CPSI - Computer Programs and Systems: Undervalued Recurrent Revenue And Beneficial Expectations

2023-08-31 21:22:16 ET

Summary

- CPSI is a leading healthcare solutions company. CPSI serves community hospitals and health systems, with a special focus on smaller facilities.

- I believe that further growth through cross-selling, customer retention, and expansion into competitive segments could bring significant net sales growth in the coming years.

- Assuming a WACC of 5%-7.5% and an EV/FCF of 15x-21x, the implied price would stand at about $15-$29, and the IRR would be mostly positive.

Computer Programs and Systems, Inc. ( CPSI ) recently delivered beneficial expectations of long term growth for each of its business segments, and noted a lot of recurrent revenue. I took into account that standardization, automation, digital innovation, and SaaS offerings could accelerate FCF margin growth. Besides, I believe that new RCM solutions and cross-selling efforts could represent a beneficial net sales growth catalyst in the coming years. There are obviously risks from failed acquisitions or new healthcare regulations, however I believe that CPSI does look undervalued.

Computer Programs and Systems: A Lot Of Recurrent Revenue And Beneficial Expectations

CPSI is a leading healthcare solutions company spanning six companies including Evident, AHT, TruBridge, Get Real Health, TruCode, and HRG. It focuses on improving community health, connecting patients, and optimizing financial operations.

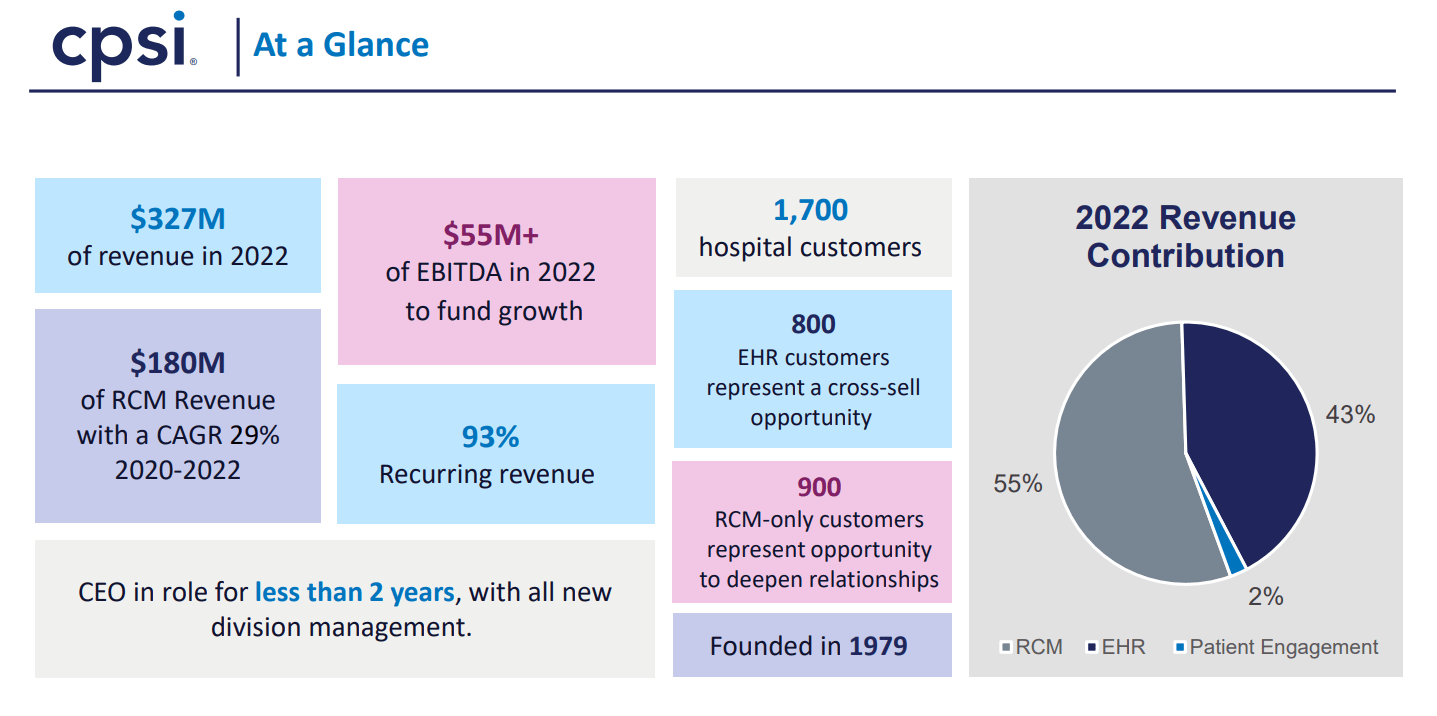

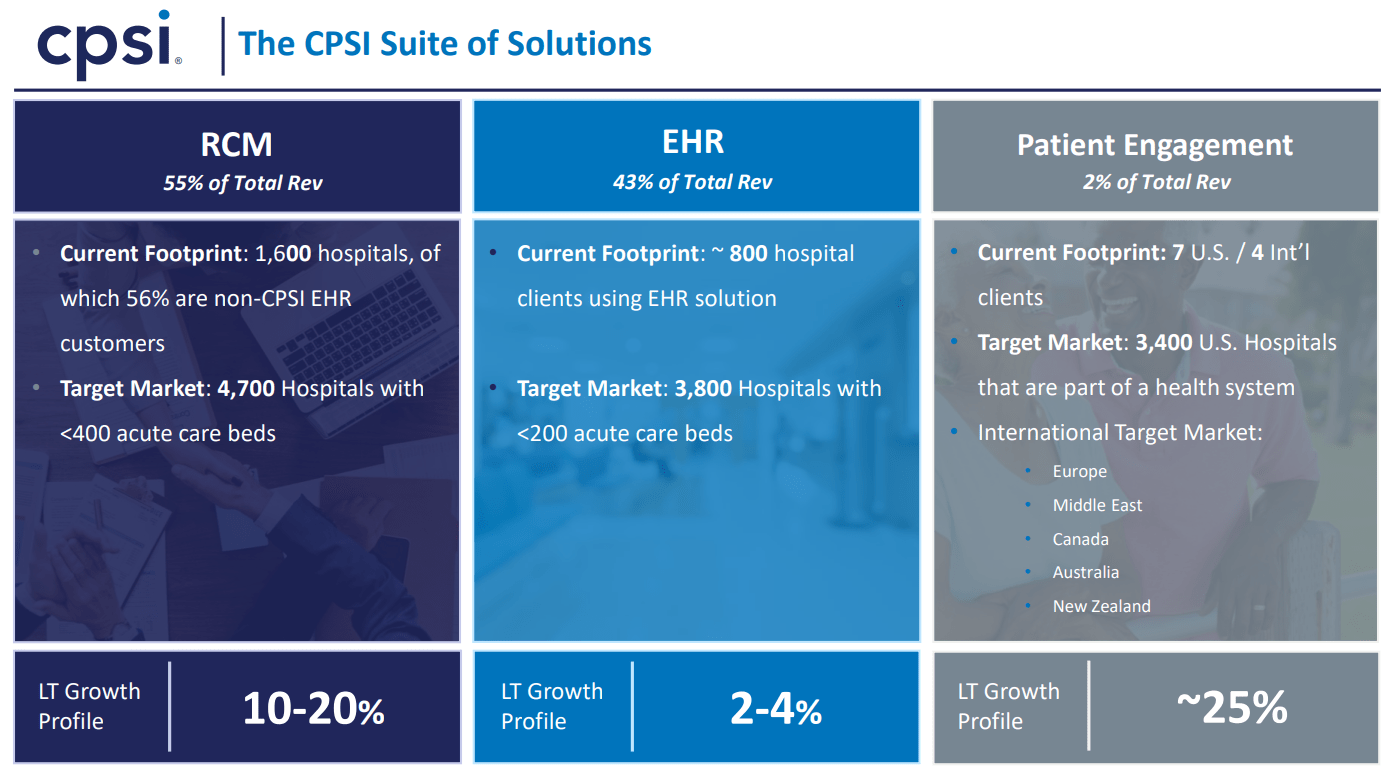

Its segments are RCM (revenue cycle management), EHR (electronic health records), and Patient Engagement. RCM offers business and IT services along with RCM solutions. EHR provides comprehensive EHRs for hospitals and post-acute care. Patient Engagement focuses on empowering patients and providers. CPSI serves community hospitals and health systems, with a special focus on smaller facilities. In 2022, the company generated $326.6 million in revenue, including 93% of recurrent revenue.

{kind=link}

Computer Programs and Systems provided optimistic expectations about the future long term growth of RCM, EHR, and Patient Engagement. I believe that these figures are the most interesting part of the business model. The RCM business model is expected to grow at close to 10%-20%, and Patient Engagement would grow at close to 25%. With these figures in mind, I decided to run a financial model to understand whether the stock was undervalued.

{kind=link}

Beneficial Market Expectations Including FCF Growth And Net Sales Growth

Market analysts are expecting sales growth in 2023, 2024, and 2025, along with EBITDA growth and EBIT growth. From 2023 to 2025, the net margin is also expected to increase. 2025 net sales would stand at close to $389 million, with 2025 EBITDA close to $65.4 million, 2025 EBIT of $30.3 million, and 2025 net margin of about 5.85%.

Source: Market Expectations

It is also worth noting that most analysts out there are expecting free cash flow growth, from $11 million in 2023 to about $41.6 million in 2025. With this in mind, I believe that running a DCF model makes a lot of sense here.

Source: Market Expectations

Balance Sheet: The Net Debt/EBITDA Ratio Appears Under Control

As of June 30, 2023, Computer Programs and Systems reported cash and cash equivalents worth $7 million, with accounts receivable close to $54 million, prepaid expenses worth $12 million, and total current assets of about $82 million.

The company also reported property and equipment worth $8 million, software development costs of $36 million, intangible assets worth $93 million, goodwill of $198 million, and total assets worth $434 million. With an asset/liability ratio of about 2x, I believe that the balance sheet appears in good shape.

Source: 10-Q

I am not really worried about the total amount of liabilities or debt. The financial debt/EBITDA stands at less than 3x, and Computer Programs and Systems reported much more leverage in the past. In my view, further decrease in the total amount of debt may lead to an increase in the stock price.

Source: Ycharts

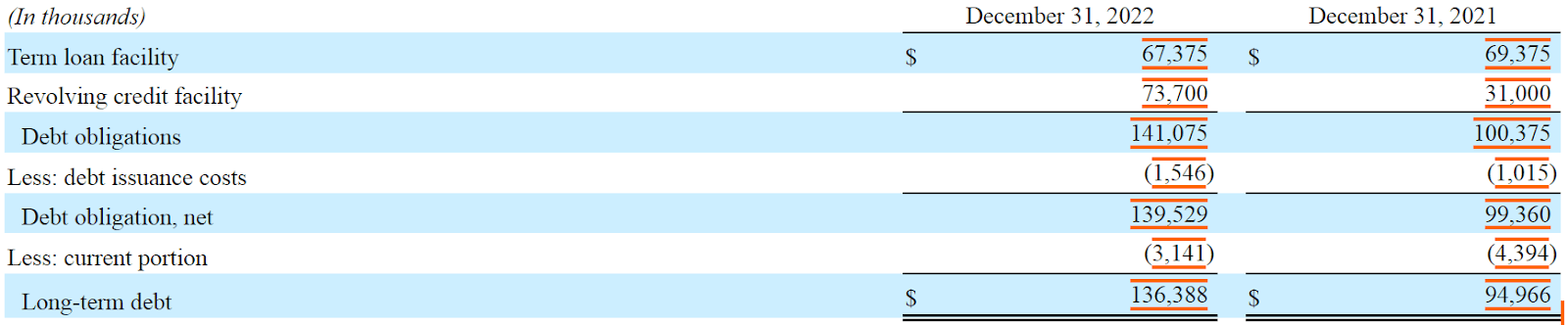

The list of liabilities includes accounts payable worth $14 million, current portion of long-term debt close to $3 million, deferred revenue worth $9 million, long-term debt of about $141 million, and total liabilities of $204 million.

Source: 10-Q

Fist Net Sales Catalyst: New RCM Solutions And Cross-selling Would Most Likely Multiply Net Sales

I believe that further increase in RCM solutions and services market, cross-selling to existing EHR customers, expansion into new hospitals, and health systems could accelerate net sales growth. In this regard, it is worth noting that the company worked with a consultant on these matters. I could not identify the name of the consultant, but it was said to be a top-tier international consulting firm.

We engaged a top-tier international consulting firm to assess our core growth strategy, with the outcome of this eight-week engagement being the confirmation of our current core strategy and the identification of other innovative potential growth opportunities. Source: 10-Q

Inorganic Growth Could Also Accelerate Net Sales And FCF Generation

It is also worth noting that Computer Programs and Systems bought other companies in the past, and expects to do the same in future. Since 2016, goodwill has increased significantly. Perhaps, management may have to lower its net debt/EBITDA to engage into new acquisitions, however given the expertise in the M&A markets, we could expect new acquisitions.

We may also seek to grow through acquisitions of businesses, technologies or products if we determine that such acquisitions are likely to help us meet our strategic goals. Source: 10-Q

Source: Ycharts

Standardization, Automation, Digital Innovation, And SaaS Offerings Could Also Accelerate Growth

I also believe that optimizing margins through standardization, automation, and the use of external resources will likely improve efficiency and save costs. Besides, driving digital innovation by providing patient engagement solutions that foster collaboration and improve health outcomes could represent a FCF growth catalyst. Finally, I am quite optimistic about the SaaS offerings, which may bring more interesting clients, and existing clients may use the products of Computer Programs and Systems a bit more.

These SaaS offerings are attractive to our clients because this configuration allows them to obtain access to advanced software products without a significant initial capital outlay. We expect this trend to continue for the foreseeable future, with the resulting impact on the Company’s financial statements being reduced EHR revenues in the period of installation in exchange for increased recurring periodic revenues over the term of the SaaS arrangement. Source: 10-Q

Limited Contractual Obligations

In January 2016, the company acquired HHI, and entered into a syndicated loan agreement with Regions Bank for $175 million. Interest rates are based on SOFR or an alternative base rate. Quarterly installment debt payments are about $0.9 million through March 2027. Revolving debt is due as per the dates given below.

{kind=link}

{kind=link}

My Expectations

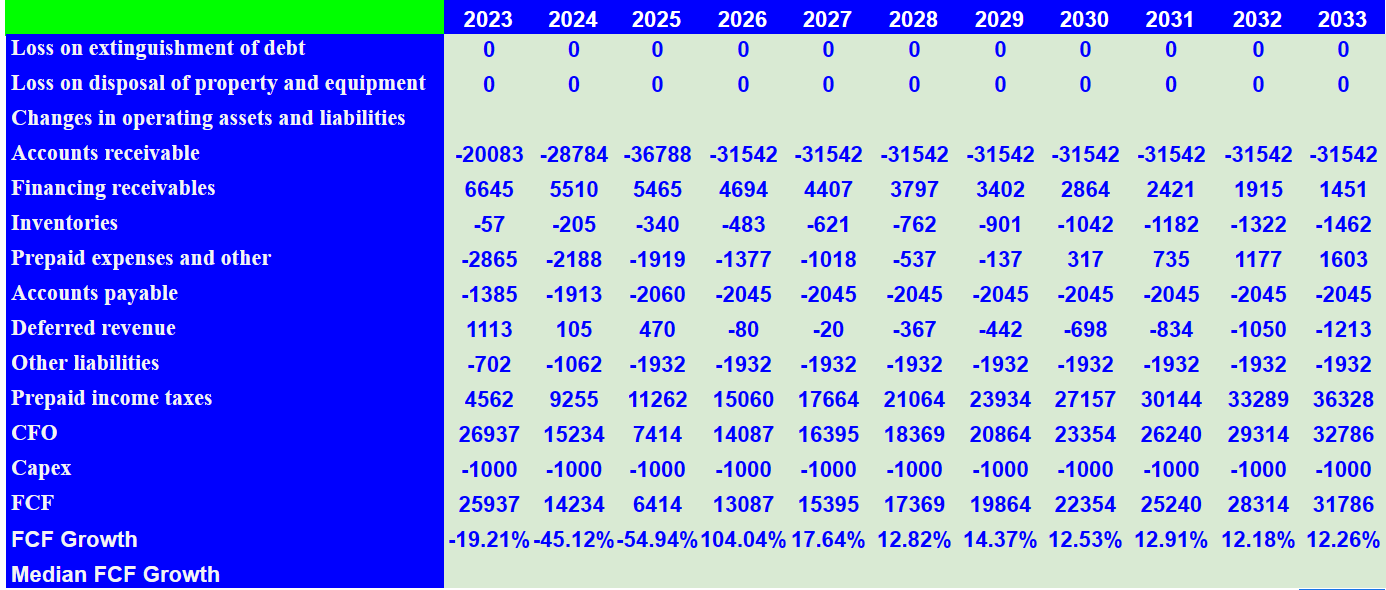

I made a few forecasts with regard to the three business segments reported by Computer Programs and Systems. The sales growth for the three segments is close to that expected by management in recent presentations. Using those expectations, 2033 RCM net sales would stand at about $513 million, with EHR net sales close to $173 million and patient engagement of about $80 million. 2033 Total sales would stand at about $768 million, with net income of $33 million and net income / sales close to 4%.

{kind=link}

Adjustments to net income also included 2033 provision for bad debt worth -$18 million, with deferred taxes close to -$69 million, 2033 stock based compensation of $2 million, and depreciation worth $5 million.

Besides, I also foresee 2033 amortization of acquisition-related intangibles worth $51 million, amortization of software development costs of about $23 million, no amortization of deferred finance costs, and no gain on contingent consideration. Finally, with 2033 changes in accounts receivable close to -$32 million, changes in inventories close to -$2 million, and prepaid expenses worth $1 million, 2033 CFO would stand at $32 million.

{kind=link}

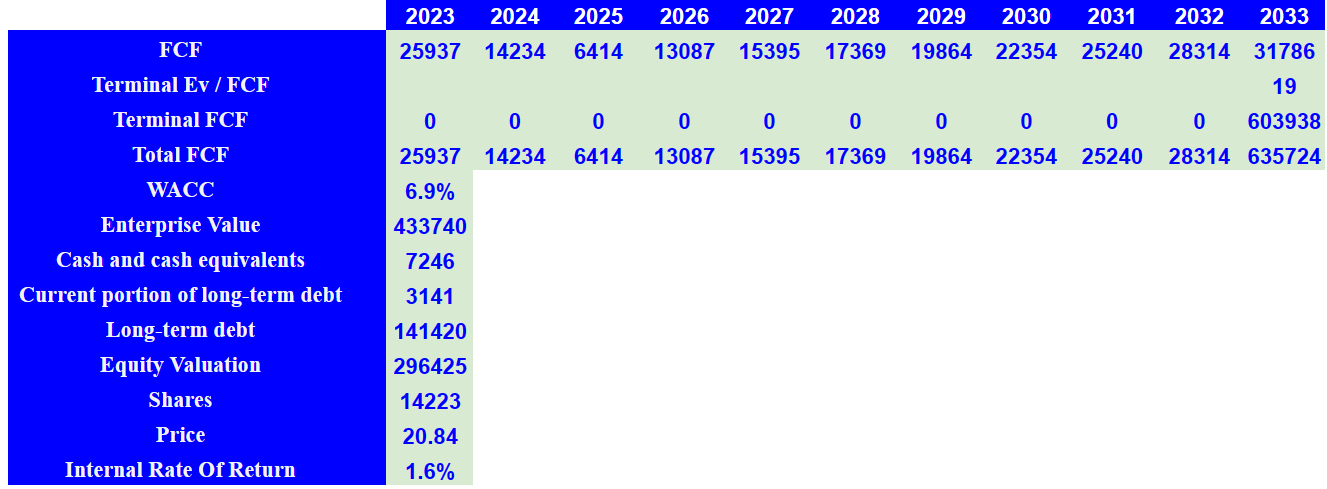

If we also assume capex of about -$1 million, 2033 FCF would be $31 million. Now, with a WACC of 6.9% and EV/FCF of 19x, the enterprise value would be about $433 million. Note that the previous EV/FCF stays at around 30x-14.9x, so my numbers are conservative.

Source: Ycharts

Adding cash and cash equivalents of $7 million, and subtracting the current portion of long-term debt worth $3 million and long-term debt of $141 million, the implied price would be $20.84, and the internal rate of return would be 1.617%.

Source: My Expectations Source: My DCF

{kind=link}

{kind=link}

Sensitivity Analysis

I believe that the model appears solid as significant changes in the WACC or the EV/FCF do not lead to significant changes in the implied price or the IRR. Assuming a WACC of 5%-7.5% and an EV/FCF of 15x-21x, the implied price would stand at about $15-$29, and the IRR would be mostly positive. I do believe that stock appears undervalued.

Source: My Sensitivity Analysis Source: My Sensitivity Analysis

Risks From Failed Acquisition, Goodwill Impairment, Or New Regulations

The healthcare industry is highly regulated, and changes due to political and legislative dynamics. Complying with direct and indirect regulations is vital. Anti-fraud law, e-prescribing, claims transmission, medical devices, and data privacy are key areas. Besides, the company may suffer significantly if Medicare and Medicaid reimbursements are reduced in any incoming regulation.

The Health Reform Laws will continue to affect hospitals differently depending upon the populations they serve and their payor mix. Our target market of community hospitals typically serve higher uninsured populations than larger urban hospitals and rely more heavily on Medicare and Medicaid for reimbursement. It remains to be seen whether the increase in the insured population for community hospitals will be sufficient to offset actual and proposed additional cuts in Medicare and Medicaid reimbursements contained in the Health Reform Laws. Source: 10-k

Besides, interoperability standards, patient access rights, and ICD-10 codes influence the business model. Compliance with regulations is essential, and future changes may affect products and development costs. Regulations can result in penalties and costs, and affect future reputation and FCF growth.

The company reports a significant amount of goodwill. Goodwill impairments and intangible asset impairments may lead to lower book value per share and stock price declines. Note for instance that the acquisition of Healthcare Resource Group included goodwill worth close to $20 million, which is a significant part of the net assets. The net assets acquired stood at $47 million.

Source: 10-k

Many Competitors

The market in which the company operates is highly competitive, with technological changes, regulations, and changing needs. Factors such as security, functionality, services, customer satisfaction, integration, and price are key in the choice of users. Its competitors include RelayHealth, SSI Group, Change Healthcare, Resolution Health, Ensemble Health (ENSB), Cerner, Meditech, PointClickCare, and MatrixCare in post-acute care. Although the company faces competition, it positions itself favorably on these factors. Competition also comes from providers of management systems and technology in a dynamic and changing market.

Conclusion

I believe that further growth through cross-selling, customer retention, and expansion into competitive segments could bring significant net sales growth in the coming years. Besides, taking advantage of efficiency and margin optimization, FCF growth could also trend higher. Yes, there are risks due to intense competition in an ever-changing technological and regulatory environment, however in my view, there is room for improvement in the stock price.

For further details see:

Computer Programs and Systems: Undervalued, Recurrent Revenue, And Beneficial Expectations