CNCE - Concert Pharmaceuticals: Negative Spread But Interesting CVR

Summary

- Concert Pharmaceuticals, Inc. is a biotech buyout trading at a negative spread but with an interesting CVR attached.

- The CVR is based on two sales milestones.

- The 1st milestone appears quite achievable.

- The 2nd milestone can be considered a "free" option.

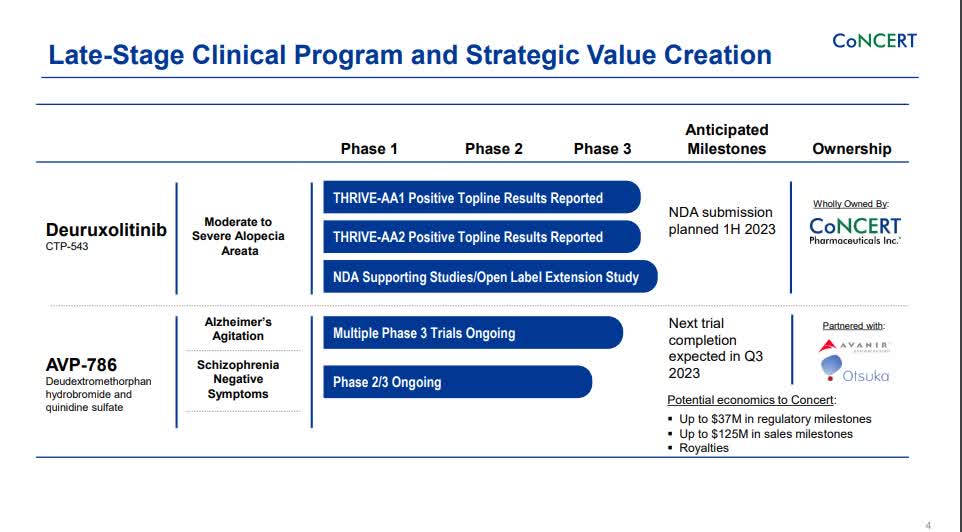

Concert Pharmaceuticals, Inc. ( CNCE ) is a $400 million market-cap biotech with one primary asset in deuterium. Sun Pharma is acquiring the company. Sun is the world's fourth-largest specialty generic pharmaceutical company and India's largest pharmaceutical company. Concert stockholders get $8 in cash and a contingent value right. The market places considerable value on the contingent value, as the stock currently trades at $8.35. The maximum payout under the CVR is $3.50 per share. The deal is structured as a tender (which tend to close much faster) and should close in Q1 2023. Most of the value can be ascribed to deuruxolitinib:

{kind=link}

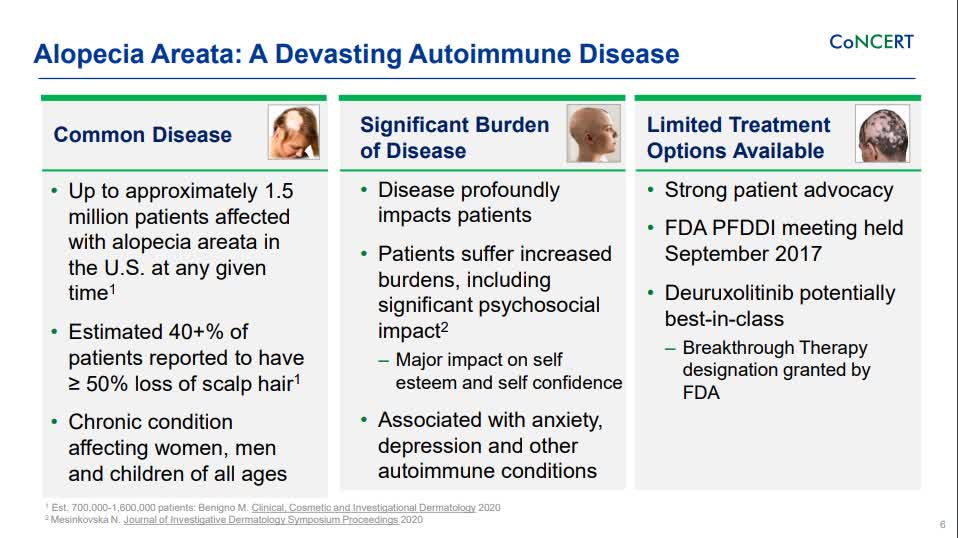

Deuruxolitinib is an oral inhibitor of Janus kinases JAK1 and JAK2 for treating Alopecia Areata. Alopecia Areata is an autoimmune dermatological disease. It results in loss of hair on the scalp and the body because the immune system attacks the patient's own hair follicles.

Concert has completed the evaluation of the efficacy and safety of deuruxolitinib in adult patients with moderate to severe Alopecia Areata in its THRIVE-AA Phase 3 clinical program, and two open-label, long-term extension studies are ongoing in North America and Europe. Concert is preparing to submit deuruxolitinib to get marketing approval in the U.S. Sun plans to continue on that path.

The milestones of the CVR look like this (emphasis mine):

((I)) $1.00 per share of common stock, payable the first time that in any fiscal year between the time of the first commercial sale of deuruxolitinib in the U.S. and March 31, 2027 , net sales of deuruxolitinib is equal to or exceeds $100 million , and ((II)) an additional $2.50 per share of common stock, payable the first time that in any period of four consecutive fiscal quarters between the time of the first commercial sale of deuruxolitinib in the U.S. and December 31, 2029, net sales of deuruxolitinib is equal to or exceeds $500 million .

First of all, there is a time component to these milestones (things need to happen before 2027 and 2029). I do get the impression the companies are ready to go get marketing approval from the most recent earnings call :

Within Concert, we've had a core team in place for some time to prepare our NDA filing, which we plan to submit in the first half of 2023. The data from our large Phase 3 trials forms the basis of our NDA application. However, there are several supporting studies and of course, CMC work that we have conducted or are wrapping up to support the filing. We have a well-defined plan going forward, and I have every confidence that our team will continue to consistently execute to our timelines as they have throughout the program.

In closing, let me underscore that we're highly committed to bringing deuruxolitinib to market as quickly as possible, and I'm extremely proud of what our team has accomplished and where we're headed.

At current prices, we are paying $0.35 cents for a contingent value right that settles in part in 4 years and the majority of which will settle in 6 years. The CVR is not free, so it is essential to look at our chances of actually picking up these milestone payments.

The sales need to take place within the U.S. to qualify so we don't have to consider global potential for our purposes.

The company is citing data of around 1.5 million patients within the U.S. The figure is based on range of 700k - 1.5 million from a 3rd party source.

{kind=link}

On pricing, we have the following guidance from the company (provided Sun doesn't take an entirely different direction)

Nancy Stuart

Hi. This is Nancy, and thanks so much for the question. Yeah. We -- what we have said is we expect that our pricing will be in line with other JAK inhibitors in the autoimmune derm space, including alopecia. That price parity is what we will be going for.

My understanding is that JAK inhibitors are currently priced between $26k/year to $60k/year in the U.S.

This treatment has the potential to be best-in-class with a favorable safety profile. There are, to my understanding, at least two other similar treatment options owned by big pharma in the market.

Something else to consider is that around 50% of patients were satisfied with the treatment a few months in. Before/after photos of the treatment show it being remarkably effective, but if someone starts taking it, it doesn't mean they will necessarily stick with it.

Let's assume 700k possible patients. Let's assume Concert takes 30% market share. Sells the treatment at $26k per year. Around 50% of patients stick with it. All these assumptions are at the lower end of the range, but it also assumes every patient trying it and a fully saturated market. At that point, you end up with $2.9 billion in revenue. That's far above figures cited in the milestone agreement, which indicates the companies expect much more modest figures. Still, it is better to see a theoretical maximum that's well ahead of the targets than the reverse.

Going through the math above, I was left a bit dissatisfied that I was likely overestimating how easy this will be. As a biotech tourist, it is easy to miss things. The great thing about Seeking Alpha is that there is a wealth of authors sharing opinions on companies. Even on a micro-cap Biotech, there are multiple interesting articles. There was one article that I found especially helpful to understand the competitive position of this (potential) treatment better. It was this one by C.C. Abbott. Here's a quote (emphasis in original):

3. While all 3 companies acknowledge the blockbuster (annual sale of $1B) potential of the AA space, CNCE is the only one that mentions CTP-543 being potentially Best -in-class.

This could mean best in terms of efficacy , as seen above in the cross-trial comparison of CNCE's first p3 data to LLY & PFE's data, which may be repeated/confirmed in CNCE's second p3 data.

It could also mean best in terms of safety profile, as LLY's OLUMIANT, an oral JAK inhibitor carries a boxed warning about serious infections, malignancies, major adverse cardiovascular events ((MACE)) and thrombosis in its approval label for rheumatoid arthritis ((RA)) and atopic dermatitis ((AD)).

She seems somewhat optimistic that the small biotech can carve out a part of the market, and the backing of Sun Pharma would likely only improve the odds of that.

I also found this article by Sage Advisors very helpful to understand how my estimate is overshooting. Sage Advisors dives into factors that explain why the actual number of patients that will end up taking the drug is smaller than proposed above. A quote (emphasis added):

Concert likely has a best-in-class JAK inhibitor for AA. Mizuho's $400 m peak sales forecast appears possible based on premium pricing. The AA market will likely be a competitive one with Eli Lilly's Olumiant, Pfizer's ritlecitinib and CTP-543 eventually vying for market share. 543 is likely to be last to market giving competitors a chance to gain market share.

Sage concludes that $400 million in peak sales is possible.

Luckily we don't need to pinpoint sales very exact to make money here. The milestones are for U.S.-based sales (yearly and consecutive quarters) of $100 million and $500 million.

The $100 million appears very doable, given only one competitor has just entered the market. If we hit that milestone and we pay $0.35 for the CVR that's a fantastic return right there.

I really don't need the $500 million to hit. The Mizuho $400 million forecast (which may have served as a basis for the CVR milestones) appears hard to hit. However, the company has until 2029 to hit. Inflation running at 7% per year helps drug pricing. Finally, the milestone is for four consecutive quarters instead of annual sales (slightly easier to hit). Not going to lie; the 2nd milestone is no shoe-in. But I view it as an attractive out-of-the-money option I'm effectively not paying up for (or at least not very much).

CNCE price change (YCharts )

The transaction is expected to be completed in the first quarter of 2023. Over 50% of shareholders need to tender (which will likely happen), and I don't expect any regulatory objections. Even though I believe the odds are minuscule that this tender offer somehow falls through, it is good to take note of the pre-deal price. The stock traded up only 21% on the announcement, which suggests the downside isn't the typical biotech scenario where it is down 50%-60% on a deal break.

For further details see:

Concert Pharmaceuticals: Negative Spread But Interesting CVR