FANG - ConocoPhillips: Refuting The Mizuho Downgrade

2023-04-18 10:32:33 ET

Summary

- ConocoPhillips stock dropped $2.89 (2.7%) Monday due to a relatively weak energy sector but also primarily because of a Mizuho downgrade.

- After Mizuho analyst Nitin Kumar viewed COP's apparently compelling Analyst Day Presentation last week, he then listed a few reasons why it really wasn't.

- Yet Kumar's reasoning seems flawed, in my opinion. While there may be "better opportunities" in the energy sector, Mizuho's "Top Picks" don't appear to be among them.

- For example, Mizuho prefers Exxon over ConocoPhillips. However, COP has a much higher TTM yield, trades at a significant discount and, I would argue, has a superior management team.

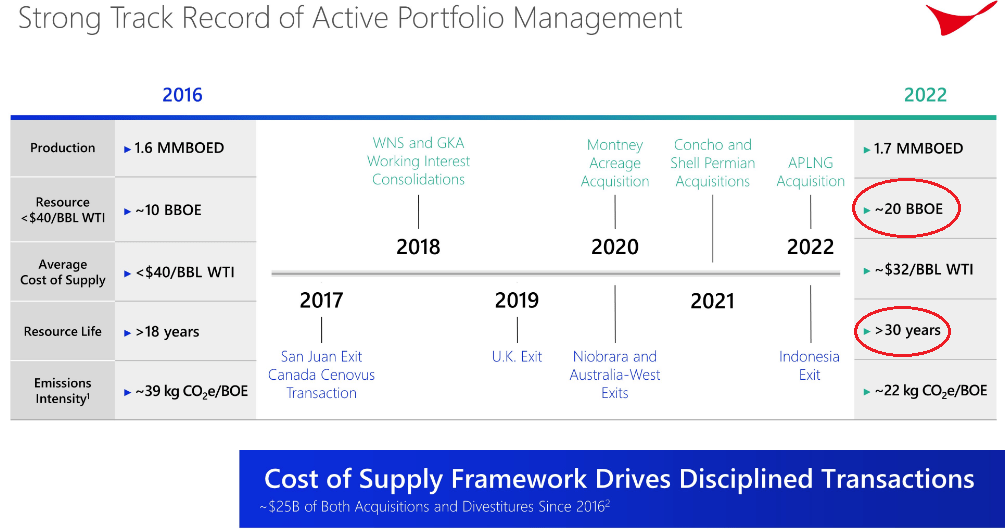

ConocoPhillips (COP) gave its 2023 Analyst & Investor Meeting last Wednesday (you can view the slides here ) and it was - in my opinion - quite compelling. It was a generally very upbeat meeting and showed that the company, through two acquisitions during the pandemic down-cycle (Concho Resources and Shell's Permian assets), has solved a long-standing criticism ever since it sold the majority of its oil sands to Cenovus (CVE): A lack of long-term inventory. The company now has a 20 billion boe resource base with an estimated life of 30+ years. Better yet, it is a tier-1 low-cost-of-supply inventory that has a ~$32/bbl WTI breakeven price (see graphic below). Note that COP's resource base of <$40/bbl WTI resource doubled from 2016 to 2022 (from ~10 to ~20 billion boe). Yet the stock was down $2.89 (2.7%) Monday after a Mizuho downgrade that I have some issues with. Let's take a closer look.

{kind=link}

Mizuho's Take

Seeking Alpha reported that Mizuho's energy analyst Nitin Kumar downgraded COP to Neutral from Buy (note that as recent as Feb. 6 of this year, Kumar put a Buy on COP with a $150 price target ). Kumar said COP's cash generation is weighted to the latter years (2029-32) and that the company's plan assumes "consistency of Permian well productivity and higher commodity prices."

COP does assume "consistency of Permian well productivity" in its projections, but as Nicholas Olds, COP's EVP of Lower 48, explained in response to Kumar's question on the subject (see transcript here ), that's because:

... in the Permian, our well performance is at or exceeding the type curves . And so that's what's integrated into the plan that we showed with you. I'll take you back to the technology section as well, where we showed 50% improvement in drilling efficiency since 2019, 60% in completions. And so we do have some level of efficiency improvement over that 10-year period as well.

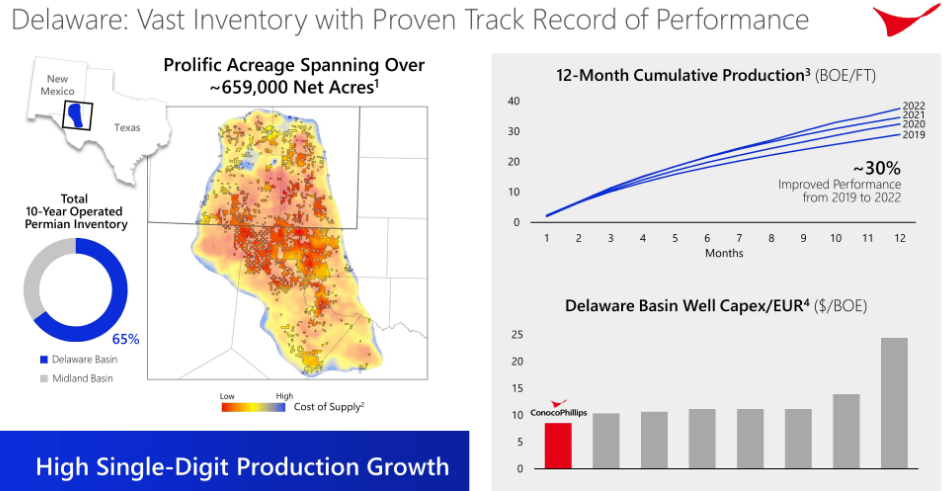

The 12-month production type-curve Olds referred to is in the upper right-hand corner of the slide below:

{kind=link}

Clearly, COP has been consistently improving its Permian well efficiency over time. So, for COP to say the 10-year forecast was based on the 2022 type cure (which it's now at or exceeding) appears to be quite conservative in my opinion. Had the company projected they'd get another 30% improvement from here, or even 10%, that I would have had a problem with as well. In addition, COP has been very prudent and has taken its time in exploiting its Permian assets (just as it did in the Eagle Ford & Bakken) to learn the rock and the best recipes to maximize EUR. COP certainly didn't willy-nilly drill-out its tier-1 acreage like some other operators have. Indeed, with the recent acquisitions, COP now has a massive Permian tier-1 inventory that enables it to drill long 2-3 mile laterals very efficiently.

As for the "assumption of higher commodity prices," that simply isn't the case. COP's 10-year forecasts were based on a $60/bbl mid-cycle price for WTI, a 50% reinvestment rate, and 6% CAGR in CFO from 2024-2032. COP is 100% un-hedged, so the company is certainly positioned very well to take advantage of higher oil prices (like right now), but management repeated several times that its planning and cash flow forecasts were based on a mid-cycle price of $60/bbl WTI. So I don't understand Kumar's take that COP's plan is dependent on "higher commodity prices." It clearly is not.

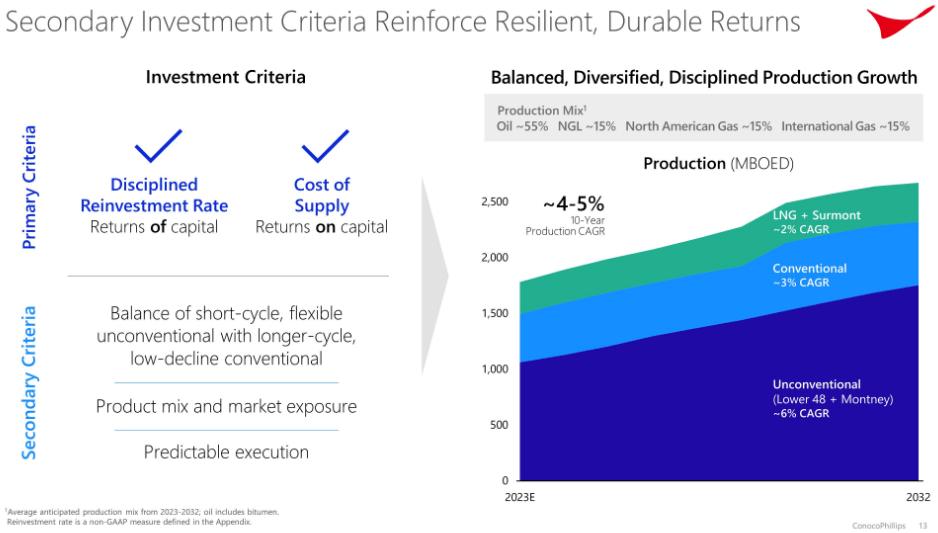

No doubt, COP's resource and production profile is now dominated by its short-cycle unconventional shale assets (purple area in the right side of the graphic below) and that - led by the Permian - will grow over the coming decade:

{kind=link}

That short-cycle optionality across three major shale basins (Eagle Ford, Bakken, Permian) is a huge advantage for the company as it can respond relatively quickly to the volatile oil market. However, what Kumar may be discounting is Conoco's long-cycle LNG and conventional assets (like Alaska) that are linked to the higher price of Brent and are what differentiates COP from all its other E&P peers. Very similar to COP's shale assets, these long-cycle assets also throw off significant free cash flow at $60/bbl Brent. Meantime, once Willow (a 600 million bbl resource) goes into production in Alaska, the development is estimated to reach 160,000 bpd of production that is expected to last 10-plus years.

Another advantage for COP vs. all its E&P peers: Due to its legacy operations in the U.K., Norway, Australia, and Qatar, COP not only has a strong U.S. natural gas marketing business with its Permian and Eagle Ford gas production, but it has a global marketing business that includes LNG. As William Bullock, ConocoPhillips Executive vice president and CFO, put the company's natural gas business:

So the bottom line is we have a strong commercial advantage, one that allows us to optimize our margins across the globe. Other E&P companies do not have this capability, and they would find it very difficult to replicate.

This is one reason why the recent Sempra ( SRE ) offtake and equity agreement in that company's Port Arthur Liquefaction Holding's project was so important going forward (see COP Shifts Focus To LNG ). As Bullock pointed out:

For instance, we continue to be one of the largest marketers of natural gas in North America. We've got a strong marketing capability, and we've got deep insights in sourcing gas supply. And in fact, we're going to be managing gas supply for Port Arthur.

The bottom line is that COP's global marketing position dovetails very nicely with its associated natural gas production in the Eagle Ford and Permian Basins.

This is a huge advantage compared to COP's Permian E&P peers who are more or less price takers with few options. That's especially the case given that Permian associated gas production (i.e. Waha) is under such extreme pressure (see The Demise of NYMEX Gas (Not To Mention Waha) ).

Valuation

Kumar pointed out that while ConocoPhillips trades at a discount to its international integrated and E&P peers on an EV/EBITDA basis, in his opinion the company offers less value based on FCF- and NAV-based multiples. As a result, Kumar prefers "more attractive opportunities" that include the firm's "Top Picks": Exxon Mobil ( XOM ), Coterra Energy ( CTRA ) and Diamondback Energy ( FANG ).

The following chart compares the EV/EBITDA multiples based on year-end 2022 data compiled on Seeking Alpha:

| Mkt Cap. |

| Net Debt |

| EV |

| TTM EBITDA |

| EV/EBITDA |

| COP |

| $128.0 billion |

| $5.95 billion |

| $134 billion |

| $34.9 billion |

| 3.84x |

| Exxon |

| $465.6 billion |

| $12.53 billion |

| $478 billion |

| $91.13 billion |

| 5.24x |

| Coterra |

| $19.7 billion |

| $1.51 billion |

| $21.2 billion |

| $6.91 billion |

| 3.07x |

| FANG |

| $32.2 billion |

| $6.23 billion |

| $38.4 billion |

| $7.34 billion |

| 5.23x |

As can be seen from the chart, Kumar is spot-on: COP trades at a steep discount relative to his "Top Picks." Note that Coterra, which trades at a EV/EBITDA discount as compared to COP, is the result of the merger of Cabot O&G and Cimerex. As most of you know, Cabot was primarily a Marcellus shale gas producer. That being the case, the company (and its peer group) typically does trade at a significant discount to its more oil-centric Permian Basin (oil centric) peers.

I'm not surprised Exxon is much more highly valued as compared to COP given its international major status and it downstream diversification (refining and chemicals) that COP no longer has given the spin-off of Phillips Petroleum ( PSX ) many years ago. That is, COP and Exxon are not an apples-to-apples comparison, in my opinion. However, I would argue that COP has a superior management team compared to Exxon. While COP was gobbling up high-quality tier-1 assets in the Permian at a discount during the pandemic-induced down-cycle, Exxon was forced to take on debt just to keep from cutting its dividend. Now, after its 2022 windfall profits and with a relatively high oil price, Exxon appears to be considering a major acquisition (see Exxon & Pioneer: A Potential Deal That Won't Change The Narrative ). Let's face it, even though the shale revolution began right in Exxon's backyard in Texas, the company has arguably been "a day late and a dollar short" since the early days of shale. It overpaid for XTO ($41 billion) and if it buys Pioneer Natural Resources ( PXD ) given the present relatively high oil price environment, it will likely overpay again. Indeed, many years ago COP began high-grading its portfolio by selling low-margin non-core global assets and pivoting to shale and LNG. Exxon was late on that strategy as well. And that's exactly why COP could add to its reserves during the pandemic down-cycle, and Exxon was not able to do so.

The most direct peer in Mizuho's group is FANG - a very well-run Permian pure play. Note that COP trades at a significant discount (26%) to FANG despite the fact that COP arguably has a superior and global portfolio that's exposed to higher Brent prices. So, any way you look at it, COP appears to be the bargain of the group, and I would argue that its portfolio is the lowest cost among all of them.

I also agree with Kumar that cash flow in the latter half of the coming decade will be even stronger for COP. After all, by then both Willow and the Port Arthur LNG project are expected to be online. That being the case, COP's major long-cycle capex spending will be declining while EBITDA will rise considerably. But that isn't something to criticize - it's something for shareholders to look forward to. In addition, note that COP's agreement with Sempra contains options for the company to increase its equity interest in SRE's LNG operations going forward.

Summary and Conclusion

My take: Mizuho and its energy analyst Nitin Kumar should have stuck with their earlier February rating on COP: A Buy with a $150 price target. I certainly like the company's forward going prospects as compared to both Coterra and FANG. I would argue Exxon isn't a direct comparison given its international integrated status. However, given XOM's 25% higher valuation on an EV/EBITDA basis, its piddly 3% dividend increase last year, and a $30 billion cash hoard that is indicative of another acquisition during an up-cycle, I'll stick with COP.

In addition, note that COP's (base+variable) dividend policy paid out $4.99/share in dividends last year. That compares to Exxon's current $3.64/share annual dividend. At current stock prices, the equates to a 4.72% yield for COP versus 3.17% for Exxon .

The fact is, COP's 10-year plan is quite compelling because there's a relatively clear line-of-sight that's not dependent upon any big gambles but instead is based on assets that COP has a long and proven track record of exploiting.

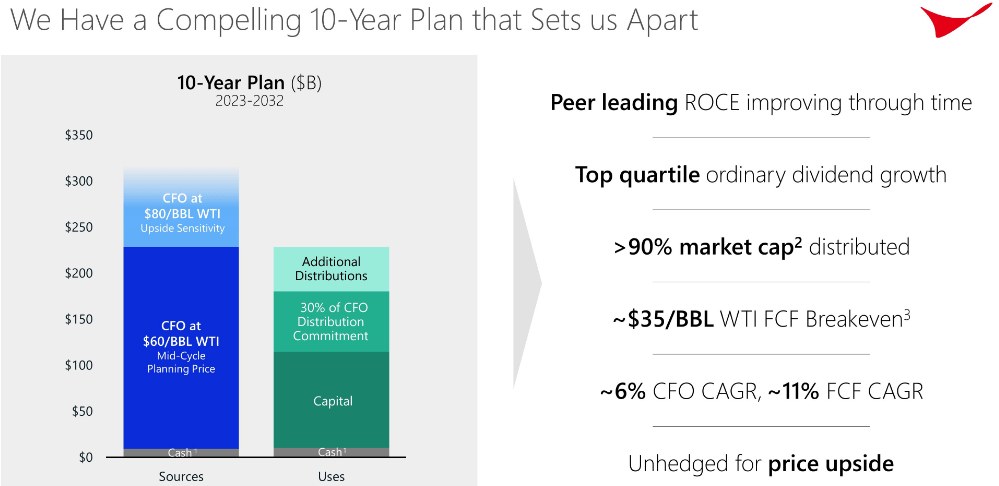

{kind=link}

As you can see in the graphic above, the plan is estimated to return - assuming a mid-cycle oil price of $60/bbl WTI - a whopping 90% of COP's current market-cap to shareholders over the next 10 years. Better still, the company now has a low cost-of-supply resource base that is expected to last 30-plus years.

I'll end with a 10-year total returns comparison of COP versus Mizuho's "Top Picks" Exxon and FANG:

As can be seen, FANG has been far-n-away the best performer while COP outperformed Exxon by over 60% over the past decade. But what matters is the performance going forward. And I would argue that COP's global portfolio - with long-cycle Brent-based assets like LNG and Alaska - is superior to FANG's and note that its Permian acreage also is tier-1 but much larger than FANG's. Time will tell, but I like COP's chances to outperform all of Mizuho's "Top Picks."

For further details see:

ConocoPhillips: Refuting The Mizuho Downgrade