CCSI - Consensus Cloud Solutions: Growth Remains Elusive Neutral

2023-12-30 03:45:50 ET

Summary

- Consensus Cloud Solutions has underperformed due to stagnant revenue growth and macro challenges in the healthcare sector.

- The company has seen a decline in customer additions and rising churn, particularly in the small/home office segment.

- Revenue growth has been flat to negative, and the company faces challenges in reaching its long-term growth targets.

- We remain skeptical and await any tangible progress on the growth prospects. Initiate at Neutral.

Investment Thesis

Consensus Cloud Solutions ( CCSI ) shares have significantly underperformed the broader software index, primarily driven by stagnating revenue growth amidst persisting macro challenges and employment shortages impacting the healthcare sector in particular (which forms over 50% of total revenues).

It reported a continued decline in total customer additions along with rising customer churn, particularly within small/ home offices (SoHo) segment, partially offset by growth within corporate segment along with lower churn. Revenue growth has been largely flat to negative over the past several quarters amidst weak macro, which has a much worse impact on the small businesses. CCSI continues to face challenges throughout 2024, and we see lack of catalyst in macros and product initiatives towards its long term growth targets of MSD to HSD revenue growth. We remain skeptical and continue to be on the sidelines till we see any measurable progress on the company pivoting to a growth model. Initiate at Hold.

Company Background

Consensus Cloud Solutions ((CCSI)) is a leading vendor of information delivery solutions for a broad range of industries including healthcare, financial, legal, government and education. The company serves over 1 mn customers in small/ home offices (SoHo) as well as 50k+ corporate customers across different sizes, but largely being small and medium businesses. Key solutions include eFax (digital cloud fax), Unite (integrating electronic health records with the overall system architecture), jSign (e-sign and digital sign) and Clarity (AI providing actionable data insights)

Historical Track Record

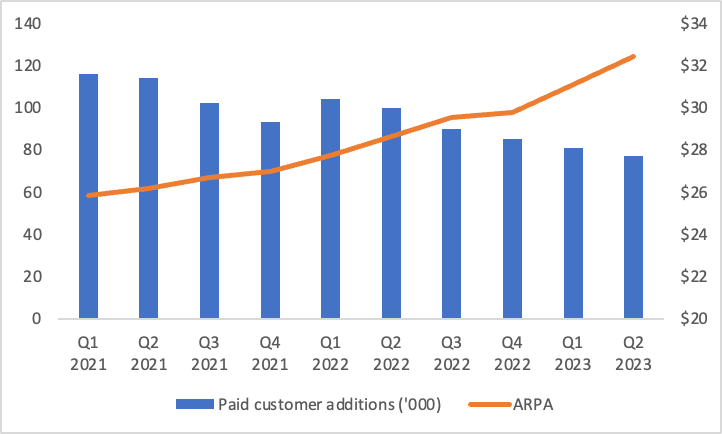

Customer additions and ARPA

The company witnessed a significant deceleration in net customer additions over the past several quarters amidst challenging macro conditions, which has led to slower signups from SoHo which remains among the worst affected. Average revenue per account improved over the quarters as a result of increasing share of the corporate customers as well as higher revenue per account from corporate segment.

{kind=link}

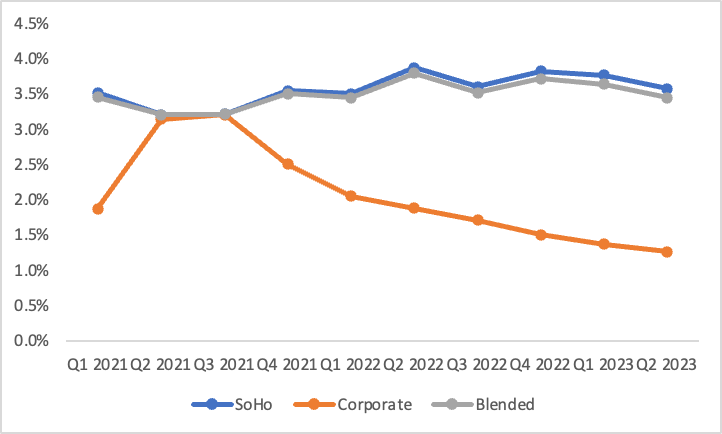

Cancellation Rates

Cancellation rates have broadly mirrored SoHo segment as it forms a dominant part of the total customers, however, the company has witnessed significant improvements within the corporate segment amidst turbulent macro conditions.

{kind=link}

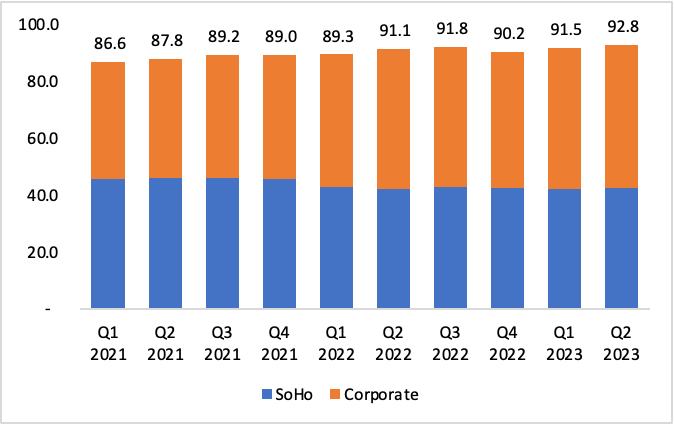

Revenue

Revenue from corporate customers have inched up over the past several quarters which remains a silver lining while revenue from SoHo has largely remained flat and declined across quarters amidst persistent macro headwinds.

{kind=link}

Current Trading Report

CCSI reported another challenging quarter in Q3 with a miss on both the topline and bottomline amidst continued macro challenges, particularly pressurizing the healthcare sector. It reported a decline of 1.3% in revenues to $91 mn missing the consensus expectations pegged at $95 mn. This was largely driven by slowing growth in its healthcare segment, which generates over 50% of the total revenues. This is evident in its corporate revenue growth which has decelerated significantly from 13% in 3Q22 to 3% in 3Q23, largely due to continued slow-decision making primarily within its healthcare customer base. Management expects these conditions to persist until there is a substantial relief in the labor markets.

Gross margins declined by about 180 bps YoY to 61% primarily due to an increase in personnel costs as well higher costs related to platform development. Gross margins have been on a downward spiral over the past year, however, the company has been able to maintain its gross margins on a sequential basis. The decline in gross margins is also due to lower employee utilization amidst stagnating revenues.

Adjusted EBITDA came in at $48 mn with margins declining by ~100 bps YoY to 53% primarily driven by lower gross margins partially offset by a decline in selling and marketing expenses. This was also below the street estimates pegging at $51 mn largely driven by lower topline. Adjusted EPS came in at $1.51 ahead of the consensus estimates pegged at $1.30 primarily due to lower share count as a result of buybacks.

Balance sheet position remained stable with the company ending with total debt of ~$800 mn while a cash balance of $155 mn yielding to a Net debt/ 2023 EBITDA of 3.5x. The board further approved to repurchase notes of up to $300 mn which would further strengthen the balance sheet and provide flexibility to capital allocation priorities.

The company further lowered its full year guidance and now expects revenue of $362 - $365 mn from $370 - $390 mn previously while Adjusted EBITDA is expected to be $186 - $188 mn significantly below the prior expectations of $192 - $206 mn. For 2024, the company expects a negligible revenue growth on a consolidated basis, driven by continued double-digit decline in SoHo space offset by an MSD growth in the corporate segment. This is also the third straight year of stagnant revenue growth and significantly below the management's target of 5 - 9% growth, pointing to continued challenges in the business operations. It expects EBITDA growth to be higher than revenue growth on the back of a lower base. EBITDA has been consistently declined over the past 3 years amidst stagnating revenues with EBITDA margins plummeting by almost 6 percentage points which does not point to any meaningful improvements in operational performance.

| 2021 |

| 2022 |

| 2023E |

| Revenue |

| 353 |

| 362 |

| 364 |

| EBITDA |

| 203 |

| 196 |

| 187 |

| % margin |

| 57.5% |

| 54.1% |

| 51.4% |

Note: 2023 revenues estimated at mid-point.

We remain skeptical on the company's ability to drive growth towards its long term as a result of lack of catalysts amidst continued challenging macro conditions along with lack of product initiatives. It has initiated rollout of 10 VA sites recently and also expects to accelerate the ECFax program in 2024, however, we do not see any measurable improvement in utilization due to continued softer macro within SoHo space. We expect the company's 2024 targets are lackluster but largely achievable, but remain skeptical on the long term growth prospects.

Valuation

We compare CCSI with other health technology players who also have similar business model. The company trades at an EV/ Fwd EBITDA of 6.1x compared to its peer average of 6.8x, which is at a slight discount. In addition, the company trades at a 25-30% discount to its long term historical averages. We believe the discount is warranted given the continued macro challenges pressurizing its core healthcare business, which can further dampen the growth prospects. We believe while the valuations appear deceptively attractive and there are some green shoots to the operational performance, there is still a long road ahead for us to be constructive on the stock. Initiate at Hold.

Risks to Rating

Risks to rating include

1) Macro risks: Any further deterioration or an improvement in the financial health of SoHo can significantly impact the utilization of CCSI solutions.

2) Regulatory risks: CCSI operates in healthcare segment with interoperability being the key growth driver. Healthcare sector is heavily regulated and any adverse implications as a result of stringent regulations which limits access to electronic health records ('EHR') or additional regulations on interoperability can impact business operations.

3) Fragmented Market: EHR is a fragmented market with several private players as well as larger hospitals having their own EHR system, which makes interoperability a challenge. In case CCSI is not able to compete with its ubiquitous offering, it can lead to an adverse impact on its business model.

Final Thoughts

CCSI has taken steps to arrest a decline in its share price amidst weak fundamentals through share repurchases and notes buyback. However, growth continues to elude them and persisting macro challenges weighs on its operational performance. We remain highly skeptical on the company's ability to drive growth amidst lack of new product initiatives and challenging macro after almost 3 years of stagnating growth continue to flow through into 2024. It trades at a discount to its long term averages and at a slight discount to its peers, which is warranted due to challenging growth prospects. Initiate at Neutral.

For further details see:

Consensus Cloud Solutions: Growth Remains Elusive, Neutral