CFLT - Confluent: A Stock On The Rise But Timing Is Everything

2023-06-30 06:25:03 ET

Summary

- While Confluent's revenue growth rates are promising, the company did not revise its outlook for 2023, and caution is advised regarding the stock's recent price increases.

- Confluent's net retention figures have shifted towards a consumption-based business model. What does this mean?

- The services segment of Confluent's business is holding back rapid growth, but investors do not assign much weight to it.

- Confluent's free cash flow profile needs improvement as the company is still burning cash.

Investment Thesis

Confluent (CFLT) is a decision-making platform. It enables companies to leverage their own data to derive actionable insights.

Confluent is rapidly growing and investors are clearly very welcoming of this aspect. However, the investment thesis has some blemishes, which I discuss here.

All in all, I believe that Confluent has what it takes to still deliver a positive surprise and upwards revise its 2023 guidance. However, given that in the past few months, its stock has already re-rated substantially higher, I don't see much reason at this point to turn bullish on this stock.

But I'm keenly watching this name. And, if Confluence is indeed able to confidently raise its full-year outlook while improving its profitability profile, I will be more than inclined to assign a buy rating to this name.

Why Confluent? Why Now?

Confluent's platform drives data-driven operational efficiencies. It allows users to process and analyze real-time streaming data at scale. Its value proposition stems from enabling businesses to make decisions using their own data.

Confluent is a company that provides a platform built around Apache Kafka, an open-source technology, and Confluent seeks to expand the capabilities of Apache Kafka.

Essentially, Confluent allows users to process streams of data to uncover insights.

I assert that the one blemish to the investment thesis is that Confluent's net retention figures have recently changed towards a consumption business model for its cloud business unit.

Here's a quote from the earnings call ,

[...] starting this fiscal year, we moved to consumption-based NRR for Confluent Cloud [...]

Total NRR for Q1 was above 130%, and gross retention was above 90%.

I've seen that, with time, consumption-led business models can be extremely volatile and noisy from quarter to quarter.

The example that I often provide to explain a consumption business model, versus the commitment-pricing, that Confluent provides for its Hybrid clients rather than their Cloud clients, is like this:

Think of watching a movie on Blockbuster. You are on a pay-per-view. The other method is like Netflix ( NFLX ). Which business is more successful? The one where you are maximizing what you charge your customer per month? Or the one where you are working to make sure it's as cheap as possible for the customer and the customer spends as much time as possible on your platform?

The one where you are conscious of buying up watch time or the one where you are just constantly binging?

For their part, Confluent goes on to say,

So think of MongoDB, Datadog, Snowflake, they all have moved to a consumption-based NRR

Still, I would reiterate my previous assertion, that a consumption-based business model can be highly volatile and prone to negative surprises. That aside, let's move forward to discussing Confluent's financials.

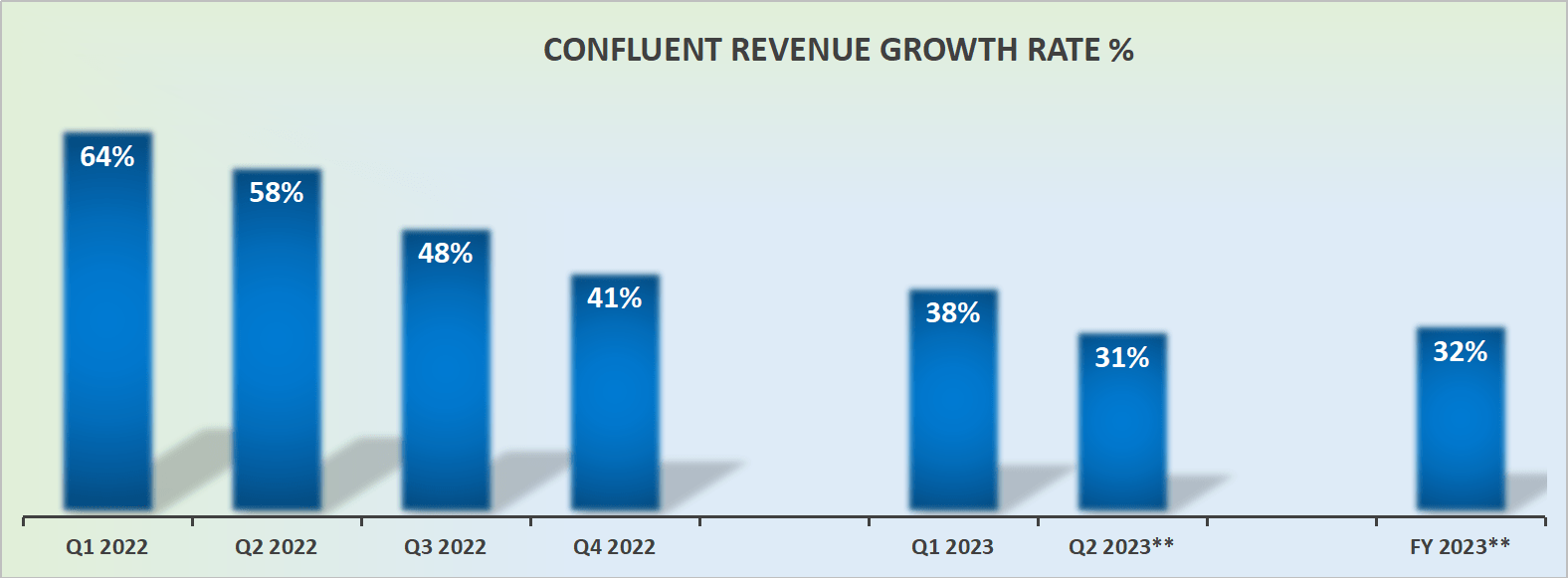

Revenue Growth Rates Are Misleading

{kind=link}

In my previous analysis , before heading into Q1 results I said,

The good news here is that Confluent's Q1 2023 is expected to beat 30% CAGR, and since that's the toughest quarter to compare against, that should mean that there's ample room to upwards revise its full-year 2023 revenue guidance.

As it transpires, Confluent did not take the opportunity to upwards revise its outlook, as Confluent is still guiding toward the same outlook as it did back at the start of 2023.

However, given that market conditions have eased up in the past couple of months, I am assuredly confident that now Confluent will be better placed, with more visibility, to upwards revise its outlook for 2023 when it reports its Q2 results in about a month's time.

Again, what I said previously, I stand by today, Q1 was the toughest comparable to go against, and as the comparables for the remainder of 2023 ease up, this will leave Confluent well-placed to positively impress investors.

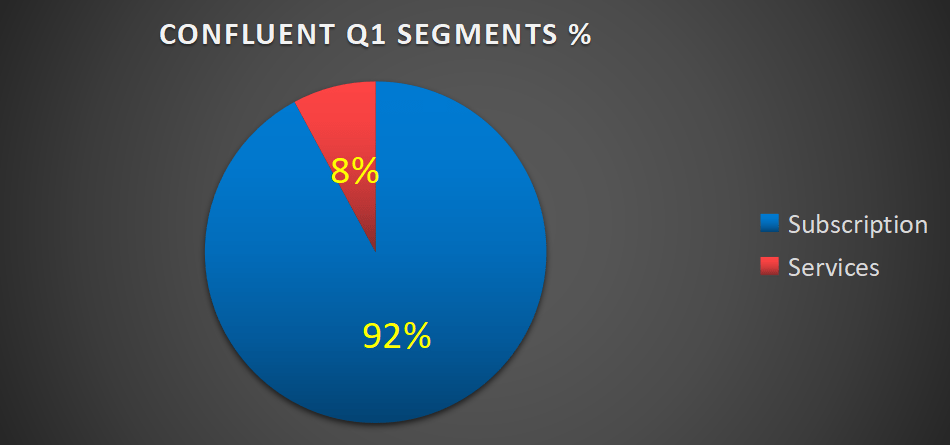

Furthermore, consider this element:

{kind=link}

What you see above is that about 8% of Confluence's revenues are made of its Services segment. And this segment didn't deliver much growth in the quarter. In fact, the Services segment was up 12% y/y, compared with its subscription segment which was up 41% y/y.

In other words, the one aspect that is actually holding back its rapid growth is the one area of the business that investors don't put much weight on , in any case.

Next, let's turn our focus to Confluent's free cash flow profile.

Free Cash Flow Profile Needs to Improve

CLFT Q1 2023

Above we see that Confluent's free cash flow margins are not improving. Recall, a substantial proportion of its free cash flow is stock-based compensation that is added back. And even with that significant expense added back, the business is still hemorrhaging cash.

Confluent does have more than enough cash on its books, with more than $700 million of net cash, so its cash burn isn't an immediate problem.

However, given that all that has happened to the stock in the past few months while there has been a substantial multiple expansion, I'm not entirely convinced that now is a good time to chase this stock higher.

The Bottom Line

Confluent, a decision-making platform, is experiencing rapid growth and investors are responding positively.

However, there are some concerns with the investment thesis. While there is potential for Confluent to surpass expectations and revise its 2023 guidance upward, the stock has already seen significant price increases, leading me to be skeptical about turning bullish at this point.

The main concern lies in Confluent's net retention figures, which have shifted toward a consumption-based business model for its cloud unit. Consumption models can be volatile and prone to negative surprises.

Despite this, Confluent's financials show promising revenue growth rates, although the company did not revise its outlook for 2023.

As market conditions improve, there is confidence that Confluent will have better visibility to revise its outlook during the upcoming Q2 results.

Confluent's free cash flow profile needs improvement as it is still burning cash.

Considering the recent multiple expansion of the stock, caution is advised when considering investing in Confluent at this time.

For further details see:

Confluent: A Stock On The Rise, But Timing Is Everything