CFLT - Confluent: Crash Due To Broken Narrative

2023-11-27 22:20:33 ET

Summary

- Confluent's share price decline reflects uncertainty regarding the company's ability to attract and retain customers.

- This is particularly problematic as Confluent has positioned its platform as a cost-effective alternative to Kafka for large customers.

- Even after the recent share price decline, Confluent is still somewhat expensive given near-term growth prospects and the company's large losses.

- Current concerns appear to be overblown, meaning Confluent's stock should bounce back, but it may take time for the company to rebuild investor confidence.

Confluent's ( CFLT ) share price drop post Q3 earnings may have seemed excessive but it needs to be viewed in light of the company's valuation and the challenges that Confluent is currently facing. Confluent's switch in focus to consumption, slow customer additions and the return of a large customer to on-prem cut to the heart of Confluent’s value proposition. Kafka is supposed to be difficult and expensive to manage at scale, making Confluent an attractive option for larger organizations. If Confluent is struggling to attract and retain customers in a cost-conscious environment, the company's value proposition may not be resonating. In addition, Confluent's growth is rapidly decelerating, losses remain large, and the company is changing CFO.

The last time I wrote about Confluent I highlighted the demand weakness the company was facing and its lack of efficiency. Soft demand continues to be a problem and progress towards profitability has only been modest.

A strong narrative and financial performance are needed to support a high valuation and Confluent has neither of these at the moment. Confluent now appears more reasonably priced, but growth will continue to decelerate sharply in coming quarters. Even if margins continue to improve and growth eventually recovers, it will likely take time for investors to regain faith in the company.

Market

While the macro environment appears to have stabilized, and is improving for some software companies, conditions are still generally challenging. Budget scrutiny remains elevated and as a result, sales cycles are still longer than normal. Customers also want to sign shorter duration contracts and start with smaller initial deal sizes.

Confluent has suggested that the macro environment is pressuring the number of net new software projects that are getting funded. This is causing slower organic consumption growth. While Confluent's net retention rates are declining, the company does not give precise figures, making the extent of the decline difficult to determine.

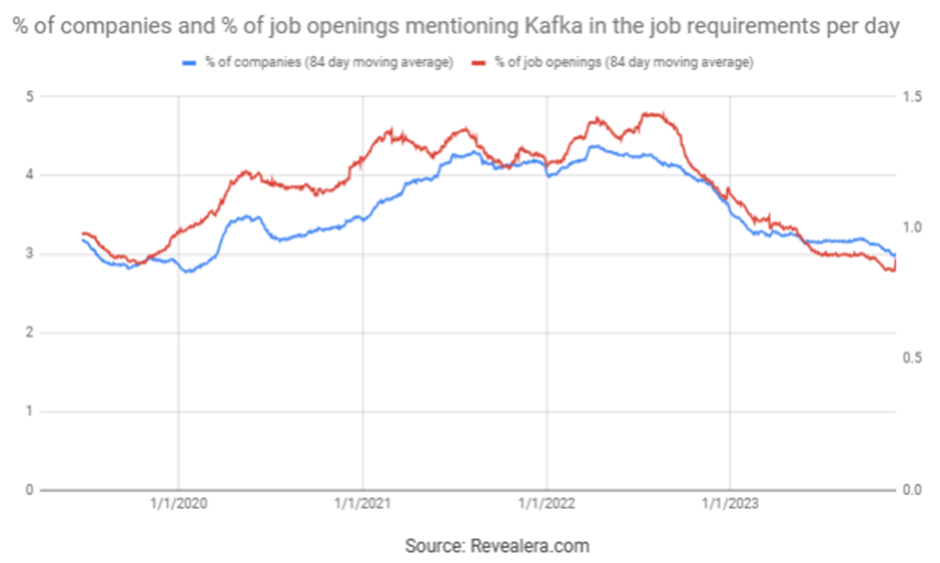

The number of job openings mentioning Kafka in the job requirements has declined significantly over the past 18 months, which may support the notion that Confluent's issues are primarily the result of the macro environment.

Figure 1: Job Openings Mentioning Kafka in the Job Requirements (source: Revealera.com)

{kind=link}

Confluent relies on a consumption-based business model, which has likely contributed to investor uncertainty and multiple compression. Confluent is not as exposed to transactions or analytics as companies like MongoDB ( MDB ) or Snowflake ( SNOW ) though. Rather, they are dependent on operational workloads which they believe are fairly resilient.

Confluent has also highlighted geopolitical headwinds, particularly as Israel is a top 10 country for the company. Confluent also referenced a potential US government shutdown as a headwind. While these factors may be a problem at the margin, Confluent's current struggles go well beyond geopolitical headwinds and a potential slowdown in Federal government spending.

Repatriation

Confluent continues to be optimistic about its prospects due to the TCO advantage of its cloud offering. Confluent believes that this advantage is sustainable due to a deep technical moat that the company has developed over time. This potentially differentiates Confluent from many SaaS companies, as it faces less direct competition.

Much of the cost of running Kafka is related to cloud infrastructure, including compute, storage, networking and the tools needed to ensure smooth operations. The personnel responsible for configuring, deploying and managing Kakfa are the other major cost component. Kakfka is a sought-after skill and as a result, personnel are generally well compensated.

Rather than just offering open-source Kafka as a service, Confluent has made a number of innovations which reduce the cost of operating its cloud service. Unlike many open-source cloud offerings, Confluent’s service is capable of multi-tenant operations which allows it to pool customers on shared infrastructure, driving higher utilization. Confluent also provides intelligent tiering of data between memory, local storage and object storage to help reduce storage costs.

Confluent also utilizes real-time performance data from customers to optimize the routing of traffic, thereby improving performance and reducing cost. This is a scale-based advantage that is likely to increase over time as Confluent Cloud grows larger.

During the third quarter one of Confluent's larger customers (an online gaming company) moved workloads back into its own data center . This move was motivated by cost, but Confluent suggested that it is not Confluent specific, rather a broader strategic shift by the customer where workloads are being repatriated company wide. This customer appears to have returned to using Kafka, although Confluent is in discussions with them about Confluent Platform. While this development is having a material impact on Confluent’s business, more importantly, it is undermining the company’s narrative.

Confluent

Confluent still believes that real-time data streaming is a 60 billion USD opportunity, but this is really dependent on both the adoption of data streaming and Confluent’s value proposition relative to open-source options.

Data streaming enables data to be harnessed in real-time and at scale. This has become increasingly important due to the volume and velocity of data being generated, as well as architectural changes, like the rise of microservices. Confluent's platform sits at the center of an organizations data infrastructure, coordinating the flow of information across the organization. This potentially creates network effects and should mean that Confluent's software has high switching costs. The company must compete with Kafka on a cost basis though, and there is now some doubt about the company's ability to do this. Long-term I believe this fear is likely to be unfounded, but investors may shy away from the company until it definitively proves otherwise.

In addition to the core business, Confluent believes that Flink, connectors and data governance provide large expansion opportunities.

- Connectors - pre-built and fully managed connectors which connect Kafka to popular data sources and sinks

- Governance - secure data sharing between organizations

- Flink – stream processing framework

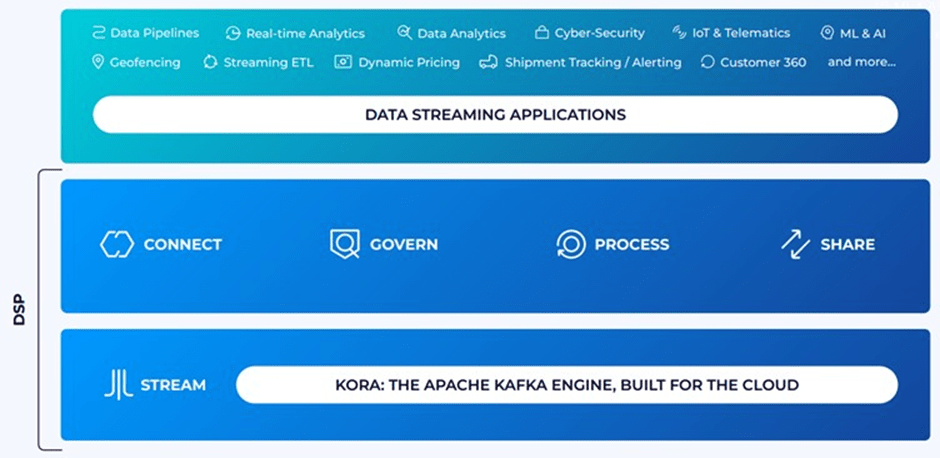

Confluent is combining Flink with Kafka and its connectors and governance capabilities to create a complete data streaming platform, which may help to differentiate its service and ensure retention remains high.

Apache Flink is a stream processing framework, which enables organizations to clean and enrich data streams. Stream processing allows customers to build applications on top of real-time data streams. Confluent has developed a cloud-native and serverless Flink offering which is now available in public preview in Confluent Cloud. Since the announcement, hundreds of customers have opted into the preview.

Figure 2: Confluent's Data Streaming Platform (source: Confluent)

{kind=link}

Confluent is currently trying to land new customers and drive expansion. As part of this effort the company has been orienting its cloud business around consumption, which is now expanding to include compensation of the salesforce. Confluent had previously made the transition to usage-based pricing, but going forward, cloud revenue will be the company's primary target rather than bookings or committed spend. This shift is designed to align customer value realization with Confluent’s revenue and is likely at least in part due to financial pressure on customers.

Financial Analysis

Confluent’s revenue increased by 32% YoY in the third quarter to 200 million USD. Confluent Cloud continues to drive growth, but this business is decelerating rapidly due to one large customer repatriating workloads and another large customer ramping at a slower pace as a result of being acquired. Consumption was also lower than expected amongst several large US digital native customers. Confluent is only anticipating 43% YoY Confluent Cloud growth in the fourth quarter. In comparison, Confluent Platform revenue growth reaccelerated to 19% in the third quarter driven by strength in regulated industries.

Table 1: Confluent Cloud YoY Revenue Growth Rate (source: Created by author using data from Confluent)

Revenue in the fourth quarter is expected to be 204-205 million USD, a 21-22% YoY increase. Confluent’s forward guidance has been impacted by both the macro environment and the headwinds created by the two large customers mentioned above. These customers account for roughly 50% of the expected consumption shortfall in the fourth quarter.

Figure 3: Confluent Revenue Growth (source: Created by author using data from Confluent)

{kind=link}

Growth in large customer cohort counts has decelerated significantly in recent quarters, suggesting either churn, an inability to land larger customers or weaker expansion. NRR has deteriorated somewhat and was just under 130% in the third quarter. Confluent’s gross retention rate continues to be above 90% though.

Given that Confluent Cloud is supposed to appeal to large organizations who don't have the resources to manage Kafka or are looking to reduce costs, the lack of large customer growth is concerning.

Table 2: Confluent YoY Customer Count Growth (source: Created by author using data from Confluent) Figure 4: Confluent Customers (source: Created by author using data from Confluent)

{kind=link}

Despite concerns about Confluent's business, hiring data supports broader adoption of Confluent and expansion of the customer base. This stands in stark contrast to the rapid decline in Kafka job openings over the past 18 months.

Figure 5: Job Openings Mentioning Confluent in the Job Requirements (source: Revealera.com)

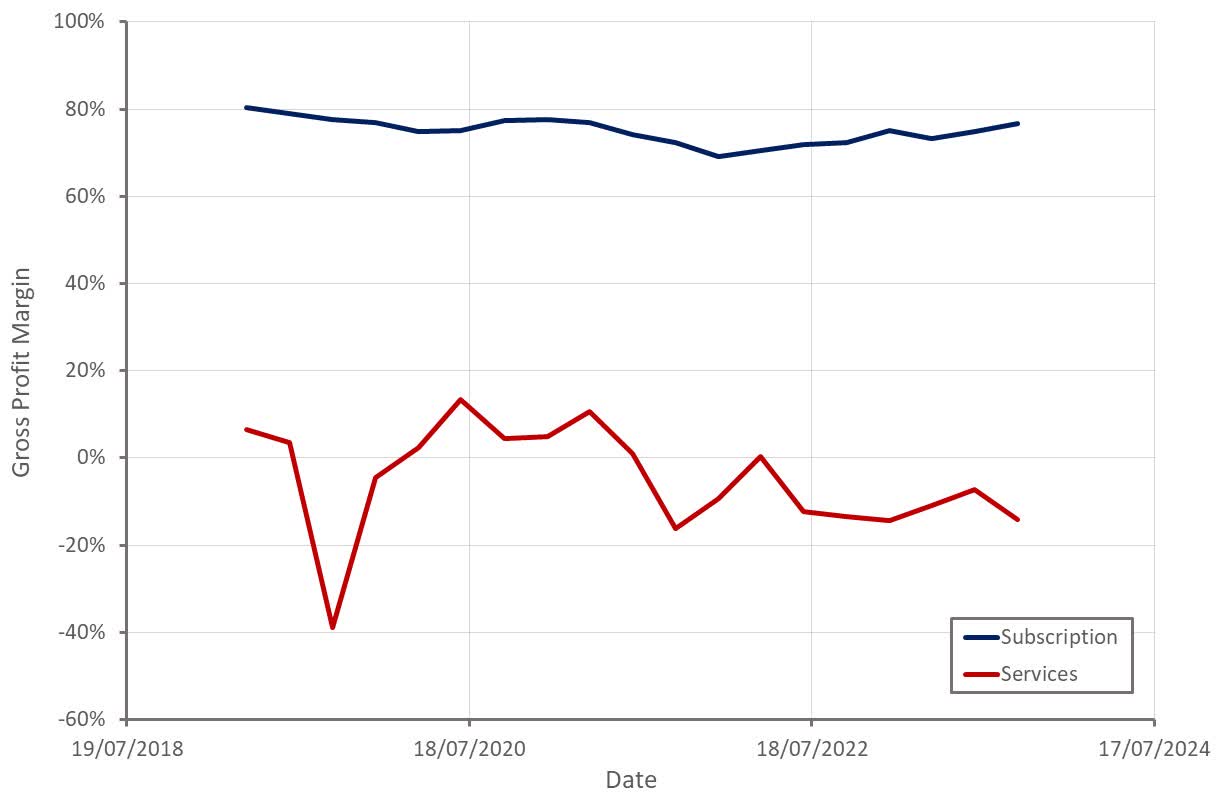

Subscription gross margin improvements are being driven by cloud product optimizations lowering costs. This has been somewhat offset by a deterioration in Services gross profit margins though. Viewing Services revenue as a customer acquisition cost, the deterioration in margins suggests that there has been pressure on growth over the last 2 years.

Figure 6: Confluent Gross Profit Margins (source: Created by author using data from Confluent)

{kind=link}

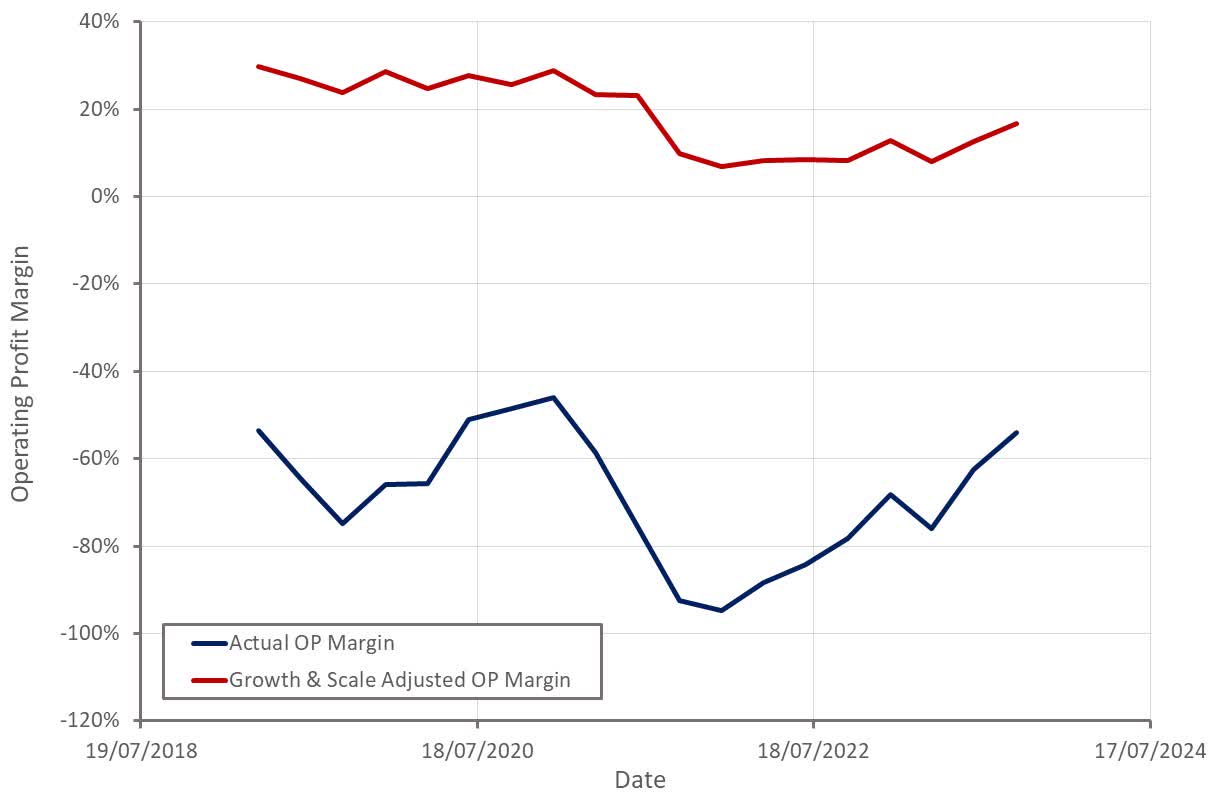

Confluent's operating profit margin has also been improving rapidly, although this should be expected given the drop in growth. Adjusting Confluent's operating profit margin for growth and scale indicates that while profitability has improved in recent quarters, it is still relatively low.

Confluent is expecting to achieve non-GAAP operating profit and free cash flow breakeven in FY2024 . This is somewhat meaningless though given Confluent's heavy use of SBC. Confluent shareholders are being diluted and this problem could become much worse if the company's valuation remains low.

Figure 7: Confluent Operating Profit Margins (source: Created by author using data from Confluent)

{kind=link}

Conclusion

Confluent now appears more reasonably valued relative to similar companies, but this is unlikely to matter until its financial performance begins to stabilize. Investors currently have little appetite for unprofitable companies, and this is exacerbated when growth is rapidly decelerating, or the company doesn't have a strong narrative.

Longer-term, Confluent still has a large opportunity ahead of it and appears well positioned to capitalize on the opportunity. While there is risk, I believe that current concerns are likely to prove to be overblown based on the extrapolation of the behavior of a handful of large customers.

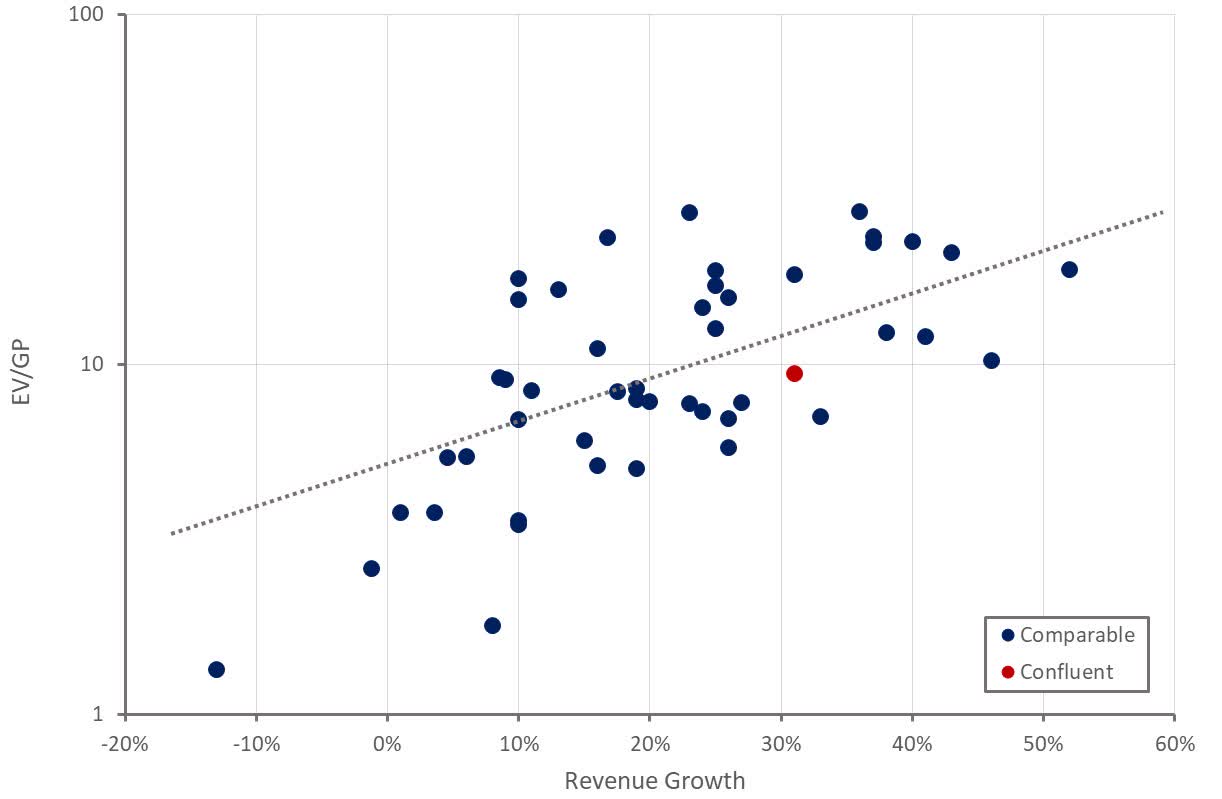

Figure 8: Confluent Relative Valuation (source: Created by author using data from Seeking Alpha)

{kind=link}

For further details see:

Confluent: Crash Due To Broken Narrative