JNJ - Compass Pathways: Private Placement Buys Less Time Than Expected

2023-11-05 01:03:52 ET

Summary

- In August 2023 COMPASS Pathways announced a major private placement that initially eased concerns regarding the group’s cash runway.

- A sharp fall in the COMPASS Pathways share price since mid-September 2023 has put the majority of the private placement funding at risk.

- Key Phase 3 trials for COMP360 are in their very early stages, but management have confirmed that they are on track.

- Focus is shifting beyond regulatory approval, but a detailed strategy for the eventual monetization of COMP360 is still a long way off.

Introduction

I last published on COMPASS Pathways plc ( CMPS ) in mid-August 2023 , and in that note, I reiterated a point I've been making about a number of stocks in the psychedelics space for a long time - CMPS was rapidly running out of cash. I doubt that anybody at CMPS reads my research, but clearly management and the board were having similar thoughts about the group’s cash runway. Just two days after my note was published, CMPS announced a major capital raise ; the news triggered a nice bounce in the price, with the stock up by ~20% on the day of the release. My Sell call at ~$8 per share looked to be badly timed for a little while, with CMPS almost hitting $10 in mid-September. However, the market's optimism quickly unwound, and CMPS was trading below $5.30 by late October (~30% down from my August rating level). The risk-on bounce in equity markets in early November has helped to lift CMPS back up to ~$6.50 at the time of writing. With CMPS now ~20% below my previous Sell rating level, action having been taken to extend the company's cash runway, and 3Q23 results recently published, it is a sensible time to update my thinking on the company.

Progress Made In 3Q23

Before turning to the key issue of the private placement deal, in the bullet points below I briefly highlight and discuss some of the operational progress that CMPS management referenced in 3Q23.

- COMP360 for treatment resistant depression ('TRD'): 3/4 of the COMP 005 Phase 3 trial sites have been initiated. Approvals for trial sites across several countries have been received for COMP 006. Initial topline data on COMP 005 is expected by mid-2024, with COMP 006 topline data to follow in mid-2025. Both trials are said to be on track.

- Patient demand, in terms of candidates to participate in the trials, is strong according to management.

- Recruitment for a Phase 2 trial for COMP360 to treat PTSD is complete. This small trial is to evaluate safety and tolerability, and so it would be surprising if it did not return positive results given previous COMP360 trial outcomes. Topline data from the PTSD trial is expected to be available before the end of 2023.

- Anorexia nervosa has the highest mortality rate of any mental health condition and there are currently no FDA approved treatments available. CMPS has a Phase 2 study underway investigating the application of COMP360 for anorexia nervosa, but there is no guidance as yet regarding the timing of trial results.

- The continued expansion and acceptance of Johnson & Johnson’s ( JNJ ) SPRAVATO (esketamine) as a treatment for TRD is cited by management as helping to establish the infrastructure needed to roll out COMP360 for TRD to patients. My understanding is that the treatment requirements for esketamine services and psychedelic-assisted therapy are actually quite different, and so I am cautious in regard to the argument that esketamine is laying the foundation for COMP360 and other psychedelics in the manner that CMPS management alludes to.

- A new insurance tracking code for the provision of services associated with psychedelic medications in the USA will be launched in January 2024. CMPS has worked in conjunction with MAPS (Multidisciplinary Association for Psychedelic Studies) to move forward this important administrative issue and I think the company deserves credit in this regard; it is another example of CMPS being an industry leader in the psychedelics space. Without funding from insurers and other payers, psychedelic assisted therapy will almost certainly be simply too expensive at the out-of-pocket level to allow widespread patient access.

Private Placement Deal – Funding At Risk

The wording included in the headline of the CMPS 16 August private placement capital raising announcement - 'Up to $285 Million Private Placement Financing Joined by Leading Healthcare Investors' - naturally results in investors concluding that something close to $285m of financing is likely to have been secured by CMPS. However, it could well actually be the case that CMPS only ever draws down $125m from the deal participants. The detail of the announcement explains that CMPS issued $125m of shares at a price of ~$7.78 per share - this cash is safely in the door, and the investors who participated in the deal are currently looking at unrealised losses of ~16%. The balance of the $285m deal relates to warrants with an exercise price of $9.93 and a three-year exercise period commencing 18 February 2024. As things stand today, the CMPS share price would need to increase by ~55% in order for the warrants to be in the money.

For investors trying to analyse the sufficiency of the CMPS cash runway, the position regarding the warrants represents an area of great uncertainty. Personally, with the warrants being so far out of the money, I'm not currently willing to assume that the CMPS balance sheet will receive any further support from the warrants. CMPS management, unsurprisingly, are putting forward a much more optimistic view regarding the contribution from the warrants (which are referred to in the CMPS commentary as 'PIPE').

Here's what CMPS had to say about the cash runway in August when announcing the 'up to $285m' private placement:

The aggregate proceeds from this proposed financing, combined with current cash and cash equivalents, are expected to be sufficient to fund the current operating plan into late 2025.

Source: CMPS News Release , 16 August 2023.

Despite the fact that the warrants are now massively out of the money - which implies that $160m of potential funding is clearly at risk - CMPS hasn't adjusted their commentary regarding the group's cash runway:

Runway lengthened to late 2025 through term loan facility, sales of shares under the At the Market (“ATM”) facility and private placement transaction (the “PIPE)”.

Source: CMPS 3Q23 Release, page 1.

The fall in the CMPS share price has balance sheet consequences beyond the potential loss of a capital inflow that management appears to be relying upon. In the absence of a share price improvement, any further stock issuance under the ATM facility will be done at lower prices, triggering greater ownership dilution for existing shareholders. Further, ongoing issuance under the ATM facility is likely to put downward pressure on the share price, which in turn makes the warrants less likely to be executed.

It seems to me that, thanks to a sharp share price decline, what looked back in August to be a potentially transformative private placement financing deal is now not enough to remove cash runway concerns. My final gripe regarding the private placement deal is that it came at a high cost in terms of fees and expenses. The headline gross upfront proceeds of $125m reduced to just $116.9m of net proceeds after costs - that's a hefty cost of 6.5% (assuming the warrants are not exercised) and a very nice earner for placement agents Morgan Stanley and TD Cowen.

Updated Cash Burn Analysis

Cash used in operating activities was -$17.1m for 3Q23 and -$69.6m for the nine months ended 3Q23. Additional operating cash outflows of -$9m to -$15m are expected in 4Q23E, but note that the 4Q23E management guidance includes the benefit of a $14m cash inflow relating to UK R&D tax credits. Excluding the expected R&D tax credit inflow, management is therefore guiding to a cash outflow of -$23m to -$29m in 4Q23E. Exhibit 1 tracks operating cash flow back to FY20 and provides an estimate for FY23E operating cash flow.

Exhibit 1:

Source: author’s calculations based on CMPS quarterly reports.

Is management's claim that the company has sufficient cash to make it through until late 2025 supportable? Cash as at 3Q23 stands at $248m. Using the upper end of the 4Q23E operating cash outflow guidance range excluding the UK R&D tax credit (being ~$29m) as a proxy for future quarterly cash outflows, and allowing for a minimum cash level covenant of $22.5m under the Hercules debt facility, CMPS appears to have sufficient balance sheet cash to last for ~7.8 quarters - on that basis, management's claim looks to be questionable but possibly achievable. However, with Phase 3 trial activity yet to fully ramp up, I think it is likely that quarterly operating cash outflows will exceed -$29m during FY24E. Therefore, I conclude that in the absence of material cash inflows from the PIPE warrants or ATM issuance, CMPS is unlikely to be able to deliver on management's claim that the cash runway is secure through to late 2025.

COMP360 Beyond TRD, Commercialization Strategy, Big-Pharma Buyout?

The prospect of application of COMP360 beyond TRD is interesting, and could potentially lead to CMPS being able to generate value for shareholders in relation to conditions such as PTSD and anorexia nervosa . However, in regard to the CMPS balance sheet and management's comments regarding the cash runway, it is important to understand that CMPS currently lacks the financial resources to launch major new trials. I therefore suggest that investors keep their focus squarely upon COMP360 for TRD.

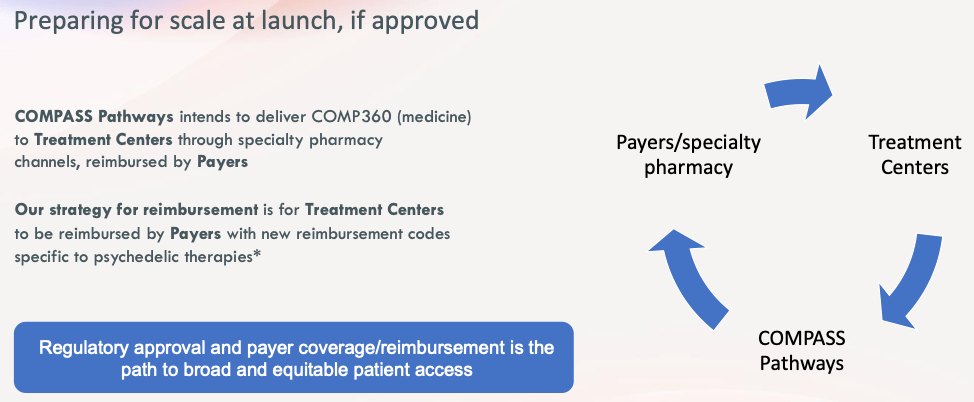

Analysts and investors are starting to look beyond the 'will psychedelic-assisted therapy be approved?' question and putting more energy into understanding the potential commercial economics for the various participants that would be involved in delivering psychedelic-related treatments to patients. CMPS included a few slides in its November 2023 presentation pack that attempt to provide an outline of how COMP360 therapy might be delivered. As an example, Exhibit 2 sets out a framework in which patients are able to fund access to COMP360 therapy via insurers and other payers.

Exhibit2:

Source: CMPS Presentation, November 2023, slide 12

{kind=link}

The slides go some way to fleshing out the CMPS strategy for commercialization, but many unanswered questions remain. Having listened to the 3Q23 analyst Q&A , I would caution investors that the slides that management presented are a long way from being a complete business plan. The title of slide 13 - 'The infrastructure to deliver COMP360 psilocybin therapy already exists and is growing' strikes me as rather misleading; I think that the CEO's comments during the 3Q23 management speech and Q&A support my view that some infrastructure is in place, but that it cannot be used without material modification.

I am starting to wonder if CMPS management references to JNJ’s SPRAVATO could have a larger strategic intent behind them. CMPS appears to be positioning COMP360 as a direct competitive threat to SPRAVATO. Is it possible that CMPS has hopes for JNJ to sweep in and gobble up the company? From JNJ’s perspective, a takeover of CMPS would give JNJ the ability to control the timeline to regulatory approval of COMP360; this would likely involve a decision to slow down the approval process and allow SPRAVATO to enjoy a longer period of high patient demand. Until now, big-pharma has seemed rather uninterested in the psychedelics space, but my sense is that the tide may be turning on that front.

Sudden CFO Departure

The CFO's departure was very sudden. The news was released on 26 October, and CFO Falvey was out of the door on 03 November. It is disappointing that the CMPS announcement did not provide any detail regarding the background to the CFO's exit. The rather vague and ubiquitous statement frequently used in such circumstances - 'to pursue other opportunities' - leaves plenty of room for investors to come up with worrying scenarios. The timing of the CFO's departure strikes me as rather odd too, coming so soon after a big capital raise. Of course, there may well be nothing untoward going on here, but I currently feel somewhat concerned regarding the risk that the CFO's sudden exit could be linked to potential problems with the group's financial management and reporting systems.

Conclusion & Rating

Unfortunately for CMPS, the stock’s share price decline has well and truly taken the shine off what initially appeared to be a solid private placement deal. Relative to my prior review, and assuming that the warrants are not exercised, CMPS has extended its cash runway by around nine months but has increased its share count by ~35%. The significant dilution to legacy investors might be regarded as a heavy price to pay for a cash runway extension that now appears to be insufficient to get CMPS anywhere close to achieving FDA approval for COMP360.

For me, CMPS and other stocks in the psychedelics sector continue to be highly speculative investments. I therefore maintain my Sell rating on CMPS. A big-pharma takeover for CMPS doesn’t appear likely at this stage, but it could well be the best outcome for CMPS shareholders.

For further details see:

Compass Pathways: Private Placement Buys Less Time Than Expected