CFLT - Confluent: Expectations Reset Upgrading To Buy

2023-11-30 14:47:32 ET

Summary

- We are upgrading Confluent to a buy.

- The stock has underperformed the S&P 500 by 41% since our sell rating from July 2021 and 34% in the past three months.

- We think the revised growth expectations for the company, as well as stock valuation, make the stock more compelling.

- We expect the lower customer consumption, average deal size, and contract duration to stabilize.

- CFLT's competitive position remained unchanged in the $60M TAM for infrastructure software and expects the company to outperform its peer group through 2024.

We're upgrading Confluent, Inc. ( CFLT ) to a buy after a long, bearish stance. The stock has underperformed the S&P 500 by 41% since our sell rating from July 2021 and 34% in the past three months. Our negative thesis of Confluent seeing mixed success in commercial versions of open-source software and difficulty convincing enterprise customers to pay up has played out. We now see a more favorable risk-reward profile for the stock in 2024.

We expect the issues that weighed on top-line growth, specifically lower customer consumption, average deal size, and contract duration, to stabilize as IT spending picks up in 2024. The following outlines our sell rating note on Confluent.

SeekingAlpha

We see a more compelling valuation at current levels. The stock is trading below the peer group average, looking at its EV/Sales multiple versus the peer group. CFLT stock is trading at 5.9x EV/C2024 Sales versus the peer group average of 7.5x. Consistent with our expectations in 2021, the stock's valuation has declined; in our last note, we wrote, "We will wait for the stock to decline to around $20-25 before recommending the stock." We see attractive entry points at current levels, with the stock hovering around $20 per share. The stock is currently undervalued, in our opinion, but we see room for the stock to re-rate higher once cloud growth gets factored into valuation in 2024. We think now is a good time for investors to swoop in at the bottom before the market wakes up to Confluent's growth potential in 2024 after its recent pullback.

The following outlines CFLT's valuation against the peer group.

TSP

Additionally, we think the revised growth expectation indicates that weakness is priced in, and now expectations have largely reset. The company plunged +25% in extended-hours trading after reporting a narrowed FY sales outlook in spite of better-than-expected Q3 results reported on November 1st. Confluent beat top and bottom line estimates over the past four quarters, and the stock traded higher in reaction to each quarter with the expectation of this quarter. We think Confluent's fundamentals remain intact, and we expect more traction for the enterprise software player in terms of ARR growth as the cloud capex expands next year. Our bearish call in mid-2021 was mainly a valuation call, and this year, we've seen the macro weakness tightening budgets weigh on top-line growth for Confluent - while the company beat estimates and maintained a double-digit Y/Y growth rate, its revenue growth Y/Y slowed significantly.

The company now expects FY sales to be in the $768-769M range compared to previous estimates of $767-772M and even earlier forecasts of $760M-765M guided in 4Q22. Management also de-risked guidance for next quarter, expecting to earn an adjusted 5 cents per share with sales between $204-205M lower than analysts' estimates of adjusted earnings of 5 cents per share and $212.3M in revenue. We think management has now factored in the macro weakness into the outlook, and we believe the market has priced it into the stock this quarter. The following outlines the stock's performance over the past three months against the S&P 500.

YCharts

Competitive edge still intact

CFLT's competitive position remains unchanged in the $60M TAM for infrastructure software; the global Software-Defined Networking Market size is expected to grow from USD 24.5B in 2023 to USD 60.2B by 2028 at a CAGR of 19.7% during the forecast period according to a new report by MarketsandMarkets. We see a wide enough market opportunity to encompass multiple players, including MongoDB, Inc. ( MDB ) and Elastic N.V. ( ESTC ).

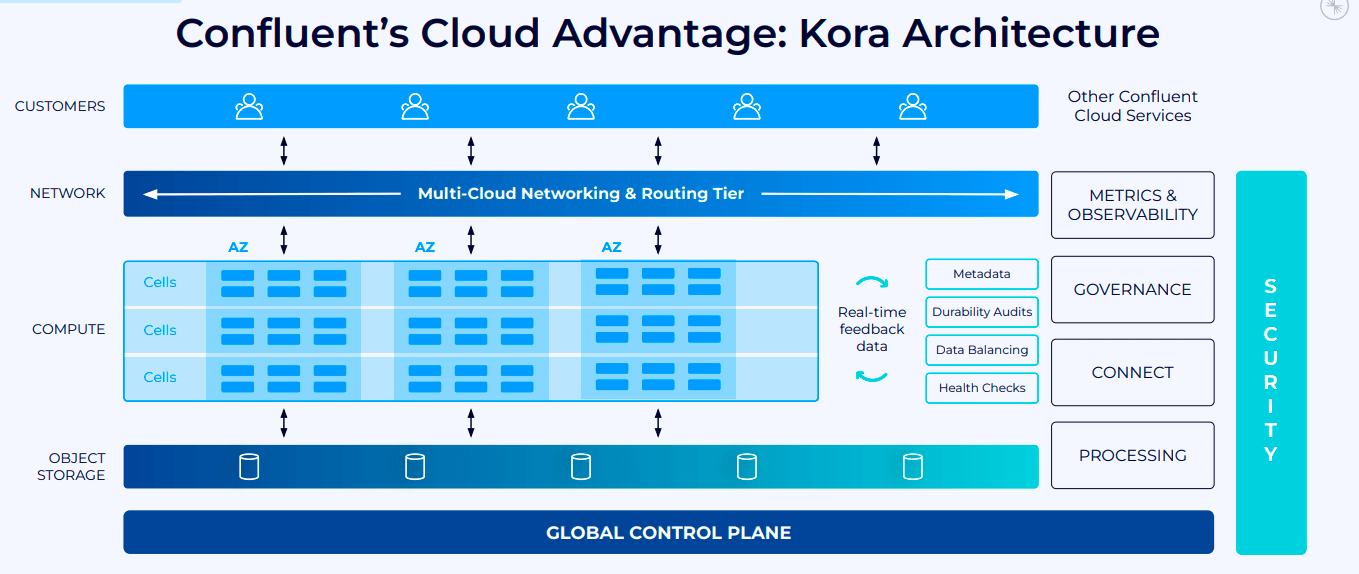

We think each player's offering truly differs in how it's 1. architected, 2. operates, and 3. the experience it gives to customers. We expect the company to outperform its peer group through 2024 as we believe Confluent has a competitive advantage in its Kora Architecture; Kora is a cloud data service that serves up the Kafka protocol for customers and their tens of thousands of clusters. The competitive edge of Kora is its ability to allow Confluent and its customers to scale its operations. We place a lot of emphasis on scale as we believe it'll be increasingly necessary to scale operations to feed the rebounding demand in enterprise digital transformation; Kora's elasticity allows for 30x faster scale up and down.

The following outlines Confluent's cloud advantage.

{kind=link}

Additionally, Kora offers reliability with more than 10x higher availability than the fault rate of Confluent's self-managed customers or other cloud services. In other words, Kora allows for a faster and more reliable scale for customers and the company and is fully compatible as it implements Kafka's protocol. We think Kora provides an attractive cost-to-efficiency ratio and see it driving outperformance in 2024.

Still, Confluent is not without its risks. We think the company remains exposed to macro uncertainty impacting enterprise budgets alongside the rest of the software peer group. Jamie Dimon, CEO of JPMorgan Chase & Co. ( JPM ), forecasted a recession earlier this week, noting, "Inflation could rise further and recession is not off the table." We think Confluent is at risk of seeing slower top-line growth due to these macro headwinds, but we already think the worst has been priced into the stock at current levels and FY sales. We think another downward guidance is unlikely in 2024.

Word on Wall Street

Wall Street shares our bullish sentiment on the stock. Of the 27 analysts covering the stock, 18 are buy-rated, eight are hold-rated, and the remaining sell-rated. The stock is priced at $21 per share. The median sell-side price target is $24, while the mean is $25, with a potential 17-20% upside.

The following charts outline sell-side ratings and price targets for CFLT

TSP

What to do with the stock

We are upgrading Confluent to a buy. The stock has underperformed the S&P 500 by 41% since our sell rating from July 2021 and 34% in the past three months. We think macro weakness pressuring IT budgets this year has been priced into the stock price and guidance for FY sales and the next quarter outlook. We see the stock outperforming the peer group in 2024 due to its competitive position and recommend investors buy in at current levels.

For further details see:

Confluent: Expectations Reset, Upgrading To Buy