COMP - Compass: Potential Impairment To Its Business

2023-11-29 07:36:26 ET

Summary

- Compass reported revenue and EBITDA in line with estimates, but negative sentiment in the housing market remains a concern.

- High mortgage rates are disincentivizing sellers from listing their homes, leading to low inventory in the market.

- Lawsuits against the National Association of Realtors and real estate brokerage firms could permanently impair Compass's business if commission rates are adjusted.

Investment action

I recommended a hold rating for Compass (COMP) when I wrote about it the last time , as I thought the better timing to buy the stock was when the economy recovered. Based on my current outlook and analysis of COMP, I recommend a hold rating. I believe the outlook for COMP is as uncertain as it can ever get, given that there is a risk that its business could be structurally impaired. On top of that, the macro headwinds are not easing either, and there is no saying that mortgage rates will be revised downward based on historical data.

Review

COMP reported revenue of $1.34 billion, largely in line with consensus estimates of $1.33 billion and management's own guided range of between $1.3 billion and $1.4 billion. Above the revenue line, COMP reported a gross transaction value [GTV] of $50.9 billion on 48,134 transactions. Moving down, COMP reported EBITDA of $22 million, which was also in line with the guided range of $15 to $35 million, and delivered a positive FCF of $12 million for the second consecutive quarter. While COMP has grown largely in line with guidance and consensus, I believe it is insufficient to overcome the negative sentiment of the housing market. My concern remains the same for COMP, where the housing market continues to be impacted by high mortgage rates (which also lead to low inventory) and the potential revision of the commission (discussed below).

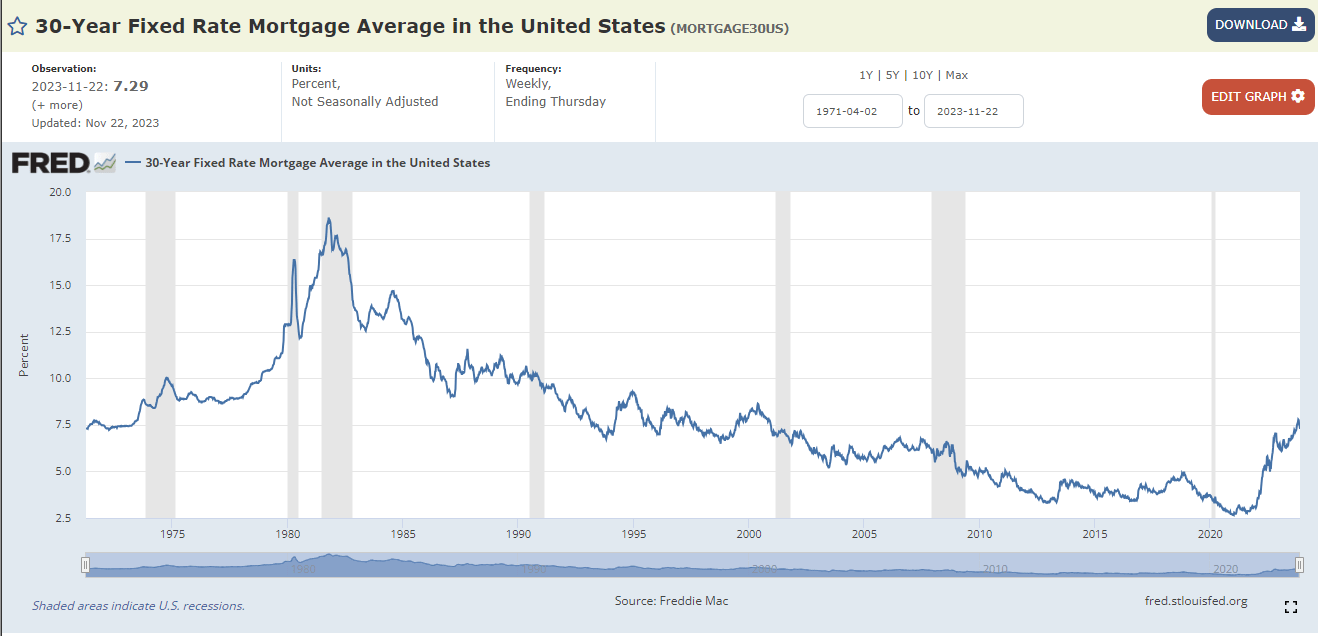

Starting by addressing the most obvious headwind-mortgage rates-I believe the current 30-year fixed mortgage rates of 7.3% continue to disincentivize would-be sellers from listing their homes. The situation is made worse when a large portion ( 62% ) of existing mortgages are less than 4%. Unless these home owners are forced to sell their housing, it is extremely unlikely that they would list their home up for sale as:

- Valuation is not going to be great in the current rate environment.

- Selling would mean they need to refinance their home loan at 7.3% (a massive step-up).

Accordingly, this leads to low inventory in the market. Note that COMP's position in the value chain is similar to that of a typical real estate agency, in between the buyer and seller, and both parties are unlikely to participate in the housing market today. The hope is that the Fed will start to reduce rates as inflation has tapered down a lot since last year. However, Powell's message to the market suggests that rates could still continue to go up. Looking at the historical mortgage rates in the US, there is clearly significant room for rates to increase. To put things in perspective, from the period between the 1990s and 2000s, the average mortgage rate was in the low 7% range, near the current 7.3%. Even if rates do not rise, there is no saying that rates will go down . Suppose rates stay at this rate for an extended period of time. COMP is unlikely to see any major growth acceleration in the near term.

{kind=link}

{kind=link}

The next major headwind that could permanently impair COMP business is the outcome of the lawsuits against the National Association of Realtors [NAR] and real estate brokerage firms. A federal jury recently handed down a decision in one of two cases that had accused real estate brokerage firms and the NAR of conspiring to artificially inflate commission rates. The worry is that the ultimate decision might prevent listing agents from future commission splits with buyer agents. That would be the worst-case situation, but even if it doesn't materialize, broker commissions will likely be subject to more scrutiny and future downward pressure. As it stands, the seller typically pays a commission of 5-6% to the listing and buying agents, split between the two. I would also note that the current commission rate is ridiculously high, ranging from 5 to 6%, when compared to other parts of the world . Being a tech-enabled brokerage that makes almost all of its money from broker commissions, COMP business would be structurally impaired if the commission rate were to be adjusted.

The only positive update that is supportive of COMP growth is the strong sequential agent growth. The idea is that with more agents, COMP will be able to address a larger part of the market, although the number of transactions is down. In the quarter, the average number of principal agents grew 422 sequentially to 14,055. However, I note that the increase is largely driven by acquisitions and that organic agent additions remain largely flat on a sequential basis.

In aggregate, there are just too many uncertainties with the growth outlook here, especially with the potential revision of commission rates that will impair COMP business. I reiterate my hold rating.

Valuation/Final thoughts

Previously, I sized the potential bull case if the market normalized. However, it seems increasingly unlikely that we will see the bull case form, especially with the risk of commission rates revising downward. This also makes it incredibly hard to project the growth rate of COMP until we gain more certainty on what the regulators' stance is, and this process is going to take a long time as I expect a lot of appeals to be made. I would also point out that COMP is still burning cash, and if the worst case were to come, it would likely need to raise capital as the balance sheet is in a net debt position. All in all, my recommendation to investors is to sit this one out.

For further details see:

Compass: Potential Impairment To Its Business