SWN - Comstock Resources: Serious Cash Flow Debt And Dividend Headwinds Loom

2024-01-22 04:17:43 ET

Summary

- Comstock Resources (CRK) is expected to continue underperforming due to high costs and limited hedge coverage for 2024.

- The company is projected to have a cash flow outspend of up to $500 million in 2024, leading to a deterioration in its credit position.

- CRK may need to cut capital expenditures and eliminate its dividend to preserve cash.

- The stock faces a potential negative borrowing base redetermination on its credit line this spring.

Back on April 26, 2023, I wrote a bearish article on natural gas-focused producer Comstock Resources ( CRK ) titled " Comstock Resources: 2023 Will Be Messy ."

My thesis was simple: CRK's high cash breakeven cost coupled with low natural gas prices and limited hedge coverage through 2023 would result in a significant cash flow outspend and rising leverage. That would be further exacerbated by the company's decision to initiate a $0.125 per share quarterly dividend payment in late 2022.

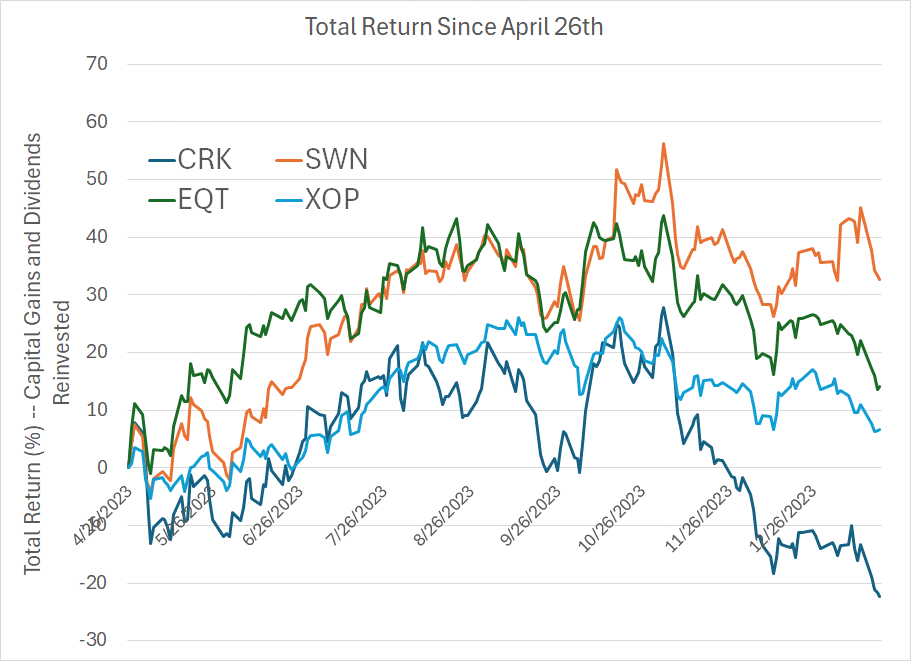

Since that time, CRK has fallen more than 22%, underperforming gas-levered peers like Southwestern Energy ( SWN ), a stock I covered in a recent Seeking Alpha piece and EQT ( EQT ) as well as the widely followed SPDR S&P Oil & Gas Exploration & Production ETF ( XOP ):

{kind=link}

Despite a constructive outlook for natural gas prices into 2025/26 and the potential for more merger and acquisition (M&A) activity following Chesapeake's ( CHK ) recent offer to acquire SWN, CRK is likely to continue to underperform this year.

CRK's cost structure remains too high and, based on my calculations, the company is unlikely to generate significant free cash flow until NYMEX gas prices recover over $3.65/MMBtu. Further, unlike fellow producers in the Haynesville, SWN and CHK, CRK has limited hedge coverage for 2024, leaving its cash flows leveraged to near-term swings in gas prices.

On course for a cash flow outspend of as much as $500 million in 2024, the company will see continued deterioration in its credit position, the potential for lenders to cut its borrowing base this spring and/or the need to eliminate its dividend to preserve cash.

Let's start with this:

Costs and Free Cash Flow

When I evaluate a producer's ability to generate free cash flow, I start by creating a simple production and cost model based on historical results and management guidance.

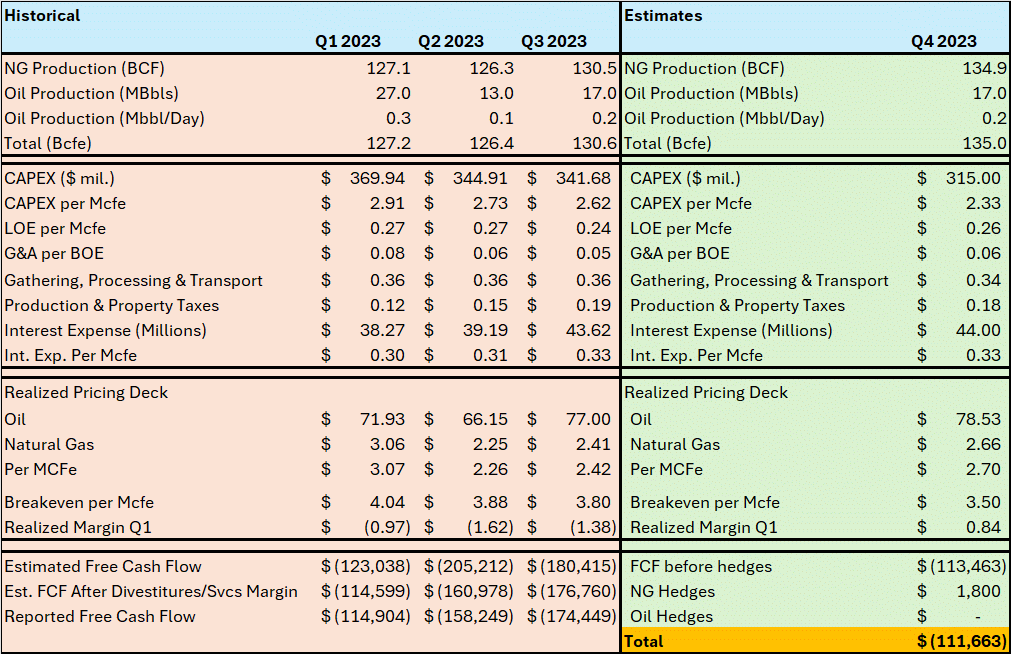

Here's a look at my historical cost model for CRK in quarters 1 through 3 of 2023 with Q4 estimates based on the company's guidance presented along with CRK's Q3 Call in October:

Production, Cost and Cash Flow Model for CRK in 2023 (Bloomberg, CRK Q1, Q2 and Q3 Earnings Results)

{kind=link}

This table is divided into four main sections, which I've divided using horizontal double black lines. Let's start with production.

CRK is a natural gas producer focused on the Haynesville Shale field located in East Texas and Louisiana. This field is what's known as a dry gas play, meaning wells in the region produce primarily methane (natural gas) with only small ancillary volumes of oil and natural gas liquids ((NGLS)) like propane, ethane and butane.

CRK doesn't report any produced volumes of NGLs though the company does report some crude oil production each quarter.

Starting in the top section of my table above, the company produced between 13,000 and 27,000 barrels of oil per quarter in the first 3 quarters of 2023.

By convention, volumes of oil are converted into volumes of natural gas equivalent at a 1:6 ratio where 1 barrel of oil equals 6,000 cubic feet of natural gas equivalent. In Q3, for example, the company's 17,000 bbl of oil production equates to 102 million cubic feet of natural gas equivalent.

Also, by convention, I use the Roman numeral "M" to denote 1,000, "MM" to denote 1 million and 1 Million British Thermal Units (BTUs) of natural gas is equivalent to 1,000 cubic feet (1 mcf).

In the same quarter, CRK produced 130.5 billion cubic feet of natural gas, so oil accounts for less than 0.1% of quarterly output. Since CRK does report oil production each quarter, I've included it in my cash flow model for granularity even though it's close to irrelevant in terms of the company's business and cash flows.

The second section of my table deals with CRK's cost structure.

The big numbers to watch in this section include capital spending ((CAPEX)), Lease Operating Expenses (LOE), Gathering and Transport, and Production and Property Taxes.

CAPEX for CRK primarily represents money spent to drill and complete new gas wells on its existing acreage. The cost of drilling is self-explanatory; completion refers to costs incurred to fracture a shale well and prepare it for commercial production.

The CAPEX figure I've listed also includes spending on midstream infrastructure such as pipelines and outlays on leasing new acreage. These latter categories are smaller - for example, management's Q4 2023 guidance contemplates total CAPEX of $315 million of which more than 80% is drilling and completion (D&C).

Lease operating expenses (LOE) refer to the costs involved with maintaining and supporting production from existing wells while Gathering, and Transportation refers to the costs associated with moving natural gas from wellhead to market using pipelines. Production & Property Taxes are not income taxes, but taxes paid based on the revenues generated from sales of natural gas and oil produced from the company's acreage.

The remaining costs listed in my table -- general and administrative expenses (G&A), and interest paid on debt - are likely familiar to most investors and common to companies across most industry groups.

Also note that, unless otherwise indicated, all the line items in the cost section of my table have been reported in terms of dollars per thousand cubic feet of natural gas equivalent production ($/mcfe).

The third section of my table shows realized prices for crude oil and natural gas production for each quarter. The company includes realized pricing data in its quarterly earnings presentations for Q1 2023, Q2 and Q3 .

The company won't report Q4 earnings until February 14th. To estimate realized natural gas pricing in Q4 2023 I calculated the average daily closing price for natural gas futures in the months of October, November and December 2023 using data from Bloomberg and subtracted $0.27 per mcf.

I'm using a 27-cent discount to the NYMEX Henry Hub price of natural gas because it's the average of price discount realizations reported in the first three quarters of the year. Specifically, the company reported it sold gas at a $0.30/mcf discount to the NYMEX gas futures benchmark in Q1 2023, $0.29 in Q2 2023 and $0.23 in Q3 2023 before hedges.

For quarters 1 to 3 the realized prices listed on my table include any benefit from volumes CRK had hedged using swaps or options. For my Q4 estimate, I handle the hedge position as a separate line item at the bottom of the table - in CRK's Q3 call, the company reported it had hedged about 250 million cubic feet of gas production using options with a NYMEX floor price of $3/MMBtu.

Since the average price of NYMEX natural gas was under $3/MMBtu in Q4, I am factoring in about a $1.8 million benefit from CRK's hedges in the quarter.

The most important line item of all is labeled "Breakeven per Mcfe." This is simply the realized price of natural gas (and gas-equivalent oil volumes) CRK needs to break even on its cash costs of production. So, if the average price of natural gas is higher than this breakeven, CRK will produce positive free cash flow and if it's below this level, CRK is outspending cash flow.

Note that this breakeven price is not the NYMEX price of gas in a given quarter, it's the price CRK actually receives from selling its gas production.

For example, I've estimated that in Q4 2023 the company needs $3.50/Mcfe to cover all its cash operating expenses. However, recall that CRK sold its gas production at a $0.27/Mcf average price discount to NYMEX in the first three quarters of 2023 and I'm assuming a similar price differential in Q4.

So, that means NYMEX gas prices would have needed to average somewhere close to $3.77/mcf in Q4 for CRK to break even on this basis. However, NYMEX actually averaged a little under $3/mcf in Q4, so the company likely outspent cash flow by a significant margin.

Of course, oil production will also have a positive impact on the gas-equivalent price realizations and breakevens I've listed. The difference is slight because, as I illustrated earlier, crude oil volumes are such a tiny portion of the production mix. In the first three quarters of 2023, I calculate produced oil added about $0.01/mcfe to CRK's price realizations.

Bottom line: For CRK you can consider the reported cash flow breakeven prices as a breakeven price for natural gas in dollars per mcf. To approximate the NYMEX futures price of gas needed to break even, you can simply add $0.27/mcf, the average discount to NYMEX for CRK through the first three quarters of the year.

And that brings me to the fourth and final, section of my table, estimated free cash flow.

The first section of my table shows historical gas production and production estimates, the second shows cash costs and cost estimates and the third shows realized natural gas prices and estimates. We can use these 3 pieces of information to derive an estimate of CRK's ability to generate free cash flow.

For example, in Q1 2023 I calculated CRK's breakeven cost at $4.04/mcfe and the realized price per mcfe in that quarter was $3.07, so the company outspent to the tune of 97 cents per mcfe produced. That's more than $123 million in negative free cash flow -cash flow outspend - in Q1 2023 alone.

In Q2 and Q3 my simple model estimated some $205 and $180 million in negative free cash flow respectively. And, given the average prices of oil and natural gas recorded in Q4 2023 and the midpoint of management's production and cost guidance outlined in their Q3 2023 call, I am looking for negative free cash flow of about $111.7 million in Q4 even after accounting for hedges. As noted earlier, CRK will report its Q4 financials on February 14th.

As you can see, the estimated free cash flow figures I've listed for Q1, Q2 and Q3 2023 differ somewhat from the numbers CRK has actually reported each quarter. There are a few reasons why that's the case.

First, CRK includes some divestitures of land in free cash flow as well as profits derived from its services business - such as handling the transport of gas volumes on behalf of third parties - which are not captured by my model. That's because my model seeks to estimate only the profitability, or lack thereof, of the core production business.

Once we adjust for these effects, listed as "Est. FCF After Divestitures/Svcs Margin" my calculated FCF numbers have generally been close to the free cash flow numbers reported by CRK. The remaining differences are primarily a function of changes in working capital, not captured by my model, and some independent rounding of cost line items reported by CRK each quarter.

I'd expect estimates for future quarters to vary more widely because the discounts CRK earns to NYMEX can move around from quarter-to-quarter and even a small change in a line item like CAPEX can cause a swing in free cash flow estimates.

However, directionally these are useful estimates, and they also offer a useful guide to the magnitude of free cash flow or cash flow outspend we can expect from CRK over time.

And, as I predicted in my April 26th piece covering the stock in Seeking Alpha , 2023 was a messy year for CRK with the company likely outspending cash flow to the tune of around $560 million for the full year.

The Outlook for 2024

Unfortunately, when we step this analysis forward to contemplate 2024, the picture doesn't look any brighter.

Typically CRK offers guidance for the year ahead at the time they host their conference call covering fourth quarter results; the company recently confirmed that's scheduled for 10 AM Central Time (11 AM ET) on February 14, 2024 .

In CRK's third quarter conference call hosted back on October 31st, management did offer some more qualitative guidance for the 2024 outlook. Specifically, the company revealed it's currently running 7 rigs including 5 rigs in its core legacy Haynesville acreage and 2 rigs over in the Western Haynesville, which is across the state line in Texas. Management also indicated it expects to keep the same rig activity going into 2024.

Later in the same call, CRK also indicated the company has a goal to add a rig to the Haynesville - targeting the Western Haynesville acreage -- in 2024.

As I'll outline in just a moment, a significant number of new liquefied natural gas ((LNG)) export terminals are scheduled to come onstream along the US Gulf Coast by early 2025 and, thanks to its geographic proximity, the Haynesville is expected to be a significant source of gas to feed these new terminals.

So, CRK's desire to add to its rig count at some point in 2024 represents a desire to ramp up production activity to benefit from new demand for LNG exports. Management was crystal clear about this point during their conference call.

On the cost front, management noted:

We've seen some signs of deflationary pressures on service costs relative to earlier this year. We believe most of those improvements will be seen in 2024.

Source: CRK Q3 2023 Conference Call Transcript

Simply put, due to weak natural gas prices through much of last year, drilling and completion activity in the Haynesville has been falling. Per Baker Hughes , the total rig count in the Haynesville has fallen from as high as 70 active rigs in early February 2023 to 43 more recently.

As demand for drilling and fracturing services declines, services and contract drilling firms have been reducing their prices, which provides a cost break to producers like CRK. They're already seeing some of that in Q4 2023; management guided to the lowest quarterly CAPEX of 2023 in Q4 as I outlined in my estimates table above. However, CRK is also looking for most of the cost benefit to come in 2024 as the company's contracts covering drilling and completion activity continue to be repriced lower.

Further, the core of the Haynesville field is in Louisiana where producers have several years of drilling experience. CRK's western Haynesville acreage is a newer target of drilling activity and reservoir characteristics are different as management explains here:

So, I'll just kind of comment a little bit on the D&C [Drilling & Completion] cost. So we have -- this is a totally kind of a different casing design down here than what we have up in the core. It just takes a lot more days to drill the vertical part of the hole. And basically, the laterals get a lot more heat.

We've made a lot of headway of the first 7 wells we have produced and we targeted the Bossier, not entirely due to temperature, but partially due to temperature we've gotten a lot better at drilling at the higher temps. We've got -- of the next -- I think we've got 10 wells targeted to turn to sales next year. 8 of those are going to be in the Haynesville, 2 will be in the Bossier. So we are going to turn our focus to that. But we've still got some things that we've got targeted to put to work out here in the field, it's going to get the cost down. We feel considerable amount.

And then the one thing I want to emphasize is we're drilling single wells here. So when you look at the cost up in the core, everything up there is a multi-well pad. Either 2 or 3 well pads. So, you're getting 6%, 7%, 8% less cost, just via a multi-well pad versus these down here are single wells. So that alone is driving our cost up a little bit. But Jay is totally right. I mean you're looking at EURs [Estimated Ultimate Recovery] definitely potentially double what we have up in the core. And then the cost is going to -- we're going to make a lot of improvements on that going forward in the future.

Source: CRK Q3 2023 Conference Call Transcript

In the above quote, explanatory text included in brackets "[ ... ]" is my own, designed to add clarity.

Simply put, when a producer targets a new field, or region of a larger play, there's always a learning curve in drilling new wells. In this case, there are two main producing formations beneath acreage in the region, the Haynesville and the Bossier Shale. In the western part of their acreage, located in eastern Texas, CRK has found reservoir temperatures are higher as is the underground geologic pressure.

At the same time, the first 7 wells CRK has drilled and put into production in the region have proved to be prolific with estimated ultimately recoverable reserves (EURs) higher than in the company's core acreage.

Right now, however, drilling in this region is more expensive than in the core of the play for a few reasons. First, in the above quote, the company references the need for a different casing design in this portion of the play. Casing refers to the thick steel pipe that's used to line as well as its being drilled; differences in casing design can slow the drilling process, which appears to be the case for CRK based on the above comments.

Further, CRK highlighted reservoir temperatures on its laterals (horizontal well segments) as an issue. This too can slow drilling times and increase costs.

None of this is insurmountable. Technology exists to drill wells under all sorts of conditions and generally, over time and through experience, producers are usually able to reduce costs and improve the efficiency of their well designs.

The most important issue of all is the use of multi-well pads. Basically, this technique allows a producer to drill multiple wells with horizontal branches targeting several producing layers all from a small surface footprint or "pad." Since rigs only need to be moved short distances between wells, this process can increase efficiency and reduce drilling and completion times.

To start, CRK has been drilling single wells in the western Haynesville as it started testing the acreage. Over time, the company plans to switch to multi-well pads -- likely 2 to 3 well pads as it uses in its core Haynesville acreage -- which would reduce the cost by 6% to 8%.

Bottom line is that right now CRK has 2 rigs in the western Haynesville out of a total of 7 operating rigs, so the higher well costs in this part of the play are boosting CAPEX relative to what could reasonably be expected as the company gains experience and starts drilling multi-well pads.

However, the operative words are time and experience -- it will take time for the company to learn the best well designs and drilling techniques for wells in the western Haynesville and these cost savings to show up in results.

In 2024, management reported it has 10 wells that it plans to put into production and 8 of those will be targeting the Haynesville Shale formation rather than the Bossier. The latter was the target of CRK's early wells. So, there could even be some additional growing pains around targeting a different formation in the same region.

Through the entirety of 2023, CRK spent about $1.37 billion in CAPEX based on actual spending in Q1 through Q3 plus the midpoint of management's guidance for Q4 I outlined in my cash flow model.

Per Bloomberg, the consensus on Wall Street is for CRK's CAPEX in 2024 to come in at $1.153 billion, down around 16% from the full-year 2023 level. So, clearly, Wall Street is already looking for some significant cost savings and efficiency gains to roll through the company's results this year.

So, as a first effort at estimating CRK's 2024 cash flow breakevens, I'm assuming flat production at 2023 levels, I'm adopting the consensus Wall Street CAPEX outlook for $1.153 billion in total spend and I'm holding all other costs at their Q3 2023 level.

Here's what that means for CRK:

Production, Cost and Cash Flow Projections for CRK in 2024 (CRK Q1 to Q3 Earnings, Author's Estimates)

As you can see, the CAPEX estimate for 2024 is about $0.11 lower than Q4 2024 on a $/mcfe basis. That's partly offset by a $0.01/mcfe increase in interest expense per mcfe for a total $0.10/mcfe decline in the breakeven natural gas price CRK needs to generate free cash flow.

The increase in interest cost comes from the fact that CRK's debt under its credit line is about $345 million and that carries a floating interest rate indexed to the Secured Overnight Financing Rate (SOFR), a short-term benchmark interest rate that replaced the London Interbank Offered Rate (LIBOR) last year. I'm annualizing the Q3 2023 interest costs as SOFR rates are similar right now to where they were in Q3.

Regardless, the bottom line is that I calculate CRK would need to see natural gas price realizations in the $3.40/mcf range this year in order to generate enough cash to offset all of its expenses. And recall, CRK tends to sell its gas production at a $0.25 to $0.30/mcf discount to the NYMEX futures price of natural gas.

That means CRK would need NYMEX natural gas prices to average around $3.65/Mcf this year just to break even on a cash basis.

To make matters worse, these cash flow projections don't factor in the company's existing dividend of $0.125 per quarter or $0.50 annualized, which equates to an annualized cash payout of an additional $138.5 million.

CRK On Track to Bleed Cash in 2024

The current NYMEX natural gas futures curve just doesn't support prices even close to those breakeven estimate levels:

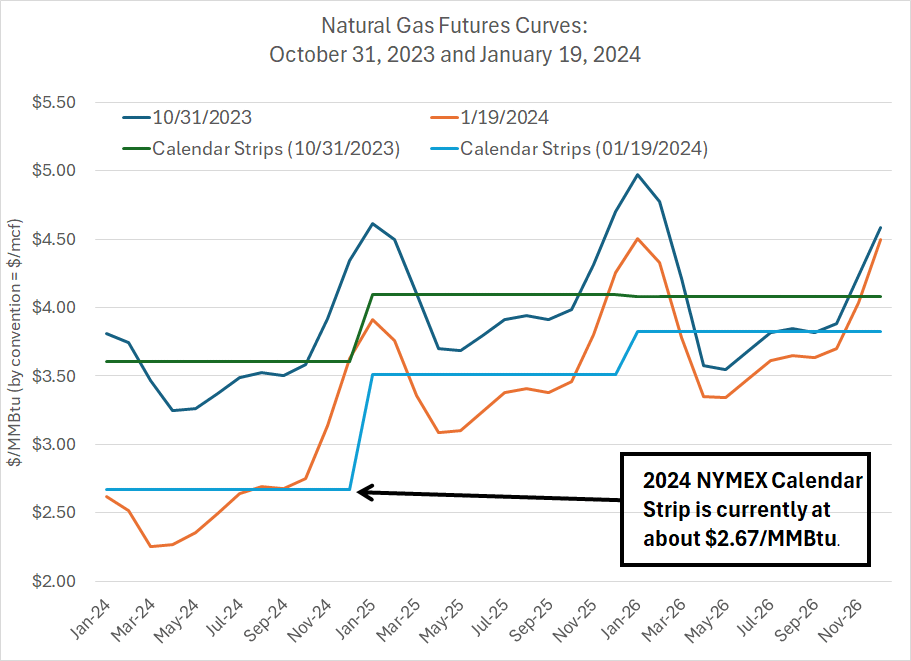

Natural Gas Futures Curves on October 31st and January 19th (Bloomberg)

{kind=link}

This chart shows the trading price of NYMEX natural gas futures contracts for delivery in every month from January 2024 through to the end of 2026 priced on two different dates, October 31st when CRK reported Q3 2023 earnings, and January 19th, 2024.

I've overlaid the calendar strips for each calendar year - this is simply the average price of NYMEX gas for the 12 monthly futures contracts in each year.

Using the average price for natural gas so far in January 2024, and the January 19th closing price of NYMEX gas futures for delivery between February and December 2024, the 2024 calendar strip for NYMEX is just $2.67/MMBtu (by convention equivalent to $2.67/mcf).

That's a full $1/mcf lower than what I estimate CRK would need to break even on a cash basis this year even before paying out that quarterly dividend on common shares.

This free cash flow math is discouraging. Using the $2.67/mcf 2024 calendar strip for NYMEX I just calculated, less a $0.27/mcf pricing discount for CRK realizations, alongside the cost and production estimates I just outlined, I calculate CRK generating negative free cash flow over $500 million in 2024 before hedges.

And CRK's hedges won't save it. As of the end of October when CRK reported its Q3 earnings results, the company only had hedges in place covering about 350 million cubic feet per day (Mmcf/day) of 2024 production using swaps:

CRK's Hedge Positions Through 2024 (CRK Q3 Results Presentation)

According to CRK's latest investor presentation, all hedges for 2024 are in the form of fixed price swaps struck at $3.55/mcf, so this table lays out the approximate quarterly cash settlements related to CRK's hedges, totaling almost $113 million for the full year.

If I take the negative cash flow estimate at $514 million derived and subtract the $113 million cash flow benefit from hedges, I come up with negative free cash flow for the full year of around $400 million:

CRK's 2023 Free Cash Flow Projections (CRK Results, Author's Estimates)

Per Bloomberg, the consensus on Wall Street is for a smaller outspend, some $220 million in 2024.

However, some of these estimates are stale and haven't been updated since shortly after the company's late October call when the 2024 natural gas strip price was higher than today (see my chart earlier). Also, per Bloomberg, the lowest estimate for CRK free cash flow in 2024 is negative $460 million, even worse than my estimate.

And keep in mind this is cash outspending before the company's $138.5 million annual dividend to common shareholders.

A cash flow outspend at just half my estimate -- $200 million for 2024 - adds up to almost $340 million including dividends. That's just not a sustainable situation for CRK this year and something will have to give.

Let me explain:

Debt, Spreads and the Credit Line

As I outlined earlier, CRK generated negative free cash flow of more than $447 million through the first 3 quarters of 2023 and, if we include my estimates for Q4, the total will come to negative $560 million for the full year.

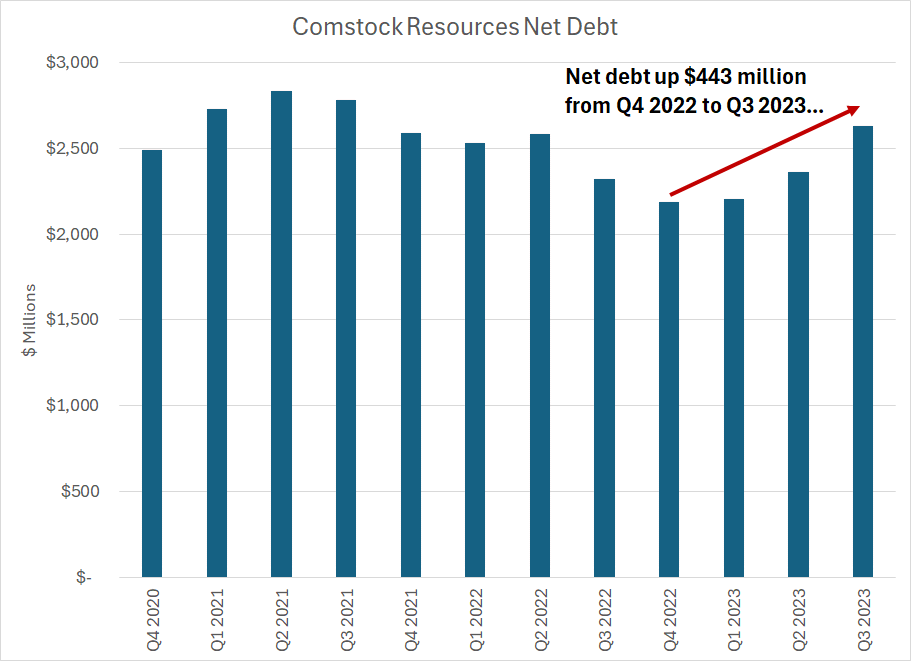

Because of that outspending coupled with the need to fund its common stock dividend, CRK's net debt position has been steadily deteriorating:

{kind=link}

As you can see, CRK used strengthening price realizations for natural gas in 2021 and 2022 to help pay down its net debt through the final quarter of 2022.

However, persistent weakness in free cash flow since that time, coupled with weak hedge coverage and the decision to pay a cash dividend, have reversed those gains - net debt ended Q3 2023 at $2.632 billion, up $443 million from the Q4 2022 lows. According to Bloomberg, total debt to earnings before interest, taxation, depreciation and Amortization (Debt to EBITDA) has doubled from a low of 1.1 times in Q4 2022 to 2.2 times as of Q3 2023, less than a year later. That's due to a combination of rising debt and falling earnings in the weaker commodity price environment.

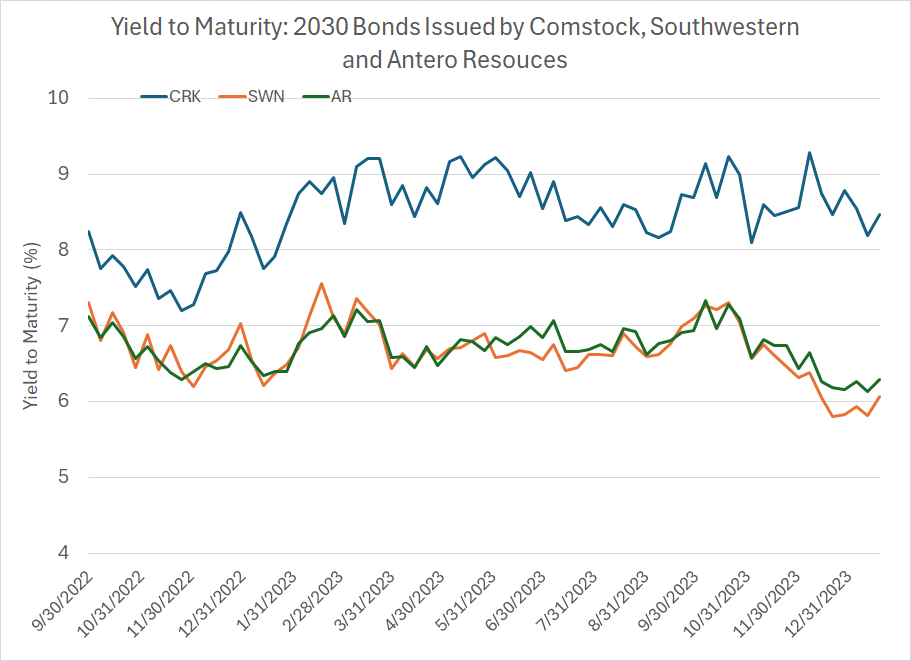

Bond markets have noticed the deterioration in credit quality and the difficult free cash flow math I outlined for 2024:

{kind=link}

This chart shows the yield to maturity for bonds issued by three different gas-focused exploration and production companies: Southwestern Energy, Comstock and Antero Resources ( AR ).

I chose SWN and AR to compare with CRK because both companies have relatively high net debt positions - according to Bloomberg, AR's net debt at the end of Q3 was $4.74 billion while SWN's was $4.25 billion.

However, it's clear that since the end of 2022, CRK's 2030 bonds have underperformed both its peers. As you can see, at the end of 2022 CRK's 2030 bonds offered a yield of 8.5% compared to SWN at 7% and AR at 6.73%.

At the end of August 2023, CRK's bonds offered a yield of a little over 8.5% compared to SWN at 6.73% and AR at 6.93%. And as of January 19th, CRK bonds still yield 8.47% compared to 6.07% for SWN and AR at 6.29%.

Granted, SWN received a takeover offer from Chesapeake Energy ( CHK ) early this month, leading to some of the outperformance for SWN of late. However, it's clear CRK's bonds have underperformed and the spread between CRK's borrowing costs and those enjoyed by peers like SWN and AR is widening as credit markets respond to the deteriorating fundamentals I just outlined.

A serious near-term risk CRK faces is its semi-annual borrowing base redetermination scheduled for this April.

Simply put, CRK has a $1.5 billion credit line facility with a consortium of banks; as of the end of Q3, the company had only drawn $345 million on this facility, leaving $1.155 billion of available borrowing power on the revolver.

This revolving credit line is secured by collateral in the form of what's known as a "borrowing base." In this case, the banks redetermine CRK's borrowing base twice per year in April and October and, according to the latest 10-Q from November , the borrowing base represents "substantially all of the assets" of CRK.

Typically, banks agree to extend credit up to a certain percentage of the borrowing base - in this case, the banks have agreed to a credit line of $1.5 billion backed by a borrowing base of $2 billion (75%).

During the company's Q3 earnings call management indicated the banks had reaffirmed CRK's borrowing base at $2 billion in October, so the company still has the capacity to borrow up to $1.5 total under the credit line facility.

However, the next redetermination looms this spring and, since October, the company has continued to outspend cash flow.

Moreover, take a quick glance at the futures curves for gas I outlined earlier and you'll see the near-term commodity price outlook has deteriorated significantly since October. At the time of the company's Q3 2023 earnings call on October 31st, 2024 NYMEX calendar strip stood at $3.61, pretty close to the level CRK needs to break even on a free cash flow basis as I calculated earlier.

As of Friday, January 19, the 2024 strip had collapsed to $2.67, implying cash flow outspend of similar magnitude to 2023 and the need to draw down credit lines for CAPEX and to pay dividends.

The first half of 2024 looks particularly problematic. The Q1 2024 calendar strip is at $2.46/MMBtu and the Q2 2024 strip is now $2.37 compared to $3.68/MMBtu and $3.29/MMBtu at the end of October respectively. That implies a rapid rate of cash burn to start 2024.

Granted, the futures curve points to a significant recovery in gas prices into 2025 and even more by 2026 with upside catalyzed by new LNG export terminal start-ups by late 2024 and early next year. However, that's a long valley of negative free cash flow between Q4 2023 and Q1 2025.

Bottom line: I believe there's a risk CRK's lenders look at the deteriorating cash flow picture, the steady rise in net debt and the company's underperforming bonds and decide to adjust the borrowing base lower, effectively cutting the amount CRK can borrow under its credit facility.

More broadly, I believe CRK faces some tough decisions in 2024.

To be fair to management, back at the end of October the company indicated that it planned to start 2024 with 7 operating rigs and hoped to add a rig in the western Haynesville acreage at some point this year. However, management did indicate on the call that their CAPEX and drilling plans could change with commodity prices and, as I've explained, near-term commodity prices were far higher at that time than today.

So, I suspect CRK will need to cut CAPEX in 2024 to preserve free cash flow, possibly by eliminating rigs from their drilling plan. Most likely this will mean allowing their production to decline over the course of 2024 and/or drilling fewer wells in the western Haynesville to prove the worth of this acreage.

I also suspect CRK will need to consider eliminating their cash dividend because it's tough to justify a continued $0.125 quarterly payout - a 6.3% yield at the current quote - when you're facing a massive free cash flow outspend for 2024.

And even if CRK eliminates its dividend and cuts CAPEX, I believe there remains risk of continued deterioration in the credit profile or a negative borrowing base redetermination this year.

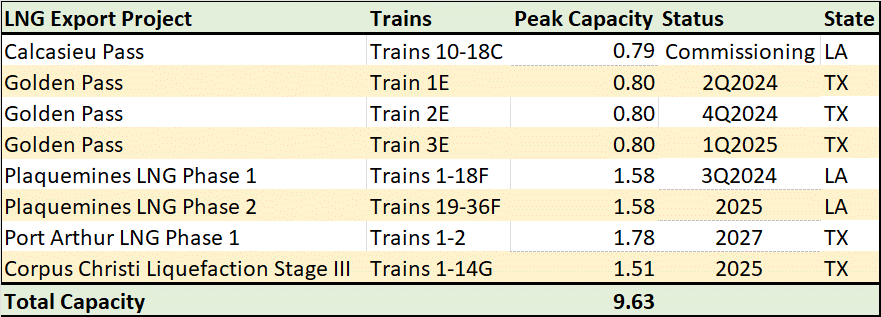

The main reason the US gas futures curve has a distinct upward slope - the calendar strip for 2025/26 is higher than 2024 - is the expectation that new LNG export facilities go into service late this year and in early 2025.

LNG Export Terminals Under Construction (Energy Information Administration)

{kind=link}

This table shows data collected by the Energy Information Administration regarding new LNG terminals due for start-up between 2023 and 2027.

As you can see, EIA had penciled in the Golden Pass LNG export project to come onstream in stages between Q2 2024 and Q1 2025. However, Exxon Mobil ( XOM ), the builder of the project, pushed back the timetable slightly last month -- Train 1 is now due for completion at the end of 2024 with first LNG in the first half of 2025.

While the EIA has yet to update its LNG construction timetable, this likely pushes back some of the expected surge in US LNG demand by 3 to 6 months from late 2024 into early 2025.

That's not a huge surprise in my view. Golden Pass is a truly massive construction project that's likely to cost project partners Exxon Mobil and Qatar Energy $10 billion once complete. The application and permitting process for Golden Pass started way back in 2012 and construction started in 2019. Simply put, when you're dealing with a multi-year, multi-billion-dollar project like this, some delays are almost inevitable.

However, even a delay on the order of 3 to 6 months can be meaningful for a company like CRK, which needs higher NYMEX gas prices to generate free cash flow and faces a significant deterioration in its credit profile until gas prices recover.

After all, the calendar strip price for Q1 2025 back on October 31st was $4.40/MMBtu, well above CRK's likely breakevens. As of January 19th, following the Golden Pass delay, the Q1 2025 strip is down to $3.68, pretty much in line with CRK's breakevens. Thus, even a modest shift in the LNG timetable can delay the expected turn in CRK's free cash flow position and result in larger draws on its credit facility.

Generally, I like to calculate a rough target price for a producer like CRK by estimating free cash flow over the next 5 years and then discounting those future cash flows to create a present value. That's the process I used to calculate target prices for Southwestern in my Seeking Alpha article in early December 2023 and for Range Resources ( RRC ) last July .

Given CRK's limited prospects for free cash flow until around the middle of 2025, and the potential credit issues I've outlined, it's tough to estimate a meaningful value target for CRK at this time using discounted cash flow techniques.

Here's a different way to think about the outlook:

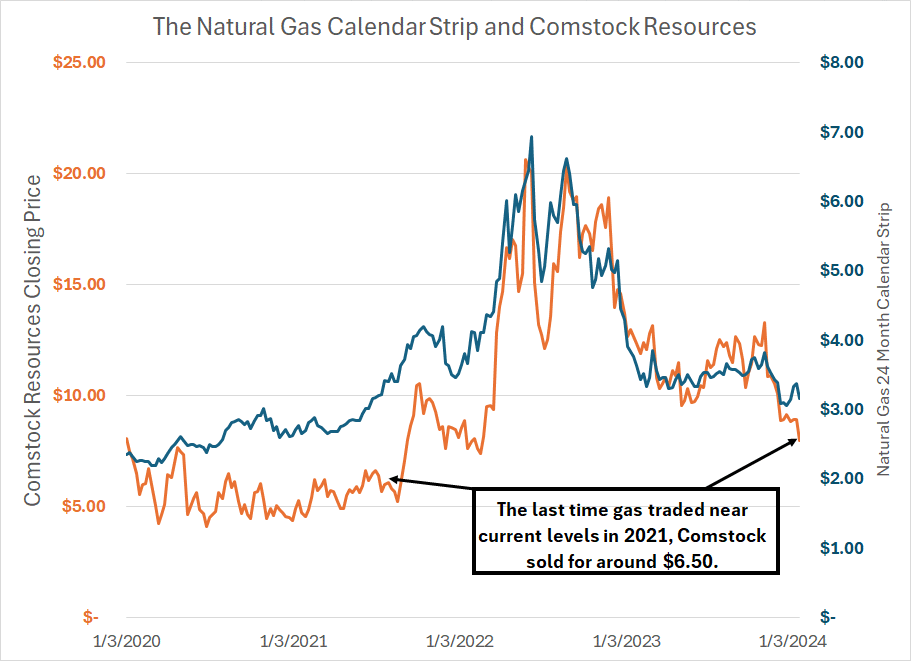

Chart of CRK and the 24-Month Natural Gas Calendar Strip (Bloomberg)

{kind=link}

The blue line on this chart represents the 24-month calendar NYMEX natural gas strip - the average price of NYMEX natural gas futures for delivery over the next 2 years. On Friday the 19th it stood at $3.16.

The last time gas traded at that price on this basis was June 25, 2021, when CRK sold for $6.50 compared to Friday's close at $7.99. Downside to the $6.50 region seems like a reasonable short-term target should gas prices remain near current levels and CRK continues to forecast significant 2024 free cash outspending on February 14th when it reports Q4 2023 earnings and releases its guidance for the year ahead.

I'd expect uncertainty about the company's free cash flow outlook and the potential for a negative borrowing base redetermination to continue weighing on the stock.

A decision to eliminate the dividend could also produce a negative reaction, as investors holding CRK for its 6%+ dividend yield exit the stock. A decision on the dividend could happen as soon as February's earnings call while the borrowing base is up for review in April - those are two powerful potential downside catalysts in the next three months alone.

Investors bullish on the longer-term prospects for natural gas prices, and LNG exports, will likely continue to favor producers like SWN and RRC I've profiled on Seeking Alpha , which enjoys lower breakeven costs and superior hedge coverage. These companies will be better able to spend broadly within cash flow over the next 4 to 5 quarters while they wait to position for higher average prices next year as LNG exports start in earnest.

Risks to my Outlook

The two most obvious risks to my bearish outlook are commodity prices and merger and acquisition activity.

On the commodity price side, a spike higher in natural gas prices, back to where they were trading in late October, would dramatically improve the company's near-term free cash flow estimates. This would eliminate some of the near-term concerns regarding the debt position, credit line redetermination and dividends.

While further cold snaps in the US could help improve sentiment, a significant spike in near-term futures prices to levels high enough to aid CRK looks unlikely.

After all, gas heating demand peaks in January and begins a sharp seasonal decline in the second half of March; as of the Energy Information Administration's latest report covering the week ended January 12th, US storage was still some 320 billion cubic feet above the 5-year seasonal average and 350 billion cubic feet above the level one year ago.

The US is running out of peak heating season weeks and it's tough to imagine a scenario where the weather is cold enough for long enough that the US eliminates that 320 bcf storage overhang by the end of gas withdrawal season in March.

Meanwhile, Chesapeake's recent offer to acquire Southwestern Energy in an all-stock deal has ignited interest in the Haynesville as a target for M&A. Southwestern and Chesapeake are both dual basin operators with acreage in the Haynesville and the Marcellus of Appalachia and, as I previewed in my SWN piece on Seeking Alpha , gaining acreage in Haynesville was a major driver of Chesapeake's interest in Southwestern.

However, it's worth noting that recent M&A deals in the energy industry have tended to be all-stock transactions offering only modest premiums for shareholders in the target firm.

CHK is offering 0.0867 shares of Chesapeake for every SWN share. On January 4, one week before the deal was announced and before a January 5th Wall Street Journal article reported a deal was imminent , Chesapeake closed at $76.96, so 0.0867 shares of CHK were worth $6.67 on that day. In the same session, SWN closed at $6.40, so the deal represented only a roughly 4.2% premium on that basis.

In an all-stock deal shareholders in the target company do enjoy longer-term upside via their stake in the new merged entity. However, there's been no immediate "pop" higher for recent targets of energy M&A.

On top of that, CRK's large net debt burden and exposure to the western Haynesville, outside the established core of the Haynesville shale field, also serve as formidable obstacles to any acquisition.

Thus, I see a deal to acquire CRK as unlikely at this time and any such deal would likely offer limited near-term upside for CRK shareholders.

Bottom line: Hefty cash flow outspend, a deteriorating credit outlook and the potential elimination of the dividend all loom as near-term risks. Sell Comstock Resources.

For further details see:

Comstock Resources: Serious Cash Flow, Debt And Dividend Headwinds Loom