CNSL - Consolidated Communications Holdings: A Deal Worth Buying Into Offering Strong Upside Potential

2023-11-06 03:24:29 ET

Summary

- Consolidated Communications Holdings is being acquired by Searchlight and BCI in a $3.1 billion deal, offering an upside of around 11.5% for shareholders.

- CNSL provides broadband and business communication solutions across the US, with strong growth in consumer fiber net adds.

- The deal presents a good short-term investment opportunity, but there is a risk of disruption due to government intervention or regulatory restrictions.

Investment Rundown

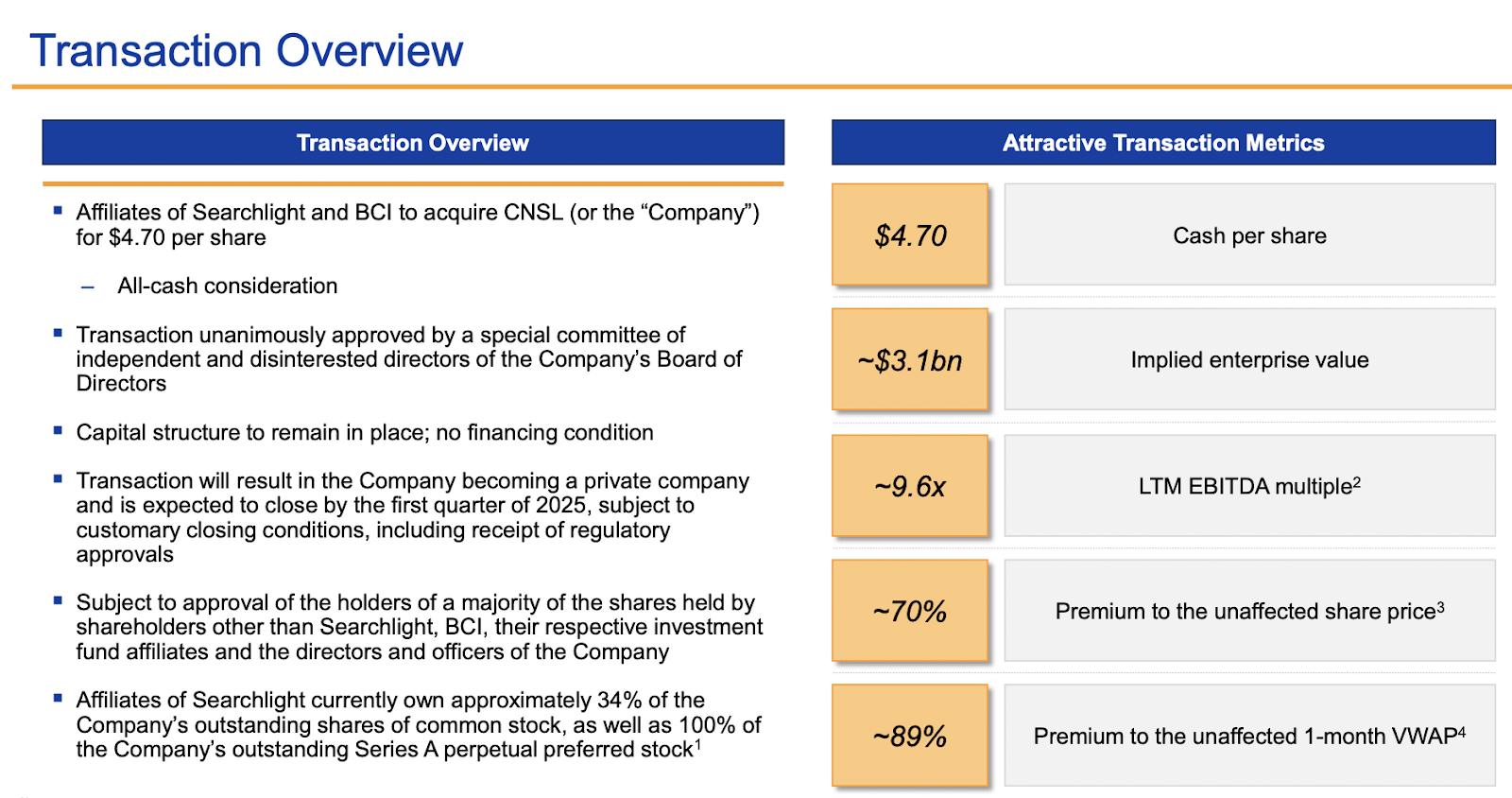

It was not long ago that the announcement came that Consolidated Communications Holdings ( CNSL ) is being acquired by Searchlight and BCI in a deal valuing CNSL at $3.1 billion. As of now that indicates an upside of around 11.5% for shareholders. The deal seems like a decent arbitrage bet right now and with the upside in the double digits, I am rating CNSL a buy right now. On its own the company is solid and we will take a look at the financials and the recent earnings for the company to also gauge the potential it has even if the deal falls through buy now would leave you with shares in the company.

Before the announcement the shares traded at around $3.5 so the deal caused a near 17% increase but still leaves some headroom for investors to buy as there seems to be some risks present still that the market is anticipating.

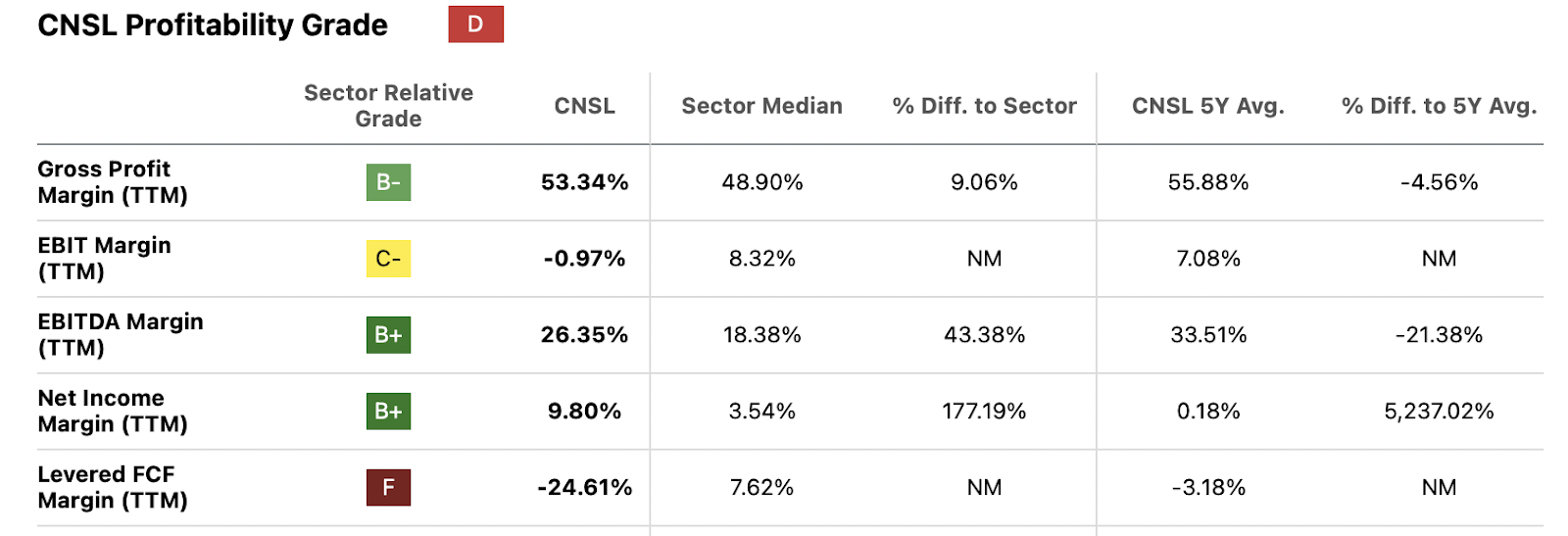

Company Segments

CNSL in collaboration with its subsidiary entities, is dedicated to delivering cutting-edge broadband and business communication solutions across consumer, commercial, and carrier channels throughout the United States. The company's comprehensive service portfolio encompasses high-speed broadband Internet access, SIP trunking, and Voice Over Internet Protocol ((VOIP)) phone services.

{kind=link}

Seeking Alpha

Beyond consumer offerings, CNSL extends its reach into commercial data connectivity services, serving diverse markets with a range of solutions. This includes Ethernet services, private line data services, and a host of innovative communication solutions designed to empower businesses and foster seamless connectivity. The company's commitment to providing robust, high-quality communication services solidifies its role as a key player in the American telecommunications landscape.

{kind=link}

Investor Presentation

Looking at the transaction for the company right now it offers a decent upside potential still of around 11.5% as the deal puts an enterprise value of $3.1 billion. This is an EBITDA multiple of 9.6 which is a decent multiple increase from its historical number of 6. Right now I think the deal is good enough to buy in and is the reason for the rating. the deal is set to be an all-in cash and is expected to be finished by Q1 in 2025. This puts an annualized return of closer to 10% given the timeframe set in place. That is a good enough return in my opinion as it will yield a return higher than most index funds. The reason I also like the deal is that CSNL has been growing indecently well with the last quarter showing consumer fiber net adds being at 96% YoY. This puts the last quarter's fiber net adds at over 18,000, up from over 9000 last year during the same period.

Looking At The Deal Further

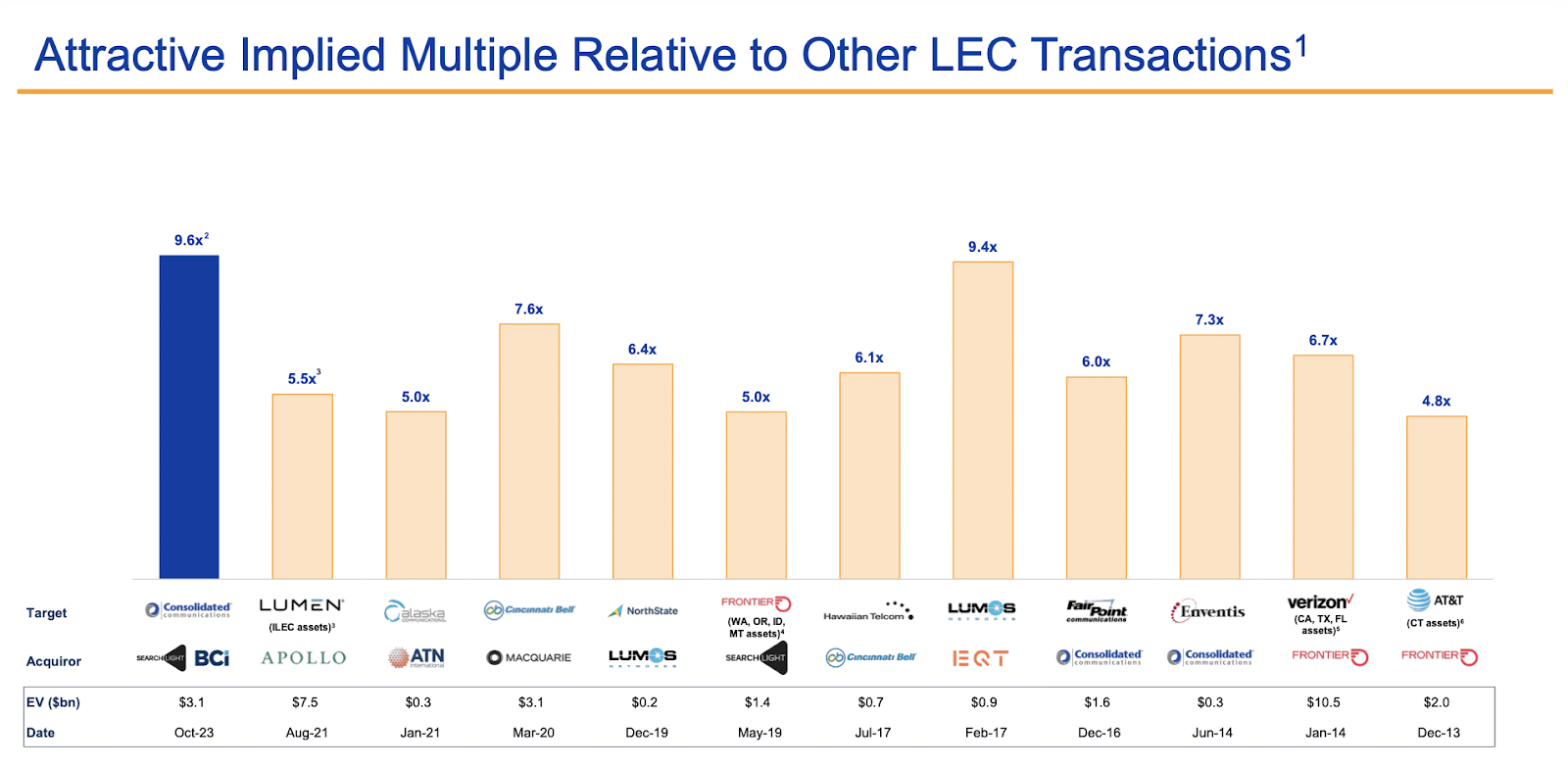

According to management , the rationale behind this transaction is bolstered by a comprehensive valuation analysis, which includes a comparison to analogous deals finalized in the past few years. Furthermore, the company's valuation assessment takes into account recent divestitures of non-core assets, one of which was announced during the second-quarter earnings release, and is set to yield $73 million upon completion. Looking at previous deals in the space this is the highest multiple a company has received. Some arguments state that an even higher one could be applicable given the sheer amount of momentum that CNSL is adding customers. Doubling the month in a 12-month time is very impressive.

{kind=link}

Transactions

This assessment underscores the careful consideration given to the company's financial standing and market position, further validating the strategic reasoning behind the transaction. By contextualizing the buyout within the broader landscape of similar industry transactions and recent asset sales, management aims to reinforce the soundness of the decision and its potential benefits for stakeholders. On its own, the company presents a pretty solid financial position with no recent intake of more debt and the cash is at over $200 million. Much of the assets the company has is the infrastructure it's investing in and expanding which right now is at over $2.7 billion. I do think it's reasonable to assume that this will continue to increase as the company adds more and more customers to its portfolio. The last quarter for example showed consumer fiber broadband revenues growing by 58% and the ARPU increased by 5.1%.

{kind=link}

Investor Presentation

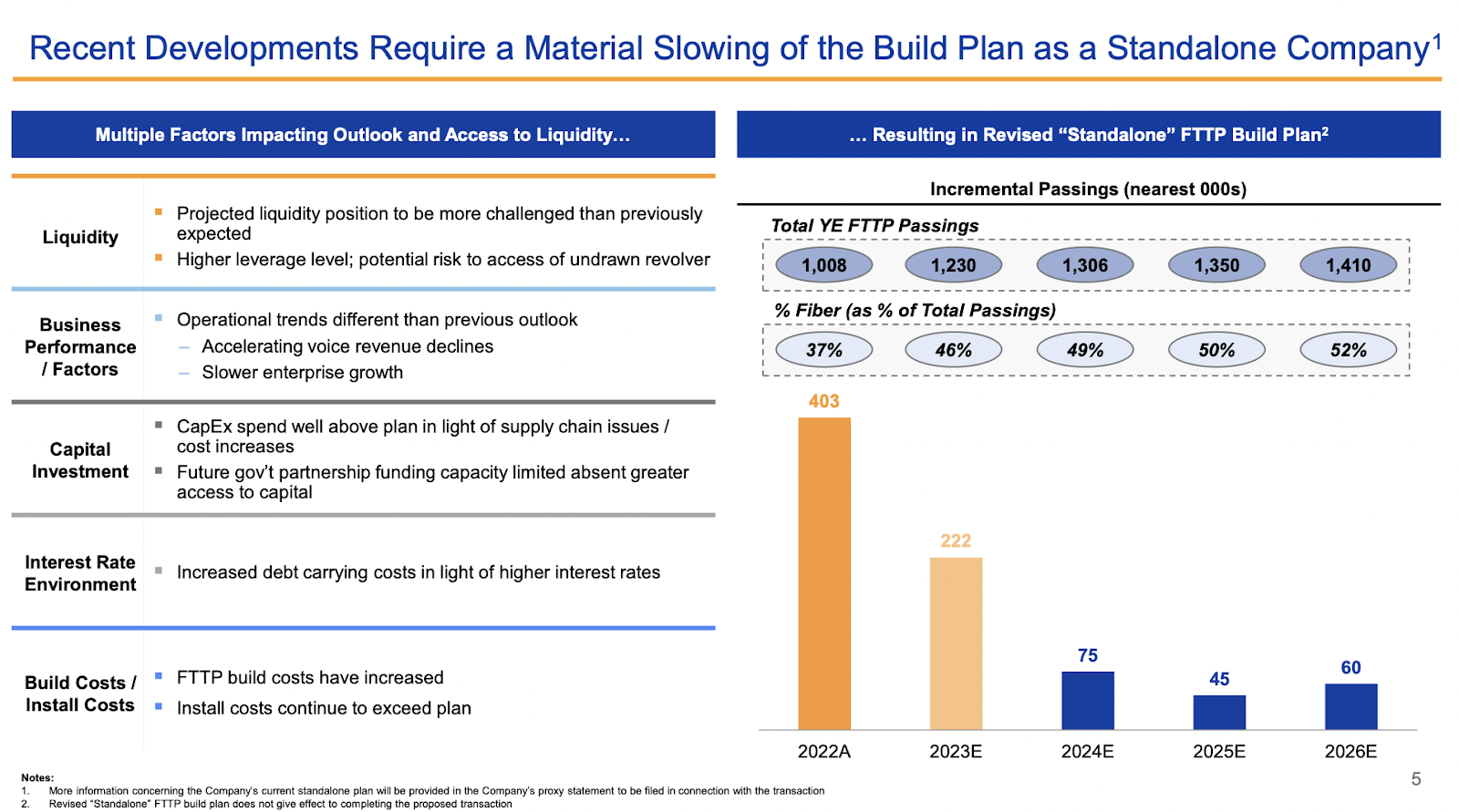

With an array of challenges at hand, including the impact of rising interest rates leading to elevated interest expenses, along with persistent issues in the supply chain, accelerating declines in voice revenue, slower enterprise growth, and heightened operational costs, management holds the perspective that beyond this year, the growth trajectory of total fiber Gig+ capable passings will decelerate. The projection indicates a climb from 1.23 million at the close of 2023 to 1.306 million by the end of 2024. In a way, this means investors can get out at a good price point as the slowdowns could potentially lead to even lower share price levels as the market adjusts for slower growth. Over the long-term, this would likely not be a significant issue, and more just a short-term bump. However, I don't think one should disregard the solid short-term appreciation that investors are getting from the company right now. An 11.5% return is plenty enough for most investors I think and should the deal fall through it's not a terrible company to hold onto shares in.

In recent news , it was revealed that CNSL stakeholder Wildcat is opposing the $4.7 share deal. Wildcat is the fifth largest holder of CNSL and cites that the reasoning behind opposing the deal is that it severely undervalued the company's equity. They see the equity value closer to $4 billion which would be 30% higher than the current offer valuation suggests. In my opinion, this news is beneficial to other shareholders as it raises the possibility of an even higher buyout price. It's not the first time the company has been approached to being bought out so I see there being a clear interest from both parties here. I think it's reasonable to assume that we may land at a higher equity valuation for the deal and that further supports my buy thesis here. A risk is certainly present and that is if there can't be a suitable price found to buy out the remaining shares for Searchlight and that could spook the markets and potentially lead to shares dropping to better reflect that additional risk. Nonetheless, I do think investors are faced with a rather good risk/reward scenario here to participate in.

Risk

A notable current risk factor revolves around the potential for a disruption to the proposed acquisition of CNSL. In the event of government intervention or the imposition of regulatory restrictions on the deal, there exists the possibility of a short-term drop in the share price. While this may not be an outcome that is expected to materialize, it's imperative to acknowledge the inherent risk, especially given the deal's current offering of double-digit returns.

{kind=link}

Seeking Alpha

The substantial returns associated with the deal directly mirror the pressure and risk associated with its execution. Although the likelihood of a major disruption remains relatively low, prudent investors should remain vigilant and prepared to adapt their strategies if any unexpected developments arise. Monitoring the deal closely and staying attuned to regulatory shifts will be key to effectively managing and mitigating this specific risk.

Final Words

The deal that has been proposed to buy out CNSL I think offers enough value right now that it makes sense to buy shares. The deal puts an enterprise value of $3.1 billion on the business and this implies around an 11.5% upside from right now. This amount is enough that I think a buy is justified. The deal is set to finalize in the first quarter of 2025 and that is putting the annualized return here a little closer to 10%, which is still above most index funds returns. In conclusion, I am rating the company a buy right now and see the arbitrage opportunity here as very interesting.

For further details see:

Consolidated Communications Holdings: A Deal Worth Buying Into Offering Strong Upside Potential