PXD - ConocoPhillips: Strong APLNG Results Will Buoy Thursday's Q4 Report

Summary

- After picking up an additional 10% interest in APLNG last February, COP is likely to see a $600-plus billion distribution from the asset in Q4.

- That will be a bright-spot in a quarter where, sequentially, oil and gas prices were lower. However, COP's full-year FY22 earnings are likely to come in ~$14/share.

- Perhaps more interesting is what COP decides to do with its variable dividend - which, last quarter, was $0.70/share. My estimate is for a variable dividend declaration of $0.56/share.

Many shareholders will likely remember that, back in February of last year, ConocoPhillips ( COP ) closed on a transaction for an additional 10% interest in Asia Pacific LNG ("APLNG") from Origin Energy ( OTCPK:OGFGY ) for $1.645 billion in cash. Talk about a well-timed transaction - the deal closed just one-week before Russia invaded Ukraine and sent global LNG prices through the roof. COP shareholders are likely to see big benefits from this transaction on Thursday, when ConocoPhillips is scheduled to release its Q4 and full-year 2002 earnings report.

Investment Thesis

APLNG is a joint-venture between ConocoPhillips (47.5%), Origin Energy (27.5%), and Sinopec (25%). Origin operates APLNG's upstream (primarily coal-seam gas, or "CSG") and pipeline assets, while ConocoPhillips is the operator of the downstream LNG assets on Curtis Island as well as the export sales and marketing for the venture's LNG cargoes.

The slide below from ConocoPhillips' APLNG Fact Sheet shows a map of the APLNG assets:

ConocoPhillips

On the Q3 conference call in early November of last year, CFO William Bullock said:

APLNG distributions were $257 million in the quarter, and we expect fourth quarter distributions to be about $600 million.

In Q1, COP received ~$500 million in APLNG distributions and in Q2, it was $750 million .

In other words, over the first three quarters of FY23, APLNG distributions were $1.51 billion - only $138 million less than what COP paid for the additional 10% ownership stake back in February. Certainly after the Q4 distribution is reported Thursday, COP will have not only completely paid for the extra 10% stake in APLNG via distributions from the venture this year alone, but will have a few hundred million extra to boot. That's phenomenal.

We can get some insight into what to expect from COP's APLNG asset because Origin Energy released its Q2 results today (Monday - Tuesday Australia time):

Average realised price for LNG in the quarter was $15.94 per metric million British thermal unit (MMBtu), up 35% from the $11.80 per mmBtu earned a year earlier .

Production from Origin's share of APLNG dropped to 45.5 petajoules (PJ) from 60.8 PJ, as wet weather caused delays to drilling and restricted site access.

So, we can expect significantly lower production out of APLNG, but realized prices will likely be up 35% yoy, and - of course - COP now owns an extra 10% of production as compared to Q4 of last year. All told, COP's previous APLNG Q4 distribution guidance of $600 million was given in early November, and thus still had a couple to go months before the end of the quarter. During that time, Asia LNG prices continued to be very strong, jumping 20% in the third week of November, and as high as $35/MMBtu in December. But of course those are spot prices, and most of APLNG's output is tied to long-term supply contracts based on the price of Brent oil - which moderated toward the end of Q4:

MarketWatch

Q4 and FY 2022 Earnings Estimates

But of course APLNG (and Qatar LNG) are only two of ConocoPhillips assets. Obviously, the Permian is playing a big role in the company's financial returns these days, as is Alaska.

The chart below shows Q4 and full-year 2022 earnings estimates:

Yahoo Finance

Note the consensus earnings estimate of $2.82/share for Q4 - which would be down ~20% as compared to the $3.55/share earned in Q3. Much of that is simply the result of lower domestic natural gas pricing and lower oil prices (as shown in the earlier Brent price graphic). Still, $2.82/share will still be up 24% yoy from the $2.27/share in adjusted earnings COP posted in Q4 of FY21.

For the year, the $14/share consensus estimate would be 2.3x the $6.07/share the company earned in FY2021.

The Dividend

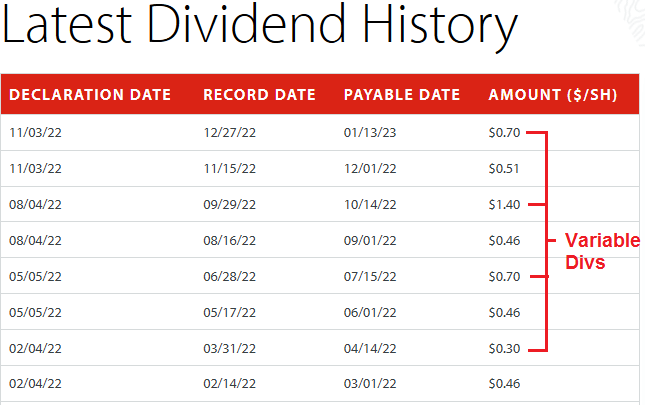

The graphic below shows COP's dividend payment declarations for full-year FY22:

{kind=link}

My first observation is that FY22 full-year dividends (base+variable) amounted to $4.99/share. Given Monday's stock price close of $120.53, that equates to a TTM yield of 4.14%. Which, as I have cautioned shale investors, differs greatly from the yield currently being reported by popular financial websites like Seeking Alpha (1.69%) and Yahoo Finance (1.92%). That's because these websites are having difficulty accurately reporting the (base+variable) dividend policies the shale oil producers have adopted.

Regardless, last quarter's variable dividend was $0.70/share. While COP could easily afford that level for Q4, my guess is the lower earnings and free cash flow on a sequential basis likely means COP will pare it back. For instance, if Q4 earnings come in at the consensus estimate of $2.82/share, and if we take a straight proportional equivalent from Q3 (i.e. $3.55 in EPS, and a $0.70 variable dividend), that would indicate a Q4 variable dividend of an estimated $0.56/share.

And that's a shame compared to a company like Pioneer Resources ( PXD ) that returned $25+/share in dividends to its shareholders last year. That's because Pioneer is not massively over-emphasizing share buybacks over the dividend like COP is. For example, in Q3 COP generated $4.7 billion in free-cash-flow and distributed $4.3 billion of that to shareholders. However, only $1.5 billion of that went to dividends while $2.8 billion was used for share repurchases.

Unfortunately, this is all too common in the energy sector these days. As I recently reported on Chevron ( CVX ), that company generated a whopping $37.6 billion of free-cash-flow last year (an estimated $19.58/share), has a pristine balance sheet, and $17+ billion in cash, yet only increased the dividend 6.3% for an annual obligation of only $6.04/share while announcing a massive $75 billion share buyback authorization (see Chevron: What A Big Dividend Disappointment ).

As I also pointed out in that piece, while the executives of these big oil companies pound the table on what a great value their stock is (while they are at or near all-time highs ...), they typically sell their stock options like a hot potato as soon as they vest. And while they're effectively forcing their shareholders to double-down on their oil investments, they appear to be selling their company's stock and investing in the clean-green energy and EV transition (see Why COP's CEO Sold Oil And Bought Copper ).

Summary and Conclusion

COP's well-timed acquisition of an additional 10% interest in APLNG last February will lead to a much stronger Q4 than it otherwise would have had. Q4 distributions from APLNG are likely to come in above $600 million. Meantime, overall results will be lower on a sequential basis due to moderation in the price of oil. A proportional analysis of the variable dividend based on EPS, and assuming free-cash-flow roughly scales in-line, suggests a variable dividend declaration of an estimated $0.56/share as compared to last quarter's $0.70/share.

Given still healthy global oil prices, and despite the crash in the price of domestic natural gas, COP still looks attractive to me. I say that because the company is currently trading with a forward P/E of only 8.9x, the dividend yield is quite attractive, and China's reopening is likely to buoy oil prices by the summer driving season. Shares could easily rise to $140 over the next 12-months. That is especially the case if the U.S. dollar continues to weaken. If so, COP offers investors an opportunity for 20%-plus total return this year.

I'll end with a five-year price chart of ConocoPhillips stock and note that it's up 40% over the past 12 months:

For further details see:

ConocoPhillips: Strong APLNG Results Will Buoy Thursday's Q4 Report