CFLT - Confluent: I Remain On The Sidelines For Now

2023-03-17 02:49:55 ET

Summary

- The market opportunity for Confluent is estimated to be around $60 billion, and the company has only penetrated less than 1% of this market, indicating significant growth potential.

- Confluent remains confident in its guidance due to healthy retention rates and consumption patterns within its current customer base.

- SBC expense is expected to decrease, with the management targeting SBC to be in the high teens as a percentage of total compensation.

- The upside re-rating potential of the stock remains limited in the near term due to macro headwinds which is why I currently keep a Hold rating on the stock.

Thesis

Confluent ( CFLT ) has introduced a new approach to data infrastructure called Data-in-Motion. This approach involves capturing and processing data in real-time across multiple systems, teams, and applications in an organization. Essentially, Confluent provides tools that enable different systems and applications to share data instantly and independently, leading to improved operational efficiency, customer experience, and the creation of new use cases. Confluent's technology is aligned with industry trends like digital transformation, machine learning, and cloud adoption, positioning it well for the future. However, the company is still trading at a premium multiple, and with the deteriorating macro-outlook, I see limited chances of a multiple re-rating in the near-term despite the company's growth outlook, which is why I currently keep a Hold rating on the stock.

{kind=link}

Post Q4 Earnings Outlook

Confluent had a good Q4 in terms of revenue and profitability, with a 3.5% beat on revenue and a record quarter-over-quarter Cloud revenue increase of $11.5 million. However, the growth in bookings slowed down compared to the previous quarter, with a 4% year-over-year increase in total bookings growth and an 18% year-over-year increase in cRPO-based bookings growth. The company continued to attract new customers, with a 35% year-over-year increase in customers generating more than $100,000 in annual recurring revenue. However, the company faced challenges in the current macroeconomic environment, which resulted in increased scrutiny of deals and longer sales cycles. Additionally, existing customer expansion slowed down slightly, with dollar-based net retention coming in just under 130% for the fiscal year 2023, according to management.

During earnings call, discussions mainly focused on Confluent's Q4 performance, including factors that contributed to its results and factors underlying its guidance. The company experienced some softness in bookings due to deal elongation, particularly in December, and did not see the typical end-of-year budget flush that it usually sees in Q4. The sales cycle elongation affected total bookings more than cRPO-based bookings. However, the commercial segment showed strong growth and resilience in the quarter, and there were no significant trends across geographies or verticals. Confluent remains confident in its guidance due to healthy retention rates, the closure of some deals that slipped out of Q4, and consumption patterns within its current customer base.

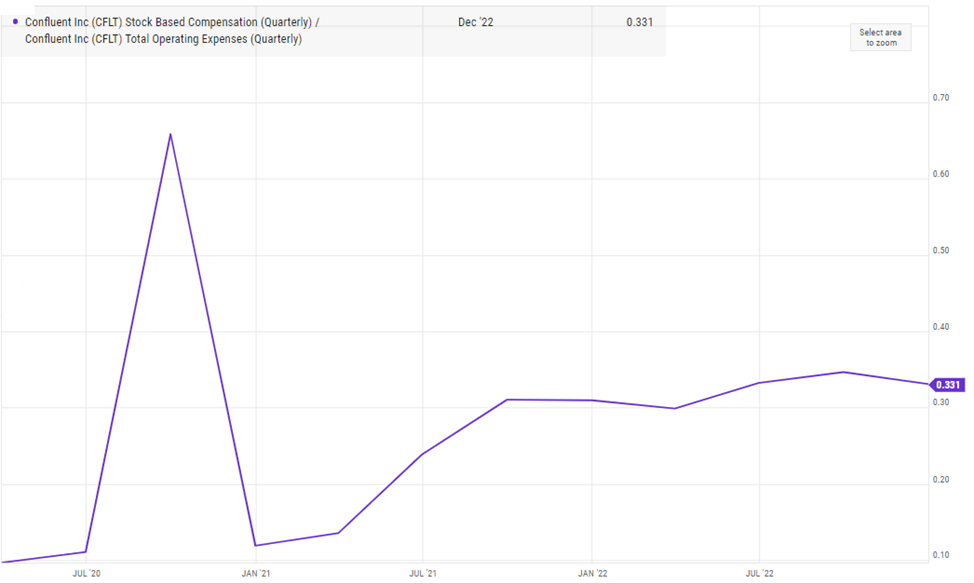

There is significant interest in Confluent's stock-based compensation (SBC) and expected dilution trajectory. It seems that the management aims to bring dilution levels in line with software peers, targeting the 50% to 75% percentile range for total compensation relative to the market over time. For FY23, the company is targeting 3-4% dilution and hopes to reduce this in subsequent years. As dilution decreases, SBC expense is also expected to decrease, although the expense is affected by stock price movements and has a lag due to the timing of grants. Over time, management is targeting SBC to be in the high-teens as a percentage of total compensation.

{kind=link}

Financial Outlook

The consumption trends for Confluent Cloud are likely to remain stable even during a slower macroeconomic environment. Some use cases, such as e-commerce or stock trading, may experience a slowdown during an economic downturn, but there are other use cases, like regulatory reporting, that are expected to be more resilient regardless of the macroeconomic conditions.

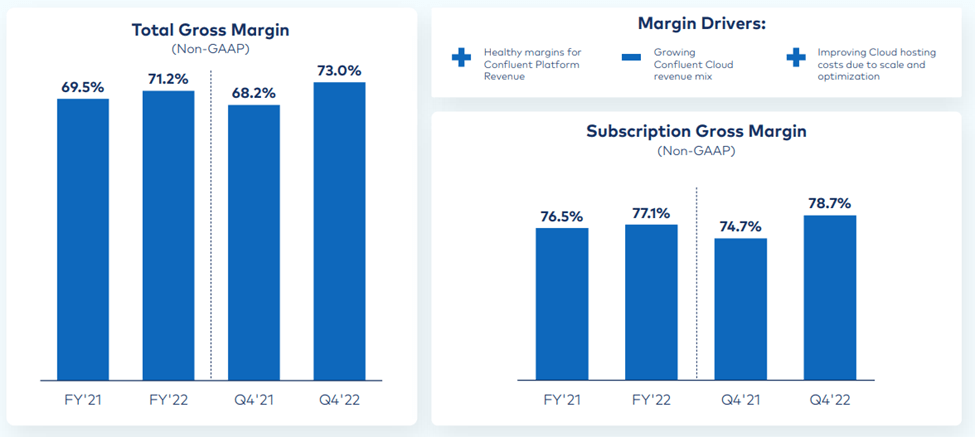

Confluent has reduced its hiring and taken other cost-cutting measures after making significant investments in 2021 and 2022. As a result, the company's OpEx growth is expected to be slower in 2023. The company is also focusing on improving sales and marketing efficiency by ramping up sales reps and strengthening partnerships with GSIs and CSPs. Even without significant efficiency gains, Confluent is expected to achieve its 2023 operating margin target as revenue continues to grow and higher-margin renewals become a larger portion of the mix.

Gross Margin Healthy as Revenue Mix Shifts (Company Presentation)

{kind=link}

Strong Market Position with Long Growth Runway

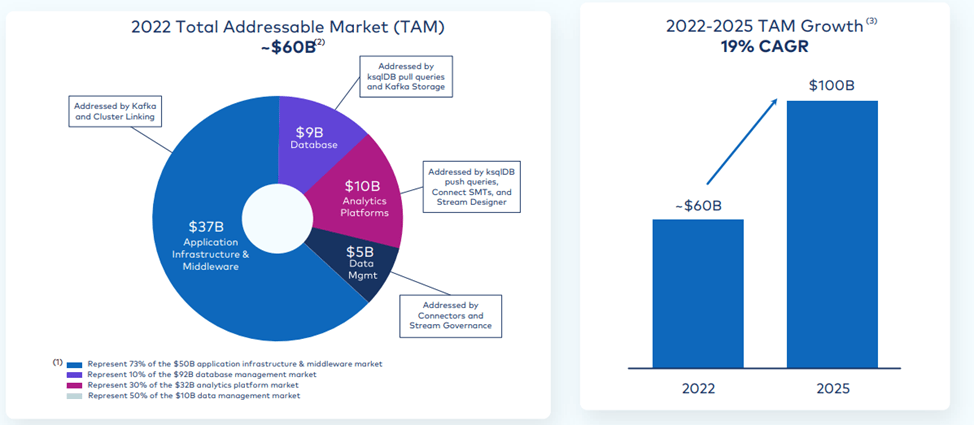

Apache Kafka is the core of Confluent's data-in-motion paradigm and was created by the company's founders as a free, open-source project in 2011. It has become the standard for real-time event streaming with broad-based adoption, used by over 300,000 organizations globally, including 80% of F500 companies, and has over 5 million lifetime downloads. Confluent is the only commercial company built around Kafka and the only one offering Kafka as a fully-managed cloud-native SaaS offering. The company's position is solidified by its expertise as the original founders of Kafka. The market opportunity for Confluent is estimated to be around $60 billion, and the company has only penetrated less than 1% of this market, indicating significant growth potential.

{kind=link}

Valuation

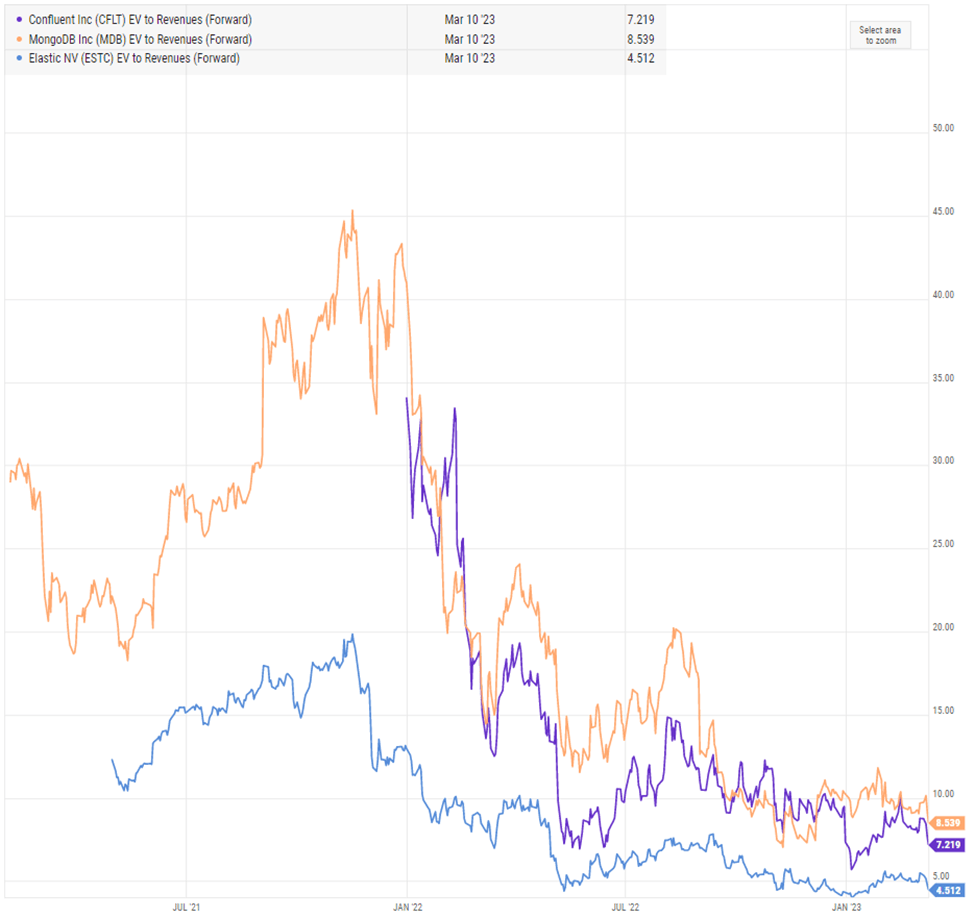

CFLT currently trades at 7.2 EV/CY23E revenue, at a slight discount to MDB and premium to ESTC. Even though the sector median is quite lower than CFLT's multiple, it has to do with other companies' slower growth rates compared to Confluent, and I think that Confluent has a better chance of sustaining its growth than most other software companies. However, factors such as higher interest rates, recession, or changes in investor preferences could restrict the potential for growth in software stock valuations. I believe that while there may be opportunities for Confluent to perform well, the growth potential of its stock valuation may be limited in the near-term, which is why I currently keep a Hold rating on the stock without a price target.

{kind=link}

Final Thoughts

Confluent's Q4 performance was impacted by softness in bookings due to deal elongation and the absence of the typical end-of-year budget flush. However, the commercial segment showed strong growth and resilience, and the company remains confident in its guidance due to healthy retention rates and deal closures. The company's solid market position with Apache Kafka and its potential for growth make it an attractive investment; however, the stock trades at a premium compared to other industry players and its own historical multiple, and I see limited opportunity for multiple expansion in the near-term which is why I remain on the sidelines for now.

For further details see:

Confluent: I Remain On The Sidelines For Now