CMPO - CompoSecure Stock: Shiny But Rough Around The Edges

2023-09-01 05:00:05 ET

Summary

- CompoSecure is capturing demand for its premium metal cards.

- Recent contract extensions with major credit card issuers support a positive growth outlook.

- We expect shares to remain volatile pressured by questions regarding near-term earnings.

CompoSecure, Inc. (CMPO) is recognized as the leading provider of metal payment cards offered to consumers by major banks and credit card issuers. The metallic form factor has gained popularity in recent years, seen as a more premium product featuring innovative security features. The company benefits from exclusive long-term supply agreements supporting a growth runway.

At the same time, CompoSecure has struggled to find momentum with its separate "Arculus" business, targeting the digital assets space with a crypto cold storage wallet solution.

The result has been some volatility in earnings with the stock underperforming more recently. Balancing some strong points in the company's outlook, we expect shares to remain volatile until there is more clarity on long-term financial targets.

CMPO Q2 Earnings Recap

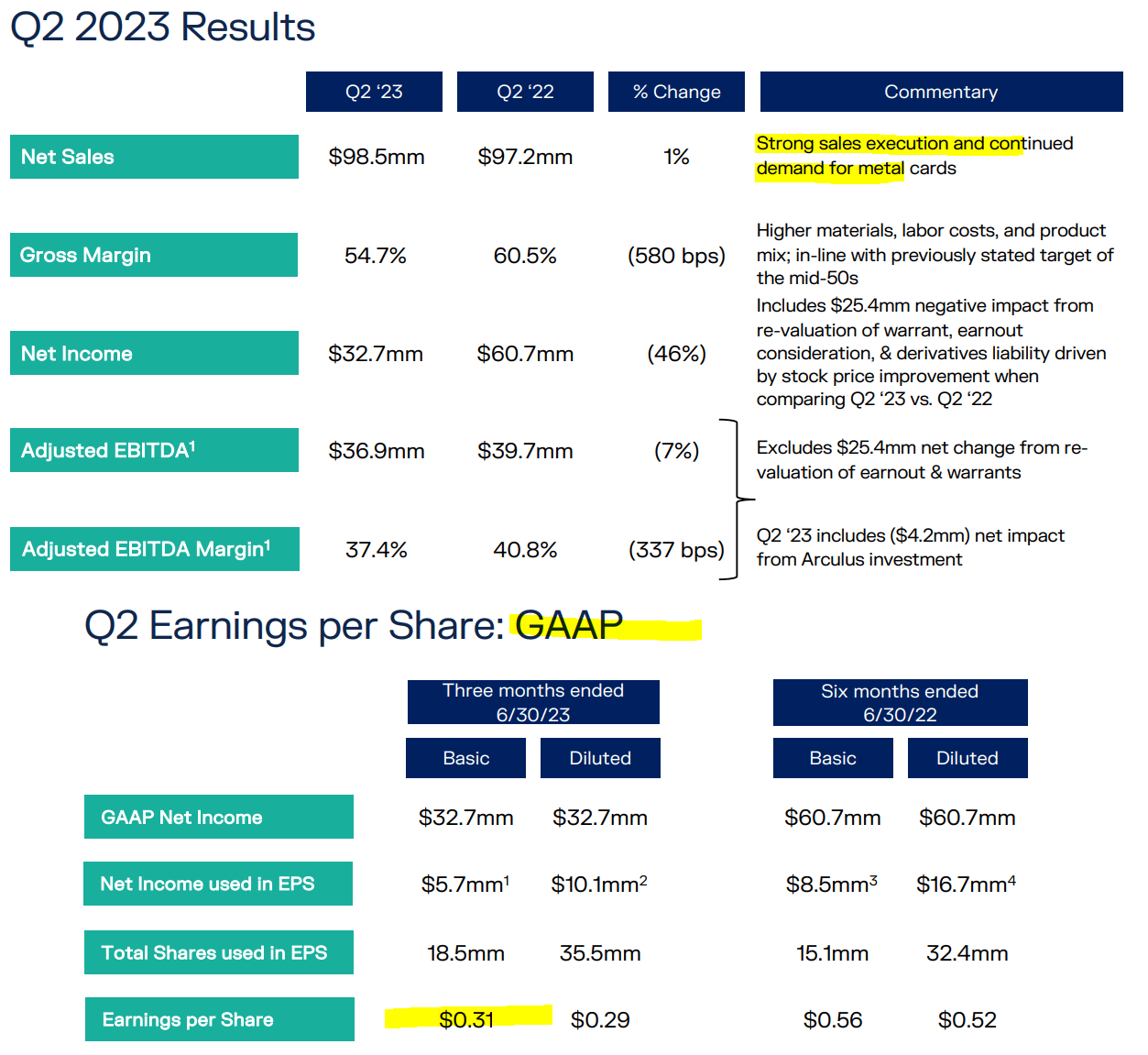

CompoSecure reported its Q2 results on August 14th with GAAP EPS of $0.31, up from $0.29 in the period last year. Revenue of $98.5 million climbed by 1% y/y. On the other hand, those headline metrics included some caveats.

Excluding the impact of derivatives liabilities, warrants re-valuation, and charges related to its 2021 reverse merger IPO, adjusted EBITDA at $36.9 million declined by 7% from $39.7 million in the period last year.

The gross margin of 54.7% fell from 60.5% in Q2 2022. This reflected some inflationary cost pressures on both materials for the metal car production and labor. Management also noted a shifting product mix expected to settle the gross margin in the mid-50% range.

Within the results, sales domestically climbed by a stronger 11%, balancing a -22% decline from the international business that has faced more uneven quarterly trends. Overall, the results were a bit messy, but the bigger point is that the company remains profitable, even if trends have slowed over the past year.

{kind=link}

A key development this quarter was the announcement of a five-year contract extension as the supplier of metal cards to "one of the company's largest customers". This follows a similar announcement of a long-term renewal earlier this year directly citing American Express Co. ( AXP ).

Separate key customers include Visa Inc ( V ), Mastercard ( MA ), JPMorgan Chase & Co. ( JPM ), Capital One Financial Corp. ( COF ), and recent wins like Barclays PLC ( BCS ).

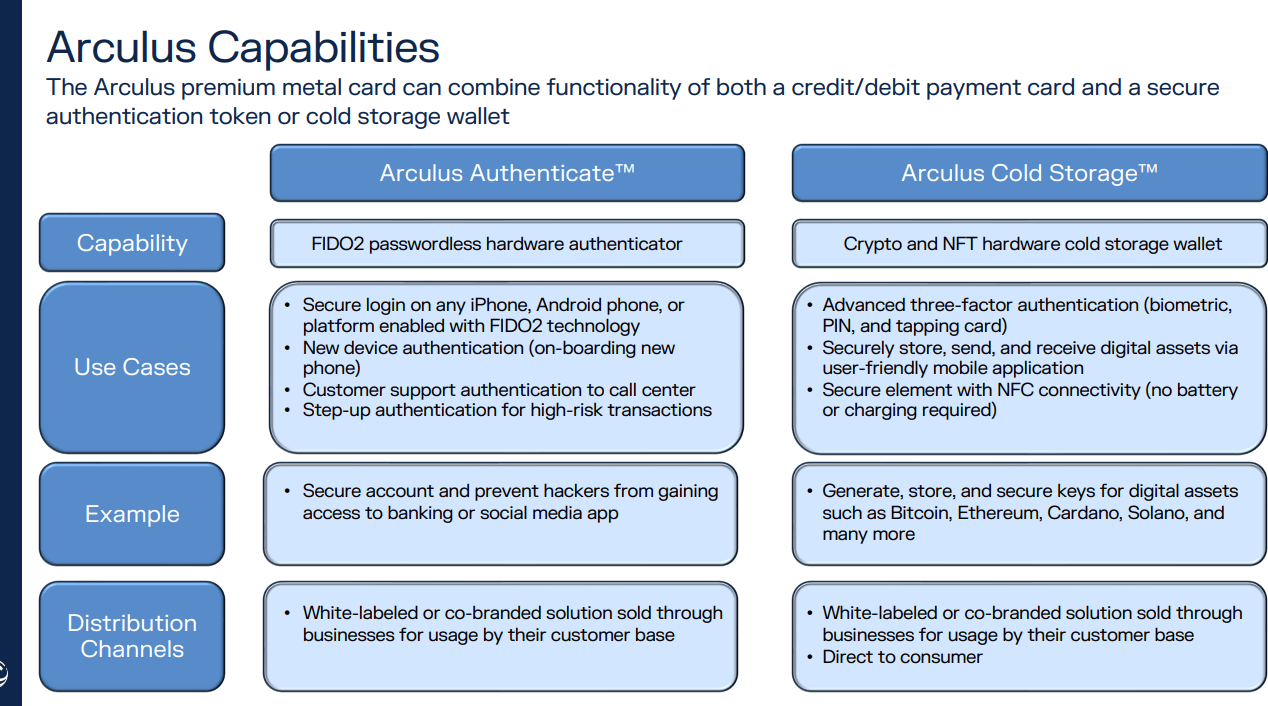

We mentioned the Arculus business. Progress in pushing that forward includes some new customers including "Plug Wallet", a branded online crypto wallet platform, and "Radix DeFi", a decentralized network.

The strategy has been to offer a private-label or branded solution for both secure authentication capability and the cold storage hardware device. These are often connected to a physical metal car which works as a token element within a three-factor authentication process. Keep in mind that the actual revenue related to this side of the group is not disclosed but is understood to be currently negligible.

{kind=link}

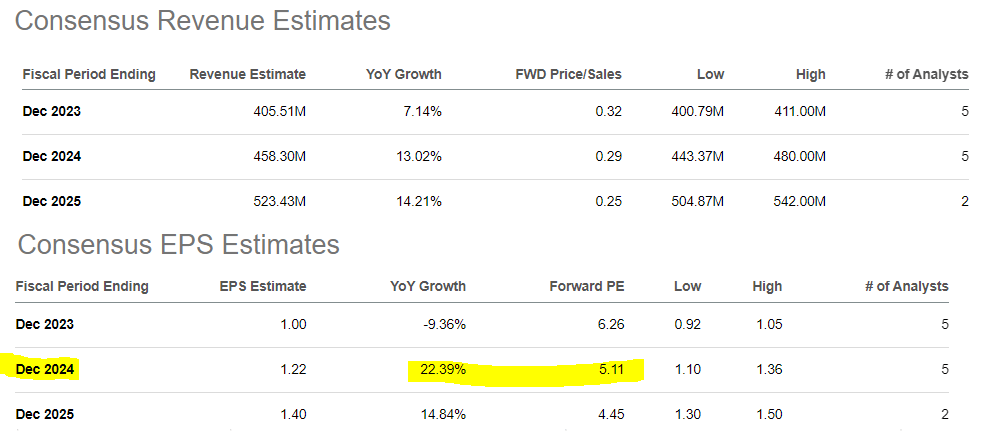

Looking ahead, management has issued guidance, targeting full-year 2023 revenue between $400 million and $425 million, representing an increase of 6% to 12%. The forecast is that adjusted EBITDA is around $150 million compared to $136 million in 2022. The expectation is for a stronger second half of the year, with an improvement in international sales while serving FinTechs as a new market.

Consensus estimates are in line with this view, reconciling the forecasted EPS drop of 9% to $1.00 this year based on the accounting adjustments we mentioned for Q2. Looking ahead, the market sees stronger growth into 2024 and 2025, capturing a tailwind from the newly signed metal card agreements and the underlying market expansion. EPS is forecast to rebound towards $1.22 next year and potentially reach $1.40 by 2025.

Finally, the company ended the quarter with a balance sheet cash position of $23 million against approximately $358 million in total debt. Considering the outlook for EBITDA this year, a net leverage ratio of around 2.5x is stable in our opinion.

{kind=link}

What's Next For CMPO?

We look at CMPO as a relatively straightforward business. The credit card issuers sign up customers who are then supplied with a new metal card from CompoSecure.

While high-level macro themes such as interest rates, consumer credit trends, and the strength of the economy play a role in this market, we believe that connection to be relatively loose as it relates to the company's direct demand impact.

What's more important is that these premium cards are essentially capturing market share from the plastic alternatives. The total volume of metal cards being issued also benefits from customer lifecycle renewals which creates a cohort of installed base that adds to the growth opportunity over time.

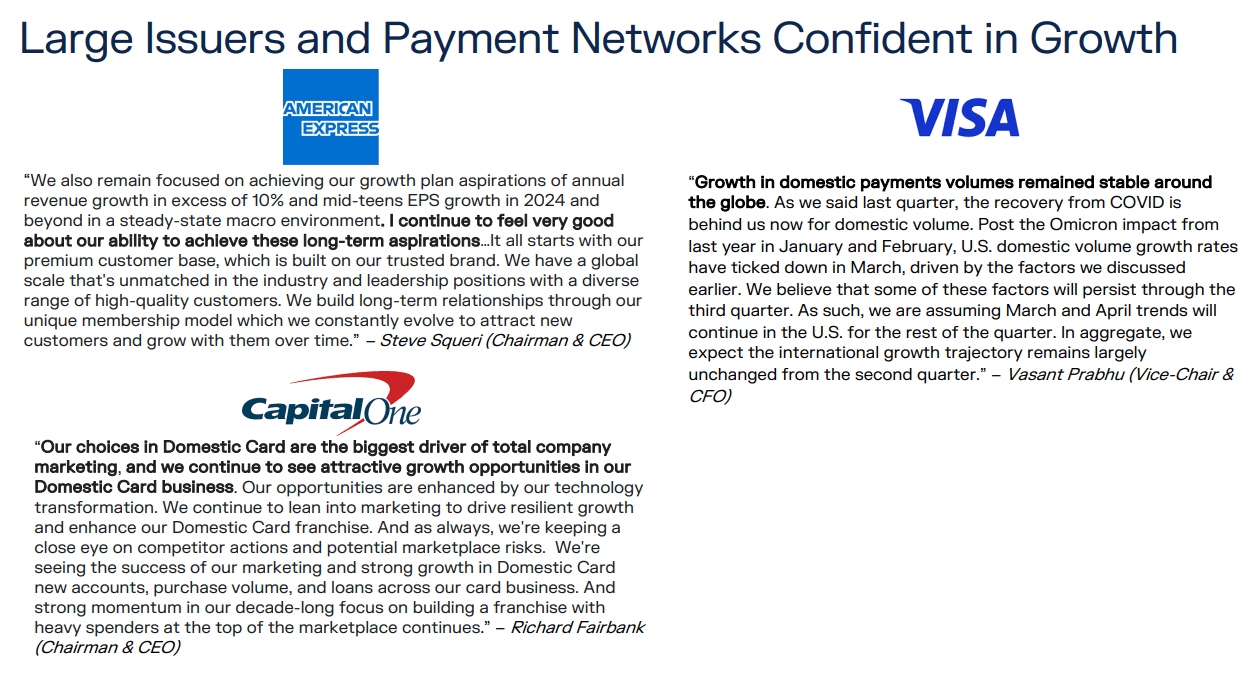

The good news is that the data suggests the underlying trends from larger issuers and payment networks are growing. We can point to the same CompoSecure customers like AXP, V, and COP where the consumer credit card business in particular has been resilient despite the more volatile economic conditions.

Even as online transactions and contactless payments gain adoption, the understanding is that a physical card establishes the customer's relationship, and is critical for security purposes. A premiumization of cards as a value-added proposition for consumers favors a move into CompoSecure's next generation of features like dynamic CVV numbers.

{kind=link}

Ultimately, this core metal side of the business is fine with more uncertainties centered on the crypto cold storage side opportunity. In our view, the company has some time to make it work, but investors should demand to see some tangible results sooner rather than later.

So if there is a knock on CMPO, it's that the company remains concentrated in this segment with otherwise poor diversification beyond its metal card product. This raises questions about the company's long-term competitive advantage and underlying economic moat. We believe that's one reason for shares to trade at a depressed valuation considering a forward P/E of just 6x and under 0.5x sales.

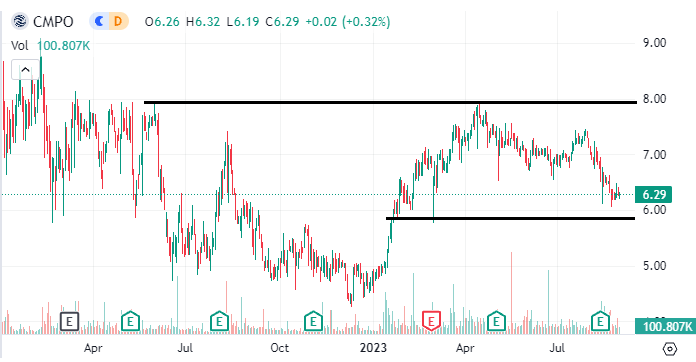

CMPO Stock Price Forecast

We rate CMPO as a hold with a price target for the year ahead at $7.00 for the year ahead balancing our favorable view of the company against a sense that it's missing a near-term catalyst.

Shares have failed to break out above the $8.00 price level multiple times over the past year, and we'd like to see some evidence that growth is accelerating and margins stabilizing to sustain a rally higher.

Shares appear cheap with a current market cap of $500 million or approximately $1 billion in enterprise value, but that valuation would also be sensitive to the risk of an operational or financial misstep.

The key risk to consider would be some unforeseen loss of even just a single card issuer relationship which would undermine the earnings outlook and force a reassessment of the company's intrinsic value.

{kind=link}

For further details see:

CompoSecure Stock: Shiny But Rough Around The Edges