SMTGF - Comparing Enphase With Its European Competitor SMA Solar Technology AG

2024-01-21 01:38:04 ET

Summary

- SMA Solar Technology has been added to the list of most sustainable corporations in the world in the most recent list published by Corporate Knights.

- The company offers a range of clean energy products and services, including solar inverters, energy management, electric vehicle charging solutions, and hydrogen projects.

- SMA Solar's financials have improved significantly, with expectations of rapid growth in various business segments, while maintaining a solid balance sheet.

We took a look at the recently published Global 100 list of most sustainable corporations according to Corporate Knights, and we noticed a new addition in the tenth position, SMA Solar Technology AG ( OTCPK:SMTGF )( OTCPK:SMTGY ), which sounded familiar. We had forgotten about this European renewable energy company since it had a spotty profitability track record and we just assumed that the inverter market was now basically dominated by Enphase Energy ( ENPH ) and SolarEdge ( SEDG ). However, when we took a closer look, we were impressed by the progress SMA Solar has made, and the fact that its valuation looks very reasonable while offering exposure to similar markets as Enphase and SolarEdge. This motivated us to take a small starter position in the company.

We are also surprised that the company is not talked about more often, given that its ten-year total return performance has actually been pretty decent. While the company has trailed Enphase, it has outperformed SolarEdge and has trounced ETFs like the iShares Global Clean Energy ETF ( ICLN ) and the Invesco Solar ETF ( TAN ).

Company Overview

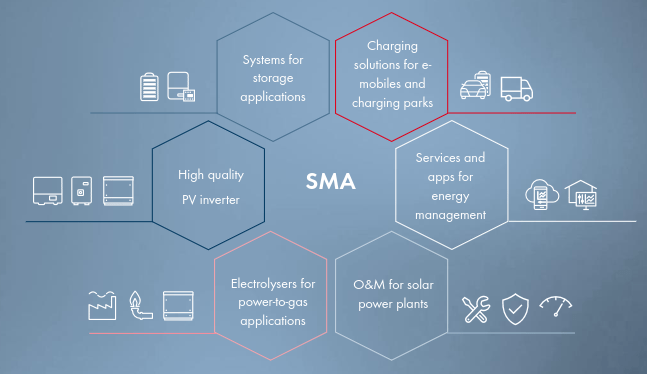

SMA defines itself as an "energy transition" company, which is probably fair given that it offers a number of clean energy products and services that help transition the world towards a more sustainable future.

The company is probably best known as a solar inverter company, but similar to Enphase and SolarEdge, it has been increasingly expanding the scope of its ambitions to include more energy management products and services. The company boasts of having an installed base of over 120 GW of solar inverters installed in 190 countries, and has a strong position in the residential market, the commercial and industrial market, and in large-scale projects. The company is close to finishing a new factory which should almost double its annual production capacity to 40 GW by 2025.

SMA also has a subsidiary that offers charging solutions for electric vehicles, and another subsidiary that develops hydrogen projects, having already completed about fifty projects with a total output of more than 500 MW. SMA is also a leader in the integration and management of battery energy storage systems (BESS) in complex energy projects. In other words, SMA is following a strategy of offering complete renewable energy solutions to customers, which seems to have strengthened its competitive moat.

SMA Solar Technology Investor Presentation

{kind=link}

The company is expecting rapid growth in the business segments where it operates, with PV inverters remaining an important part of the mix closely followed by battery solutions, but other segments contributing significantly to growth too, and becoming more relevant. On average, it expects these markets to grow with a roughly 21% CAGR through 2026.

SMA Solar Technology Investor Presentation

Financials

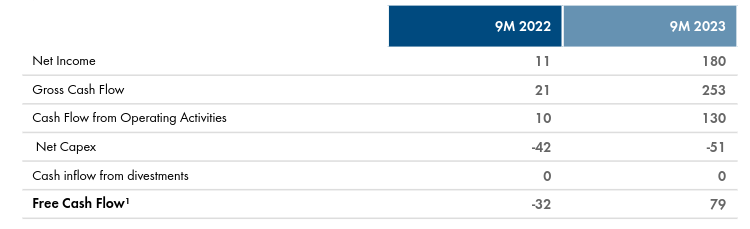

Financial results have improved significantly, but it remains to be seen if the improvements can be sustained. In any case, profitability rose to 180 million Euros in the first nine months of 2023, compared to only 11 million Euros in the corresponding period of 2022. Despite increased CapEx compared to the previous year, the company managed to turn its free cash flow around, to 79 million Euros.

SMA Solar Technology Investor Presentation

{kind=link}

While SMA's gross margin is clearly improving, it still lags behind Enphase's. It is impressive that its gross margin is now more than 10% above its ten-year average, but it still has a lot of work to do to close the gap with Enphase.

Growth

Enphase's revenue growth has been spectacular in recent years, but recently something interesting has happened. SMA has finally started delivering rapid growth, at the same time that Enphase is showing difficulty maintaining its previous growth.

This could be another sign of SMA's turnaround, and that maybe it is recapturing previously lost market share.

Balance Sheet

Both companies have very solid balance sheets, with SMA carrying basically no long-term debt and a net cash position of ~$300 million. Meanwhile, Enphase does carry about $1.8 billion in debt, but most of it is offset by cash and short-term investments of almost $1.3 billion. The net debt is quite manageable given Enphase's current EBITDA of almost $700 million, which puts net debt to EBITDA at less than 1x.

Similarities and Differences

One big similarity between the two companies is that both are increasing the scope of their services, going from being solar inverter companies to energy management companies. As they increase their scope, they are able to increase the revenue they can generate per project, adding high-margin software and management services into the mix.

{kind=link}

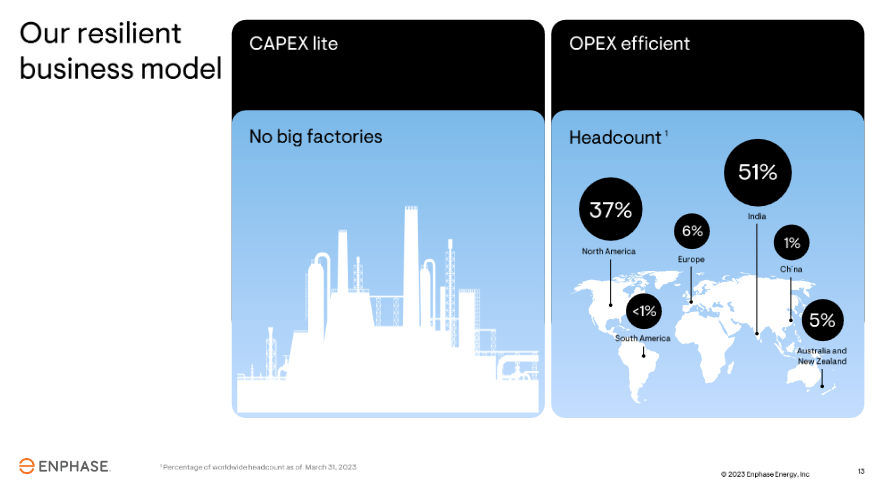

One significant difference is that Enphase has followed a CapEx-lite model with no big factories and a significant portion of its headcount in countries that have lower wages on average. For example, one investor slide shows that it has about 51% of its employees based out of India. This model has worked well for the company so far but comes with some risks as well. For example, some countries are starting to condition clean energy incentives to local manufacturing. Wages are also rising more rapidly in emerging economies, which means this headcount distribution advantage could erode over time.

{kind=link}

Outlook

In general, the outlook for both companies is very positive due to a strong international and local push for renewable energy. SMA Solar in particular is set to benefit significantly from German and European programs. The United States is also incentivizing renewable energy through the Inflation Reduction Act.

SMA Solar Technology Investor Presentation

{kind=link}

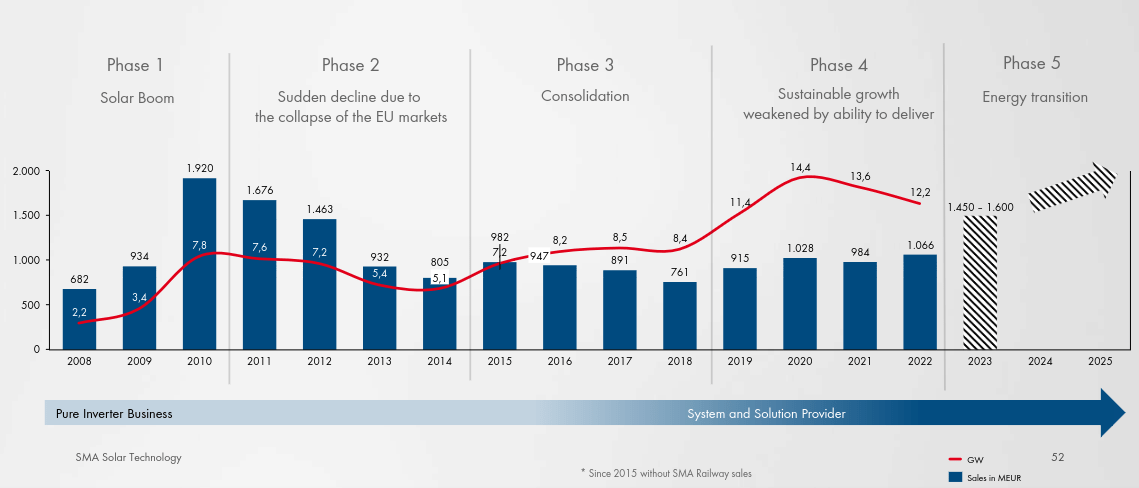

Expectations are for their end markets to roughly double by 2026 when compared to 2022. According to SMA Solar, we are entering the fifth phase in their industry's evolution. This new phase should be characterized by more profitable and sustainable growth, compared to the initial solar boom that was overly dependent on subsidies, which were quickly retired after the financial crisis. What followed were tough years for the industry, where most companies experienced losses, and it was a period of industry consolidation. More recently the industry has seen more sustainable growth but was hesitant on expanding too quickly. If the company is right, we could be entering a new phase with reduced production costs, higher production capacity, and exponentially growing demand.

SMA Solar Technology Investor Presentation

{kind=link}

There have been some positive signs, for example, SMA increased its full-year 2023 guidance three times. It also shared that it expects continued strong revenue growth and profitability in the fourth quarter. The order backlog remains elevated but did come down in the third quarter, which should moderate our enthusiasm.

SMA Solar Technology Investor Presentation

Valuation

Perhaps the most compelling reason to take the time to analyze SMA Solar Technology is that it is currently trading at a very attractive valuation, despite the size of the opportunity. Its price/book multiple is lower than its five-year average, despite its recent profitability improvements. It is also a fraction of the price/book multiple at which Enphase trades.

More importantly, its price/earnings is extremely low, at roughly 7.7x, compared to Enphase's ~27x. Such a low price/earnings multiple shows heavy skepticism from investors that the company can grow, or even just maintain its current profitability.

This is despite management sounding quite optimistic about their growth prospects, significant industry tailwinds, and clear gross margin improvements.

Another valuation metric hinting at severe undervaluation is the EV/Revenues multiple, which is around 0.86x for SMA, a significant discount to its historical average, and much lower compared to Enphase's more than 5x.

Finally, the price to cash flow from operations is less than 12x for SMA, and around 17x for Enphase. Both companies are trading at significant discounts to their historical averages, despite the current tailwinds in their industry.

Risks

The solar industry has been notoriously cyclical, and heavily dependent on subsidies in the past. That appears to be changing, as the cost of wind and solar energy is now often lower compared to alternatives like electricity from natural gas-powered plants. Industry consolidation has also strengthened the remaining companies, and difficult times forced them to become more efficient and adaptive. The risks are mitigated by the companies' strong brands and solid balance sheets.

The biggest risk we see with Enphase is that the valuation remains relatively elevated, even after a significant share price decrease. With SMA Solar Technology, the biggest risk we see is that its gross margins are still considerably lower compared to Enphase's, which makes it vulnerable to a pricing war for market share.

Conclusion

Investors should be paying more attention to SMA Solar Technology, which is showing signs of a successful turnaround, and reigniting growth. The global market for PV inverters and complementary energy solutions is expected to more than double by 2026 when compared to 2022. This means there is an opportunity for both SMA Solar and Enphase to significantly increase sales. We also like their new strategy of offering complete energy solutions, and not just solar inverters. This gives them added differentiation and opens the door to high-margin opportunities selling software and services. As such, we are maintaining our 'Hold' rating of Enphase, given the still relatively high valuation, and we are starting SMA Solar Technology with a 'Buy' rating given that it is trading at low valuation multiples despite clear signs that its profitability is improving.

For further details see:

Comparing Enphase With Its European Competitor SMA Solar Technology AG