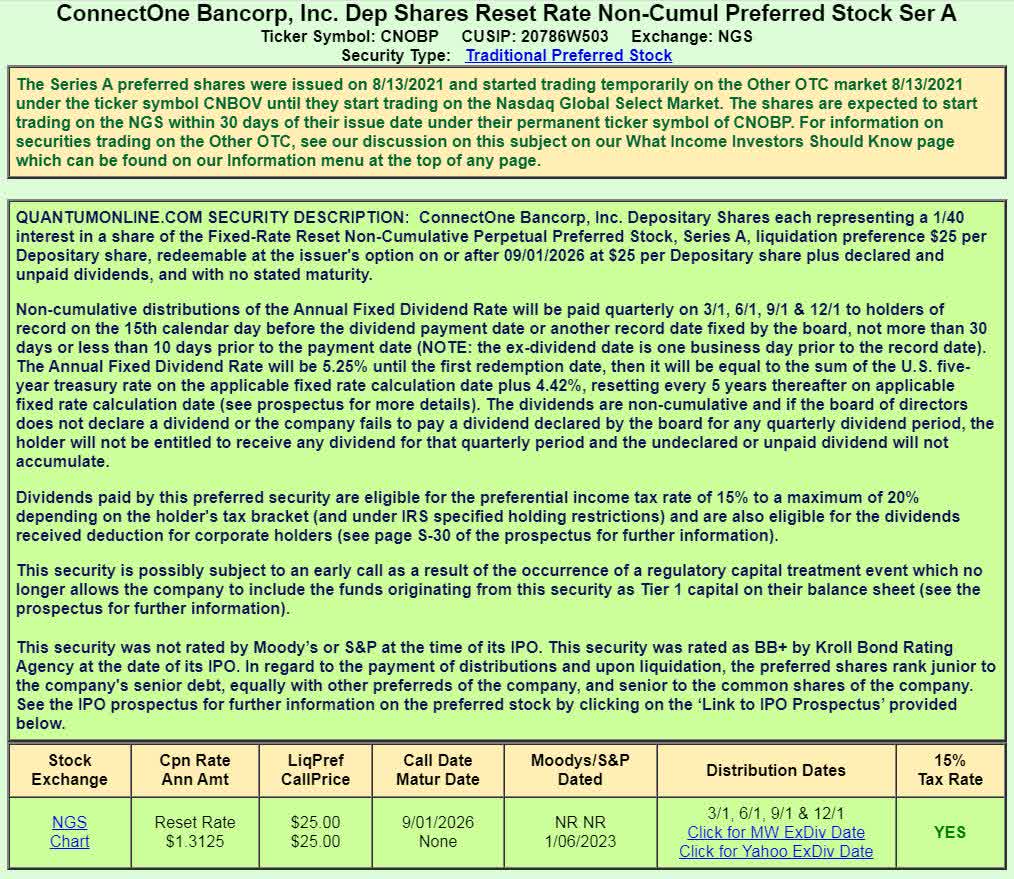

CNOBP - ConnectOne Bancorp: Beat Up Preferred Shares Yielding 8.7%

2023-05-22 08:15:07 ET

Summary

- ConnectOne Bancorp has been caught in the regional bank selloff.

- The bank's preferred shares have also sold off, creating a good income opportunity.

- A look at the bank's strengths and risks has helped affirm my ownership in the preferred shares.

ConnectOne Bancorp ( CNOB ) has been caught in the regional bank selloff. As I have done with the other regional banks, I took this opportunity to evaluate the company’s preferred share offering ( CNOBP ). At a current yield of 8.7% and an attractive reset rate in 2026, ConnectOne’s preferred issue can generate great income if the bank doesn’t become distressed.

{kind=link}

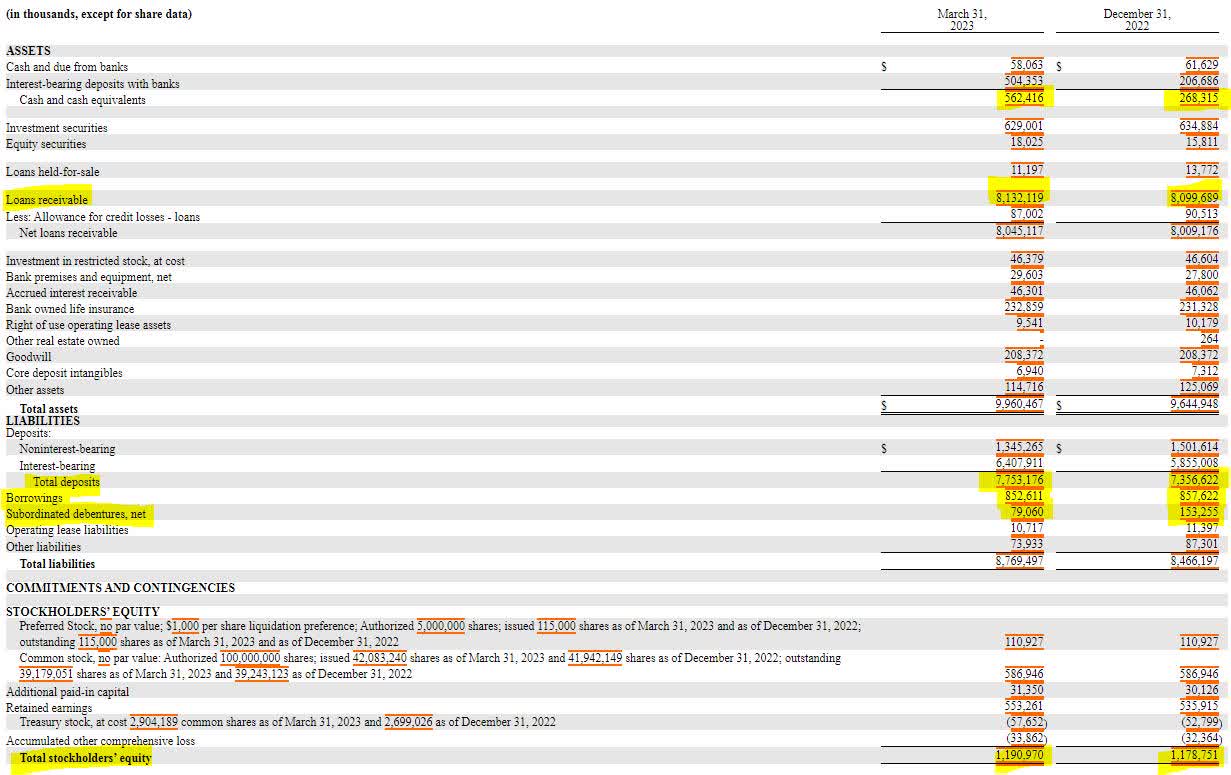

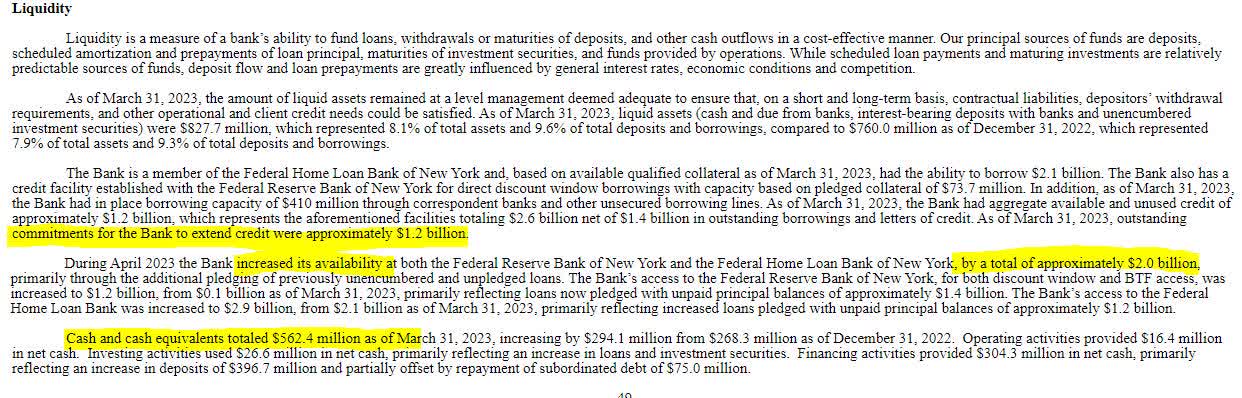

While other banks were losing deposits, increasing their borrowings, and building their cash reserves in the first quarter, ConnectOne increased its deposit base, maintained its short-term borrowings, and paid off nearly half of its debenture debt. The bank also more than doubled its cash equivalents to $562 million. Shareholder equity also inched up by 1% in the first quarter.

{kind=link}

ConnectOne’s preferred dividend obligation is a modest $1.5 million per quarter or $6 million per year. The common share dividend is four times larger and would have to be eliminated in order to remove dividends on preferred shares. Considering that the bank is increasing its deposits and paying down debt while raising cash, I think a suspension of the preferred dividends are highly unlikely.

{kind=link}

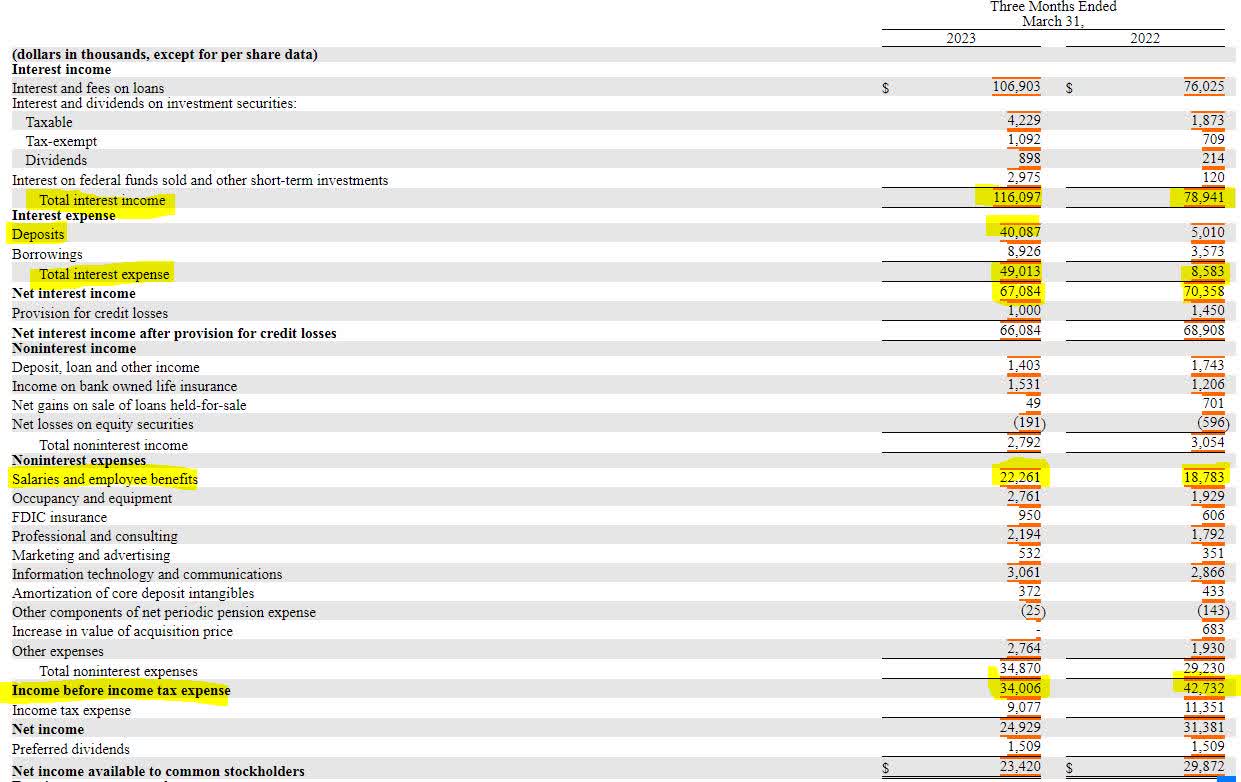

ConnectOne’s profitability slipped modestly in the first quarter compared to the same quarter a year ago. Interest income increased by $38 million, but interest expenses increased by more than $40 million, led by a growth in interest paid on deposits. Ultimately, net interest income fell from $70 million to $67 million for the quarter. After incorporating nonbanking income and expenses (comprised of mostly salaries and benefits), net income declined by $8 million or 20% to $34 million.

{kind=link}

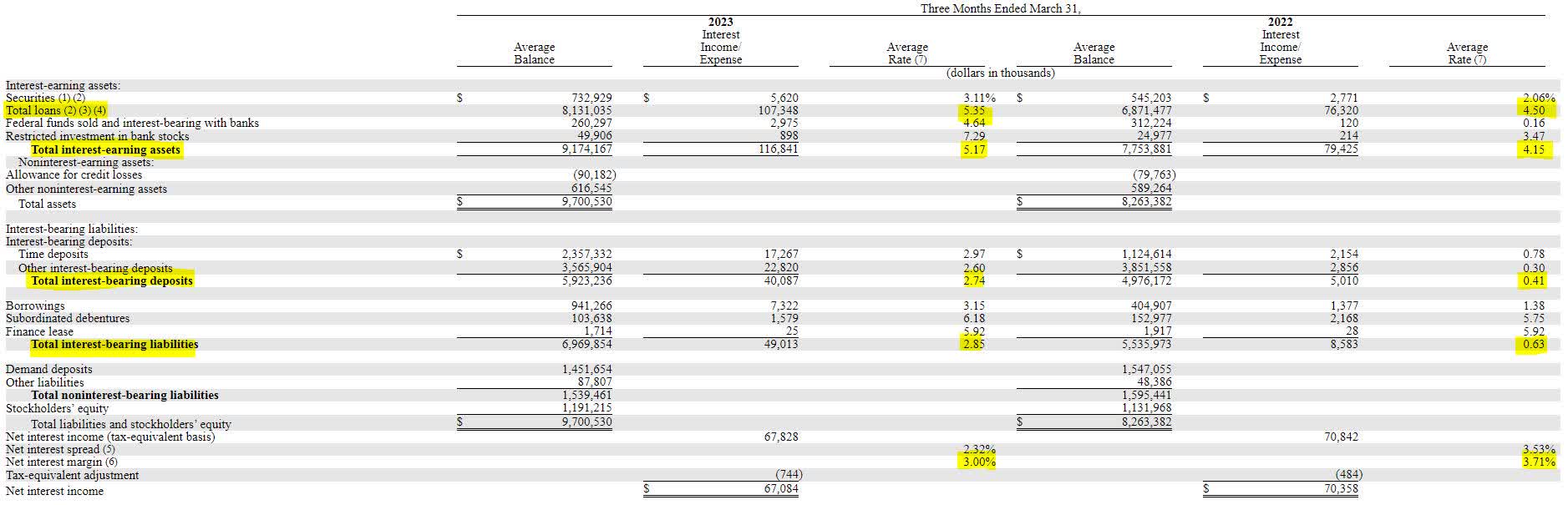

A deeper dive into the bank’s interest income and expenses does reveal some risks. Net interest margin has declined 71 basis points to 3% from a year ago. This decline was driven by an increase of 233 basis points in deposits and a 222 basis point increase in overall interest bearing liability costs. Meanwhile, the average interest rate on loans only rose 85 basis points to 5.35% while overall asset income yields rose slightly better (102 basis points) to 5.17%. The bank’s loans seems to have more fixed rates originating during the 2020-2021 rate drop that it will need to carry through a high rate market.

{kind=link}

When it comes to liquidity, ConnectOne is in good position. With the strengthening of the balance sheet in the first quarter, the bank now has close to $4 billion in liquidity available. This covers more than half of the bank’s total deposits, but more importantly, their liquidity covers the bank’s uninsured deposits 2.5 times over.

{kind=link}

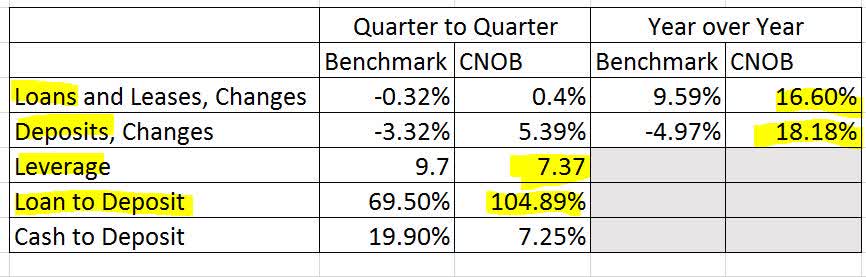

Comparing ConnectOne’s ratios to the entire commercial banking system reveals some interesting observations. First, the bank’s 105% loan to deposit ratio is notably high but it is offset by a reasonable leverage ratio of 7.37 to 1. Loan losses have the potential to increase leverage, but ConnectOne's low leverage has created a sizable capital cushion in place to protect itself.

{kind=link}

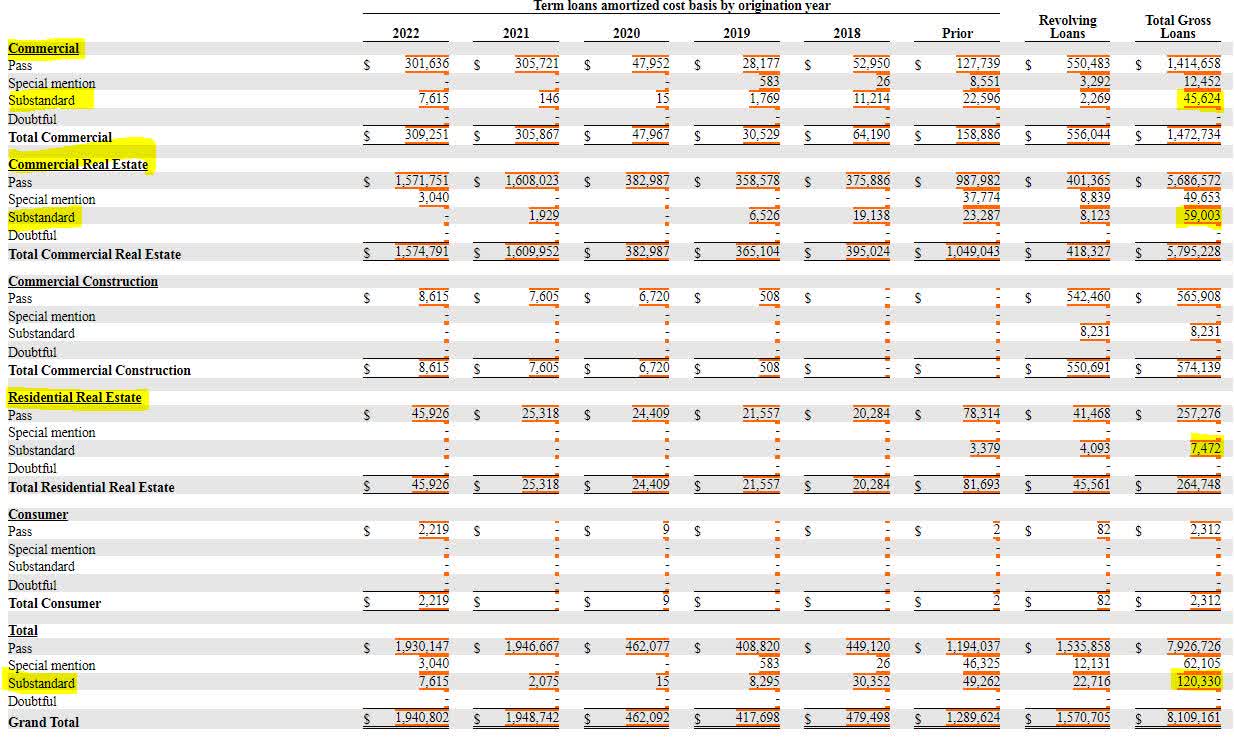

ConnectOne does have exposure to commercial real estate, as it represents a majority of the bank’s total loan portfolio. However, the reality is that these loans are performing well, even better than the bank’s residential real estate portfolio. Substandard loans currently account for 1.5% of the bank’s total portfolio, while commercial real estate’s substandard loans are currently at 1%. Past due and nonaccrual loans are less than half of the bank’s substandard loans.

{kind=link}

{kind=link}

It is important to note that there is a small risk of floating rate decline in the ConnectOne preferred shares when the rate resets in 2026. The new rate will be calculated by the 5 year U.S. Treasury rate plus 4.42%. As long as the five year rate is above 83 basis points, investors should see a dividend increase. If the five year rate rivals today's levels, it will create an incentive for the bank to call in the shares.

ConnectOne Bancorp is not exempt from the risks in the regional banking sector. The bank lent out beyond its deposits and is exposed to the commercial real estate space. But, the low leverage ratio, recent deposit growth, and liquidity growth seems to have isolated the bank from distress. The preferred shares, paying income of 8.7% and trading at 60% of par value represent a good value and income play in this space.

For further details see:

ConnectOne Bancorp: Beat Up Preferred Shares Yielding 8.7%