CFLT - Confluent: The Multiple Will Most Likely Compress

2024-01-16 00:09:51 ET

Summary

- Caution on Confluent due to perceived significant growth rate slowdown.

- Challenges include unexpected shifts in consumption patterns, macroeconomic uncertainties, and potential talent retention issues.

- Despite recent stock rally, skepticism persists, deeming Confluent a "show-me story" not worthy of investment.

Investment Thesis

Confluent ( CFLT ) specializes in data streaming, helping businesses manage and analyze large volumes of real-time data through their platform built around the open-source technology Kafka.

My contention with Confluent is that its underlying growth rates are slowing at a rapid rate. This leads me to have difficulty in confidently extrapolating its growth rates.

Given that this stock isn't particularly cheap to start with, as well as the fact that it's only just profitable, leaves me unwilling to recommend this stock.

Rapid Recap,

In my previous bearish analysis at the start of November, I said,

With revenue growth rates tapering down and the company's shift towards a consumption-based business model, the underlying profitability has come under increased scrutiny. Notably, the stock's current valuation at around 180 times next year's non-GAAP operating profits is exorbitantly high, especially considering the deceleration in its growth trajectory.

Author's work on CFLT

Since I made that call, the stock has rallied strongly by 40% in a few months. Despite being wrong in calling the stock last time, I reiterate my view, that Confluent is a show-me story and not worthy of my capital.

Why Confluent? Why Now?

Confluent is a company that helps other businesses manage and make sense of large amounts of data in real time.

They specialize in something called "data streaming," which is like a constant flow of information rather than dealing with data in chunks. Confluent's main product is built around an open-source technology called Kafka, and they offer a cloud-based service called Confluent Cloud.

Essentially, they provide tools and services that allow companies to process and analyze data as it comes in, enabling them to make quick and informed decisions based on the most up-to-date information.

In the near term, Confluent faces challenges that could potentially impact its financial performance and growth trajectory. Firstly, the unexpected shift in consumption patterns from two major digital native customers, including an online gaming company that relocated workloads back to its own data center and a significant customer experiencing slower ramp-up due to an ongoing acquisition, has led to a substantial shortfall in expected cloud revenue for the fourth quarter. The most important question investors need to form a view on is whether this is temporary or the ''new normal'' (more on its growth rates soon).

Moreover, the slowdown in organic consumption is worthwhile noting as this has been attributed to a deceleration in the rate of new use case additions within the customer base.

Additionally, the macroeconomic landscape poses challenges, with geopolitical tensions in the Middle East, particularly in Israel, a crucial market for Confluent.

Given this background, let's turn to discussing Confluent's growth rates.

Revenue Growth Rates Are the Telling Tale

CLFT revenue growth rates

The reason why I don't support an investment in Confluent boils down to this simple assertion. The business is rapidly decelerating its growth rates. Even if we consider that management is undoubtedly being conservative with its guidance and may end up delivering up to around 25% y/y growth rates in Q4, the fact of the matter remains that there's a clear and consistent deceleration in its top line.

This has two main implications for the business. The first one is less obvious and is down to the retention of top talent. Executives that are highly ambitious and wish to participate in the next big software company are likely to exit a company that is losing its ways. After all, it goes without saying that they too are acutely aware of the underlying growth of the business, oftentimes even more so than investors.

And second, when it comes to investing in stocks, I'll say, this is a game of probabilities. Nobody is always right or always wrong. The game we are playing is one of probabilities and attempting to improve the odds of our game by putting a few key indicators in our favor. Not too many, mind you. Too many indicators and it becomes too noisy.

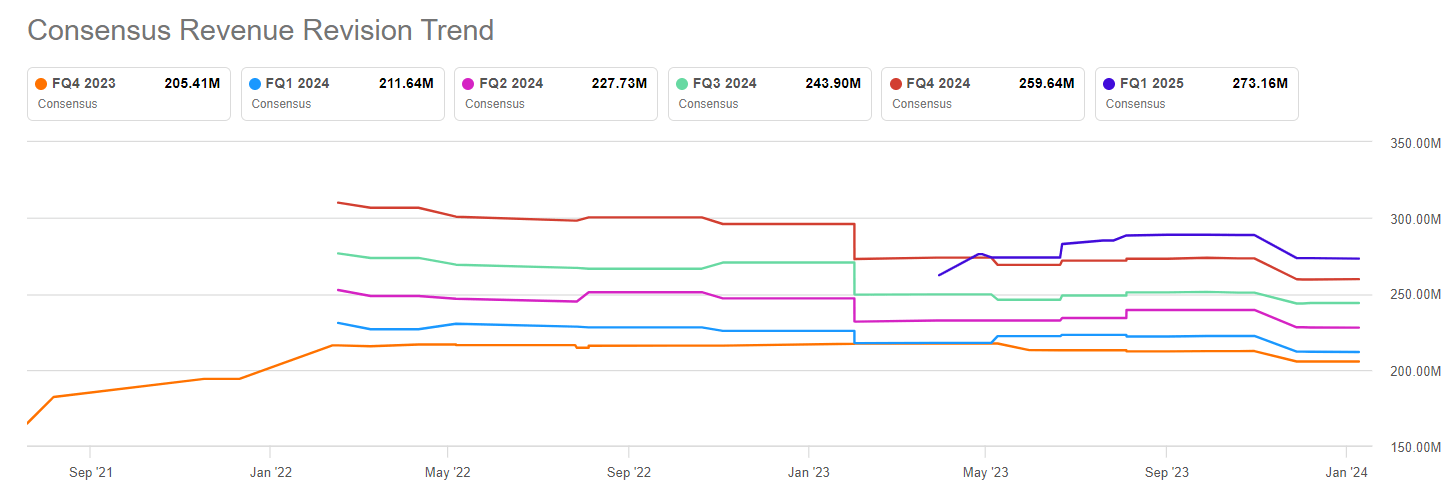

I've found that looking at whether or not the Street views your stock favorably is a helpful indicator of the stock's prospects. With that in mind, consider this graphic.

{kind=link}

As you can see above, in the past 1 year, the Street has reduced its revenue consensus figures. This means that the Street is not out there recommending this stock and pumping the stock higher.

Now, this doesn't mean that the Street is always right. Some companies can reaccelerate their growth prospects. But again, this is a game of odds. And the odds of reacceleration are relatively minor.

Even as the comparables with the prior year have eased up, Confluent is still expecting to deliver decelerating growth rates. Accordingly, as we strive to form a view on 2024, I believe that Confluent will end up delivering sub 30% CAGR in 2024.

What this means in practice is that Confluent is getting to approximately a run-rate of $1 billion of revenues annualized and its growth prospects appear to be fading.

Why am I putting so much emphasis on its growth rates? Because Confluent is a growth stock. And with growth stocks, a lot can be forgiven, provided they deliver strong and consistent revenue growth rates. Because that's what drives the multiple on the stock. With that in mind, let's discuss its valuation.

CFLT Stock Valuation -- 7x Forward Sales

What you can see above is that CFLT's multiple has been under pressure in the past few quarters. For a growth stock, changes in the multiple can have a dramatic impact on the underlying share price appreciation.

The one thing that Confluent should do to support its multiple is turn its focus to proving to investors that the business can be meaningfully profitable in the next couple of years , and then, later down the road, it can once again strive to reignite its growth rates.

As I've made the case already, hiring top executive talent and retaining talent, particularly when it's the culture that they are paid the bulk of their salary with SBC, the company needs to have a healthy stock. Because otherwise, potential employees become dismissive of the company's prospects.

To further complicate matters, Confluent has already been making tremendous improvements in profitability in the past twelve months. More specifically, the guidance for Q4 2023 implies an approximate 22% improvement in underlying profitability relative to the same period a year ago.

This means that the vast majority of the gains in profitability have already been made. Better said, the company has already picked the low-hanging fruit. Making additional meaningful gains in 2024 will be a challenge.

When it comes to tech companies, you are either a growth company or you are not. And if you are not, and the business is only marginally profitable this can see the company's multiple compress even further. In my experience, thinking that a stock is undervalued relative to its peers has never been a key driver of upside potential. After all, cheap stocks can always get cheaper.

Looking out to 2024, let's presume that Confluent can grow by 25% CAGR. This would be slightly higher than the Street expects, at around 22% CAGR. Nonetheless, taking my revenue growth estimates, this would imply that Confluent would be priced at closer to 7x forward sales, rather than 9x forward sales shown in the graphic above. Is that enough margin of safety to get involved with Confluent's stock? I don't believe that's a reasonable assumption. Therefore, given all these considerations, I'm avoiding this stock.

The Bottom Line

In my analysis, I hold a cautious perspective on investing in Confluent due to what I perceive as a significant slowdown in the company's growth rates. I point out challenges such as unexpected changes in consumption patterns from major customers, macroeconomic uncertainties, and potential issues with talent retention stemming from the company's growth trajectory.

Despite a recent surge in the stock, my skepticism remains, and I reiterate that Confluent is a "show-me story" that doesn't seem worthy of investment in my view.

Concerns about the company's decelerating growth with the need to demonstrate meaningful profitability pose challenges. Even if Confluent achieves a 25% CAGR in 2024, I argue that the valuation may lack a sufficient margin of safety for investors.

For further details see:

Confluent: The Multiple Will Most Likely Compress