CMTL - Comtech Telecommunications: Still A Lot To Prove

Summary

- The company has a lot of work to do to break out of its multi-year downward spiral.

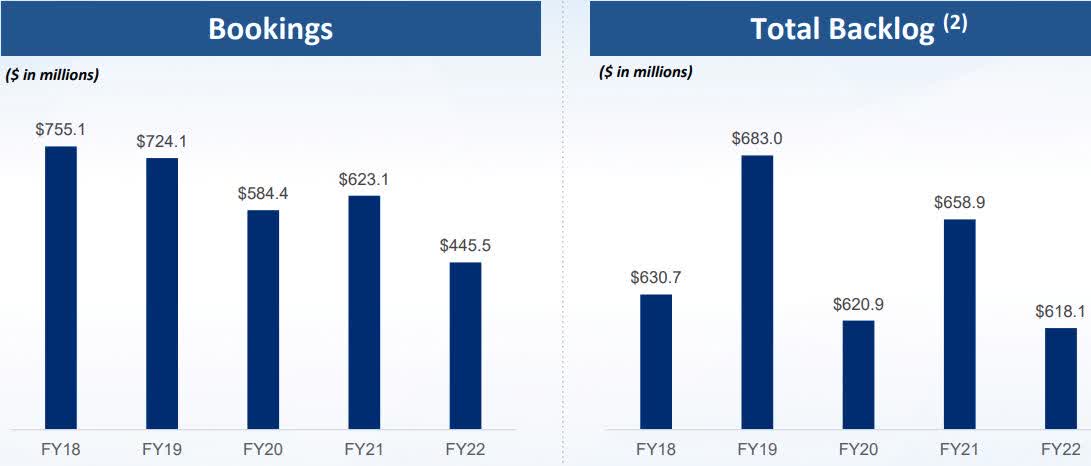

- Bookings since 2018 have plunged from $755 million to $455.5 million in 2022, while total backlog has been uneven, culminating in its lowest level of $618.1 million in 2022.

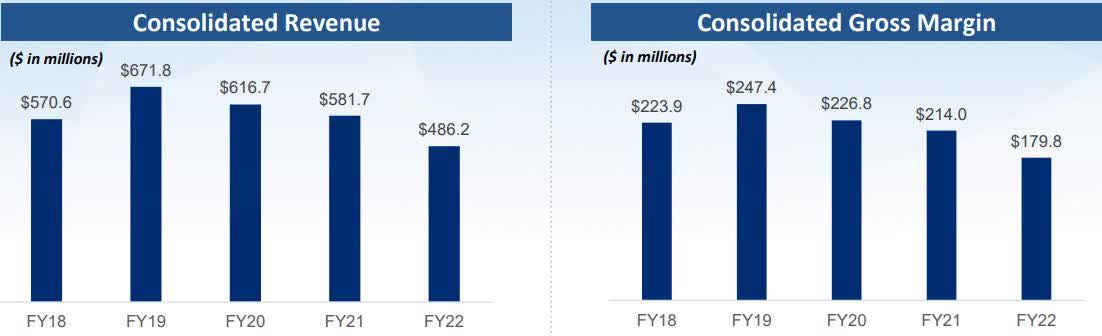

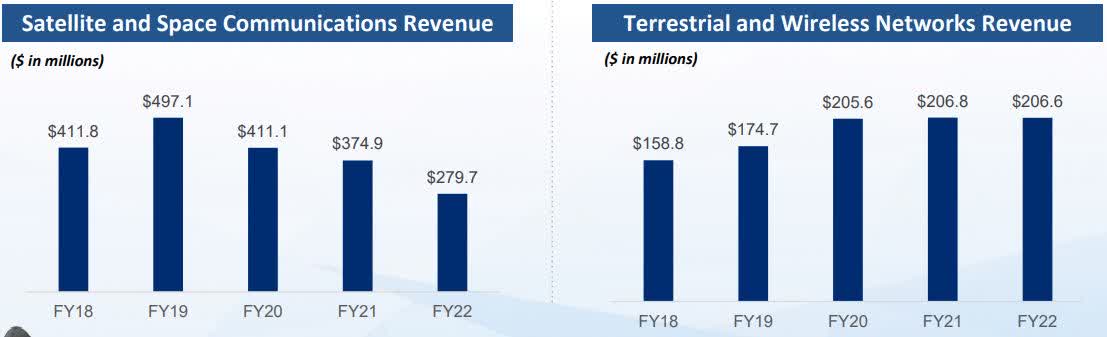

- Satellite and Space Communications revenue has been showing some strength recently, but it's still way down on a five-year historical basis.

- The company has recently enjoyed the best upward run in its share price during the last two years, but I think it's not likely to last.

Comtech Telecommunications Corp. ( CMTL ), from the way it has traded over the last couple of years, has been enjoying one of the longest upward moves in its share price during that time, climbing from a 52-week low of $8.42 on June 13, 2022, to approximately $14.13 on December 12, 2022, before pulling to a little under $12.00 per share and pressing against the $13.00 per share mark on January 11, 2023.

{kind=link}

What's important about this is the company had a very mixed earnings report, even as it continues to perform well below the levels it has been over the last five years.

To give some contrast, the company has been increasing revenue recently, from $116.8 million in the first fiscal quarter of 2022, to $!31.1 million in the first fiscal quarter of 2023. Net bookings during that same period climbed from $86 million in value to $181.2 million in the first fiscal quarter of 2023.

On the other hand, over the last several years, consolidated gross margin has dropped from 38.1 percent in the second quarter of fiscal 2022 to 35.7 percent in the first fiscal quarter of 2023. Consolidated adjusted EBITDA margin also fell quarter over quarter, from 10.0 percent in the fourth fiscal quarter of 2022 to 8.2 percent in the first fiscal quarter of 2023.

In this article, we'll look at its recent earnings numbers, some of the emerging trends, and why the company has a way to go before it returns to sustainable growth, and that will only happen if the company is able to execute on its strategy.

Some of the numbers

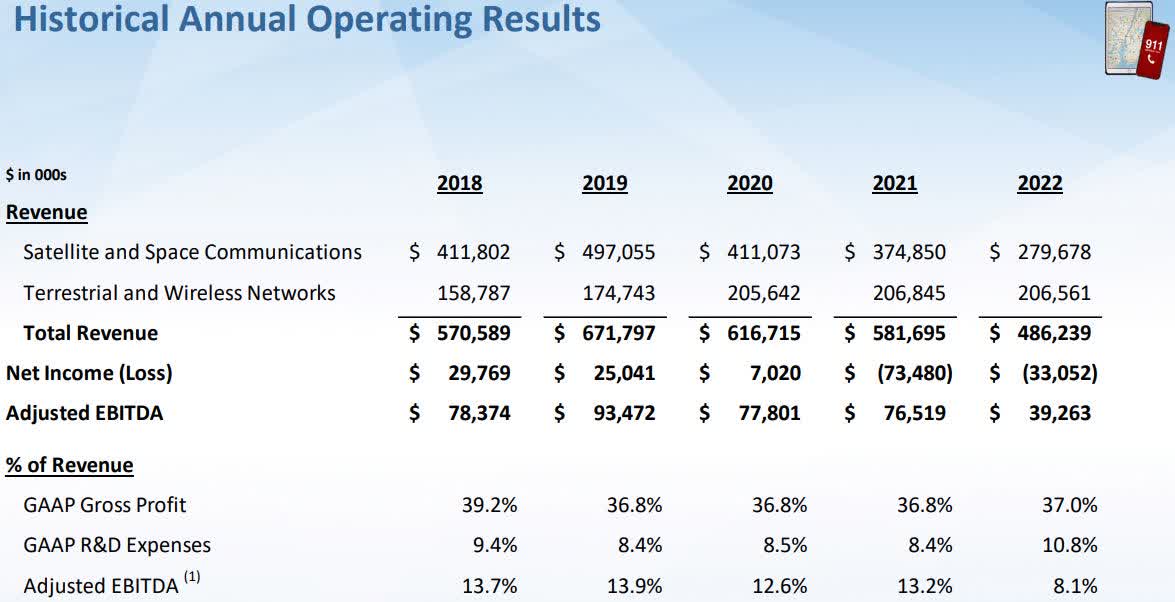

Revenue in the first fiscal quarter of 2023 was $131.1 million, compared to $116.8 million in the first fiscal quarter of 2022. Its Satellite and Space Communications segment accounted for $80.9 million in revenue, while its Terrestrial and Wireless Networks segment accounted for the remaining $50.3 million.

Expenses in the reporting period were $56.5 million, resulting in an operating loss of $(9.7) million, compared to expenses of $48.3 million in the first fiscal quarter of 2021, resulting in losses of $(6.5) million. Taking into account $9.09 million in CEO transition costs, expenses were down in the quarter, and all things being equal, show some improvement in the quarters ahead because of the one-off expense there.

{kind=link}

Adjusted EBITDA was $10.7 million or 8.2 percent of consolidated net sales, up from the $5.5 million in adjusted EBITDA or 4.7 percent of net sales year-over-year. Consolidated adjusted EBITDA margin dropped to 8.2 percent in the quarter, down from 10 percent in the prior quarter. On a year-over-year basis, it was up 3.5 percent from the 4.7 percent in adjusted gross margin in the first fiscal quarter of 2021.

Gross margin in the quarter was 35.7 percent, flat sequentially and year-over-year.

{kind=link}

Net loss in the quarter was $12.8 million, or $(0.46) per share, compared to a net loss of $(11.2) million, or $(0.43) per share in the first fiscal quarter of 2021.

Cash and cash equivalents at the end of the first fiscal quarter of 2023 were $21.5 million.

Concerning bookings and total backlog, the company has been dropping significantly in bookings over the several years, having $755.1 million in bookings in full-year 2018, and $445.5 million in bookings for full-year 2022. For total backlog, that has been uneven since 2018, moving in a range of $618.1 million in full-year 2022, representing the lowest total backlog since 2018.

{kind=link}

Breaking down the segments

Satellite and Space Communications

On an annual basis, revenue in Satellite and Space Communications has been steadily falling at a rapid pace, dropping from $497.1 million in revenue in full-year 2019, to $279.7 million in full-year 2022.

Quarterly revenue in the segment has been increasing modestly over the last year, climbing from $64.6 million in the first fiscal quarter of 2022, to $80.9 million in the first fiscal year of 2023.

During that time, net bookings have started to take off, jumping from $59.4 million in the first fiscal quarter of 2022 to $135.8 million in the first fiscal quarter of 2023.

Adjusted EBITDA in the segment has been steadily improving, from -2.0 percent in the first fiscal quarter of 2022 to adjusted EBITDA of 12.2 percent in the first fiscal quarter of 2023.

Terrestrial and Wireless Networks

On an annual basis, revenue in the Terrestrial and Wireless Networks has been trading flat over the last three years, with revenue of $205.6 million in full year 2020, $206.8 million in full year 2021, and $206.6 million in full year 2022.

That has also remained the case with quarterly revenue, which has been in a range of a little over $50 million to $53 million over the last five reporting periods.

Net bookings in the segment were $45.4 million in the first fiscal quarter of 2023, plunging from $83.1 million in the fourth fiscal quarter of 2022.

Adjusted EBITDA in the segment has been consistently dropping since the second fiscal quarter of 2022; from 23.2 percent in Q2 to 11.9 percent in the first fiscal quarter of 2023.

Management noted that there was a lot of backlog in this unit that are of a multi-year nature, so it'll take time to work through that. That downside will continue to impact adjusted EBITDA and margins because of the unfavorable deals that are below market pricing when taking into account inflation. For that reason, the company is attempted to reset some of the backlog, but the degree to which it has been successful is probably moderate, otherwise, it would have been mentioned in the earnings report.

{kind=link}

Conclusion

New CEO Ken Peterman touted the idea that the company is under new leadership, is a new organization, now has a common operational infrastructure, and a team that is now energized.

In the earnings report, he emphasized he has instructed his workers that they must embrace a sense of urgency, i.e., move with speed in response to a rapidly changing market and customer wants and needs.

To a degree, it's okay I think to think in terms of the company's recent past performance may not be indicative of the future if this new team can execute at various areas of the company to drive revenue and earnings up on a sustainable and consistent basis, something that hasn't been there over the last several years.

{kind=link}

On the other hand, they have still inherited a company that has been operating for many years, and while it's not too difficult to change things at the top with a new team and a relatively small number of people, it's very different to see if it's embraced by the workers under them and put into practice across the footprint of the company.

I think the reason for the boost in its share price by over 50 percent since October is from the hope new leadership will turn the company around, and bidding the share price up leading to its earnings call.

Based upon the visibility we have, I don't see how the share price of the stock will remain elevated. It's probably going to take a downturn sometime in the near future because of the lack of tailwinds to find support at a higher bottom, which would lead to a breakthrough past the $14.00 mark, which is the technical level it would need to surpass in order to gain more momentum.

I don't think that's going to happen in the near future and expect it to pull back and remain lower until the next couple of earnings reports provide some clarity on how the company is performing and what the future holds for it, within the parameters of a murky macroeconomic environment that has made it hard to confidently provide guidance beyond a quarter of two at most.

For further details see:

Comtech Telecommunications: Still A Lot To Prove