CRK - Comstock Resources: The Race Is On

2023-12-21 04:45:54 ET

Summary

- Haynesville pure play E&P companies face challenges in 2024 due to falling natural gas prices, rising supply and stable demand.

- Comstock will see cash burn through 2024 as a result of lower natural gas prices and high infrastructure & drilling costs in the Western Haynesville.

- Production data shows high IP and decline rates in the Western Haynesville.

- Comstock stock is a medium-term play on rising natural gas prices.

It’s not easy being a Haynesville pure play E&P company these days. Despite the loss of rigs in 2023, natural gas production in the US keeps breaking records . In November of 2023, dry gas production hit a new all-time high of 105 Bcf/d, a rise of 3.3 Bcf/d from the 2022 average and up 3.1 Bcf/d since September 2023. The increased gas since September came from three major areas: Marcellas (up 1.5 Bcf/d), Permian (up 1.1 Bcf/d) and even the Anadarko region kicked in 0.6 Bcf/d. The latest boost came in part from E&P companies who delayed production to take advantage of the natural gas market’s contango structure (higher forward prices) – they are now back to drilling.

Demand, Forward Curve & The Shorts

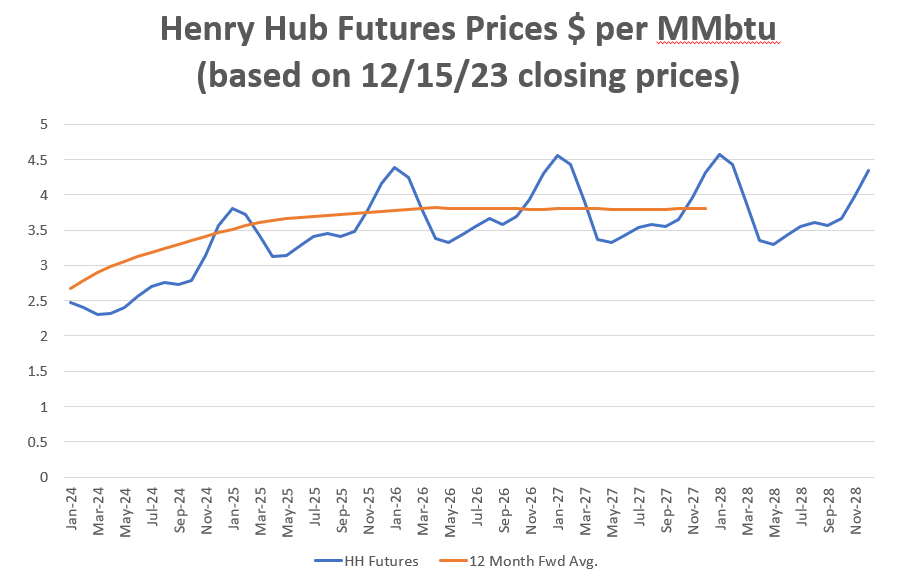

On the demand side of the equation, things aren’t looking so good. We’ve got a relatively mild start to the winter and Exxon announced the delay of the start of the Golden Pass LNG terminal from late 2024 to the first half of 2025. This was too much for the natural gas market to take and the leading edge of the forward curve bled out – moving all of 2024 below $3/MMbtu. HFIR Research, a natural gas commentator on Seeking Alpha, doesn’t see 2024 natural gas rising above the $3/MMbtu handle, and I agree with them, it’s looking that way. The following chart is telling the market to leave it in the ground and produce it in 18 months.

Henry Hub forward curve (Author with data from CME Group)

{kind=link}

Meanwhile, Matterhorn Express Pipeline (a new Permian pipeline) is scheduled to come online in Q4 2024 and displace as much as 2 Bcf/d of Haynesville gas. That pipeline gives the Permian license to grow their natural gas production and dump it on Houston’s doorstep. From the other direction, MVP (the long-awaited Appalachian pipeline) goes into service in Q1 2024, although it will take several years to debottleneck that new stream of 2 Bcf of supply into Transco and much of that supply will be soaked up by power generators. Most estimates have the near-term throughput at 0.7 Bcf/d.

Sensing blood, the shorts have piled in , using Comstock (CRK) as an inexpensive vehicle to trade natural gas. They have borrowed and sold a total of 22 million shares, up from 15 million in July. This is 24% of the available shares. It seems salvation is a new LNG terminal away, but even when those terminals begin to come online, there is a slow but steady ramp to full capacity. That could take months. In the meantime, 2024 is looking like a cash-burn write-off.

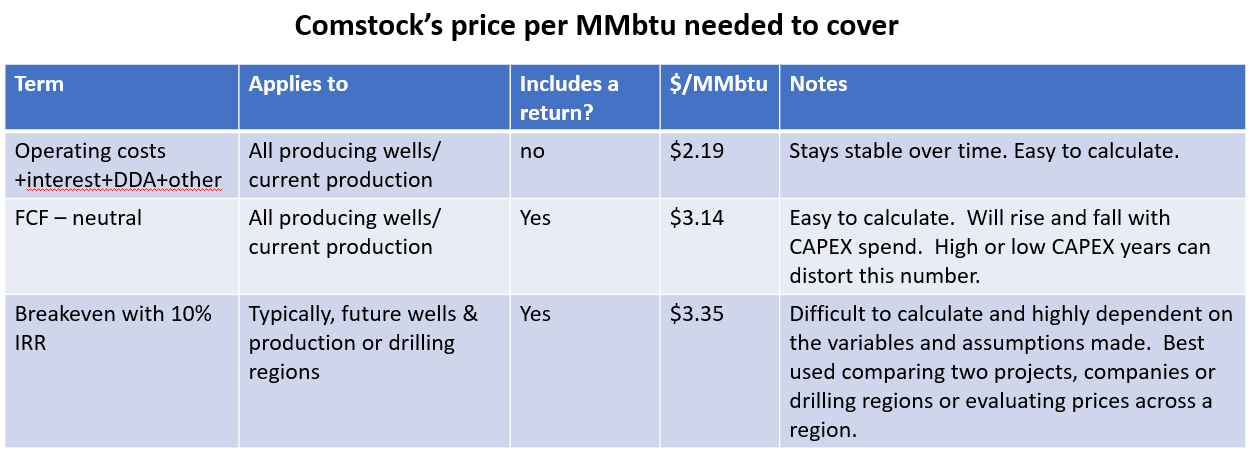

Cost of Producing Natural Gas

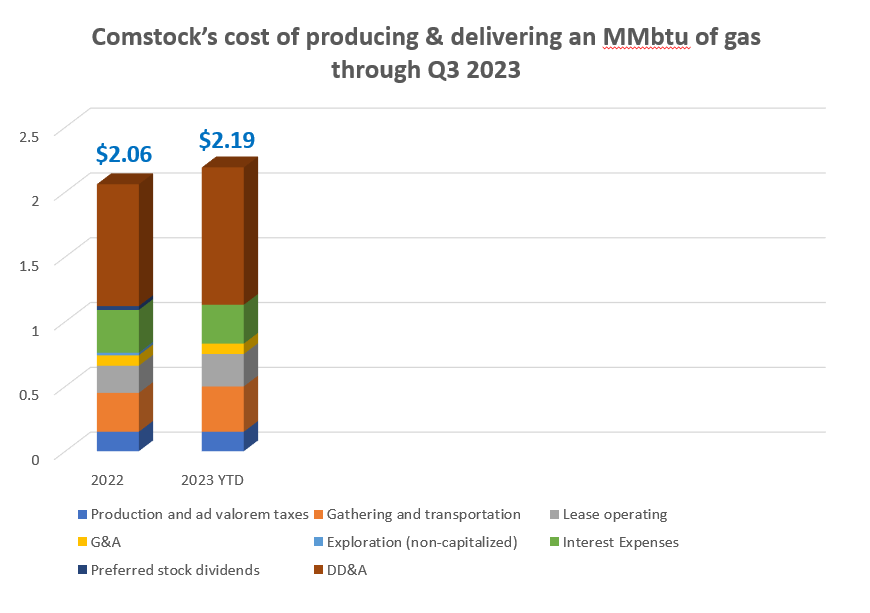

When we last looked at Comstock back in early August, the 2024 future gas curve was comfortably above the $3 level. Their all-in cost of delivering an MMbtu of gas to the market in the first half of 2023 was $2.17 versus a realized price of $2.49 plus another $0.27 for cash settlements on derivatives. If we add in Q3, their all-in cost rises a bit to $2.19 and their realized price is nearly flat at $2.46 plus another $0.21 for cash settlements on derivatives. We can see their margins are getting squeezed, but haven’t gone negative just yet.

Comstock's cost of production (Author with data from Comstock's quarterly report)

{kind=link}

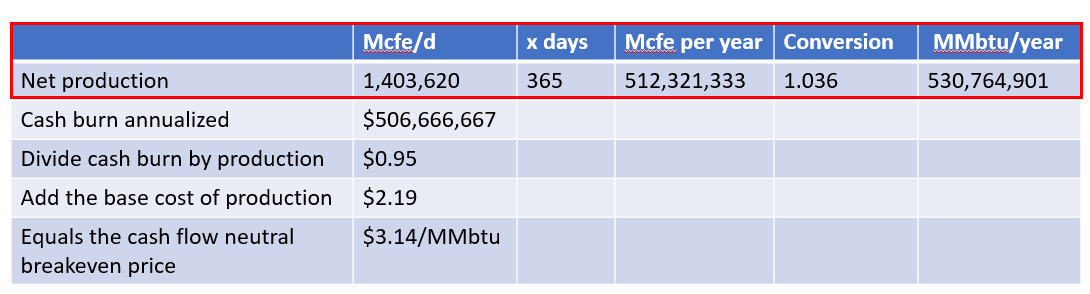

Despite the near-term weakness in natural gas prices, Comstock should see higher realized prices in Q4 because prices rose in October and November. They also hedged 18% of their production at $3/MMbtu in Q4 and 29% of their 2024 production at $3.55/MMbtu. Those hedges will serve them well given the weakness we’ve seen. To keep their production flat at 1.4 Bcfe/d and keep their investment in their massive Western Haynesville project moving forward through 9 months of 2023, they dug into their piggy bank to borrow $345MM against their bank credit facility and drew down their cash by $35MM. To stop the cash burn, they would need to eliminate the dividend and achieve a realized price that is $0.45/MMbtu higher.

Comstock's FCF breakeven price (Author with data from Comstock's SEC filings)

{kind=link}

Exploratory drilling and completion costs, predominately tied to their Western Haynesville project, rises to $179MM (through Q3) and infrastructure costs rose YoY as well. A significant amount of that new debt burden can be tied to investment in that region. Selling the prolific gas coming from this project is offsetting but not covering their cost to develop and support the acreage. It’s not FCF positive yet and it’s unclear when they will turn that corner.

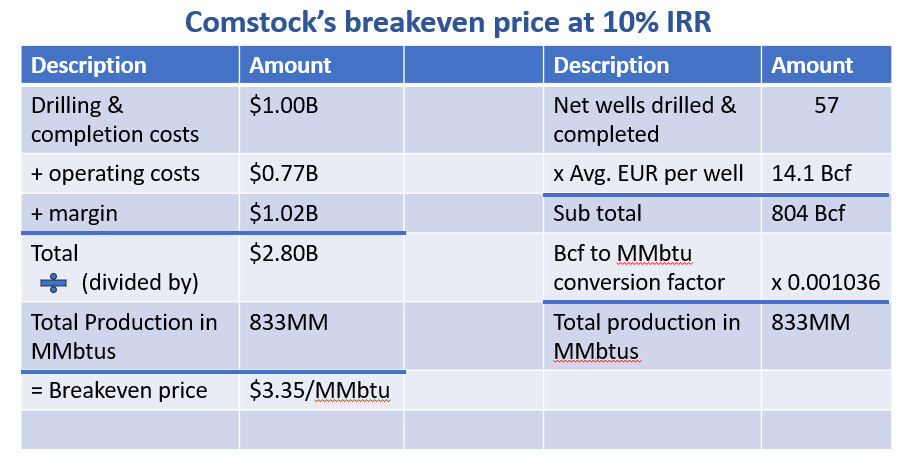

For every $278.5MM of cash burn (without a corresponding rise in production), I estimate that $1 is wiped off their equity value. Some relief comes from a partnership they formed with Quantum Capital Solutions to take on the capital burden (up to $300MM) of building out their gathering and treating system for the Western Haynesville project. Suspending the dividend would preserve $139MM per year, but, so far, they are reluctant to take that step. I estimate that using 7.5% debt from their new banking facility to drill new wells requires an estimated breakeven of $3.27/MMbtu at a 0% IRR (with a 5-year debt payback) versus a Henry Hub trailing 5-year annual spot price of $3.62/MMbtu.

The Term, "Breakeven"

In the comments section of the previous article, readers commented on the term “breakeven,” so it is worth reviewing. The term “breakeven” is typically used in conjunction with an IRR – internal rate of return. It is especially important to use an IRR because drilling and completing involves high initial capital expenditures followed by a long payback period. This is a complex calculation best left to a spreadsheet, but we can summarize the main points this way:

Comstock's breakeven price with 10% IRR (Author)

{kind=link}

EUR is the estimated ultimate recovery of the wells assuming an 8% terminal decline rate. Operating costs inflate 2% annually. The margin is derived by subtracting discounting future cash flows from non-discounted cash flows. This $1B margin is the time value of money when you invest $1B and it is returned over many years. Different assumptions affect the calculation. For example, if the terminal decline rate is 12%, the estimated average EUR per well is only 13.1 Bcf and that drives the breakeven price up to $3.62/MMbtu.

The calculation excludes the cost of interest expenses. If we add that back, the breakeven rises to $3.78/MMbtu. Also excluded are their exploratory drilling and completion expenses which would likewise skew this number to the high side. These types of breakeven prices are best used when comparing one drilling region to another or comparing one E&P company to another, where you can keep the variables stable across all examples and compare the relative value of one company or project to another.

We’ve thrown a lot of numbers around so let’s summarize:

Comstock cost to cover (Author)

{kind=link}

Jerry Jones Rose Colored Glasses

Next, let’s put on a pair of Jerry Jones rose colored glasses and peek into Comstock’s future. There are two major long-term bets with Comstock – one is outlasting the competition by maintaining an inventory that will last 20+ years. Based on all the available public and private data on drilling inventory and assuming no major technological advances or newly discovered resources in the region, the Eastern Haynesville region will reach a peak in next 4-6 years, maintain that peak for 6-8 year and then roll over. Depending on natural gas prices and the willingness of E&Ps to drill, that gives this basin between 10-14 years before we're going to need a major new source of gas.

We’ll dive into that topic in detail in a future article, but suffice it to say, E&P companies that preserve or grow their drillable inventory and outlast that Haynesville inventory exhaustion point stand to reap large rewards. Excluding their Western Haynesville region, Comstock currently has 1491 locations of drillable inventory with an average lateral length of 8,949 feet. At current drilling rates, this is enough to last 20+ years. That inventory includes some of the best drilling locations in the basin. They’ve also done an excellent job balancing their drilling program to prevent the premature exhaustion of their best drilling locations and to take advantage of their infrastructure in multiple areas.

Western Haynesville – New Drilling Data!

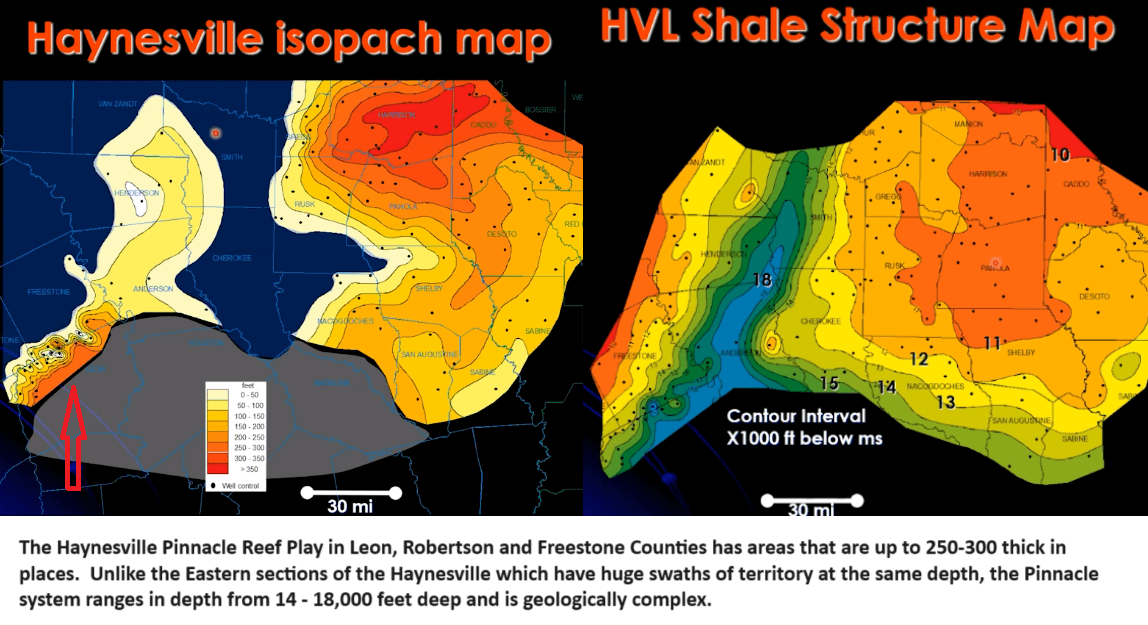

The second Comstock bet is developing a new core region that produces gas at a lower breakeven price and expands their drillable inventory. Let’s unpack the details of their new Western Haynesville project to see what we can learn. The Pinnacle Reef system is a continuation of the same prolific benches we see in the main Haynesville region, mainly the Bossier and Haynesville shale.

Haynesville Isopach & Structure Maps (Ursula Hammes AAPG presentation at Super Basins 2021 Virtual Conference)

{kind=link}

The productive Haynesville bench in that region is roughly 45 miles by 15 miles wide with thicknesses ranging from 50 to 300 feet but the subsurface gets deeper as you move southeast, so it’s unclear if all the acreage is usable. Based on permitted locations, Comstock appears to be targeting this region in 2024 (red arrow). Above that deep layer, lies the Bossier which extends into a larger area and is also productive. The Bossier has been their primary target in 2023.

History of the Play

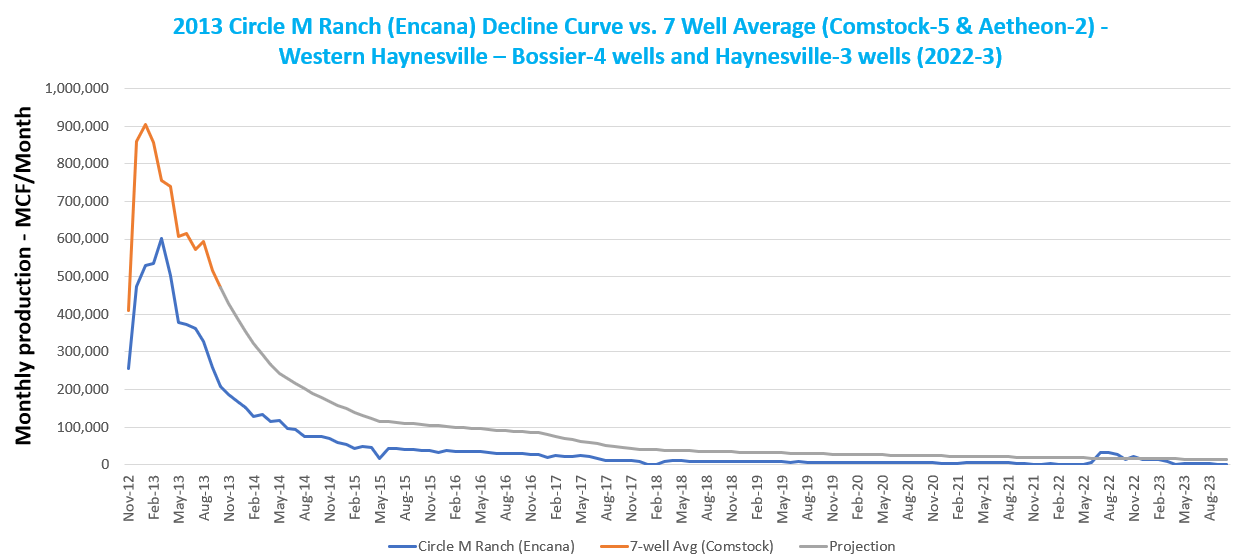

Back 2013, Encana owned 90,000 acres in Robertson and Leon counties and drilled the first well at 16000 feet into the Bossier play, creating a 4,866 foot lateral well (that was the prevailing length at the time) called Circle M Ranch that went on to eventually produce 8 Bcf of gas. It also had a high IP rate (22 MMcf/d), but the decline rate was murderous. Seventeen months after that well turned on, over 80% of the production was lost to decline. Essential 80% of the well’s EUR (6.2 Bcf) came out in the first two years.

The well was no doubt expensive to drill, and the economics never worked out. Admitting defeat, Encana sold their entire 90,000 acre position in 2014 to Covey Park (the predecessor to Comstock) for $530MM – a position Encana originally bought in stages for $2.9B from 2005 to 2007. Drilling for gas is never easy. Fortunately, the decline rates for Comstock (at least so far) are better (more on this topic below). Circle M Allocation 1H, the now infamous Comstock well, drilled right next to Circle M Ranch, and completed in April 2022, has already produced 13 Bcf of gas in 19 months, proving that infill drilling is possible and showing the power of modern completion techniques.

Comstock's Western Haynesville Position

I believe Comstock currently has between 150,000 and 175,000 net acres in the Western Haynesville primarily in Robertson and Leon counties, so they’ve grown the position since the Covey acquisition. In 2022, they acquired a 145-mile pipeline and natural gas treating plant and the undeveloped rights on approximately 68,000 net Haynesville and Bossier shale acres in East Texas for $35.6MM. In 2021, they acquired approximately 17,500 net acres of predominantly Haynesville shale acreage in East Texas, which also included interests in 37 producing wells for $34.7MM.

If we add these purchases to their existing 90,000 acres in the Western play, it brings us to an estimated 175,000 (140,000 net) acres. They have been actively acquiring additional property, having spent about $77MM in capital through 3 quarters. Because of the depth and heat at these drilling locations – drilling is expensive, north of $30K per well. Bottom hole temperatures range between 275 and 400 degrees F which is extremely hard on drilling equipment, especially the drill bits which tend to burn up. Drilling at these depths and temperatures also requires special rigs and drilling tools and thicker casings, etc.. Total vertical depths range from 16,000 to 18,000 feet which also increases the cost of drilling and adds challenges. Drilling the vertical sections takes an especially long time.

Comstock has improved their ability to drill at higher temperatures and over time, they’ve eliminated 20 drilling days per well. Once they switch to full pad drilling, it will continue to speed up the drilling process and lower the costs. They will turn 10 wells to sales in 2024 – 8 in the Haynesville play, and 2 will target Bossier, with laterals between 10,000 and 10,500 feet. So far, they have turned 9 wells to sales and of those, 7 are Bossier and 2 are Haynesville. They believe the production from the Haynesville will be more favorable, but of course, the drilling depths will be slightly deeper and probably more expensive to drill.

Q4 and Beyond

In the 4 th quarter, Cazey MS debuted at an IP of 34 MMcf/d in Robertson and Lanier CW came on at 35 MMcf/d in Leon. They will add a third rig next year and then a 4 th rig in 2025. They project 0.5 Bcf/d by mid-2025 with growth to 2 Bcf/d by 2028. Publicly available data from RRC shows that 6 of the 9 wells produced 151MMcf/d in October 2023. The two additional wells in Q4 and 10 additional wells in 2024, gives them a 2024 exit around 360 MMcf/d. Comstock will increase the pace of drilling in 2025 to meet their goals.

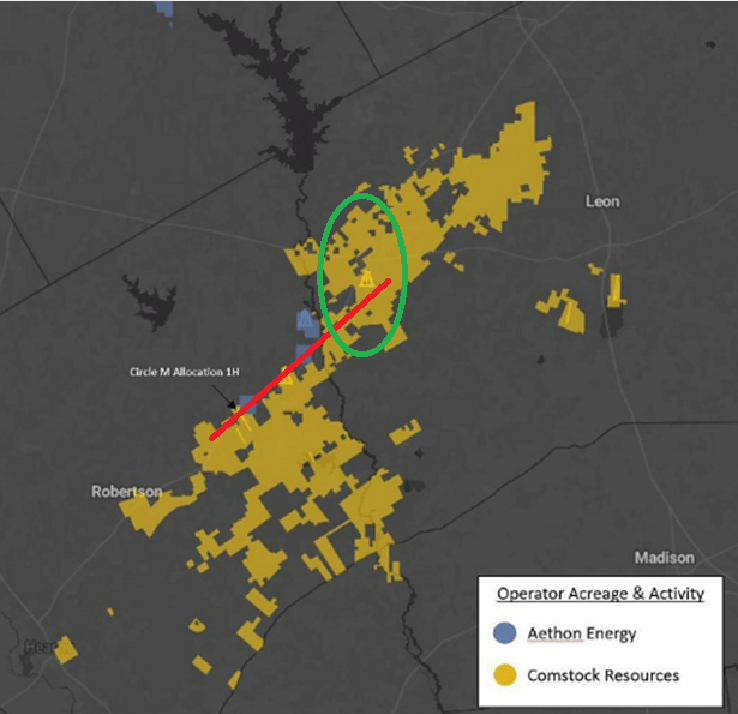

I found a total of 11 drilled wells in the RRC database targeting these deeper layers, including 2 from Aethon drilled in the Haynesville play. They appear to be drilling along a straight line (along US Highway 79) as shown by the red line in this acreage summary. Based on 8 registered permits, the 2024 Haynesville drilling program appears to be primarily focused on Leon county along US highway 79 within the green circle, although I see 2 permits pulled in Robertson (again, along the red line).

Comstock and Aethon's Western Haynesville Acreage Map (Author with image from Hart Energy)

{kind=link}

Risks

We’ve talked extensively about the risks of lower gas prices and cash burn. As mentioned, 2024 gas prices look like a write-off, but you never know what the weather will bring. Salvation comes with the 2025 buildout of new LNG export projects slated to come online then. The forward gas curve looks healthy in that 2025-28 range, and they can hedge into that to reduce risk. With the coming LNG export boom continuing, this is the perfect time to de-risk all that Western Haynesville acreage. If the world needs more gas, they can ramp up production. If not, they can dial back and take comfort knowing how many new drilling locations they’ve unlocked.

Decline curves in their Western Haynesville project will be something to watch. I compiled the available production data from 7 wells in the RRC database, including 2 wells from Aethon and 5 wells from Comstock, and aggregated them into an average to see how these wells are performing. Data shows these wells are declining at an average rate of 9% per month from the peak (orange line in the following chart). While the IP rates are impressive and decline rates will inevitably slow, this decline path is ferocious. We can plot this average against that Circle M Ranch well that Encana drilled back in 2013 to compare:

Western Haynesville Decline Curve (Author with data from RRC database)

{kind=link}

Compared to the 7 well average, the Circle M Ranch initially declined at an average rate of 11% per month, so the Comstock and Aethon wells have a 2% advantage in that respect. Assuming they maintain that advantage to some degree, we can project out the remaining production (gray line) and estimate an EUR value for the average of the 7 wells at 16.5 Bcf per well. That’s probably not good enough for $2.50 gas and wells that may cost on average $35MM to drill, but if they can bring down the drilling costs to $20MM per well (or less) or the decline curve improves, the play may come out on top. At the end of the day, predictable high IP rates coupled with high decline rates just means a quick payback. It means they can bring production on quickly to satisfy new demand. That’s a handy thing to own. If the inevitable price spike comes their way, they can quickly ramp.

Final Thoughts

Their Leon acreage looks reasonable, and their 2024 drilling in that region will provide valuable insight. They’ve also proven to some extent that they can drill wells with the normal spacing without stealing production from the adjacent well. It would be good to get another test of that theory by drilling another adjacent well. Except for the 2 Circle M wells, every other well is at least a mile away from the nearest well, although there are plans to drill them closer. I’d also like to see some drilling on their southeastern Robertson acreage to prove that it works in that direction. As we can see from geology, it gets deeper in that direction.

As far as positioning goes, Comstock is a decent bet on rising natural gas prices for those with a 3-year horizon. A good downside acquisition price is $6-8. They are just an LNG terminal and a short-squeeze away from blowing out to the mid-teens or higher. This will be an interesting one to watch. Will the decline curve settle out? Will Comstock drive down drilling costs to a manageable level? Wills the shorts let go of the bone? Let’s revisit this topic in 6 months to see how things are progressing. Until then, the race is on!

For further details see:

Comstock Resources: The Race Is On