CFLT - Confluent Sees Slower Sales Cycles As High Operating Losses Continue

2023-03-31 13:49:36 ET

Summary

- Confluent, Inc. reported its Q4 2022 financial results on January 30, 2023.

- The firm provides data streaming software and services worldwide.

- Confluent has grown quickly, but like so many tech companies it has generated high operating losses, and this has been punished in an increasing cost of capital environment.

- With management guiding to slower growth in 2023 and seeing longer sales cycles, I'm on Hold for Confluent, Inc. until we see a meaningful move toward GAAP operating breakeven.

A Quick Take On Confluent

Confluent, Inc. (CFLT) reported its Q4 2022 financial results on January 30, 2023, beating revenue and EPS consensus estimates.

The firm has created a platform providing data infrastructure that speeds data communications across the enterprise.

While CFLT is a fast-growing company in a promising industry, its operating loss profile means the market will likely continue to punish its stock, especially given slower growth ahead.

I'm therefore on Hold for the stock until Confluent, Inc. can make meaningful progress toward GAAP operating breakeven while retaining a strong growth trajectory.

Confluent Overview

Mountain View, California-based Confluent, Inc. was founded in 2014 to create a platform enabling companies to more easily build and deploy data-driven applications for real-time use.

Management is headed by co-founder and CEO Jay Kreps, who was previously a software architect at LinkedIn and was one of the creators of Apache Kafka, which Confluent uses as the basis for its system.

The company's primary offerings include:

-

Confluent Cloud - SaaS platform

-

Confluent Platform - Self-managed system

-

Kafka Connect - Data hub.

The firm pursues relationships primarily with large and medium-sized companies through a direct sales and marketing approach.

Confluent has customers across numerous industries including financial services, retail and ecommerce, manufacturing, government, gaming, insurance, communications and media & entertainment.

Confluent's Market & Competition

According to a 2022 market research report by Market Research Future, the global market for event stream processing (as a proxy for the larger data streaming market) was an estimated $790 million in 2022 and is forecast to exceed $2.4 billion by 2030.

This represents a forecast CAGR of 12.86% from 2023 to 2030.

The main drivers for this expected growth are a growing demand for real-time analytics, increasing desire by businesses to analyze their data stores, the continued transition of enterprises to cloud applications and the need to drive efficiencies across all aspects of the enterprise.

Also, as companies transition to cloud infrastructures, their systems are becoming more complex and there is a substantial need for vendor reduction to improve integration and lower complexity.

Major competitive or other industry participants include:

-

IBM

-

Aiven

-

Oracle

-

SAP

-

StreamSets

-

Striim

-

Imply

-

Coralogix

-

Ververica

-

StarTree

-

Materialize

-

Crosser

-

Quix

-

Lenses

-

BangDB.

Confluent's Recent Financial Results

-

Total revenue by quarter has risen markedly, as the chart shows here:

Total Revenue (Seeking Alpha)

-

Gross profit margin by quarter has trended higher in recent quarters:

Gross Profit Margin (Seeking Alpha)

-

Selling, G&A expenses as a percentage of total revenue by quarter have trended lower more recently, a good sign:

Selling, G&A % Of Revenue (Seeking Alpha)

-

Operating losses by quarter have worsened substantially recently:

Operating Income (Seeking Alpha)

-

Earnings per share (Diluted) have remained significantly negative, as shown below:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP.)

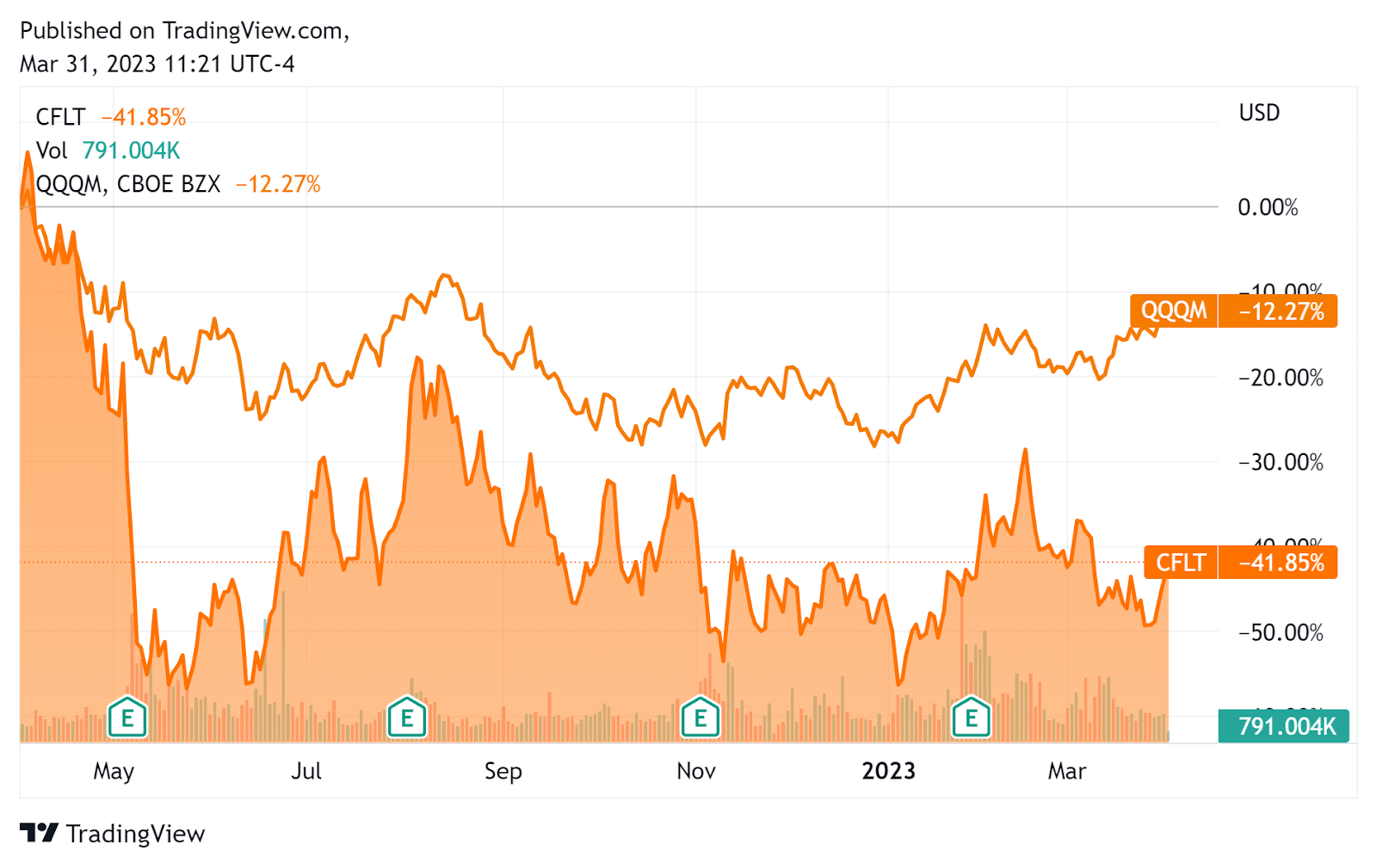

In the past 12 months, CFLT's stock price has fallen 41.9% vs. that of the Nasdaq 100 Index's drop of 12.3%, as the chart indicates below:

{kind=link}

As to its Q4 2022 financial results, total revenue grew 40.7% year-over-year and gross profit margin increased by 6.3 percentage points.

SG&A expenses as a percentage of total revenue trended lower, indicating increasing revenue gains from each dollar of SG&A spend.

However, operating losses have been worsening sharply as have negative earnings per share.

The company's dollar-based net retention rate was 'just under 130%', indicating very good product/market fit and strong sales & marketing efficiency.

For the balance sheet , the firm ended the quarter with cash, equivalents and short-term investments of approximately $1.9 billion and long-term debt of $1.08 billion.

Over the trailing twelve months, free cash used was a hefty $161.4 million, of which capital expenditures accounted for only $4.1 million. The company paid a very high $277.7 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Confluent

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 9.5 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 10.5 |

| Revenue Growth Rate |

| 51.1% |

| Net Income Margin |

| -77.2% |

| GAAP EBITDA % |

| -77.5% |

| Market Capitalization |

| $6,370,000,000 |

| Enterprise Value |

| $5,560,000,000 |

| Operating Cash Flow |

| -$157,330,000 |

| Earnings Per Share (Fully Diluted) |

| -$1.61 |

(Source - Seeking Alpha.)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

CFLT's most recent GAAP Rule of 40 calculation was negative (26.4%) as of Q4 2022's results, so the firm has performed poorly in this regard due to its high operating losses, per the table below:

| Rule of 40 - GAAP |

| Calculation |

| Recent Rev. Growth % |

| 51.1% |

| GAAP EBITDA % |

| -77.5% |

| Total |

| -26.4% |

(Source - Seeking Alpha.)

Future Prospects For Confluent

In its last earnings call ( Source - Seeking Alpha ), covering Q4 2022's results, management highlighted recent results exceeding its previous guidance.

However, leadership is seeing increased sales cycles as companies exert greater scrutiny on new deals in a slowing or uncertain macroeconomic environment.

In response, management has made a decision to reduce its workforce by 8%. It believes with these changes and a 30% revenue growth trajectory in 2023, it can achieve a non-GAAP operating margin of negative 14.5% by the end of the year.

Note that adjusted EBITDA doesn't include stock-based compensation. In CFLT's case, that has been a very large number, handing out $278 million in stock as compensation. In GAAP terms, the company will still be generating highly negative earnings.

The company's financial position is strong, with a lot of cash and investments, net of debt.

Regarding valuation, the market is valuing CFLT at an EV/Sales multiple of around 9.5x.

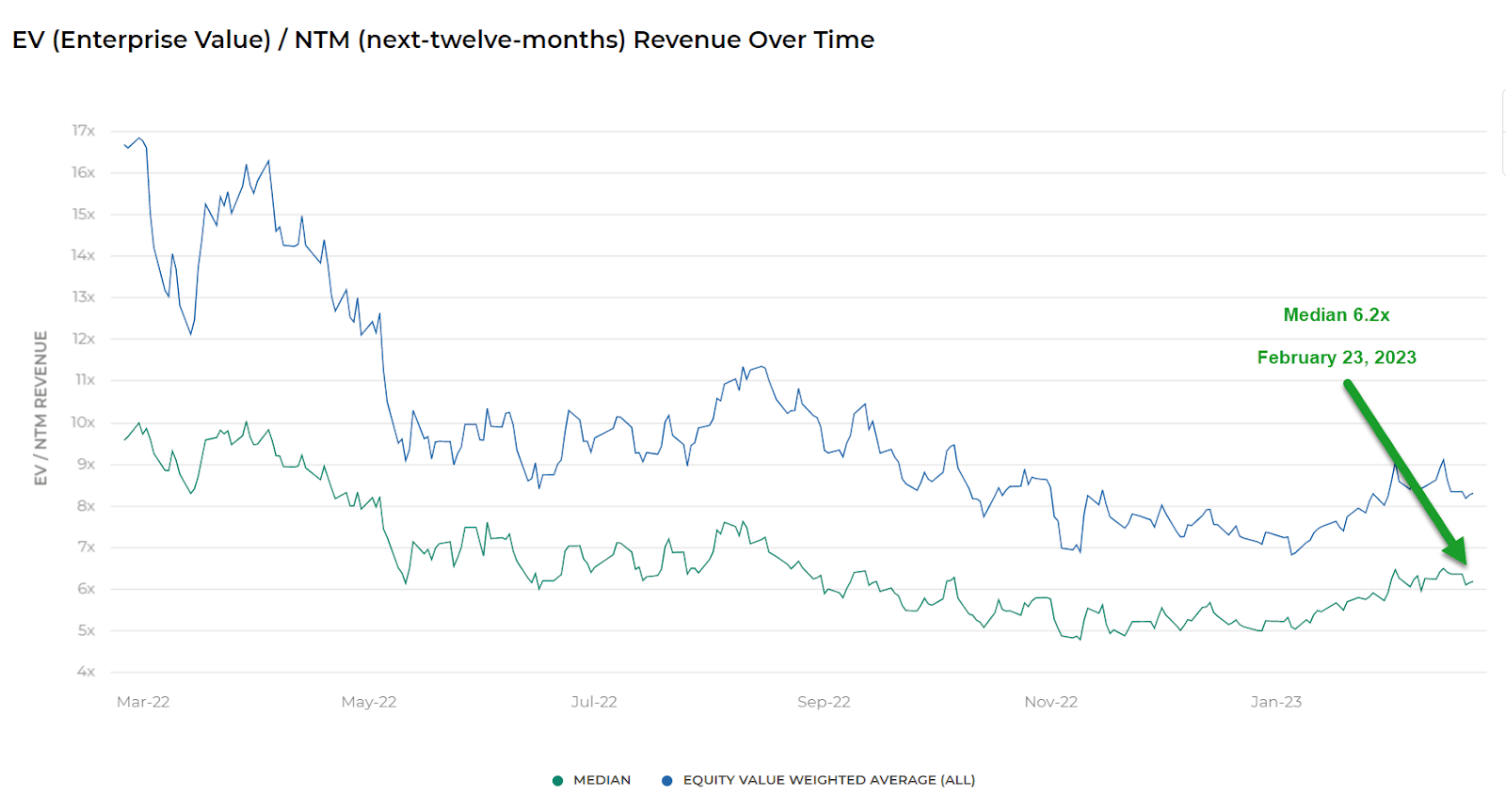

The Meritech Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 6.2x on February 23, 2023, as the chart shows here:

Enterprise Value / Next 12 Month Revenue Index Multiple (Meritech Capital)

{kind=link}

So, by comparison, CFLT is currently valued by the market at a substantial premium to the broader Meritech Capital SaaS Index, at least as of February 23, 2023.

The primary risk to the company's outlook is an increasingly likely macroeconomic slowdown or recession, which may accelerate new customer discounting (although it hasn't led to this just yet for the company), produce slower sales cycles and reduce its revenue growth trajectory.

A potential upside catalyst to the stock could include a pause in interest rate hikes and a potential drop in terminal rate assumptions, leading to improvement in its valuation multiple.

However, at 30% revenue growth, that indicates a slowing growth trajectory for 2023 versus 2022.

While CFLT is a fast-growing company in a promising industry, its operating loss profile means the market will likely continue to punish its stock, especially given slower growth ahead.

I'm therefore on Hold for Confluent, Inc. until it can make meaningful progress toward GAAP operating breakeven while retaining a strong growth trajectory.

For further details see:

Confluent Sees Slower Sales Cycles As High Operating Losses Continue