CPB - Conagra: Buy Alert For Dividend Defensive And Value Investors

2023-10-23 10:17:47 ET

Summary

- The non-commodity food processing industry has experienced a significant decline in stock prices this year, more than other industries.

- The industry's stock prices have been negatively impacted by increasing interest rates, but appeals to defensive investors in a recession.

- Conagra is the best value among its peers, with above average EPS growth, moderate leverage and a significantly higher dividend yield.

There is a big sale in the grocery aisle.

As a deep value investor, normally I wouldn't look twice at a company like Conagra (CAG). But stock prices of the non-commodity food processing industry have dropped over 23% year to date, more than almost every other industry. Non-commodity means companies not heavily exposed to commodity prices like Tyson (TSN), Pilgrim's Pride (PPC), Cal-Maine (CALM) and Lamb Weston (LW) are. Those are excluded. In this article this industry will be analyzed. Then reasons why I am picking Conagra as the best value among them are provided.

Food Processing Industry

Conagra and its peers stock price results year-to-date are shown below.

Yahoo Finance and Value Line

The industry's results were enhanced in 2020 by hoarding due to the lockdowns and then by massive stimulus in 2021 and 2022. More recently inflation and reversion to the mean have become major headwinds, leading to stock price declines. Food inflation has resulted in less industry volume, though that has been offset by price increases. The recent stock drops were for the most part not preceded by a stock runup. The decline wasn't a reversion to the mean, just a drop.

This is a slow growth mature industry. Almost all revenue growth since 2020 has been from inflation or to a lesser degree, small acquisitions.

Once you remove the commodity players, the industry is very stable. These companies have very diversified portfolios of brands and are all national in scope. They historically have had significantly higher PE ratios than the commodity players due to less volatility in earnings. They historically have paid above average dividends which usually grow annually.

The stock prices for this industry have been hurt by increasing interest rates. While this hasn't impacted earnings much yet, it has seen income investors move to alternatives such as bonds or higher yielding stocks. The average stock has dropped over 23% year to date. Interestingly, this is a bigger decline than utilities and REITs, two other defensive higher income sectors dividend investors are attracted to. A week ago I did a detailed review of the REIT industry Sorting Through The REIT Wreckage: Public Storage, Healthcare Realty And 32 Others .

Peer Group Comparison

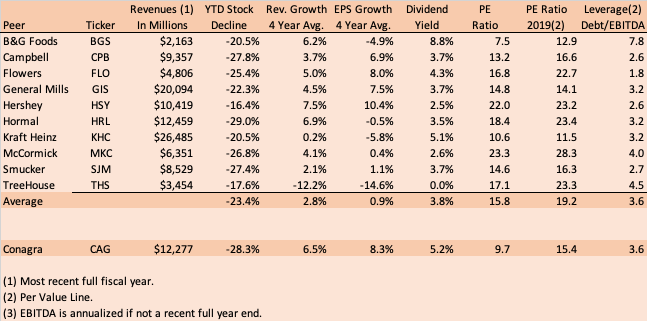

I compared the non-commodity food processors with annual revenues over $2 billion and with revenues mostly in the U.S. to determine which if any were the best buy. I excluded two, Kellanova ( K ) and Post ( POST ) due to recent large spinoffs making 4 year averages and stock decline percentages not applicable. The industry was compared for revenue and EPS growth, dividend yield, PE ratio, and leverage. The PE ratio is actually a better valuation measure for this group than EV/EBITDA. This is because capex and depreciation tend to be quite similar and offset each other. While EBITDA is not a good measure for valuation, it still works well in determining leverage which is shown in the last column.

Value Line, Yahoo Finance and SEC filings

{kind=link}

Two PE ratios were shown including one from 2019 (as shown in Value Line), the last full year before Covid. The comparison to 2019 shows how the industry PE ratio has dropped significantly, with most of that drop in 2023. This drop roughly corresponds to interest rate increases with a 6 to 9 month lag. This indicates the drop may reverse when interest rates come back down.

Conagra had one of the highest stock price drops among its peers. This is despite having well above average revenue and EPS growth. It also has the second highest dividend yield in the group. The only one higher is from B&G Foods ( BGS ) which is the weakest financially in the group. In fact, B&G is getting scary with high leverage and declining earnings. Conagra has dropped to the point it also has the lowest PE ratio other than B&G. The only negative peer-wise is Conagra's leverage at 3.6x debt to EBITDA. This ratio is not high, but higher than management would like. It actually matches the peer average, though that average is distorted by B&G. Their priority is to reduce the leverage ratio. Based on the factors reviewed, Conagra appears to have the best valuation among its peers.

Looking briefly at some of the others, Treehouse ( THS ) has also struggled financially and has divested a number of segments in recent years to reduce leverage. The result has been declining sales and EPS. It may not be done shrinking. Kraft Heinz ( KHC ) was a similar story to a much lesser degree. They leveraged up in a huge merger about 8 years ago and have been reducing leverage and costs ever since. Kraft Heinz has now reached a point where leverage is moderate and they can go back on offense. The yield at 5.1% is the next highest after Conagra and it may be worth a look. Some like Hershey ( HSY ) and McCormick ( MKC ) have high PE ratios, more than double Conagra. Hershey's is justified by solid growth and low leverage but it also has a low dividend yield. McCormick's PE ratio does not appear justified due to high leverage and low growth. General Mills ( GIS ) and Campbell ( CPB ) both have average leverage and dividends and above average recent growth. General Mills has a much better growth history than Campbell. They are both down enough to consider.

Conagra Background

Conagra has had a long history of little sales growth but steady earnings growth. Per Value Line, revenues per share are currently almost exactly the same as 15 years ago. Earnings in that time have more than doubled, at a 4.1% annual rate. The current CEO came in 2015. Conagra then divested a number of businesses over the next 2 years, reducing sales by almost half. In fiscal 2019, it turned around with a $10.9 billion acquisition of Pinnacle Brands, funded mostly with debt. It acquired the following brands among others; Birds Eye, Duncan Hines, Earth Balance, Vlasic, Glutino, Udi's, Wish-Bone and EVOL. The result was long term debt increased to $10.6 billion from $3.2 billion one year earlier. Revenues returned to pre 2015 levels. The company has since focused on reducing the long term debt. It was down to $7.1 billion as of May 31, 2023. Other major brands owned, but not acquired from Pinnacle include; Hunts, Healthy Choice, Slim Jim, Marie Callender's, Orville Redenbacher, Swiss Miss, Banquet, Parkay and Mrs. Pauls.

The financial results shown below are for the 6 fiscal years ended May 31, 2023.

Value Line

As shown above, revenues jumped from fiscal 2018 to fiscal 2020 due to the merger. Long-term debt also jumped in 2019 resulting in a lower net profit margin. The net profit margin has since returned to slightly above average historical levels.

In the first quarter of fiscal 2024 (ended 8/31/23) revenues totaled $2.90 billion, flat to the prior year quarter. Net income was $0.67 versus a $0.16 loss in the prior year quarter which was impacted by a goodwill write-off. It was about flat when annualized to fiscal 2023 results. Unit volume declined by 6.3% but was offset by price increases. Management presented the following chart in its earnings slides showing unit volume declines are actually an industry trend.

Conagra last quarter slide presentation

Management expects organic revenue declines to end in the second half of fiscal 2024. The analysts spent a lot of time on the conference call questioning management's rationale for this. They answered with favorable comps, more investment and more marketing. There is also momentum in two of their largest businesses, frozen foods and snacks.

Management attributes the volume decline to temporary factors primarily tied to inflation. Consumers are buying less due to price increases. They are also ordering less single serve SKUs. Profitability-wise, this is not currently a negative as margins went up as volume went down. Prices were raised above cost inflation and consumers pushed back by buying less. I believe management is probably right about the unit drop being temporary, though it may take longer than they think if there is a recession. The industry revenue surge in 2022 and 2021 was also temporary. It was also across the board in other industries due to stimulus and inflation. It is reasonable to see a pullback or reversion to the mean in volume.

In the most recent conference call, management guided for $2.70 to $2.75 adjusted earnings this fiscal year (ends May 31, 2024) on 1% organic revenue growth. This was unchanged from prior guidance.

Catalysts and Strengths

I believe Conagra is a good pick here for the following reasons.

1. Recession protection - The food manufacturing and distribution industries have historically held up very well during recessions. Food is much less a discretionary item than most other things. Also, when the stock market declines, investors usually move money to safer stocks. Reasons 4-7 below detail how Conagra is a safer stock. Conagra has a beta of 0.60 (per Yahoo Finance) which indicates its price moves much less than the market as a whole.

2. Valuation - After its big stock drop, Conagra has a very low PE ratio at under 10. This ratio is well below both historical levels and peers as shown in the preceding section. Conagra's PE ratio ranged from 15-25 during 2014 to 2019 , the 6 years just before the pandemic. It averaged 13-15 in fiscal 2021 to 2023. In my opinion, valuation is the best reason to own the stock.

3. Large dividend - The dividend's 5.2% yield is well above the peer average and comfortably covered. This indicates increases are likely. The payout was only 47% of net income in the fiscal year just ended on May 31, 2023. That is a historically normal level for them. It has been increased each of the last 3 years and was just increased another 6% last quarter.

4. Diverse portfolio - Conagra has one of the largest portfolios of brands in the business. Most are sold at the national level and about 9% of sales are international. It has a history of quickly following trends so while some older brands fade, others are growing.

5. Limited commodity exposure - Some food processors such a Tyson, Pilgrims Pride, and Cal-Maine have stock prices that can fluctuate wildly with changes in commodity prices. This has not happened with Conagra.

6. Deleveraging - The interest bearing debt to EBITDA ratio is currently 3.6x. This is slightly above peers. Management's first priority is to lower this number. They expect to be down to 3.4x this fiscal year. That will help mitigate the impact of maturing low cost debt in a high interest rate environment. It will also make Conagra a defensive haven for investors if we have a recession in 2024. Conagra has had no material acquisitions in the past 3 years. The focus is on deleveraging and dividend growth.

7. Stability - Revenues and earnings per segment and overall tend to vary little from year to year. In fact, Conagra and some of its peers, are some of the least volatile companies in the world. Investors traditionally have given companies with low volatility in earnings a higher valuation.

8. Frozen foods - Frozen foods are one of the faster growing segments in food sales. Conagra claims the industry CAGR is over 4% per year. While that is slow compared to other industries, it exceeds the industry average. Frozen foods are their largest category at 42% of sales in the most recent fiscal year. Sales grew 8% over the past 2 years.

9. Acquisition potential - Conagra's stable of brands is certainly worth well over 9.7x earnings to an acquirer. The industry average PE ratio is almost always much higher. Insiders own less than 1% of the stock, and the major holders appear to be mutual funds or ETFs. That indicates no vested interests to block a takeover.

Concerns

As with all stocks I write about, I have concerns. These are listed below.

1. Debt maturities - There are $2.5 billion of loans maturing by end of 2025, $1 billion in 2024 and $1.5 billion in 2025. Refinancing these in a high interest rate environment will increase the average interest rate on their loans. This should be partially mitigated by management's deleveraging strategy. They will likely payoff some with cash which should offset some of the rate increase. The company also has a $2 billion unused line of credit it can use to temporarily refinance debt so they don't have to lock in higher rates for years. Interest expense was $409 million in the last fiscal year. Management expects $450 million this fiscal year.

2. Concentration - Walmart is Conagra's largest customer and accounted for 28% of sales in the last fiscal year. That is a concentration to one customer, though the strongest player in the food retailing industry.

3. Slow revenue growth - While things have picked up some in recent years, Conagra has a long history of below average growth for revenues. There appears to be no plan to get beyond lower single digit organic revenue growth. Growth in the last 4 years has been above this average, primarily due to inflation. They should reach their leverage goals within a year or two. When that happens, growth should be enhanced again by acquisitions. That's how their peers primarily do it.

4. Consumers are pulling back - Management has noticed a number of trends showing consumers pulling back. They are buying less discretionary foods, using leftovers more, reducing household inventories, and doing more meals for many and less for one. These trends are moderate at this point. Most of Conagra's foods are not what I would call discretionary or higher cost.

5. Margin reversion - The adjusted operating margin increased 297 basis point (3.0%) in the most recent quarter from one year ago. Most of this increase was due to raising prices. There is consumer pushback on higher prices industrywide.

Valuation

Let's return to the chart shown earlier comparing Conagra to its peers. The peer median PE ratio is 15.8 versus 9.7 for Conagra. Conagra has slightly more leverage but a better EPS growth history. My sense is the benefits from their big fiscal 2019 merger with Pinnacle drove a lot of that growth and should be fading. This puts Conagra at slightly inferior to peers. But you also need to factor in their well above average and well covered dividend. Conagra historically traded at a PE ratio of 15-25. The 25 was on an off year so 15-20 is a better number. I would expect them to return to at least a PE ratio of 15 as their prospects are no worse than they were historically. The analysts expect earnings this fiscal year of $2.70, which is in line with management's guidance. At a PE ratio of 15, that indicates a price of $40.50. This is where the stock traded last January, so it isn't a stretch. It is 50% above the most recent closing price of $26.99.

Take Away

The whole food processing industry has been hit hard this year, harder than other defensives such as utilities. Yet this is one of the more defensive industries out there in a recession. I believe this drop was primarily due to higher interest rates, creating alternatives for dividend investors. This is corroborated by large (though smaller) drops in utility and REIT stocks. It also appears caused by a recent drop in unit volume which I view as temporary. If we do have a recession in 2024, interest rates will likely drop relatively quickly and investors will look for safe havens. Both would benefit Conagra.

I recommend a long position in Conagra, with a one year price target of $40.50. For dividend investors, this is a great opportunity to enter a position in a solid high and growing dividend company at a historically low price. It also appeals to defensive investors concerned about a recession and value investors.

Consider also a position in Kraft Heinz as the deleveraging appears over there and the last few quarters have seen good earnings and revenue growth. There is also a high dividend. General Mills is another to consider.

For further details see:

Conagra: Buy Alert For Dividend, Defensive And Value Investors