KCE - Confidence Crisis: Implications Of Bank Failures On The Industry

2023-04-25 11:35:00 ET

Summary

- Considering the pace and magnitude of interest rate hikes over the last year, it’s not surprising that issues in the banking industry have resulted in a confidence crisis.

- The swift and aggressive intervention by regulatory and private sector authorities in March might have been sufficient to extinguish the immediate fires seen in the market, but embers are likely to remain, and additional measures may be needed to avoid further crises.

- This crisis will continue to shift the banking landscape in meaningful ways, creating opportunities within the industry for investors to identify winners and losers.

By Jonathan Perez, CFA, Sr. Analyst, Fixed Income, and Mary Brown, CFA Analyst, Equities

Recent bank failures have understandably dominated much of the news cycle, with many waiting with bated breath for the next shoe to drop. Considering the pace and magnitude of interest rate hikes over the last year, it’s not surprising that issues in the banking industry have resulted in a confidence crisis. While the full impacts have yet to be felt across the economy, there will likely be real economic consequences, including slower-than-anticipated growth, increased credit losses in riskier credit categories (auto loans, credit cards, etc.), and unrecognized pockets of weakness that may require further monetary/fiscal policy measures.

The swift and aggressive intervention by regulatory and private sector authorities in March might have been sufficient to extinguish the immediate fires seen in the market, but embers are likely to remain, and additional measures may be needed to avoid further crises. The question that remains is: Where do banks and financials go from here?

Big banks will get bigger

Significant rate hikes over the past year complicated the funding situations of banks - particularly those with vulnerabilities - leading to acute pressures on a small selection of unique institutions. Following the news of the recent bank failures, depositors with shaken confidence quickly voted with their feet and decided the relative winners and losers. Fears of broader contagion led to rapid deposit flight, and many regional U.S. banks fitting a similar mold to the two failed institutions - Silicon Valley Bank ( SIVBQ ) and Signature Bank ( SBNY ) - were swiftly penalized. In fact, even banks with otherwise sound balance sheets were impacted.

At the outset, the largest banks appear to be the relative winners of the confidence crisis. As markets work through bank liquidity fears and commence the credit cycle, the perceived safety of large banks, that go through extensive annual stress-testing, will work in their favor. Behavior of depositors over the past few quarters has been a tug-of-war between seeking yield and achieving safety. The biggest banks, with geographic and customer diversity, often have a nationwide footprint that provides a deposit base of small transactional and non-interest bearing checking accounts. If the lesson learned from the recent bank failures was a concentrated deposit base with significant uninsured deposits can cause a bank to fail quickly, depositors seeking safety will likely continue to behave in ways that aim to mitigate that risk.

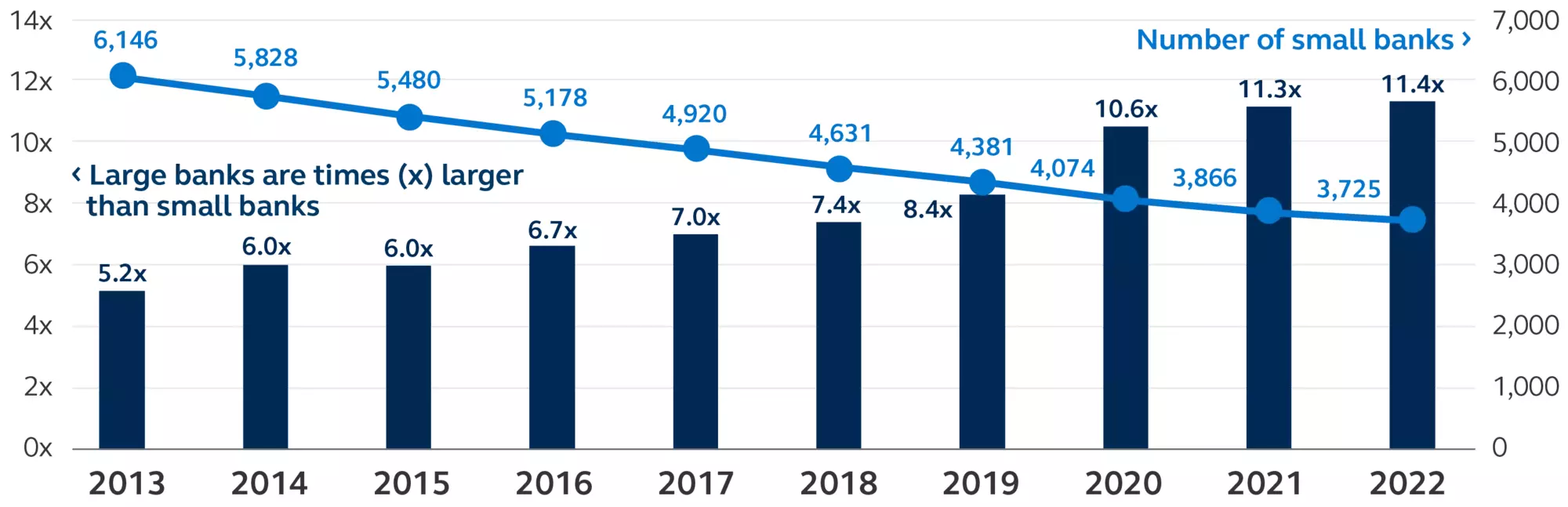

The number of small banks has decreased, while the assets at large banks have steadily increased

Large bank assets times ((x)) larger than small bank assets, number of small banks, 2013-2022

Federal Deposit Insurance Corporation and Principal Asset Management. Data as of December 31, 2022

{kind=link}

Note: Small banks defined as banks with less than $1B in assets. Large banks defined as banks with more than $250B in assets.

More regulation and stress-testing

Following the Great Financial Crisis (GFC), new resolution frameworks focused on bail-ins vs. bailouts were crafted by financial regulators, resulting in required annual stress-testing for the biggest U.S. banks. This was thought to be unnecessary for smaller banks, as they were not considered of systematic importance to the greater financial system. But even in today’s post-GFC environment, otherwise healthy banks - those with no capital or asset quality problems - were still penalized, leaving many asking what threshold should be considered systemic.

There will likely be regulatory calls going forward for the liquidity coverage ratio framework to be applied to smaller banks and for annual stress-testing to be required for banks under the $250 billion threshold. Clearly, the failure of SVB and Signature Bank, and the teetering of First Republic ( FRC ) and other penalized U.S. regional banks, underscores the need to emphasize stress-testing and contingency plans across the banking industry.

Imposing the liquidity coverage ratio on smaller banks, better incorporating severe outcomes into testing, and expanding the total loss-absorbing capital rules (i.e., the requirement that banks have enough loss absorbing debt) across a larger selection of banks could help to prevent future crises.

Accelerated credit cycle

After a prolonged period of low rates, quantitative easing (QE), and pandemic-related stimulus, a financial bubble has seemingly grown, and recent U.S. regional bank failures may be the signal that this bubble has popped. If not a full rupture, the confidence crisis has - at a minimum - accelerated the credit cycle, highlighted by a meaningful rise in the near-term probability of recession.

Amidst and just following the GFC, banks were tight on credit to consumers due to decreased housing values and increased unemployment. While these exact issues don’t exist today (consumers are far less levered and unemployment, although slowly rising, remains relatively low), interest rates are markedly higher today than the near-zero level that resulted from the GFC. Another notable difference is the persistent level of inflation in the current environment, which will likely lead to continued margin compression for companies dealing with higher expenses and elevated interest rate costs. If companies are levered and experiencing stress from inflation, interest payments, and tighter credit conditions, banks that have provided them loans may experience losses. U.S. regional bank failures could exacerbate these conditions as smaller banks tend to have less diversified loan books and are more exposed to commercial real estate than larger banks. From here, smaller banks will likely further tighten their credit standards, and with no one available to extend them credit, the financial condition of the weakest borrowers in the economy will likely begin to erode quickly.

In the end, this confidence crisis could ignite a cycle of rating downgrades, loan and corporate bond defaults, and further the risk of a broader credit crunch. Initially, banks will bear the brunt of the cycle as credit normalizes and they book more reserves based on the higher likelihood of a recession. Once realized, however, the recession will prompt more rating agency downgrades as corporate margins are squeezed and earnings recede.

Increased market turbulence and recession risk

This crisis will continue to shift the banking landscape in meaningful ways, creating opportunities within the industry for investors to identify winners and losers. Now that the market has absorbed the acute impact of the bank failures, it’s moved on to what’s next - the fear of the unknown, which markets dislike most and discount heavily. How deep will the recession be? Has the aggressive Federal Reserve (Fed) overshot, potentially causing GFC 2.0? While the answers to these questions are unknown, pockets of opportunity have been created by equity multiple compression and fixed income spread widening.

Data that proves the recession and credit cycle have begun will solve for the unknowns and could be a clearing event for the market. Look for early signals that the credit cycle has commenced, and inflation is turning over, to capitalize on opportunities. Peak inflation means the Fed can stop hiking, which affects the predicted terminal rate. The lower the predicted terminal rate, the more likely banks and financial companies that bore the brunt of rapid Fed hikes - those with real estate or alternatives exposure or the strongest banks without heavy commercial real estate exposure - could see a recovery. As always, a diverse business mix and strong balance sheet are crucial and will contribute to the magnitude of multiple and spread recovery - and will separate the winners from the losers following the banking confidence crunch.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Confidence Crisis: Implications Of Bank Failures On The Industry