COMP - Compass: Focus On The Efficiency Plan

Summary

- Shares of Compass cratered after the company reported Q4 results and issued guidance for the first quarter of 2023.

- The company is expecting y/y revenue declines to worsen to the mid-30s, as the real estate industry continues to suffer from a bevy of macro headwinds.

- Still, Compass is holding onto its ~5% market share.

- I'd focus instead on Compass' commitment to its cost-cutting plan and hitting FCF positive in 2023. It will emerge from the market downturn leaner and more efficient.

We've always known that the real estate industry is incredibly cyclical, prone to huge booms and busts. And while today's recession may not have the scale of the 2008 crisis, the combination of high interest rates, low housing inventory, and widespread layoffs among office workers has had an incredibly dampening impact on home sales.

Against this backdrop, it's not surprising that Compass, Inc. ( COMP ) posted disappointing results. Now, one of the country's largest real estate brokers, Compass rose quickly to prominence by acquiring local brokerages and dramatically expanding its agent base. But now, against this tough macro backdrop, the company is finding itself in the positioning of scaling back.

Compass recently reported lackluster Q4 results and issued disappointing guidance for Q1, causing its stock to tank:

Though an unpopular stock now, I remain bullish on Compass stock and am adamantly holding onto the stock in my portfolio. I encourage investors to take a longer-term view here: Real estate is, again, obviously cyclical - but we should focus on the fact that Compass has managed to hold market share in a downturn as well as applaud its plans to significantly slash expenses to prepare for leaner times. When we emerge from the housing downturn (as history shows we always do), Compass will become a much more efficient and profitable company.

Here is my full long-term bull case for Compass:

- Within a few years, Compass has become a dominant brokerage - Compass' market share of U.S. real estate transactions is growing rapidly to ~5%. Already deeply embedded into major coastal markets, Compass is more recently pushing into new office opportunities in the Midwest. There's still room for further expansion. Even after the new market activity this year, Compass is still penetrated into less than half of the U.S. population.

- Tertiary revenue opportunities - Recently, Compass has been opening the door to new monetization opportunities, including starting its own title company. This positioning helps Compass derive more wallet share from real estate transactions as a whole. Compass has commented that attach rates on these tertiary services are rising. Compass estimates its U.S. TAM is $240 billion, of which only $95 billion and the rest is coming from adjacent services.

- Strong branding - Compass built a brand around being a full-service, high-quality real estate brokerage, very similar in style and profile to competitors like Berkshire Hathaway HomeServices or Sotheby's. This gives the company a very strong distinguisher against other tech-first rivals like Redfin.

- Scalable platform - Compass' primary costs lie in the R&D spending to deliver its technology platform for Compass agents, as well as the sales and marketing costs of advertising its brand to homebuyers/sellers and potential new agents. These costs are scalable: as Compass' scale grows, and as agent productivity grows (the average Compass agent generates 19% more sales in the second year), Compass will be able to improve its profitability margins, which we have already seen in the company's latest results.

Stay long here: This is a great small-cap rebound opportunity.

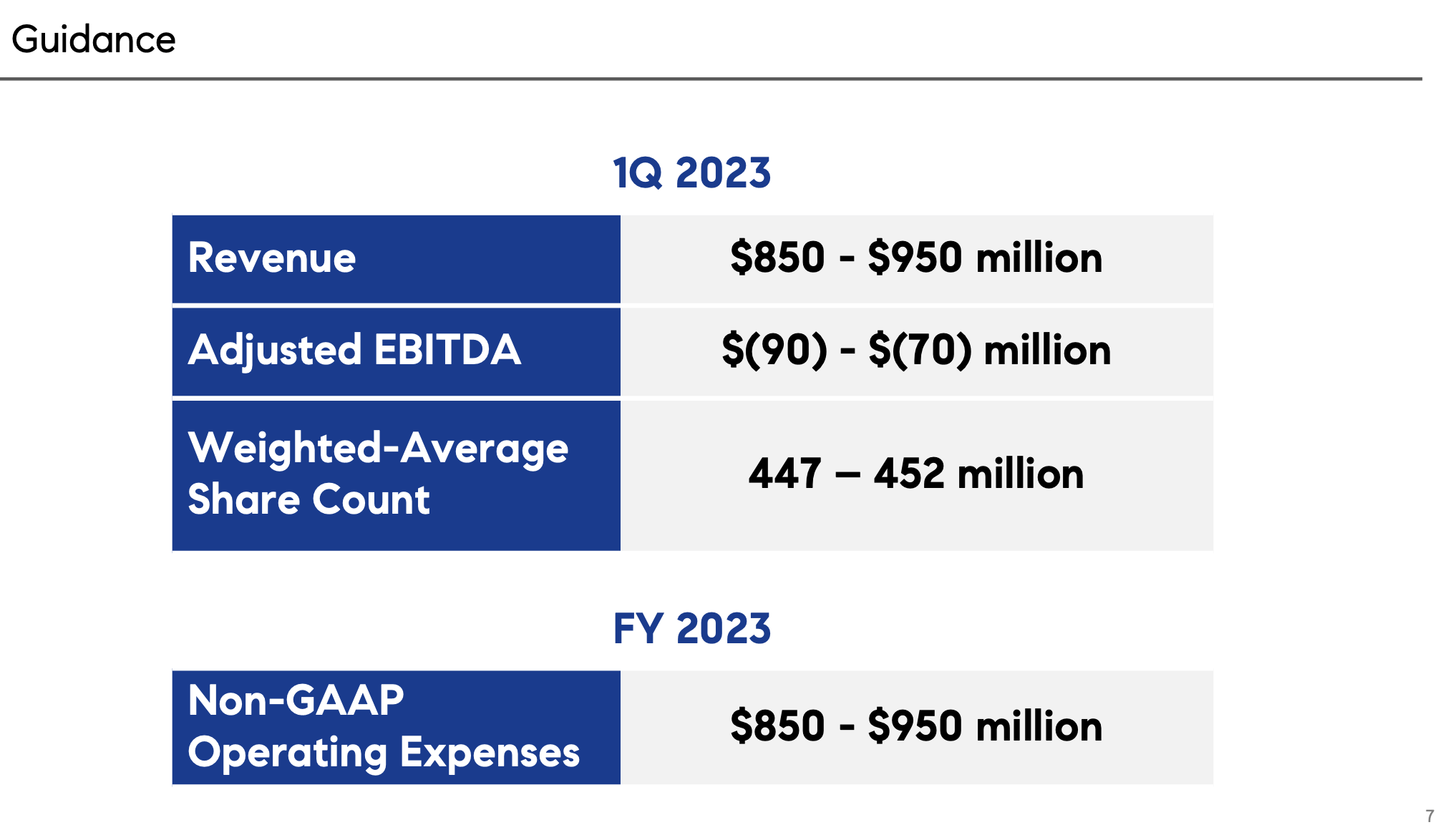

Guidance calls for sharpening revenue declines

Let's start with the biggest drag to sentiment stemming from the Q4 earnings release: The guidance outlook for Q1.

{kind=link}

Compass is guiding to $850-$950 million in revenue for the first quarter, which versus the $1.40 billion in revenue in the prior-year Q1 would imply a decline range of -39% y/y to -32% y/y. This indicates deterioration from Q4 results of -31% y/y.

Wall Street analysts, meanwhile, had hoped for $982.2 million in revenue, or -30% y/y decline.

While the news of extended pain for an extended period of time certainly hurts, I would almost completely discount Compass' performance during the downturn and focus mostly on market share maintenance (more on that in the next section). Moreover, it's also important to recognize that the company has reaffirmed its target of becoming free cash flow positive for the full year 2023, starting in Q2.

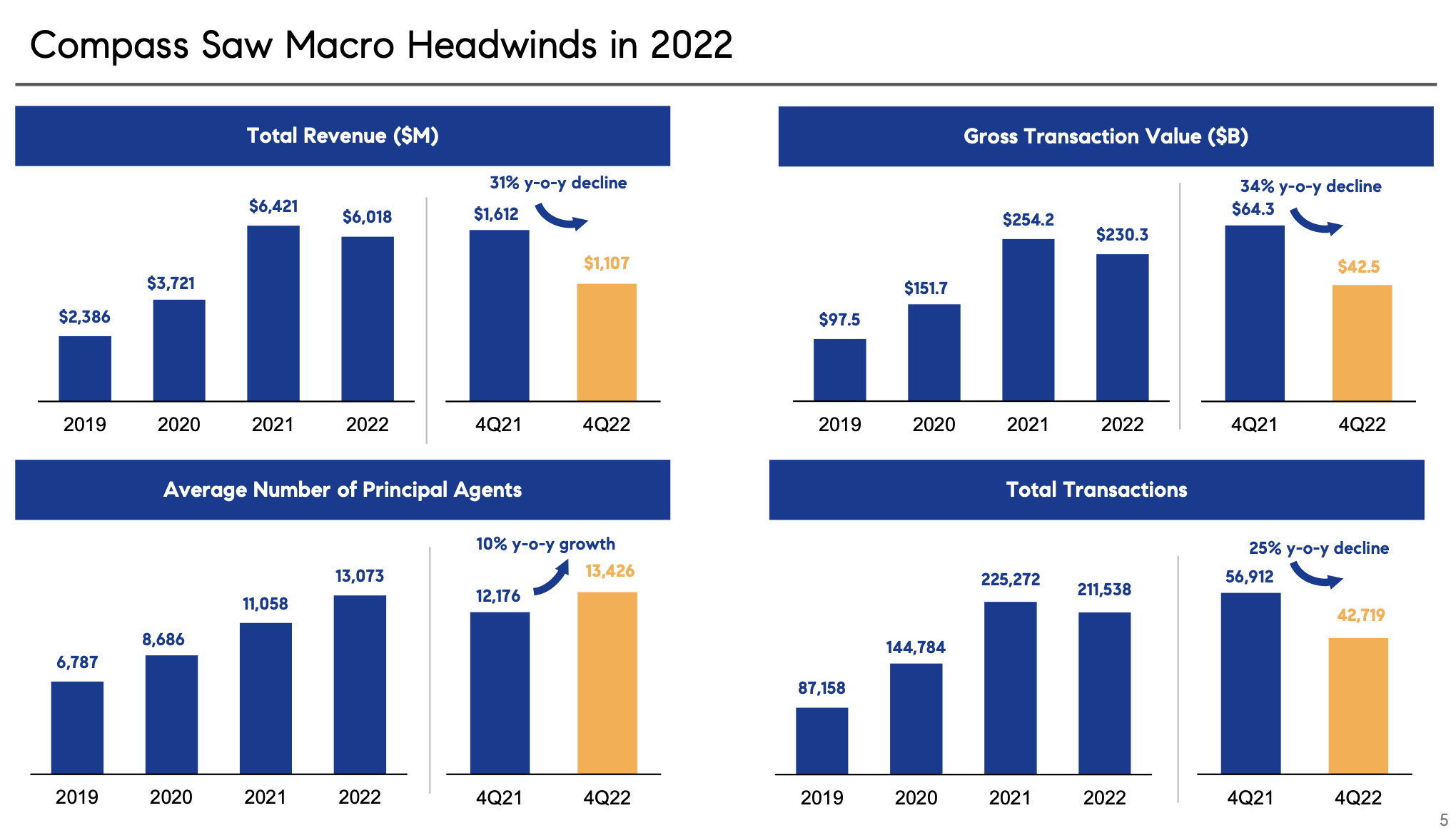

Q4 highlights and the cost-cutting plan

The chart below shows how Compass fared in Q4: Revenue declined -31% y/y, total transactions declined -25% y/y while transactional volume fell -34% y/y. Meanwhile, the number of principal agents also grew 10% y/y - which is what Compass is now trying to correct.

{kind=link}

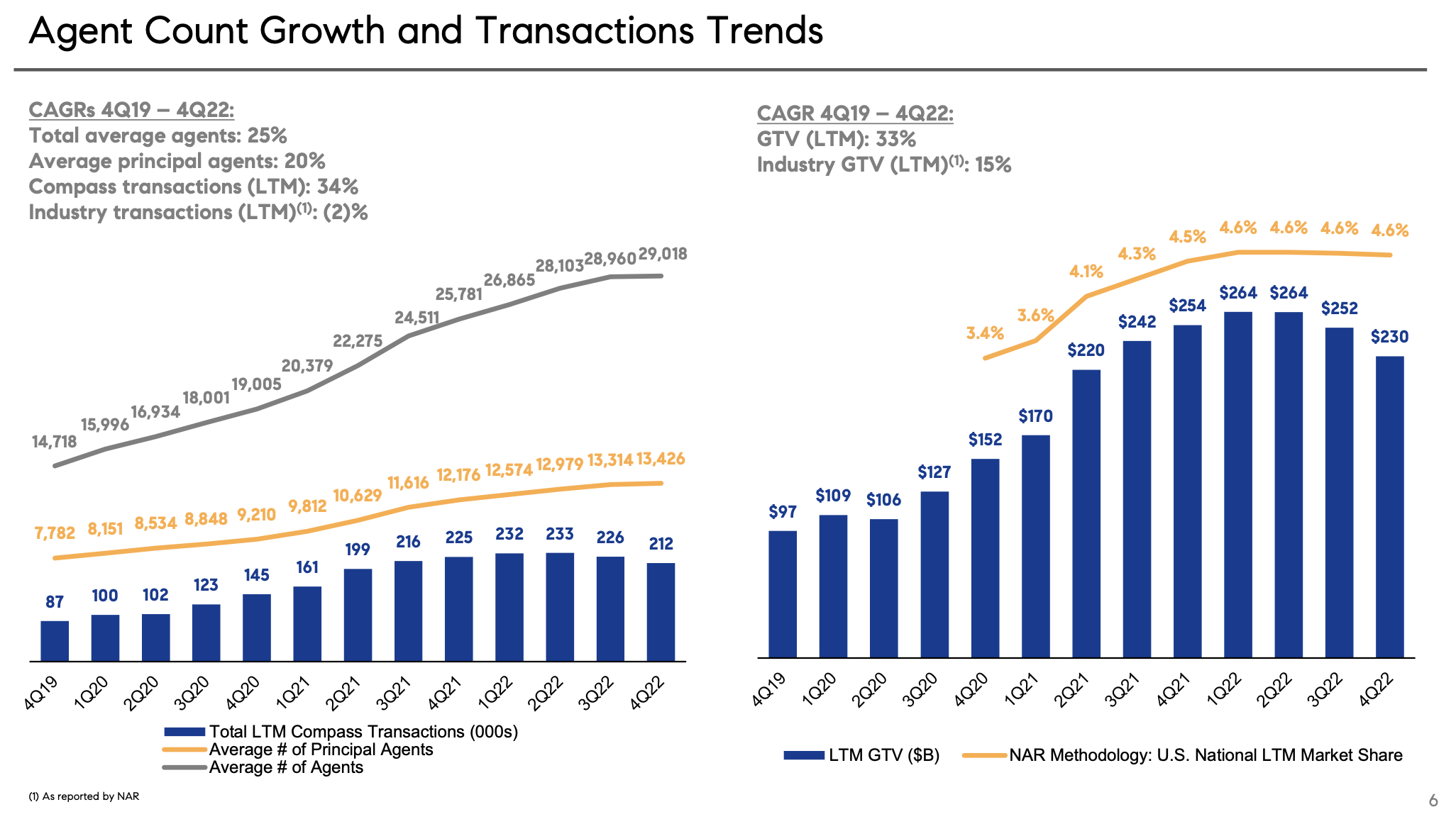

In the face of these headwinds, however, we should focus on the fact that Compass has retained market share. In other words, it's not declining by any more or less than its peer brokerages in the U.S. On the right-hand side of the chart below, the yellow line indicates that Compass has retained its 4.6% market share all throughout a tough 2022:

Compass agent and market share stats (Compass Q4 earnings deck)

{kind=link}

Robert Reffkin, Compass' CEO, noted that 2022 was similarly painful to 2008 in terms of unit declines. He reiterated management's commitment to slimming expenses, and even more importantly, maintaining this expense discipline when the market starts recovering again. Per his prepared remarks on the Q4 earnings call:

The 2022 industry decline in units was as bad as the Great Financial Crisis when the number of units fell by 18% year-over-year from 2007 to 2008. While 2022 was a tough year for the housing market, particularly in the fourth quarter, we responded to the challenging market conditions by taking the initiative to reset our cost base. We took decisive steps throughout 2022 to reduce expenses and drive operating efficiencies in the business with a very specific goal to become free cash flow positive for 2023, starting with being free cash flow positive in the second quarter of 2023.

As the market deteriorate fast, we moved quickly to respond and initiated cost-cutting actions that reduced our non-GAAP operating expenses by $338 million, which is 23% less on an annualized basis from the second quarter of 2022 to the fourth quarter of 2022. We shared on our third quarter call that we intend to develop and implement a plan to further reduce our non-GAAP operating expenses to a range of $850 million to $950 million. As we reported in early January, we believe our actions make it possible to achieve below the middle of the $850 million to $950 million range of annualized operating expenses by the fourth quarter of 2023.

As a result of investments in prior years, even at this reduced level of operating expenses, we continue to invest in growth and technology to further strengthen the company during this downturn in the market. We are seeing industry forecasts for negative volume of 22.6% from Fannie Mae, negative 18.6% from MBA and negative 12.6% from NAR. We expect to achieve our goal of being free cash flow positive in 2023 at each of these levels. We are confident that this is the right level of non-GAAP operating expenses. However, as we have demonstrated throughout 2022 and into 2023, we are prepared to move swiftly to implement additional cost cuts if the markets turn out to be worse than expected. Our employees have worked incredibly hard to reset our cost base over the last 12 months. We believe it's the right cost base, and we are committed to maintain our OpEx levels even if and when the market goes up. "

Versus the OpEx levels that Compass had in Q2 of 2022 (midway through last year), management notes that the company's target of $850-$950 million of pro forma operating expenses (excluding commissions) would represent a reduction of $565 million or roughly -40% y/y.

Key takeaways

There's no doubt that Compass is in a bind now, but it's difficult to avoid sharp declines with the multiple factors weighing down the housing industry: High interest rates, widespread layoffs, and tight inventory. I remain encouraged by Compass' ability to retain its market share and its commitment to expense controls and profitability, which will help the company emerge as a more profitable organization when the real estate industry gets back on track. I'm equally enthused by the company's commitment to becoming free cash flow positive even in a tough 2023. Stay long here and invest while the stock is down.

For further details see:

Compass: Focus On The Efficiency Plan