CFLT - Confluent: Rating Downgrade Due To Change In Sales Strategy And Macro Risk

2023-11-15 21:47:58 ET

Summary

- On a standalone basis, 3Q23 earnings were solid, beating revenue estimates and improving profitability.

- The company's shift to a consumption-based sales strategy and increased macroeconomic risks have led to a downgrade from a buy rating to a hold.

- Confluent's growth outlook for 2024 has been reduced to 22%, which is lower than my >30% assumption.

Summary

Readers may find my previous coverage via this link . My previous rating was a buy, as I believed Confluent ( CFLT ) would continue to grow at more than 30% for the foreseeable future. I am revising my rating to a hold due to the sales strategy change, heightened macro risk, and weak forward guidance.

Comments

CFLT 3Q23 earnings were alright on a standalone basis. Revenue grew 32% to $200.2 million, primarily driven by the Confluent Platform, outperforming consensus estimates. Profitability also came in better than expected. Adjusted gross margin reached 76.4% at $152.9 million, and adjusted EBIT margin improved to -5.5%, which was way above management guidance of -10%.

While the results were alright from a standalone basis, the stock saw a massive drop of >30% post-earnings. At a high level, I think there are 3 key reasons that drove this, and unfortunately, they have also forced me to downgrade my rating to hold, as the fact is that CFLT growth will be pressured in the near term.

To begin, the management team has made the decision to shift its cloud go-to-market [GTM] strategy to a fully consumption-based model, which is expected to better align the company's customers and sales force based on actual usage rather than the current upfront commitment model. As a result, the pipeline is going to be filled with more new customer logos and workloads. For starters, this is a massive change. It is a very different strategy from the expansion strategy, where CFLT targets its existing group of customers, which has a lower cost as CFLT already has a direct relationship with these customers. Starting in 1Q24 and concluding in FY24, CFLT will switch to a model in which all cloud sales compensation is based on incremental consumption and new logo acquisition, as opposed to the current model, in which only 10–15% of cloud sales compensation is consumption-based. My worry is the cost associated with this transition, which is going to cause huge volatility in FY24 financials.

- Remember that the majority of CFLT customers are still under the committed contract, and the management strategy to convert them is by offering discounts (which hurts profitability).

- As the GTM strategy has changed to focus on new logos, CFLT will need to hire more sales personnel, which is going to blow up the cost structure in the near term until these sales personnel deliver. Since it typically takes some time for a new sales team to mature, near-term profitability is definitely going to be impacted.

- The new product structure would also mean that CFLT needs to step up its R&D investments to align the products in order to reduce any friction in usability.

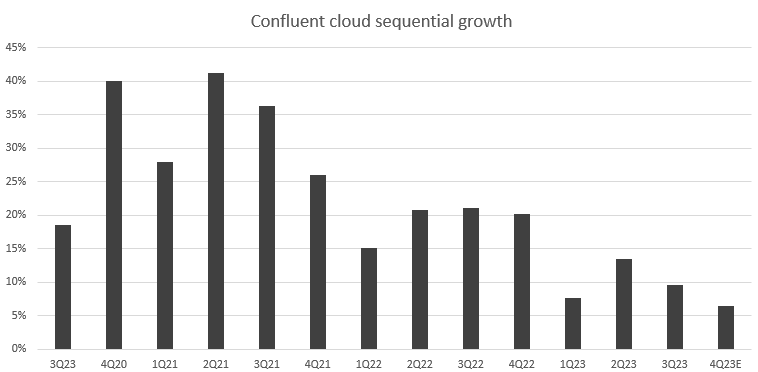

Secondly, while Confluent Cloud continues to be the fastest growing part of the business, growing 61% y/y in 3Q, management now expects Cloud revenue in 4Q to slow down to 43% y/y growth. This is a drastic decline from the 61% seen in 3Q, and sequential growth is only expected to slow further.

{kind=link}

Additionally, Cloud revenue is now expected to account for 48% of total revenue moving ahead, down from the previous guidance of 48–50%. What this means is that the growth contribution from Confluent Cloud will be less in the coming quarters, which again is a headwind to growth. Growth headwinds are appearing from CFLT’s major customers as well, where one of the customers has moved workloads back to open-source Kafka in their own data center and another customer is ramping slower as they are in the process of being acquired.

Additionally, it appears that a few other key US digital native clients are seeing slower organic consumption as well, which had a slight impact in Q3 and is projected to have a larger impact in Q4. Lastly, geopolitical conflict has found its way to hurt CFLT growth outlook (Israel is a top 10 country for the CFLT and it is currently in major conflicts with neighboring countries).

“Second, the continuing macro pressure, including the ongoing conflict in the Middle East, where Israel is a top 10 country for us, and the possible U.S. government shutdown, both of which add uncertainty and disruption in particular segments.” Source: 3Q23 earnings

The equity story of CFLT has been considerably impacted in the near term by the combination of slower consumer trends amidst a turbulent macro environment and probable disruptions in the business from the switch to consumption-based sales compensations. The uncertainty was confirmed via management guidance, where the early 2024 growth outlook landed well below my previous assumptions. The new growth forecast from management is 22% for 2024, a significant reduction from my original projection of >30%. It is difficult to model the company at this time due to the modified GTM model and increased consumer/macro risk. As a result, I am shifting my rating to "hold" while I monitor the change over the coming quarters.

Conclusion

The shift in sales strategy towards a consumption-based model, coupled with macroeconomic uncertainties, has led to a downgrade from my prior buy rating to a hold. Management’s growth forecast for 2024, now at 22%, significantly deviates from my assumption of over 30%. Importantly, the new sales strategy and increased risks make it challenging to model the company accurately at this juncture. As I monitor these changes in the upcoming quarters, I recommend a hold rating (neutral) until there's clearer visibility on these transformative shifts.

For further details see:

Confluent: Rating Downgrade Due To Change In Sales Strategy And Macro Risk