PMT - Comparing PennyMac Pfd C And Its New Note

2024-01-17 09:45:00 ET

Summary

- mREITs like PennyMac Mortgage Investment Trust may perform well if the US returns to a normal yield curve without a recession.

- PennyMac Mortgage Investment Trust is a specialty finance company that primarily invests in mortgage-related assets. Higher interest rates on mortgages are impacting the origination of new mortgages, but PMT has.

- With limited default risk and yields over 8.4%, plus some Call protection, both PMTU and PMT.PR.C get a Buy rating.

Introduction

REITs and especially mREITs, should do well if the US can return to a normal up-sloping yield curve without the economy slipping into a recession which would increase late or skipped payments from mortgagees. Investors who believe the first will occur and the second won’t should own mREITs like PennyMac Mortgage Investment Trust ( PMT ). With its recent issuing of a Note, investors have two fixed-rate security types to pick from, both of which I covered recently in separate articles: links provided later.

- PennyMac Mortgage Investment Trust 6.75% RED PFD C ( PMT.PR.C )

- PennyMac Mortgage Investment Trust NT 8.5% 28 ( PMTU )

I like the yields available and see no risk of default, thus I give both issues a Buy rating.

PennyMac Mortgage Investment Trust review

A good due diligence for any Note or Preferred stock should start with an examination of the Issuer. A good income stream becomes meaningless if the company cannot redeem the Note or Preferred stock.

This is how Seeking Alpha describes this mREIT (abbreviated):

PennyMac Mortgage Investment Trust, a specialty finance company, primarily invests in mortgage-related assets in the United States. It operates through four segments: Credit Sensitive Strategies, Interest Rate Sensitive Strategies, Correspondent Production, and Corporate. The company’s Credit Sensitive Strategies segment invests in credit risk transfer agreements. Its Interest Rate Sensitive Strategies segment engages in investing in mortgage servicing rights, excess servicing spreads, and agency and senior non-agency mortgage-backed securities (MBS). The company’s Correspondent Production segment is involved in purchasing, pooling, and reselling newly originated prime credit residential loans directly or in the form of MBS. PennyMac Mortgage Investment Trust was founded in 2009.

Source: seekingalpha.com PMT

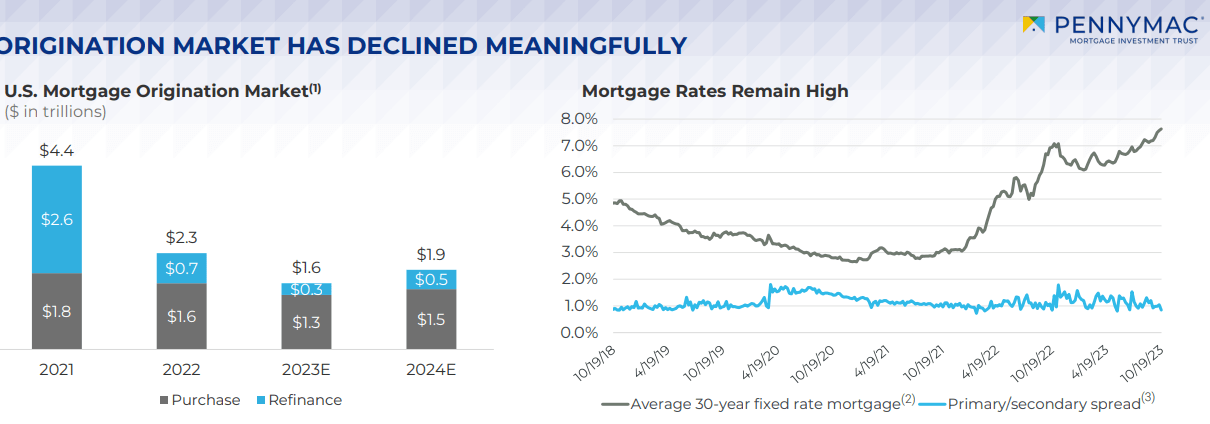

PennyMac's recent 3rd quarter report included this chart showing interest-rate movement and the effect on mortgage creation.

{kind=link}

Higher interest rates on mortgages are hurting the origination of new mortgages in two ways. First, new buyers cannot afford payments. Second, folks with sub-5% mortgages aren't selling or refinancing. On the positive side for mREITs, mortgage prepayments are down; such activity cuts into the mREIT's profit margin.

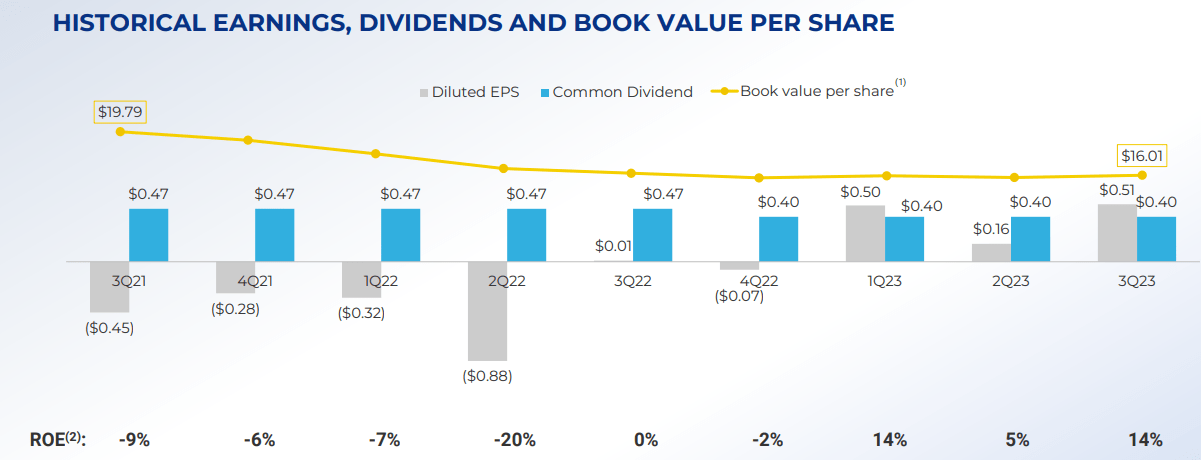

Approximately 70% of PMT’s shareholders’ equity supports seasoned investments in Mortgage Servicing Rights or MSRs. PMT’s book value per share seems to be stabilizing and for the third straight quarter, PMT turned a profit, both good signs for investors.

{kind=link}

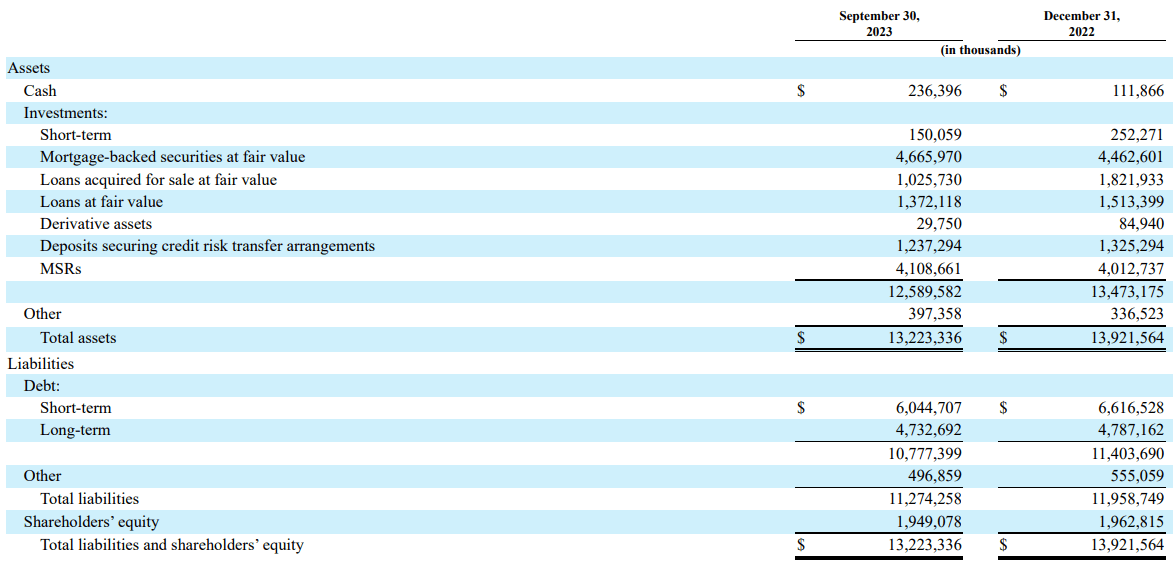

PMT has shown a small decrease in shareholders' equity since the end of 2022, but with the Notes and Preferreds under $600m combined, there is still plenty of coverage.

d18rn0p25nwr6d.cloudfront 10-Q

{kind=link}

To summarize, I feel there is no default risk holding the PMT Notes or any of their Preferreds. Both non-reviewed Preferreds have a unique risk that is mentioned later.

PMT NT 8.5% 28 and PFD C reviews

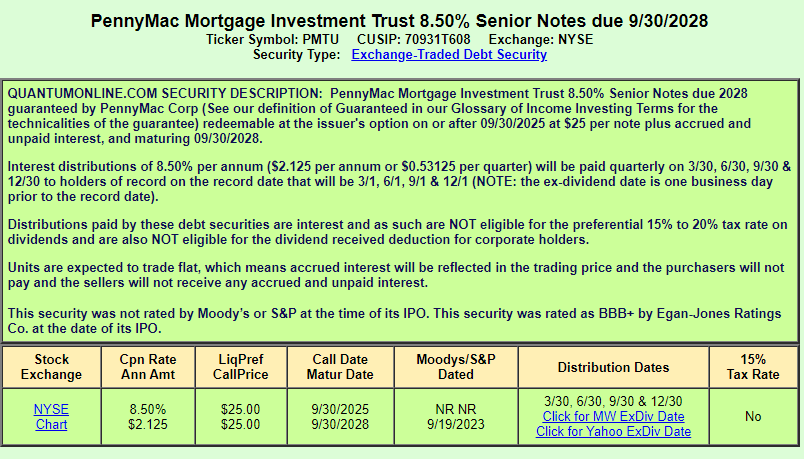

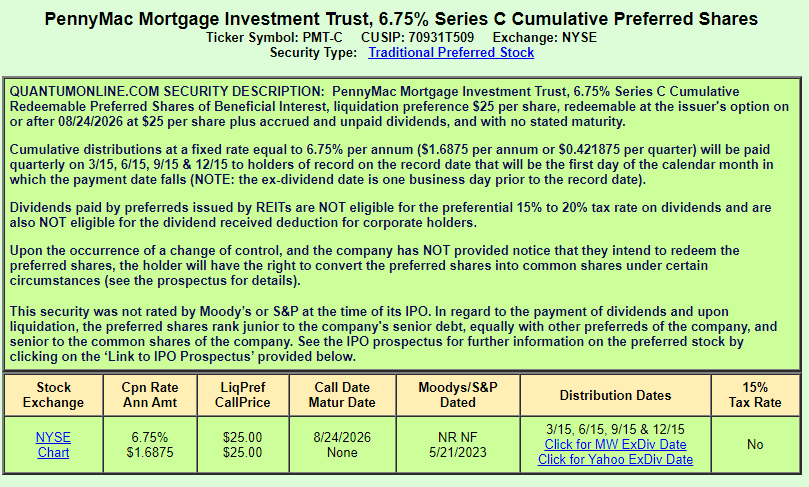

As I usually do, I turned to my Quantumonline.com for an overview description on fixed income assets.

quantumonline.com Note quantumonline.com PFD-C

{kind=link}

{kind=link}

Similar features include:

- Both are cumulative though skipping a Note payment would require a bankruptcy filing.

- Both are fixed-rate assets.

- Neither is eligible for the 15% tax rate on income.

For the more conservative amongst us, the Notes have some advantages over the Preferred stock:

- They are higher in the capital structure than the Preferreds, lowering the odds of any default damage.

- Payments have greater legal protection being debt, not stock.

- They have a higher fixed coupon rate.

- They have a maturity date, though not every investor might see that as positive.

The biggest two negative I see in the comparison are:

- The Call date on the Note is sooner than the PFD C's.

- With a higher fixed coupon, the Note would be Called before the PFD C. PMT has two now non-floating Preferreds that will play into that Call hierarchy too.

Portfolio strategy

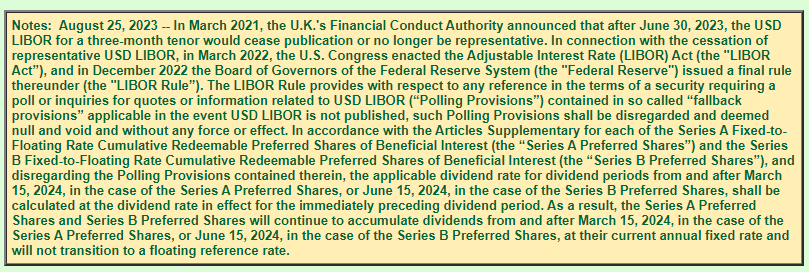

While this article's purpose was comparing both fixed-rate assets, PMT does had two floating-rate Preferreds, but as How PennyMac Is Hurting Their Preferred Shareholders article explains, PMT has said they won't and will keep their fixed-rate instead. Here is the explanation I found for their action.

{kind=link}

Based on that, I will treat them as fixed. The floating coupon was originally listed as 3-mo LIBOR + 5.99% for both.

| Factor |

| Note |

| PFD C |

| PFD A |

| PFD B |

| Call Date |

| 9/30/25 |

| 8/24/26 |

| 3/15/24 |

| 6/15/24 |

| Coupon |

| 8.50% |

| 6.75% |

| 8.125% |

| 8.00% |

| Price |

| $25.23 |

| $19.50 |

| $23.64 |

| $23.78 |

| Yield |

| 8.4% |

| 8.7% |

| 8.6% |

| 8.4% |

| YTC |

| 7.9% |

| 17.3% |

| 37.2% |

| 19.5% |

Only the NOTE has a maturity date; being 9/30/28.

Sometimes deciding between choices from the same Issuer is much tougher than what I read from the above table. With the understanding PMT might be challenged on not floating the A and B preferreds, which would increase their current coupon, price and Call risk, I would give the PMTU and PMT A the Buy ratings, and only a Hold for the other two. Here is my reasoning:

- With similar yields, the Pfd C offers the best protection on being Called, based on both its later Call date and the fact it has the lowest coupon.

- PMT's ability to float replacement preferreds with a fixed/floating rate is dead in many folks opinion, including mine. I think that is reflected in the coupon required to sell their recent Note.

- While both A and B become Callable in months, with them trading below Par, open market purchases by PMT would be the logical step. As stated above, replacing them with a lower coupon would be a tough sell.

- If challenged and PMT must float A & B, I would expect them to be Called since their coupon would be over 11%. PMT might do that to minimize any interest due if they lose any litigation on that action. That could make them a good speculative Buy.

Final thoughts

After climbing thanks to the FOMC raising the FFR, rates set a peak in the fall of 2023 after the feeling that “higher for longer” might not happen. That decline has been mostly on pause since 2024 started but the idea that rates will be cut this year is still predicted, maybe by 75bps.

When that idea truly takes hold or we actually sees a cut, fixed-rate assets should outperform floating-rate assets as the yield competition gets easier. For the rate-cut skeptics but mREIT believers, there are other Issuers to consider, like MFA Financials ( article link ).

Promised links

To read about both PMT assets and how they have moved and how my viewpoint has evolved, here are the links to prior articles in these assets:

- PennyMac Exposure Now Available To Note Investors

- Revisiting The MFA Preferreds With A Comparison To PennyMac Preferreds

- PennyMac Investors Have A Choice: Equity Or Preferreds

For further details see:

Comparing PennyMac Pfd C And Its New Note