CNDT - Conduent To See Unpredictable Forward Revenue (Rating Downgrade)

2023-12-27 15:28:27 ET

Summary

- Conduent Incorporated provides business process outsourcing services to organizations and governments worldwide.

- The company is forecasting "lumpy" revenue recognition ahead, and analysts expect a decline in revenue in 2024.

- My outlook on Conduent stock is to Sell due to ongoing uncertainty and potential sales cycle delays.

A Quick Take On Conduent

Conduent Incorporated ( CNDT ) provides business process outsourcing services to organizations and governments worldwide that have transaction-intensive applications.

I previously wrote about CNDT in September 2023 with a Hold outlook on further client spending headwinds.

The firm is forecasting unpredictability, which, when combined with expected revenue decline in 2024 and ongoing uncertainty in its large commercial division, my outlook on Conduent is to Sell.

Conduent Overview And Market

New Jersey-based Conduent provides a range of outsourced business process services to companies, governments and transportation concerns.

The company is led by president and CEO Cliff Skelton, who was previously President of Fiserv Output Solutions.

The firm’s primary offerings include:

-

Commercial Industries

-

Government Services

-

Transportation.

CNDT seeks new customers via its direct sales and marketing efforts and through various partner channel referrals.

Conduent serves virtually all major industry groupings, the U.S. government and various transportation entities.

Per a 2023 market research report by Grand View Research, the global market for business process outsourcing was an estimated $262 billion in 2022 and is expected to reach $537 billion by 2030.

This represents a forecast CAGR of 9.4% from 2023 to 2030.

The primary reasons for this expected growth are the increasing usage of digital tools and delocalized talent to maximize business efficiencies while enabling the business to focus on its core competencies.

The versatility of outsourcing services is growing as other types of service process automation and intelligence add to the return on investment for enterprises.

Below is a chart showing the historical and expected future growth trajectory of process outsourcing services in the U.S. from 2020 to 2030:

Grand View Research

Major competitive or other industry participants include:

-

24/7 Intouch

-

Appen

-

TDCX

-

Accenture

-

TaskUs

-

Genpact

-

Tata Consultancy

-

Cognizant

-

Teleperformance

-

Telus International

-

TTEC

-

VXI

-

Sutherland.

Conduent’s Recent Financial Trends

Total revenue by quarter (blue columns) has continued to decline due to softness in its Commercial segment, which accounts for the largest segment the company serves; Operating income by quarter (red line) has also dropped recently:

Seeking Alpha

Gross profit margin by quarter (green line) has remained stable in recent quarters; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have also changed little.

Seeking Alpha

Earnings per share (Diluted) have been volatile and turned sharply negative in two of the last four quarters:

Seeking Alpha

(All data in the above charts is GAAP.)

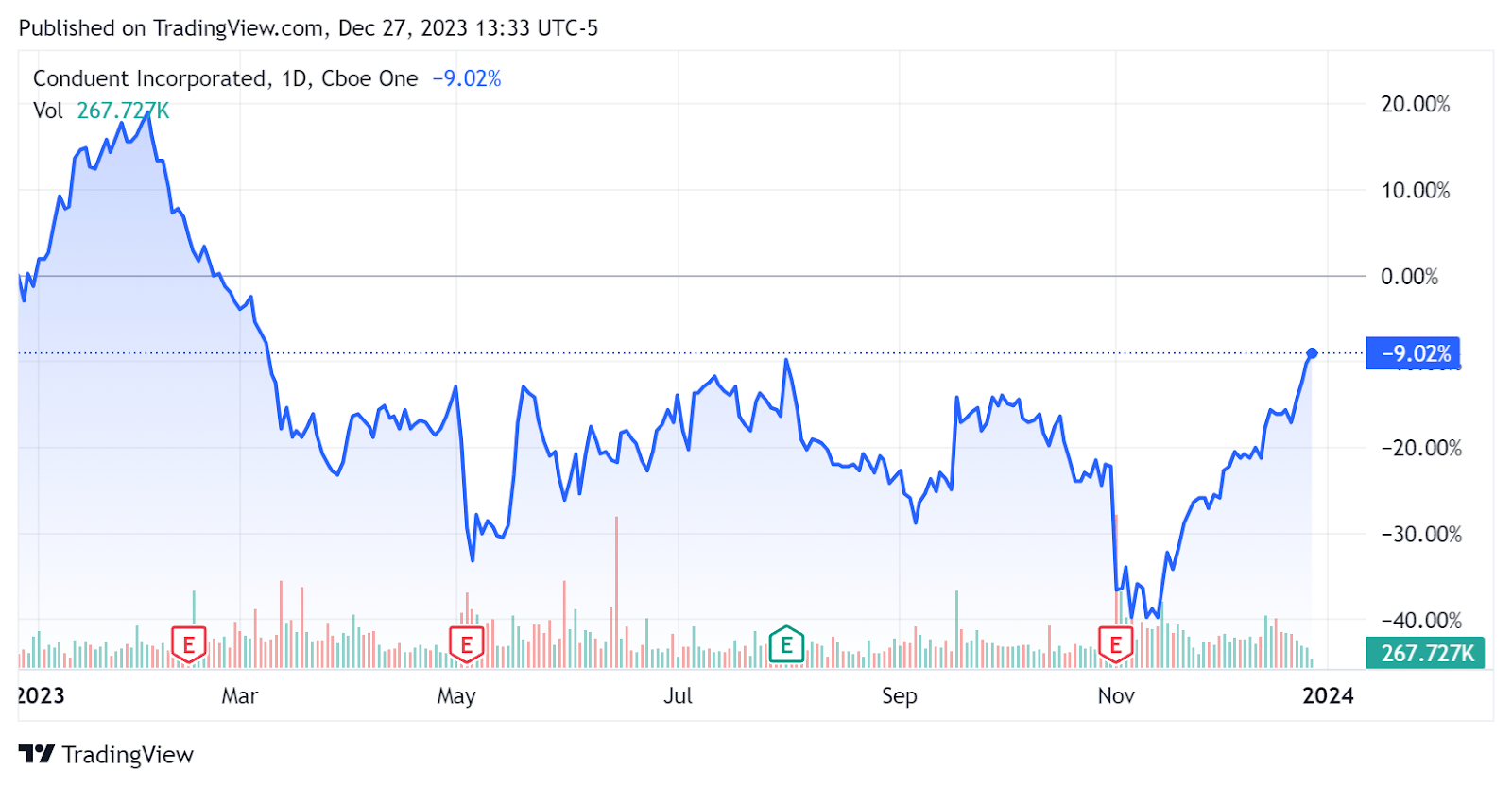

In the past 12 months, CNDT’s stock price has fallen by 9.02%:

{kind=link}

For balance sheet results, the firm ended the quarter with $451.0 million in cash and equivalents and $1.3 billion in total debt, of which $40.0 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash used was ($45.0 million), during which capital expenditures were $63.0 million. The company paid $19.0 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Conduent

Below is a table of relevant capitalization and valuation figures for the company:

| Metric |

| Amount |

| EV/Sales ((FWD)) |

| 0.5 |

| EV/EBITDA ((FWD)) |

| 5.9 |

| Price/Sales ((TTM)) |

| 0.2 |

| Revenue Growth (YoY) |

| 4.2% |

| Net Income Margin |

| -16.9% |

| EBITDA Margin |

| 7.2% |

| Market Capitalization |

| $799,620,000 |

| Enterprise Value |

| $2,020,000,000 |

| Operating Cash Flow |

| $18,000,000 |

| Earnings Per Share (Fully Diluted) |

| -$2.99 |

| 2024 FWD EPS Estimate |

| $0.08 |

| Revenue Growth Estimate ((FWD)) |

| -3.2% |

| Cash Flow/Share ((TTM)) |

| -$0.45 |

| Seeking Alpha Quant Score |

| Sell - 2.04 |

(Source - Seeking Alpha.)

Commentary On Conduent

In its most recent earnings call (Source - Seeking Alpha ), management’s prepared remarks highlighted the increased diversification of its revenue streams, with a strong quarter from its Government healthcare segment.

Management has been taking steps to rationalize its portfolio of offerings and previously announced the sale of its BenefitWallet business.

The firm also continues to market its FedNow network capability for immediate payment processing.

New business sales have been stronger in Government and Transportation verticals, while its Commercial vertical "continues to be impacted by macro-economic trends."

However, since its Commercial vertical accounts for the largest share of the firm’s business, per the following Q3 2023 chart from the company, it has an outsized impact on the firm’s results:

Seeking Alpha

For the quarter’s results, total revenue fell by 4.6% year-over-year, while gross profit margin slid by 0.5%.

Selling and G&A expenses as a percentage of revenue dropped by 1.1% YoY, but operating income fell sharply by 66.7%.

The company's financial position is moderate, with plenty of liquidity but substantial long-term debt and materially negative free cash flow.

The firm’s employee retention rate was characterized by CEO Skelton as the "strongest since I arrived and improving."

However, the company is seeing longer sales cycles amid a more cautious buying environment among its Commercial segment customers, its largest segment.

This will likely weigh on future revenue growth along with the divestiture of its BenefitWallet business for $425 million, which is expected to close in Q1 2024.

Looking ahead, 2023 topline full-year revenue is expected to decline by 3.6% versus 2022’s results.

2024 revenue is now expected to drop a further 3.2%, per consensus estimates.

Also, management expects greater unpredictability in its government and transportation billing milestones, presaging potentially higher volatility in outcomes in Q4 2023 and 2024.

Given such unpredictability combined with expected revenue decline in 2024 and ongoing uncertainty in its large commercial division with the potential for continued sales cycle delays, my outlook on Conduent Incorporated stock is to Sell.

For further details see:

Conduent To See Unpredictable Forward Revenue (Rating Downgrade)