CMPGY - Compass Group: Costly For What It Is

2023-06-29 15:19:42 ET

Summary

- Compass Group raised its full-year guidance for operating profit growth to around 30% and announced a £750m share buyback.

- The company's long-term prospects remain solid with a proven approach to growth and high demand in its sector, particularly in North America.

- However, challenges include differentiation in a price-driven industry and long-term margin issues due to factors like food inflation and labor shortages.

- Despite its strong performance, the company is overvalued with a price-to-earnings ratio of 30 and a dividend yield of under 2%.

Catering and outsourcing company Compass Group ( CMPGY ) has done a good job of putting the pandemic behind it and getting on the front foot again with its simple but historically well-proven business model.

I last covered the company, with a hold rating, in October 2020 ( Compass: Starting To Right Itself ). Since then, during the depths of global workplace shutdowns amidst the pandemic, the shares have moved up by 93%. I now see them as overvalued.

Strong Business Momentum

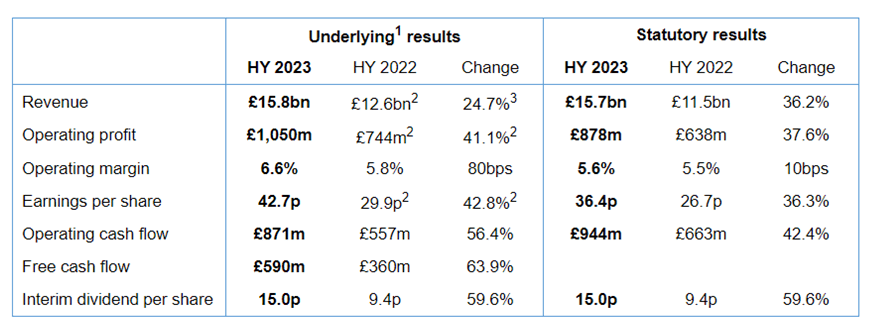

The company is currently benefiting from strong performance in its business. Its half-year results to the end of March showed strong gains compared to the prior year period in revenue, profit and cash flow.

{kind=link}

The company raised its full-year guidance for operating profit growth from above 20% to towards 30%. It also announced a further £750m share buyback alongside the results.

Long-Term Prospects Remain Solid

I do not see the results as a flash in the pan.

The company has essentially recovered from its pandemic-era woes and is now firing on all cylinders.

| (all figures ‘000 except EPS) |

| 2019 |

| 2022 |

| Revenue: |

| £24,878 |

| £25,512 |

| Operating Profit |

| £1,570 |

| £1,500 |

| Profit after tax |

| £1,143 |

| £1,117 |

| EPS ((P)) |

| 71.6 |

| 62.6 |

| Net debt |

| £3,272 |

| £2,990 |

Chart compiled by author using data from company announcements

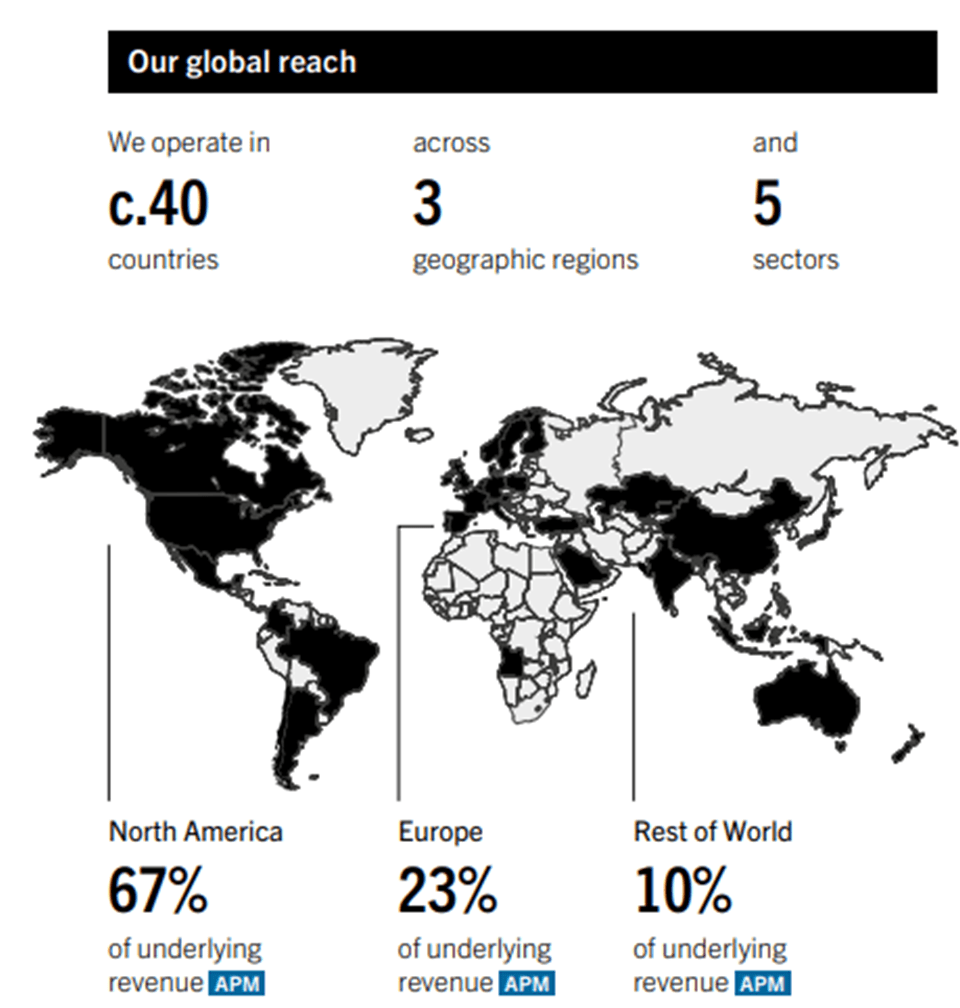

The proven approach that has fuelled the company’s long-term growth continues to work, and I expect demand in its sector will remain high in future. North America is the key market and from October on, Compass will start reporting in US dollars.

{kind=link}

The challenge with this industry, however, is differentiation. Contracts are often price-driven and there can be a race to the bottom, especially with local players keen to build market share. In some cases, Compass’s international spread or specific experience is a real competitive advantage. But often I think it has limited impact unless the firm delivers on pricing.

The net post-tax profit margin last year was 4.4%, a bit lower than 2019’s 4.6%. At the half-year level, the company did say it was targeting an operating margin of 6.7% - 6.8%, from the previous guidance of above 6.5%. But the margin issue is a long-term one for the industry, and I do not think Compass or any of its competitors have a great solution. In many cases, foodservice provision has at least some of the attributes of a commoditized industry.

The chief executive said, “Longer term, we expect the growth opportunities in the market to sustain mid-to-high single-digit organic growth and a path back to our historical margin, leading to profit growth above revenue growth.” I have my doubts about sizeable margin expansion. Food inflation is pushing up input costs and the same applies to labor, exacerbated by labor shortages in unskilled jobs in many markets. None of that bodes well for foodservice economics. Meanwhile, at a time of economic difficulty, I expect customers will be loath to raise budgets more than they feel is necessary.

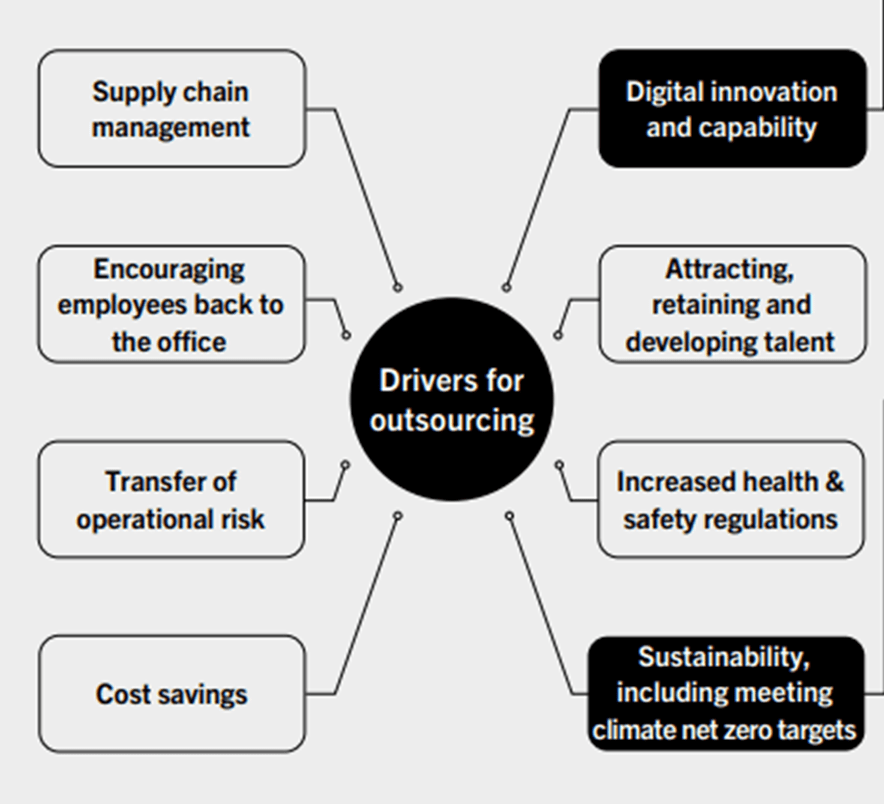

As an example, consider Compass’ discussion of drivers for outsourcing in its most recent annual report.

{kind=link}

In what way can Compass respond uniquely well to any one of these drivers versus rivals like Sodexo ( SDXOF ) (which last year managed even lower post-tax profit margins)? I am doubtful that it has a sufficiently broad range of meaningful differentiators.

So I see Compass as a solid player in a large but fairly unattractive industry. That means that, to want to add it to my portfolio, I would need to be able to buy in at what I saw as a compelling price.

Costly Valuation

Right now, however, I do not think the valuation is attractive. The firm trades on a price-to-earnings ratio of 30, with a dividend yield of under 2%.

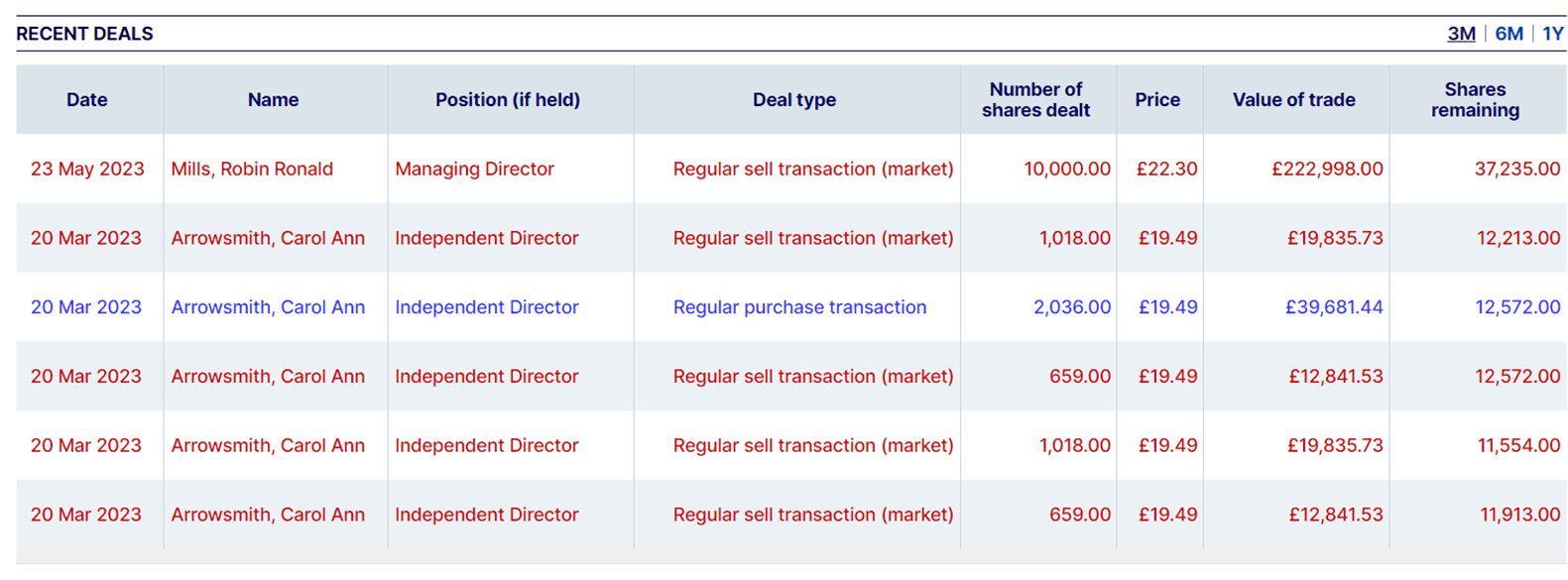

Several directors have made open market sales of shares this year, including at prices well below the current share price.

{kind=link}

The shares are trading close to their all-time high. But earnings per share remain below pre-pandemic levels and I think the pandemic also highlighted a previously underappreciated risk for Compass, that of a sudden, unforeseen and sustained switch to where people work and learn. In addition to that, the ongoing shifting balance between site-based work/study and location-independent activity is also a threat to long-term profitability in an industry that relies on economies of scale.

With a P/E in the mid-teens or so, I would see Compass as a bargain. It is a strong player in an industry with low barriers to entry, fairly low profit margins and a lot of operational complexities. For such a business, I think a P/E ratio of 10-15 is about right and as Compass is an established player it could merit a valuation at the upper end of that range. But higher than that, and I would want to see evidence of outsized growth opportunities that I do not think exist in this industry.

It is priced at double that, so I see it as a “sell”.

For further details see:

Compass Group: Costly For What It Is