MTBCO - Computer Programs and Systems And CareCloud: Avoid These 2 'Innovators'

- In the market, there are often "wolves in sheep's clothing".

- While CPSI and CareCloud list innovative keywords as the benefits to their platform, they fail to realize the entire healthcare industry does too.

- Competition and risky management will continue to prevent both companies from providing any predictable or meaningful returns.

Competition Defeats Innovation In Health

Although 20 years ago it would have been a great strategy to provide software or cloud-based services to the healthcare industry, these solutions are now commonplace. Unfortunately, a few small companies continue to try and use these buzzwords to expect growth that is not available, and investors may be lured into the trap. This article will highlight two different examples of this issue at hand, and I hope it highlights risk points to look for when investing in small companies. Let's get started.

A Laggard In Healthcare Innovation

Computer Programs and Systems, or CPSI ( CPSI ), is a small provider of healthcare software and outsourcing solutions, predominantly targeting rural or underserved regions. While the recurring revenue rate is over 90%, investors have frowned upon the latest earnings as acquisitions over the past year or so have failed to impress. The 8% drop on earnings news is not a rarity for the usually volatile share price, but is not a good indicator of success. However, the shares have rebounded over 6% since the day after earnings thanks to news of increased buybacks and positive market sentiment, allowing for these earnings to remain a blip on the radar.

Unfortunately, the fact is that the share price is essentially flat over the past 20 years is not a strong signal to buy this company. While some investors may be lulled in by profitability and the expectation of growth, I remain wary of CPSI and will be remaining neutral. This article will highlight the financial reasons why with a series of charts highlighting the general stagnation that is present.

CPSI is a provider of software and paperless solutions for healthcare, with a focus on revenue cycle management and operations. While generally a profitable endeavor, due to competition, there is little growth. Further, short-term increases in SG&A expenses have poorly impacted earnings this last quarter, as highlighted in the image below. While focusing on short-term performance is not telling the entire story, longer term patterns are being suggested in the financial data for more than just a year.

CPSI Q2 Earnings Results

The first main issue is flatlining organic revenues and earnings. Most growth in revenues has a lumpy growth pattern where revenues jump up fast then the rate of increase falls. This is either due to the small company gaining a new customer or through acquisition. At the same time, profitability has trended downward along, not keeping up with revenue growth. While only EBITDA is shown below, the pattern also remains for net income to the company. This means that the company either is spending more to try to find growth, or the acquisitions are doing more harm than good. This is a very poor income profile in my eyes and is an instant red flag in terms of the investment.

Koyfin

To fund growth, we can see that the balance sheet is weakening as acquisitions come through. To fund a $250 million purchase of Healthland Holdings in 2016, the company issued $150 million in debt and diluted shareholders. Initially, things looked alright as debt was paid off and FCF remained positive the subsequent quarters. Some investors may be lulled into a sense of complacency during this time, especially as FCFs increased each quarter, but more acquisitions in 2021 led to the issuance of more debt. As long as the company is leveraged to this degree, net income and cash flows will remain weak, leading to poor shareholder returns.

Koyfin

Considering the financial weakness and the expectation for continued sub-par performance, the current valuation of CPSI may be seen as too high. While performance is at one of the worst points in the company's history, the valuation remains high across the P/E, EV/EBITDA, and even P/S. While certainly not overvalued compared to prior years, I do not expect significant upside from these levels unless major financial improvements occur. At the same time, downside is also limited as a few catalysts now exist.

Koyfin

One major catalyst investors may rely on is the fact that there is a new CEO in place. In fact, these Summer earnings are only his first, and the November report will be the conclusion of his first 100-day period. This quarter can be given as a transition period with the expectation for increased performance soon. While I will remain on the sidelines until data suggest an improvement, I am sure plenty of investors consider the company a turnaround play. Per CEO Chris Fowler:

For our next call in early November, I will have completed my first 100 days as CEO, and I look forward to sharing more details and updates to our long-term vision at that time. However, I will call out three important items that are already in focus. First, is to identify opportunities for revenue growth acceleration through calculated internal investment in existing products and services and thoughtful M&A.

Second, and of course, complementary to the first is to thoroughly and regularly evaluate our capital allocation strategy to ensure that we fully take advantage of our strong balance sheet and cash flows in order to provide maximum shareholder return. And finally, to aggressively accelerate the work already in progress to build and maintain an always evolving culture of innovation and digital transformation at CPSI.

After 22 years of working at CPSI in various positions, my first month as CEO has been indescribably challenging, rewarding and enjoyable. In meetings with leaders of our hospital and post-acute customers, it's clear they continue to work daily in the stress of endless regulatory, economic and competitive pressures and that they need a partner that can provide a platform of services and solutions for their operations, clinicians and patients so that they can solely focus on providing the highest quality of patient care. We will be that partner.

If CPSI's valuation falls below the levels shown in the chart above, I believe there may be a better risk/reward proposition due to the stickiness of the business. However, investors will continue to face volatility and instability of the share price, along with limited upside even if the company is successful for a time. When facing the historical fact of performance in the image below, I believe I will be staying on the sideline in perpetuity.

10 Year CAGR data, with emphasis by Author (Seeking Alpha)

Higher Growth Won't Save CareCloud

The story is the same for CareCloud ( MTBC ). The company is another "innovator" who solicits software and services for healthcare providers to optimize their operations. On the surface, the company lured in investors with fast growth, cloud-based services, and even significant profitability. Unfortunately, as a sub-$100 million market cap company, significant risk has led to both a decrease in share price, risky balance sheet management, and lagging organic growth. As such, I find this is another name to avoid, albeit with a twist I will discuss later.

{kind=link}

As shown in the chart below, CareCloud seems to offer significant revenue growth opportunity. While this is true as the five-year annual growth rate hovers between 20-30% per year, this is due to two factors. First, the incredibly small size of the company allows for lumpy revenues as new large customers are picked up. This is mostly the result of acquisitions, much like care cloud, and organic growth in-between acquisitions is usual ~10% YoY instead of 20-30%.

This bolt-on acquisition business style only works as long as there are profits to drive towards growth and a strong balance sheet. Thankfully, the company offers fairly strong EBITDA growth recently. The current 15% EBITDA margin allows for reinvestment into growth, and may allow for revenues to continue the upward trend.

Koyfin

However, cracks are beginning to form in the balance sheet as a result of the acquisitions. The glaring issue is having more debt than cash, although cash is only $4 million less than total debt as of the last earnings. I find the bigger issue is the significant dilution, at approximately 10% per year. Investors must stay long until buybacks increase earnings per share or else this is a significant reduction in total return. However, if expenses and investments are managed from this point, the favorable pattern in FCF increases may allow for a reduction in dilution and debt moving forward.

Koyfin

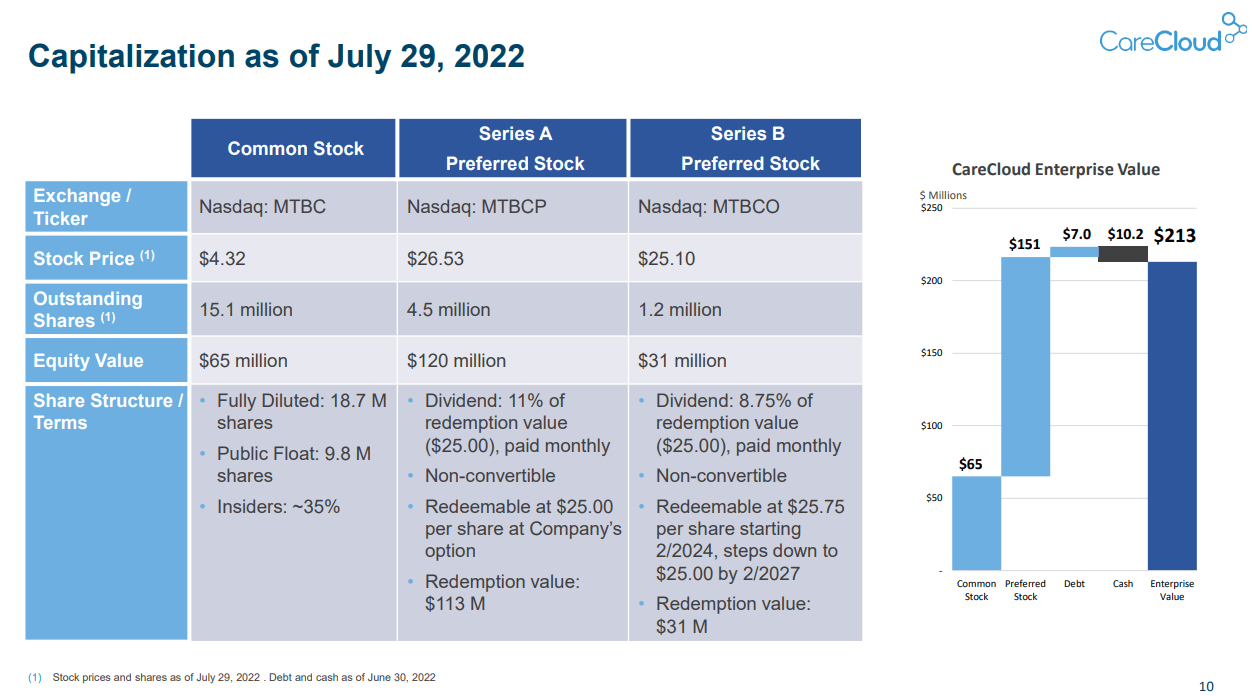

Unfortunately, that is not the end of the line for the weak balance sheet. Instead, CareCloud is one of the smallest companies on the market to list preferred shares, with both series totaling $150 million in capital as of July 29th. These expensive 11% and 8.75% dividend rates are extremely costly, and one wonders who thought these would be a good idea. This is one reason why EBITDA has increased over the past few years because CareCloud had to rein in costs to supply the preferred dividend. And, over the next few years all earnings will be going into either redeeming these preferred shares or paying the large dividend, inhibiting the company's ability to reinvest in growth.

Significant costs per year to pay off debt and match dividends. (Seeking Alpha)

{kind=link}

{kind=link}

As a result of the significant capital being measured in the preferred shares, rather than the normal market listing, the current enterprise value of CareCloud is $215 million rather than the $65 million share price. As such, investors must disregard valuation metrics that do not take into account "paid in capital", the preferred shares. Unfortunately, Seeking Alpha and Koyfin do not add the preferred shares to their EV values. Therefore, the chart below is a lie, and must not be considered for the investment.

The current valuation is deceptively low. (Koyfin)

Instead, the true value of the company is a "price" ($216 million in capital) to sales of 1.5x ((TTM)). In terms of EBITDA, the company is trading at a 11.7x ((TTM)). Now we come full circle, as these values now match to CPSI to a tee as I highlighted. Therefore, as I would not believe in CPSI's current valuation as favorable, I feel the same for CareCloud.

Sure, investors can consider the preferred shares as less not part of the valuation, but they certainly drag on performance and I would include them in my analysis. In fact, with the associated risk due to the high cost of managing the preferreds, I say CareCloud does not offer a favorable risk/reward profile. The only benefit I see is if you are seeking a 11% dividend yield, as seeking capital gains on the normal shares is best to be avoided.

Conclusion

Unfortunately, labeling a company as "cloud-based" or "innovative" only works when industry peers are not doing the same thing, and the financials prove the narrative. Instead, small healthtech peers CPSI and CareCloud suffer from a lack of true organic growth and instead damage their balance sheets to drive inorganic revenue growth. Due to the risks, and lack of upside potential, I will stay on the sidelines in regards to CareCloud and CPSI. In terms of the healthcare industry, the strongest names will have the highest valuations, meaning undervaluation is a red flag in my eyes. You get what you pay for.

Thanks for reading. Feel free to share your thoughts below.

For further details see:

Computer Programs and Systems And CareCloud: Avoid These 2 'Innovators'