FANG - ConocoPhillips: Beating Big Brothers Exxon And Chevron

2023-10-31 14:10:02 ET

Summary

- Over the past decade, ConocoPhillips has outperformed Exxon and Chevron in terms of total returns to shareholders, thanks to its focus on efficiency and total returns rather than simply getting bigger.

- The company was early to recognize the value and implications of the shale revolution. It bought shale acreage on the cheap, and sold high-cost assets before others, achieving higher prices.

- ConocoPhillips now has one of the lowest, if not the lowest, cost-of-supply asset bases in the business.

- Today, I'll discuss just how COP ran rings around both Exxon and Chevron over the past decade, and take a preview of the Q3 earnings report, which is due out before the market opens Thursday.

As you know, the U.S. "Big 3" used to be composed of Exxon Mobil ( XOM ), Chevron ( CVX ), and ConocoPhillips ( COP ). All three were international integrated majors with both upstream and downstream operations. Then, on May 1, 2012, ConocoPhillips had the audacity to unleash tremendous shareholder value by spinning off its downstream operations into Phillips 66 ( PSX ). It's been over a decade since the spin, and as the graphic below clearly shows, ConocoPhillips has been running rings around its former peers - delivering total returns almost 50% higher than its much larger big brothers. And that doesn't even include the returns which PSX has delivered for shareholders (384% since the spin).

Which begs the question: How did COP do it?

Investment Thesis

One reason COP has outperformed its big brothers is because, even going back to CEO James Mulva, COP has never been focused on "getting bigger" simply for the sake of "getting big." Instead, the company has always been focused on total returns to shareholder. That being the case, ConocoPhillips had no problem "becoming smaller" by spinning off its downstream (refining, midstream, chemicals) operations into a separate entity because it knew both companies could be more efficient on their own (with some close commercial ties that remain to this day).

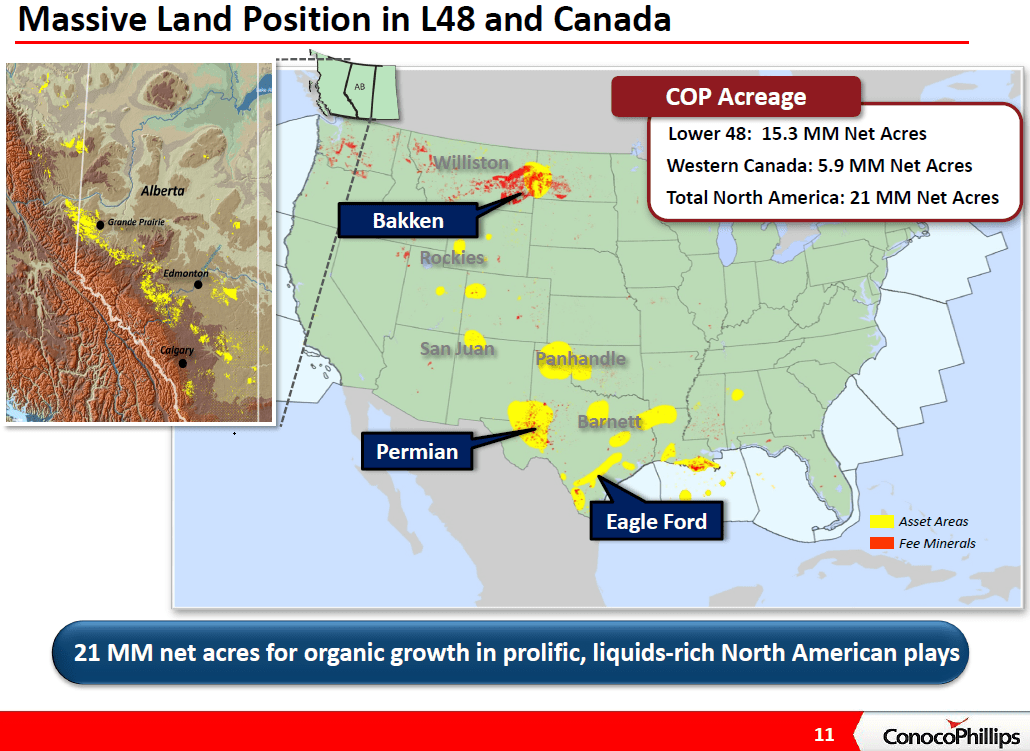

Secondly, COP was arguably much earlier to the shale revolution as compared to both Exxon and Chevron. Now, some may say that COP was lucky and backed into its shale position with its takeover of Burlington Resources for $35.6 billion way back in 2006. Interestingly enough, that takeover was primarily based on growing demand for natural gas (as was XOM's takeover of XTO years later). However, with the BR takeover COP assumed additional acreage in three burgeoning shale plays: The Eagle Ford, the Bakken, and the Permian Basin. By 2012, COP had assembled a huge leasehold in the L-48:

COP's L-48 Leasehold Post Burlington Resources Acquisition (ConocoPhillips)

{kind=link}

COP recognized the value of the Eagle Ford shale early on. Indeed, it grew its footprint in the Eagle Ford at an overall cost of less than $300/acre and by 2012 the company was producing 100,000 boe/d with a cost-of-supply significantly under $40/bbl and with a liquids split near 80%. See my 2012 Seeking Alpha article COP: Exploiting The Eagle Ford Shale .

Next, and unlike its peer Exxon Mobil and its ill-fated XTO acquisition for $60 billion, COP realized that shale gas production, and associated gas production from drillers targeting oil, was going to lead to abundant domestic natural gas production and, as a result, significantly lower prices. That being the case, COP began selling its natural gas properties long before others in the industry recognized the trend, and therefore achieved significantly higher prices for those properties than what they would be worth today. Another example of getting "smaller" in terms of production, but becoming much more cost efficient.

Along those same lines, in 2017 COP made a huge transformation by selling the majority of its Canadian oil sands production to Cenovus ( CVE ) for $10.6 billion in cash, 208 million Cenovus shares (worth $2.8 billion at the time), and a contingency cash payment agreement should WCS trade above ~$39/bbl over the following five years (see COP Sells Major Oil Sands Assets ). It was a grand deal for COP shareholders because despite the loss of 298,000 boe/d of production in the deal, the transaction was actually accretive to shareholders because, as CEO Ryan Lance put it, all the distributions the joint venture paid out had to be sent back to the JV to pay for annual maintenance expenses to keep the tar sands production facilities running. COP took the proceeds, paid down debt, and started buying back its very undervalued stock.

The Key: Low Cost-of-Supply

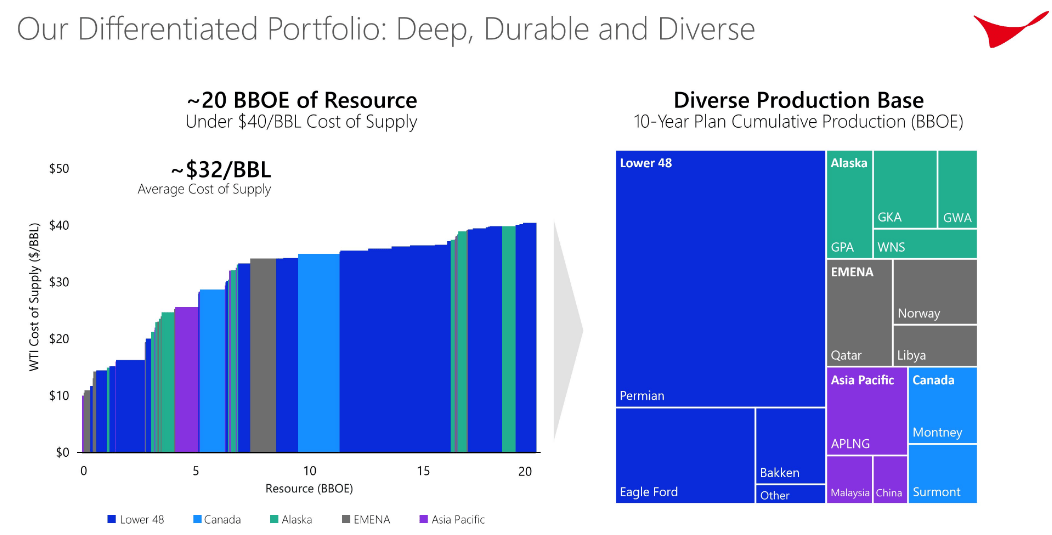

The consistent theme in COP's strategy over the past decade has been to acquire the lowest cost-of-supply assets in the business. That theme was reinforced in spades when the company entered the pandemic year of 2020 with a very strong balance sheet that enabled it to pick-up tier-1 Permian producer Concho Resources as well as the Permian assets of Shell during the commodity price downturn. Today, COP not only has a very strong position in short-cycle L-48 shale acreage, but also a diversified portfolio with strong assets in Alaska, Canada, the North Sea, and Asia. The result, as shown in this slide from an April presentation , is an average cost-of-supply of ~32/bbl:

{kind=link}

Other advantages COP has as compared to Exxon and Chevron:

- COP has also been a leading LNG technology company with a robust licensing program of its Optimized Cascade Process, which has been licensed for use in 27 LNG trains at 12 different locations around the world. Some of these LNG plants are owned by Exxon and Chevron.

- COP has not been investing heavily in large-scale global petchem projects that have been delivering such poor returns for Exxon and Chevron.

- COP has instituted a (base+variable) dividend plan that has been returning a much higher percentage of free cash flow directly to shareholders while Exxon and Chevron have been over-emphasizing share buybacks during a commodity price up-cycle.

Add it all up, and ConocoPhillips - the "little brother" - has been running rings around its big brothers Exxon Mobil and Chevron.

Q3 Earnings Preview

As a result of its low cost-of-supply and the current relatively high commodity price environment, shareholders can expect another strong quarterly report when the company releases Q3 results before the market opens on Thursday.

{kind=link}

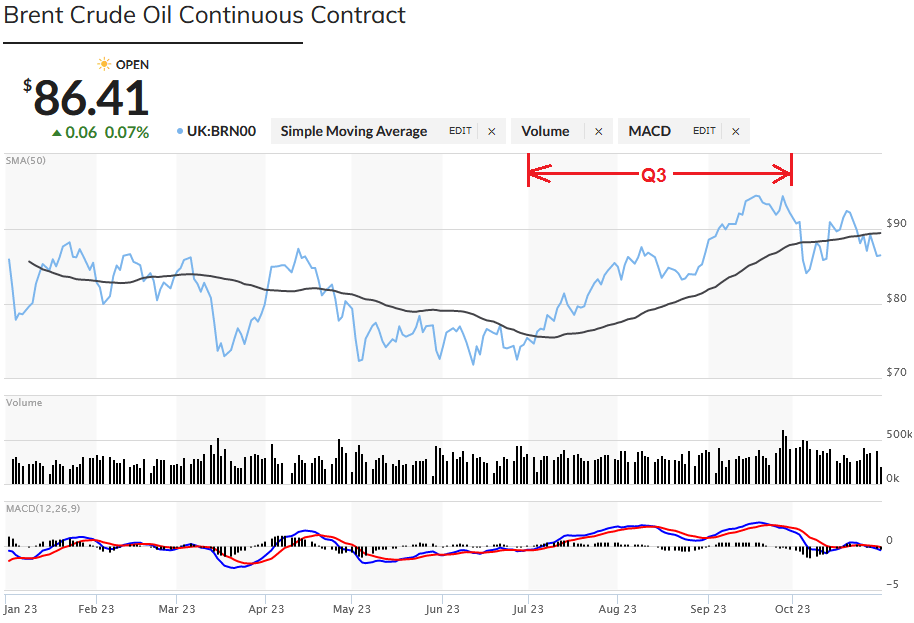

As you can see from the graphic above, Brent rallied sharply during the quarter compared to Q2. In addition, NYMEX gas firmed during Q3 and jumped from $2.84 to $3.77 at pixel time. These moves in O&G prices bode well for even stronger results in Q4.

For now, and according to Yahoo Finance , the analysts' consensus estimates for Q3 are for revenue of $14 billion and EPS of $1.97/share:

Yahoo Finance

While that would obviously be lower than the $3.60/share COP earned in Q3 of last year when commodity prices rallied strong due to Putin's horrible war-of-choice on Ukraine, it would be $0.13/share higher on a sequential basis. Perhaps more importantly, investors may be watching for acquisition synergies, an improvement in COP's free cash flow margin, and what the variable dividend declaration will be (Q2's variable dividend was $0.60/share). If COP is planning on making an acquisition, I suspect there will be no increase in the variable dividend.

On a full-year FY23 basis, the current analysts' consensus earnings estimate is EPS of $9.81/share, which at pixel time would equate to a TTM P/E of only 8.3x.

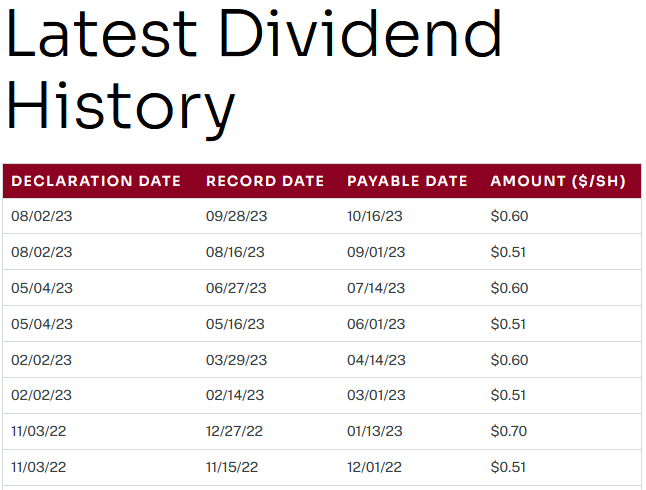

Over the past year, the variable dividend has been significantly higher than the base dividend of $0.51/share:

{kind=link}

Total dividends paid over the past four quarters equate to $4.54/share, or a yield of 3.9%. Note that is more than double what the typical financial media sites reports, which is usually based only on the base dividend. For instance, Seeking Alpha currently reports COP's dividend yield as 1.73%.

Risks

COP has a strong investment grade balance sheet , ending Q2 with $6.8 billion in cash and total long-term debt of $14.4 billion. No doubt the company will have added to that cash position during Q3.

Over the short-term, there is considerable talk that COP needs to make an acquisition in order to compete in the Permian with the size-n-scale of Exxon - which recently agreed to buy Pioneer Resources ( PXD ). The obvious hole in that argument is that COP had Permian production of 709,000 boe/d in Q2, which ranks the company in the top-5 producers in the play, and only an estimated ~70,000 boe/d less than Chevron is producing. Given COP's substantial Permian inventory due to the Concho and Shell acquisitions, and combined with its shale production in the Eagle Ford and Bakken, I'd argue that COP is already very well positioned.

That said, analysts think COP should make a deal. Exhibit No. 1 is a recent Barron's article: COP Should Buy An Oil Company After Chevron/Hess Deal ). That piece cited Diamondback Energy ( FANG ) and Matador Resources ( MTDR ) as possible targets, and rumors are swirling that COP is interested in making a bid for private Permian company CrownRock, which is also reportedly being studied by Devon Energy ( DVN ) and Marathon Oil ( MRO ), among others. As I recently opined, I don't think COP will get into a bidding war for CrownRock and instead is likely to focus on FANG (see Why Diamondback Energy Will Be The Next Permian M&A Target ), which is larger than the other players could swallow. Regardless, any acquisition by COP during an up-cycle like the one we are currently in will likely, in my opinion, be viewed somewhat negatively and would be a departure from the company's historical laser-focus on low cost-of-supply strategy and buying assets in down-cycles.

Summary and Conclusion

ConocoPhillips' long-term strategy of focusing on cobbling together what is arguably the lowest cost-of-supply asset base in the business has been a boon to its shareholders. Indeed, COP has delivered total returns that have run rings around its much bigger former peers Exxon and Chevron - and that's true over the past decade and even after the PSX spin-off, which in and of itself unleashed tremendous shareholder value.

I maintain my Hold rating on ConocoPhillips as I do believe CEO Ryan Lance is looking to make an acquisition. Unfortunately, this will be a departure from his historical track record of making timely assets sales and acquisitions. Yet as I have written in the past on Seeking Alpha, the only possible rationale for COP not paying out more of free cash flow directly to shareholders in the form of dividends (ala shale peers PXD and EOG Resources ( EOG )) is because he wants to keep the balance sheet uber-strong in order to enable another relatively large acquisition. And that could come sooner rather than later.

For further details see:

ConocoPhillips: Beating Big Brothers Exxon And Chevron