CCSI - Consensus Cloud Solutions: High EBITDA Margins But Slowing Top-Line Growth

Summary

- Consensus Cloud Solutions, Inc. is expanding into the $8 billion healthcare interoperability market.

- The corporate segment is expected to drive outsized growth offset by flat to declining growth in SoHo.

- While Consensus Cloud Solutions has higher EBITDA margins compared to its peers, I keep a Hold rating on the stock due to a slower revenue growth outlook and near-term macro risks.

Thesis

Consensus Cloud Solutions, Inc. ( CCSI ) is a leading vendor of information delivery solutions for a variety of industries and for small and home offices. The company serves a $3B online fax addressable market, which is largely penetrated, and an $8B healthcare interoperability market. CCSI holds 18% market share in the $3B online fax space and points to amassing 125 patents in fax technology over the past 25 years as creating a competitive moat.

To add another layer of growth, CCSI is expanding into the $8B healthcare interoperability market. I have modelled a 6% revenue growth through 2025, at the lower end of management’s 5-9% target driven largely by increasing healthcare penetration, with mid 50% EBITDA margins. I keep a December 2023 price target of $58 on CCSI based on 8.4x 2024 EBITDA estimate.

{kind=link}

Company Description

Consensus Cloud Solutions, Inc (CCSI) is a provider of cloud fax and healthcare interoperable solutions. The company got its start in the SoHo cloud fax space over 20 years ago and entered the corporate fax space in 2010. As of FY21, CCSI is ~18% penetrated in the total cloud fax market. More recently, CCSI launched its Enterprise Cloud platform, which includes cloud-based SaaS solutions and the interoperability platform. CCSI’s customer base covers healthcare, financial services, law, and education and includes over 1M Small/Home Offices ((SOHO)) and ~45,000 Corporate businesses (SMBs and enterprises).

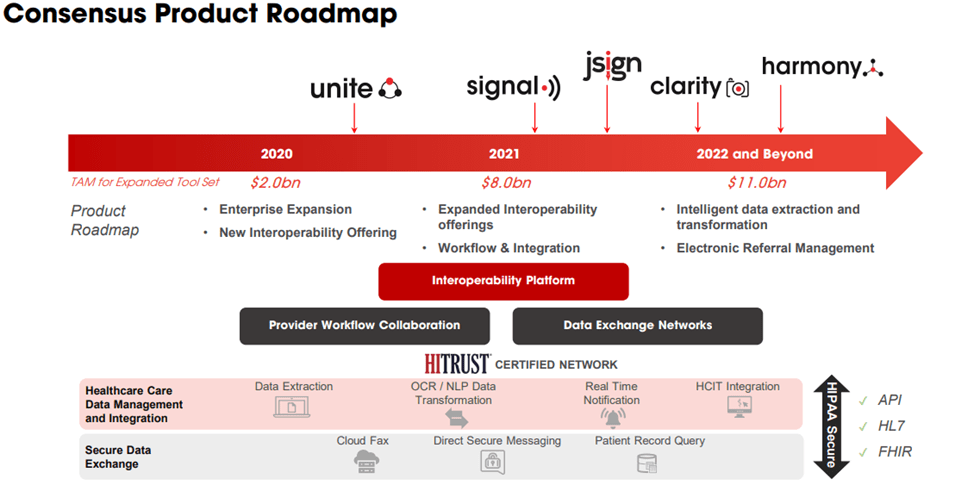

$11B Addressable Market Driven by Healthcare Interoperability

CCSI has identified an ~$11B+ addressable market split $8B+ from its cloud-based healthcare interoperability solutions and $3B from online faxing. At this stage, while the opportunity is larger in interoperability, the company derives 99% of its revenue from eFax and associated products, leaving online fax the primary market, which is growing mid to high single digits. Growth will come as the company expands its offering of interoperability products.

While interoperability and portability of electronic patient records is the holy grail for U.S. healthcare, the reality is that fax is the predominant method that providers use to transfer records. This is due to the fact that it is highly secure, verifies delivery, includes complete originating information, and is HIPAA complaint. With that, CCSI’s fax solutions are meeting the market where it is today and providing it with a very necessary solution.

{kind=link}

Financial Breakdown

Revenue Segment Breakdown CCSI reports its revenue in two segments: Corporate and SoHo. This represents its two sets of customers, which include legal, finance, education, and healthcare within the corporate segment and Small and Home offices in the SoHo segment. The two segments contribute relatively equal portions of revenue, but the corporate segment is expected to drive outsized growth offset by flat to declining growth in SoHo.

Corporate Segment

CCSI’s corporate segment is a fairly predictable business with one- to three-year contracts and recurring revenue. There are roughly 45,000 customers in this segment: 550 are enterprise customers and about 44,000 are SMBs as of FY21. The Corporate segment is smaller in customer count compared to the SoHo segment, but its monthly average revenue per customer account ((ARPA)) stands at about $354K as of 3Q22, and the revenue retention rate for 2021 was greater than 100%. Additionally, as CCSI shifts its business toward larger commercial customers, management is committed to growth within this segment and plans to increase R&D spending to support this growth.

SoHo

The SoHo segment includes monthly contracts and annual plans that include one to two discounted months. Management expects 1-3% revenue growth for FY22 given an increased focused in the corporate segment and high churn rates for SoHo customers. The SoHo segment is larger in customer count than the corporate segment; however, its 1+ million customers have an ARPA of only $14.6K compared to the $354K ARPA for the Corporate customers.

Mid-Single-Digit Top- & Bottom-Line Growth

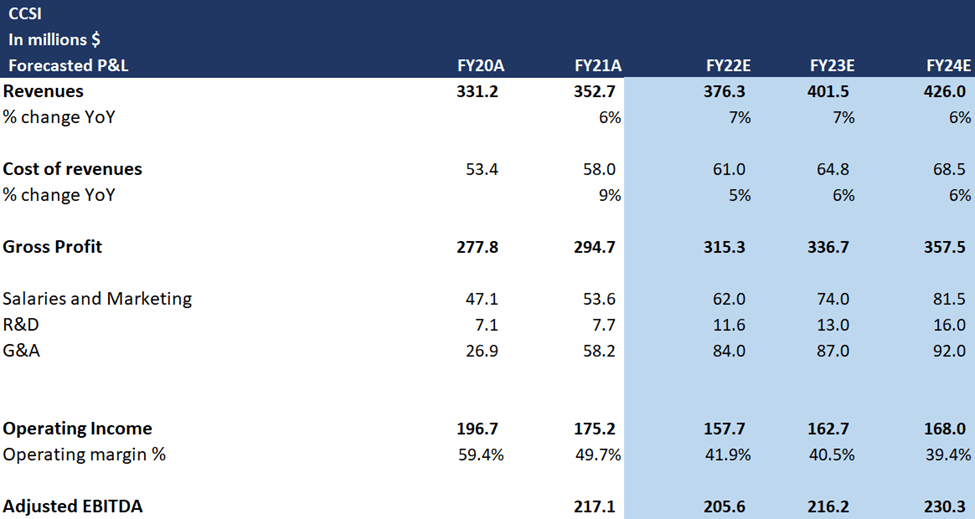

I have modelled a 6% revenue CAGR over the next three years, through a combination of mid-teens growth in corporate and declining growth in SoHo. While the company has targeted 5-9% revenue growth longer term, I have modelled to the lower end of that range due to macroeconomic headwinds and potential recession risk in the event of rising unemployment. Specifically, CCSI has spoken to “slower decision cycles for their larger corporate customers” as well as customers lacking the personnel needed to implement CCSI’s solutions. I see potential for these issues to persist into 2023, and management has stated that they do not expect much upside to margins in 2023. Looking to the bottom line, while there is some inherent fixed-cost leverage in the business, the company expects to reinvest in growth resulting in mid-single-digit EBITDA growth. I have modelled steady mid 50% EBITDA margins through 2025 (in line with the company's 50-55% target ).

Valuation

CCSI is currently trading at a forward EV/EBITDA of 8.76x, and 4.69x on forward EV/sales basis. My December 2023 price target. My $58 December 2023 price target is based on 8.4x 2024 EBITDA estimate, in line with the company’s historical average and above its forward growth due to its potential to move into the interpretability market and likely M&A, which is not embedded in my model.

{kind=link}

Risks

Economic Environment & Employment

The financial health and staffing levels of both SoHo and Corporate customers can impact utilization for CCSI’s solutions. The company’s cloud fax solutions depend on usage, and in the event of a recession or higher unemployment levels, SoHo customers may cancel their subscriptions, and corporate customers will likely reduce usage.

Competitive Environment

CCSI is a new participant in the fast-growing interoperability market. Should CCSI fail to capture adequate market share in the space, this could impact its ability to penetrate its ~$8B total addressable market ("TAM") estimate. Additionally, major electronic health records (EHRs) vendors have begun to enter the interoperability space, which could reduce demand for CCSI as these vendors implement ex-vendor communication capabilities.

Final Thoughts

Consensus Cloud Solutions is a leading vendor of information delivery solutions for a variety of industries, including Healthcare, Financial, and Legal, as well as for small and home offices. The company holds a 18% market share of the $3B online fax space and points to amassing 125 patents in fax technology over the past 25 years as creating a competitive moat. While the online fax market is largely penetrated at this point, Healthcare remains an area of growth for CCSI, driving 70% of new customer wins. To add another layer of growth, CCSI is expanding into the $8B healthcare interoperability market. While Consensus Cloud Solutions has higher EBITDA margins compared to its peers, it has slower growth, and near-term macro risks reduce visibility, which is why I keep a Hold rating on Consensus Cloud Solutions, Inc. stock.

For further details see:

Consensus Cloud Solutions: High EBITDA Margins But Slowing Top-Line Growth