CNXC - Concentrix: M&A Provides Upside To Valuation

2023-12-08 17:38:02 ET

Summary

- Concentrix provides customer experience services globally, with the recent acquisition of Webhelp providing a better footprint especially in EMEA.

- The company has had significant acquisitions even prior to Webhelp, bolstering Concentrix's growth.

- The current valuation doesn't seem to fully price Concentrix's earnings potential, providing high upside to investors.

Concentrix ( CNXC ) provides CX services globally. The company’s services include customer experience solutions such as process automation, front- and back-office automation, and analytics, servicing clients in a large number of industries. Concentrix has completed two significant acquisitions within the past two years, creating a very large entity in the CX space.

After Concentrix was separated from Synnex in late 2020 due to Synnex’ and Concentrix’s differing customer requirements and markets, as told in Synnex’s presentation about the spin-off. Since the spin-off, Concentrix’s share value has dropped by 29% from the initial trading price:

{kind=link}

Financials

Concentrix has been able to grow its revenues well – the revenues have gone from $1990 million in FY2017 to trailing revenues of $6525 million at the time of writing, representing a CAGR of 26.0%:

{kind=link}

The revenue growth has largely been due to Concentrix’s history of acquisitions. Particularly, the historical growth rate has been affected by a large cash acquisition worth almost $1.1 billion, made in FY2019. Besides the FY2019 acquisition, growth has been achieved organically as well as through small acquisitions, with two very large acquisitions starting to effect Concentrix’s growth for the future – I believe that Concentrix has been able, and will continue to organically grow revenues, albeit with a very modest rate.

Along with the revenue growth, Concentrix has achieved a good amount of operating leverage – the company’s EBIT margin has gone from 5.8% in FY2017 to a trailing figure of 10.8% as of Q3/FY2023 in mostly stable increases. As Concentrix’s scale of operations has increased through acquisitions, the company has been able to drive down SG&A as a percentage of revenues from 28.6% in FY2017 to 22.7% with trailing figures as of Q3/FY2023. The company has completed acquisitions even more aggressively in the past couple of years, making the future financial performance intriguing.

Recent Acquisitions Bolster Growth

Concentrix completed an acquisition of PK in late 2022 for a consideration of around $1.6 billion, adding an estimated $530 million in revenues and $85 million in adjusted EBITDA to Concentrix’s financials. The acquisition seemed quite expensive at first glance – the acquisition price implies an EV/EBITDA of 18.8. From the company’s press release, though, the acquisition seems to have been made mainly with technological additions in mind – Concentrix mentions AI and intelligent automation as PK’s capabilities. Although expensive, the acquisition seems to improve Concentrix’s offering’s competitiveness, making the acquisition more valuable than just its financials.

More notably, Concentrix announced the acquisition of Webhelp in March of 2023 to increase Concentrix’s footprint internationally, especially in Europe. The acquisition has a transaction value of $4.8 billion, consisting of Webhelp’s debts, a share issue for Webhelp’s shareholders, and a cash & note payables of 1.2 billion euros – as the acquisition has such a large consideration compared to Concentrix’s value, the transaction is depicted as a combination. The Webhelp acquisition was made with a significantly better valuation than the PK acquisition – Webhelp is expected to add $3.0 billion in revenues and $500 million in adjusted EBITDA, implying an EV/EBITDA of 9.6. In addition, the merged operations are estimated to have $120 million in possible synergies, to be achieved by year three. The transaction was finalized in September.

Valuation

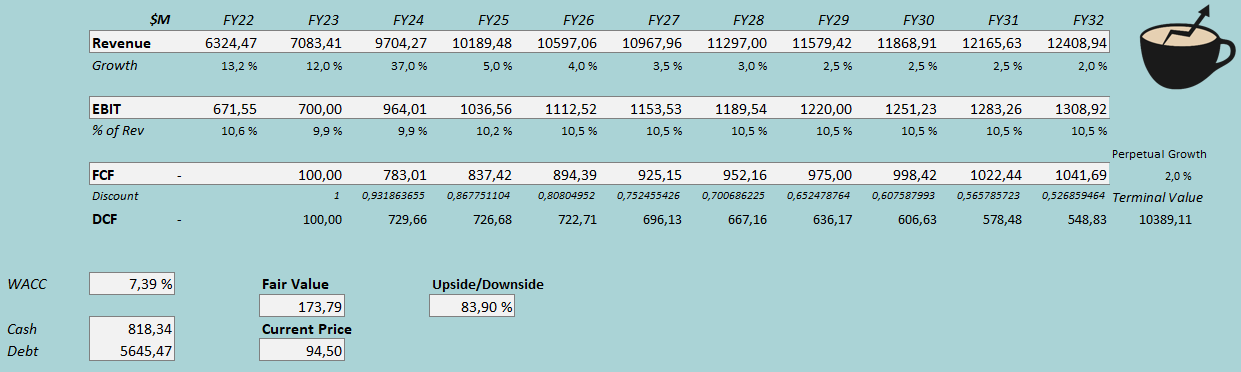

Concentrix’s stock seems very cheap, as the company has a forward P/E multiple of only 8.6 at the time of writing. To demonstrate the cheap valuation better, I constructed a discounted cash flow model in my usual manner. In the model, I factor in Concentrix’s acquisition of Webhelp into debt figures, cash reserves, outstanding shares, as well as the financials.

After the Concentrix starts to effect revenues after the deal was closed in September, I estimate revenues to grow significantly in Q4 and FY2024, with a FY2023 growth of 12% and a FY2024 growth of 37%. After FY2024, I estimate a very slight organic growth to continue with an estimate of 5% for FY2025, slowing down into a perpetual rate of 2%. Altogether, the period from FY2024 to FY2032 represents an organic CAGR of 3.1%. For margins, I estimate some scaling as Concentrix and Webhelp start to realize synergies – for FY2024, I estimate an EBIT margin of 9.9%, that scales into a margin of 10.5%, achieved in FY2026. Because the company has a significant amount of amortization from past acquisitions, Concentrix’s cash flow conversion from EBIT seems to be quite good.

With the mentioned estimates along with a cost of capital of 7.39%, the DCF model estimates Concentrix’s fair value at $173.79, around 84% above the stock price at the time of writing. The DCF model suggests a very good amount of upside for the stock with quite modest organic earnings growth – I believe that the most significant downside to the DCF model would be through a higher cost of capital.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

For Concentrix’s interest rate, I use the company’s interest rate that the company issued their most recent senior notes at, with the weighed average interest rate of the notes being 6.68%. Because of the company’s recent acquisitions, Concentrix seems to leverage quite a high amount of debt; I believe that a long-term debt-to-equity ratio estimate of 40% is reasonable.

The risk-free rate on the cost of equity side is the United States’ 10-year bond yield of 4.18% , which I believe is the most representative figure for the purpose. The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States made in July. Yahoo Finance estimates Concentrix’s beta at a figure of 0.67 . Finally, I add a small liquidity premium of 0.2%, crafting a cost of equity of 8.34% and a WACC of 7.39%.

A Note on the WACC

The used WACC of 7.39% is low compared to most companies, mostly due to Concentrix’s high amount of debt and a quite low beta. The low beta of 0.67 could be due to change in coming years, raising the cost of capital and lowering the stock’s fair value estimate. As Concentrix has issued debt to finance acquisitions, shareholders’ returns have higher leverage. The theoretical beta of Webhelp is unknown.

Still, Concentrix has proven a stable earnings level despite macroeconomic worries in recent times – I believe that the low beta is estimated for a reason. I don’t see a reason yet to raise the beta estimate, although I believe it’s a noteworthy possibility. For example, with a beta of 1.00, the stock would have an upside of 30% as the debt leverages the equity’s worth significantly. With a higher beta, Concentrix’s value still seems to have a good amount of upside left; I don’t think a higher beta would deteriorate the bullish thesis around valuation.

Takeaway

The investment case for Concentrix has many variables, as the acquisitions of PK and Webhelp are integrated into the company. It seems that Concentrix’s valuation doesn’t take Webhelp’s and Concentrix’s synergies for granted, as I estimate the valuation to be off by a huge margin, providing investors with high potential upside. At the moment, the stock’s risk-to-reward seems very favorable, constituting a buy rating.

For further details see:

Concentrix: M&A Provides Upside To Valuation