CFLT - Confluent: Streaming To Success

2023-09-21 06:45:42 ET

Summary

- Confluent's Data Streaming Platform should give it a significant competitive advantage and a barrier to entry.

- The Data Streaming Platform has several integrated components that will lead to greater engagement and monetization.

- Confluent had an excellent first half performance in a difficult environment.

- While the valuation is a little stretched, it's a great company to buy on declines for the long term.

I had analyzed Confluent (CFLT) in February, at $25, planning to buy on declines, around $20. My patience paid off as I managed to buy between $20 and $21.

Here is a summary of the major reasons from my earlier article for buying the stock.

The demand for real time, low latency data streams from IoT, Ad-Tech, and Autos to name a few, is only going to get greater and Confluent has the best cloud platform to constantly stream it at scale, enhance, maintain, and provide analytics for it. Confluent does have large competitors, Amazon's (AMZN) AWS, Microsoft's (MSFT) Azure and Alphabet's (GOOG) Google Cloud have their own managed data streaming products as do some of the legacy on premise providers such as Tibco Streaming, Red Hat, part of IBM (IBM) and Oracle (ORCL). Of course, open-source Kafka, upon which Confluent built its own product, remains the free alternative. However, none have the focus, scale, rich features, implementation, integration, support, and cost savings, that Confluent does. Besides, Confluent having an agnostic platform has partnerships with the CSP's filling in their data streaming product needs or bringing them customers for storage and processing. Confluent also serves all markets, cloud, hybrid and on-prem with a focus on their cloud native subscription platform, which is growing at 83% and is their best bet for sustainable and recurring revenue streams.

Right now, the stock is around $31-32, after briefly reaching $40-$41 during the AI hype in July. Confluent's first half performance confirmed all the positives of the company; hence, I think it's worth accumulating more. Let's take a deeper dive.

First half 2023

Confluent continued with good growth in the first half of 2023. All the metrics below were solid.

Confluent First Half Metrics 2023 (Confluent, Fountainhead)

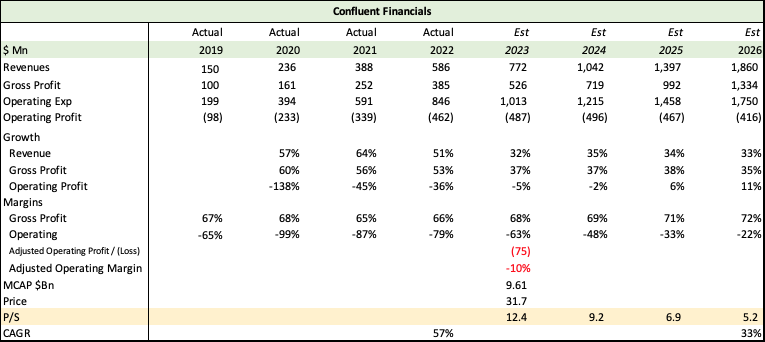

Revenues grew 37% YoY, aided by massive growth in Cloud platform revenue of 83%. The Cloud platform is the backbone of their business, getting sustainable and recurring subscription revenue. It is a great SaaS land and expand strategy with 130% Net Revenue Retention with a gross retention rate of about 90%. The cloud platform has an NRR of 140%. On Premise license revenues also surprised to the positive with growth over 16%.

The other big pluses were the improvement in margins, with single digit improvements in gross GAAP and adjusted margins, resulting in a 50% improvement in adjusted operating losses. Currently, the adjusted OPM is down to -16% and Confluent has guided to -10% for 2024, promising to break even on an adjusted basis in Q4. Clearly, they realize that in a choppy and difficult environment, focusing on reining in costs is crucial, and for the first half the biggest improvements came through lower sales and marketing expenses. Of course, Confluent is far from GAAP positive with a humongous $171Mn of Stock Based Compensation in 1H2023, nor is it generating operating cash - but it is a step in the right direction. Large clients over $100,000 in ARR also grew well with a 33% YoY increase, as did the 147, over 1 clients with an even more impressive 48% growth. Clearly, they met and exceeded guidance as well.

What makes Confluent stand out?

Best in Class Product : Even though AWS, Azure, and Google Cloud are strong competitors, they don't have the core functionality or rich features, integration, and breadth that Confluent does. A Comparison of the products revealed 26 integrations for Confluent Versus 9 and 10 for the rest, much wider deployment and stronger support and training.

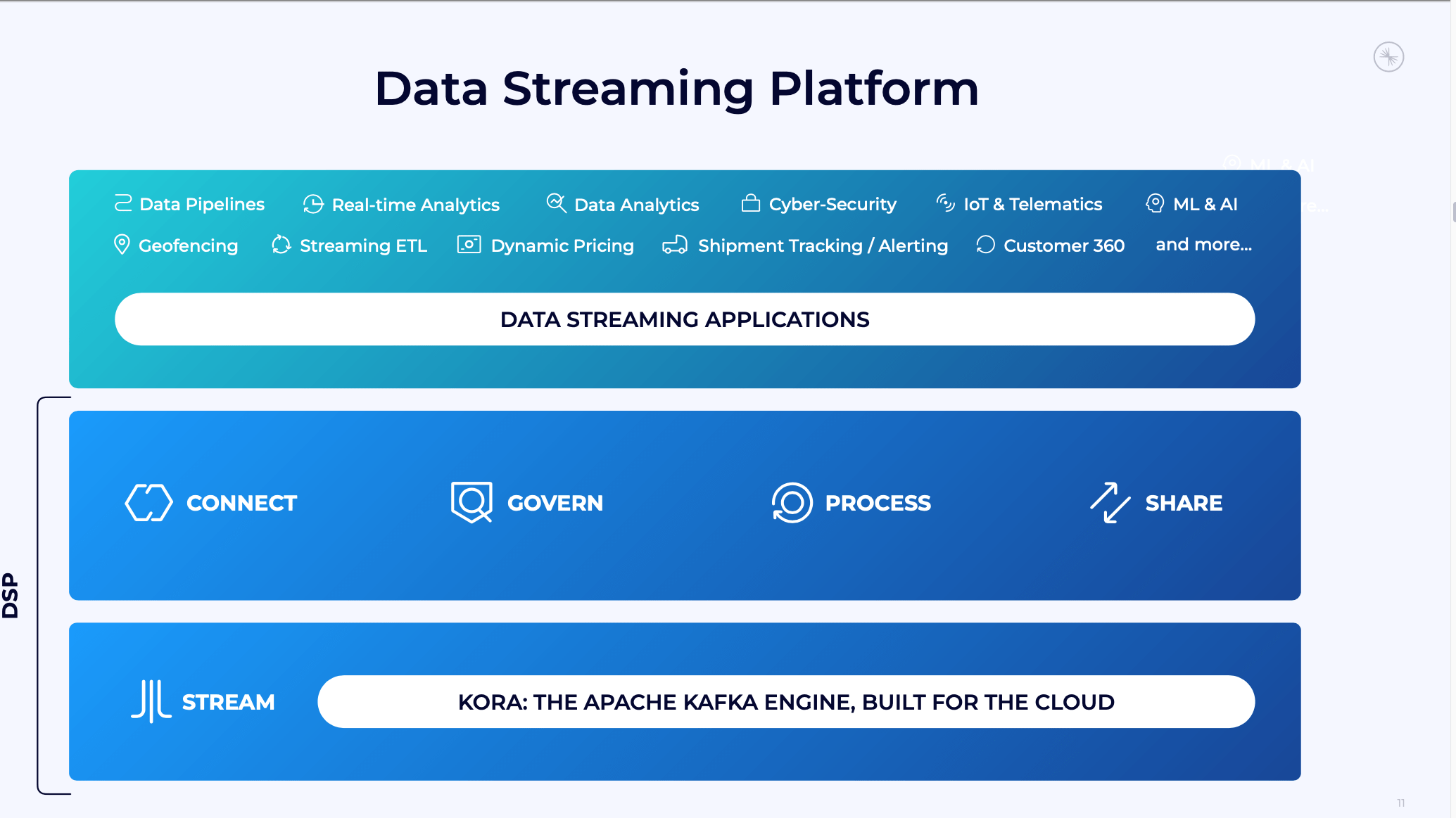

Integrated Data Streaming Platform: Management outlined several new aspects and growth drivers, and the build out of a comprehensive DSP (Data Streaming Platform) stood out. Given the massive $60Bn Total Addressable Market , and the speed at which data streaming is moving, a comprehensive best in class platform at scale is a necessity, and building it gives them a big competitive advantage.

{kind=link}

With Kafka as the foundation, the DSP does a lot more than just stream data, it uses 5 integrated processes of streaming, connecting, governing, processing, and sharing. All these components, including the non-Kafka ones can be monetized and Confluent has started Freemium licensing/subscriptions to increase engagement and revenue. Using Apache Flink, it's also increasing engagement and monetization for stream processing, governance and sharing from customers like Netflix ( NFLX ) and Instacart ( CART ). For example, revenue from the Stream Governance Advanced Offering was their fastest product grower ever. Their stream processing offering should be available next year. The stream sharing offering would be very valuable to the finance, insurance, and travel insurance industries, which need to share data with providers and customers.

Here are two examples from C.E.O. and CO-Founder, Jay Kreps from the Q2 conference call:

Meesho is a high growth Indian e-commerce company who last year was one of the most downloaded shopping apps in the world. It was the fastest shopping app to cross 500 million downloads and regularly sees huge traffic spikes that see over 1,000,000 requests per second. Kafka is used broadly across Meesho's business including its real time recommendation engine to deliver great user experience for customers and sellers. But manually configuring and tuning open-source Kafka wasn't aligned with their overall push for sustainable solutions and driving business efficiencies. So, they migrated to Confluent Cloud. Confluent now processes its shopping transactions and is a key part of the architecture that delivers exceptional experiences for its buyers and sellers.

Recursion Pharmaceuticals is a leading biotech company that uses advancements in AI and biology to accelerate and industrialize the discovery of new drugs. Traditional drug discovery is often slow and expensive, relying on manual bespoke processes and experiments influenced by human bias. Recursion, on the other hand, runs over 2 million experiments per week to generate a massive biological and chemical data set to train machine learning models that discover new insights beyond what is known in scientific literature.

Confluent is the backbone stream infrastructure for experimental data that feeds their AI models, with more than 23 petabytes of real time biological and chemical data improving the predictions of the models.

Besides the increased engagement and monetization of integrated components and modules, the main strength of this strategy is providing an integrated streaming platform , which no one has right now. I believe this is a huge competitive advantage that should continue to propel growth for Confluent for at least the next decade.

Buy on declines

Challenges and Weakness: To be sure there are several challenges, and a difficult sales environment with longer sales cycles, reduced and postponed budgets did take a toll in the first half; on average new clients this year have been smaller in size with shorter contracts. A revenue CAGR of 57% in the last 3 years has petered down to a still strong 33% growth in the next 3-4 years. And clearly with estimated SBC of over $350Mn for 2023, Confluent is not going to make profits in a hurry. This will remain a revenue story for a while, with rich valuations for a while. Besides, the constant SBC dilution, there is the overhang of another 11Mn shares from $1Bn in convertible notes.

Platform Development : I would actively cheer the emphasis on platform and product development, when it results in a sustainable competitive advantage, even if some of the capabilities of the DSP only start getting monetized in 2024 and 2025. It would become a strong barrier to entry.

The company is just 8 years old, having been formed in 2015 with an IPO in 2021. There is a tremendous runway of growth still ahead, and having an integrated platform gives them a huge first mover advantage.

Besides, its laudable that they've grown 32% in a difficult year, with customers actually over-consuming smaller contracts, suggesting that there is a lot of product value. A $ based NRR of 130% is very solid.

Confluent Financial Forecast (Confluent, Seeking Alpha, Fountainhead)

{kind=link}

Valuation: The forward P/S ratio is over 9, with high growth of 33% bringing it down to 7 and 5. Like last time, I believe patience will pay off and given the Fed's higher for longer stance and with 10 year treasury yields over 4.4%, valuations are stretched across the board and I don't believe the market is going anywhere. I would buy between $27-29, there is room for a 10-15% drop.

For further details see:

Confluent: Streaming To Success