. The interest rate cut is seen as positive for copper demand as investors associate it with a recovery in investment in the industrial sector. However, retail investors should be aware that the impact of the rate cut on capital markets will not be felt quickly, while previous rate hikes will continue to impact copper demand amid recessionary headwinds.

These economists , along with the inverted yield curve for 10- to 3-month US Treasuries’ spread, predict that a recession will hit the economy as early as 2024. In this sense there are already numerous signs of a slowdown in consumption through declining profits (actuals) and lower sales (forecasts) from major US retailers, as well as signs of a slowdown in investment activity as evidenced by Morgan Stanley's ( MS ) Q3 2023 data on IPOs and M&A.

As soon as weaker consumption and investment are accompanied by a deterioration in working conditions, one can speak of a recession. The latter is a negative cycle resulting from sharp increases in financing costs to combat inflation. As reported in this Seeking Alpha article , recent readings from Challenger, Gray and Christmas, Inc., the Automatic Data Processing, Inc., and the U.S. Bureau of Labor Statistics report on nonfarm pay growth in November indicated worsening working conditions.

The downturn in the economic cycle will weigh on demand for copper, as this base metal is used in many everyday product categories. Higher borrowing costs will continue to impact the growth plans of companies looking to invest in renewable and environmentally friendly projects. While China's measures to upgrade and strengthen the domestic infrastructure could have a positive impact on demand for copper and other base metals by offsetting the real estate sector crisis, the positive impact will not be as immediate as market participants currently expect. It will likely take time for these government measures to make their positive contribution to the economic cycle, which is still struggling after three years of restrictions and lockdowns against COVID-19 and now with deflation problems that could trigger a vicious circle, among other things. If people and companies delay purchases and investments because they expect even lower prices to emerge, that may not be good for short-term demand for copper and other base metals either.

Conclusion

BVN faces several headwinds that outweigh the positives that could emerge from a potential gold bull market. In addition, the stock does not seem to have a solid financial base to significantly improve production, which, on the contrary, has deteriorated for most metals.

This analysis assumes that the investor should not miss the opportunity to sell at these prices, and should not take the risk of keeping both feet in this stock, which also tends not to grow over time and does not pay satisfactory dividends.

For further details see:

Compania de Minas Buenaventura: A Major Share Price Opportunity Before Further Headwinds