CNSL - Consolidated Communications Holdings Skyrockets: I'm Angry And You Should Be Too

2023-10-17 17:11:23 ET

Summary

- Consolidated Communications Holdings shares spiked 16.2% after announcing an acquisition by Searchlight Capital Partners and British Columbia Investment Management Corporation.

- The deal is being done at a high valuation compared to previous offers and market prices.

- Management justifies this by forecasting slower future growth, but the gap between the sale price and the company's value is significant.

While it's always wonderful to get short term gains, it's better to get much larger long-term gains. Unfortunately, sometimes, we don't have a choice in the matter. Any gain is better than a loss. But it is frustrating to see a company spike, only for that spike to be caused by a sale of that business at a price that doesn't make sense. Such is the case regarding Consolidated Communications Holdings ( CNSL ). On October 16, shares of the company skyrocketed, closing up about 16.2%. This movement higher came after management announced that the company would be acquired by two firms working together. Although some investors might be happy because of the short-term pop, I find myself very unhappy with this transaction. Given how it's structured, it is possible the deal could fall through, and investors would be wise to hope that it does.

A frustrating deal

Back in the middle of July of this year, I found myself interested in Consolidated Communications Holdings. Just prior to that article having been published, shares of the company spiked. This move higher was driven by a presentation issued by Wildcat Capital Management wherein the firm, which owned 2.6% of the telecommunications operation at the time, made the case for why the present value of the stock should be at least $14 per share at the time. As a value-oriented investor, I am always cautious of activist investors making claims that shares should double, triple, or even quadruple, if only some changes are made. But after going through the presentation in great detail, everything provided by Wildcat checked out.

At the time the article was published, I did not own any stock in the company. But I eventually bought in with the expectation of generating strong returns. I didn't mind waiting for a year or two for this to play out. And actually, for some of the time that I held the stock, I was underwater on it. Now, with a weighted average price paid for it of $3.70, I am currently up about 10.9%. And if I hold on until the deal is completed, that should add another 14.4%, taking my gains to 27% in all. But happy is not one of the emotions I’m feeling right now.

{kind=link}

Consolidated Communications Holdings

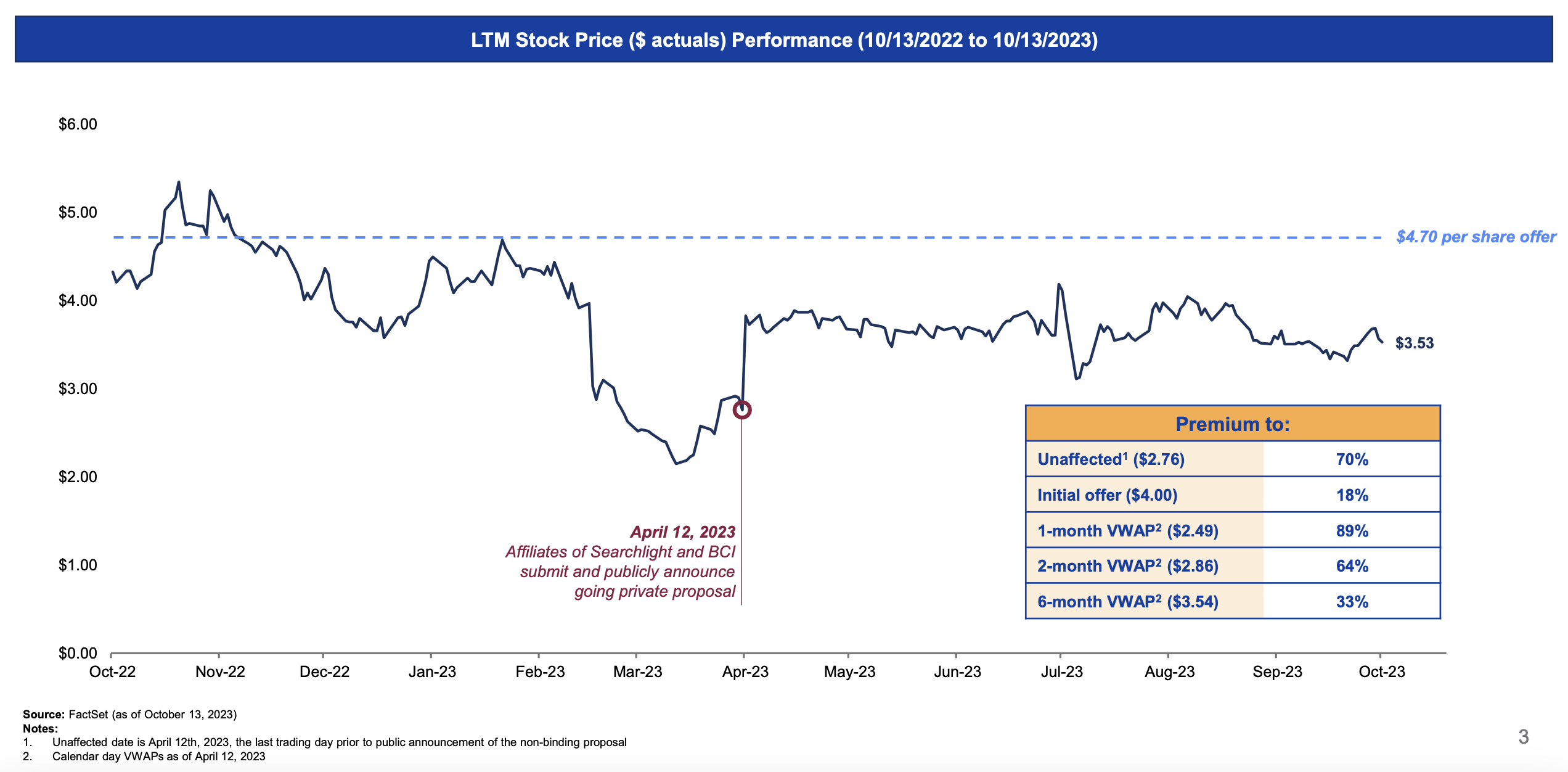

The buyers, in this case, are Searchlight Capital Partners and British Columbia Investment Management Corporation. If these names sound familiar to you, it's because they should be. These are the same two companies that offered to buy Consolidated Communications Holdings in an all-cash deal earlier this year valuing the stock at $4. As the management team at Consolidated Communications Holdings was keen to point out, this transaction is being done at a rather lofty premium to almost any other base metric you want to compare it to. For instance, it's 18% higher than the initial offer price earlier this year. It's also 89% higher than the one-month volume weighted average price of the stock. And for the six-month volume weighted average price, it's 33% higher.

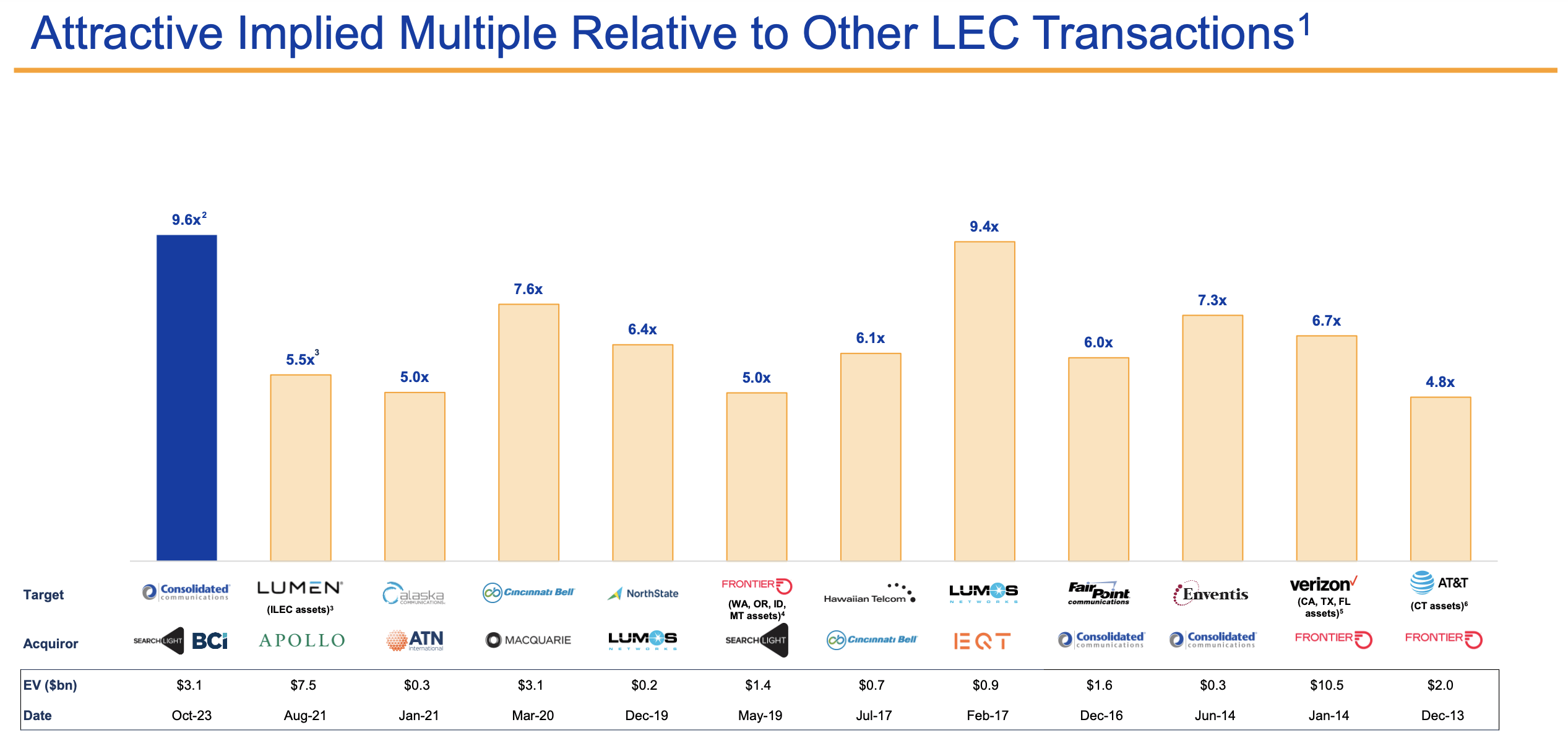

Management makes the argument that this transaction makes sense from a valuation perspective by comparing it to similar deals that have been completed over the past several years. After accounting for recent non-core asset sales, including one that has yet to be completed that was announced during the second quarter earnings release in exchange for $73 million, the company is being bought out at an EV to EBITDA multiple of 9.6. This is well above the 6.3 average that we get when looking at the last 11 transactions completed that management detailed in the image below.

{kind=link}

Consolidated Communications Holdings

Recent financial performance achieved by Consolidated Communications Holdings has been quite impressive. In the second quarter earnings release that the company made public in early August, management pointed out net new fiber additions to its network of 18,651. This was a significant increase over the 9,643 net additions reported the same time one year earlier. The company upgraded 57,438 locations to fiber Gigabit+ speeds and, as a result of its efforts, succeeded in growing its consumer fiber broadband revenue by 58% while simultaneously growing ARPU by 5.1%, all on a year-over-year basis. To make matters even better, the company even announced, at that time, that business simplification and cost cutting initiatives we're going to help the enterprise save over $30 million per annum moving forward.

There was a lot to like about this kind of earnings release. And when you add on to this the aforementioned analysis of Wildcat, which I highly recommend you read my assessment of in the aforementioned article, it can be difficult to swallow even a premium to the other transactions that management used to justify its decision. But there is another element to this deal that investors should be aware of. And this is that management now believes that future growth will be slower than past growth has been.

{kind=link}

Consolidated Communications Holdings

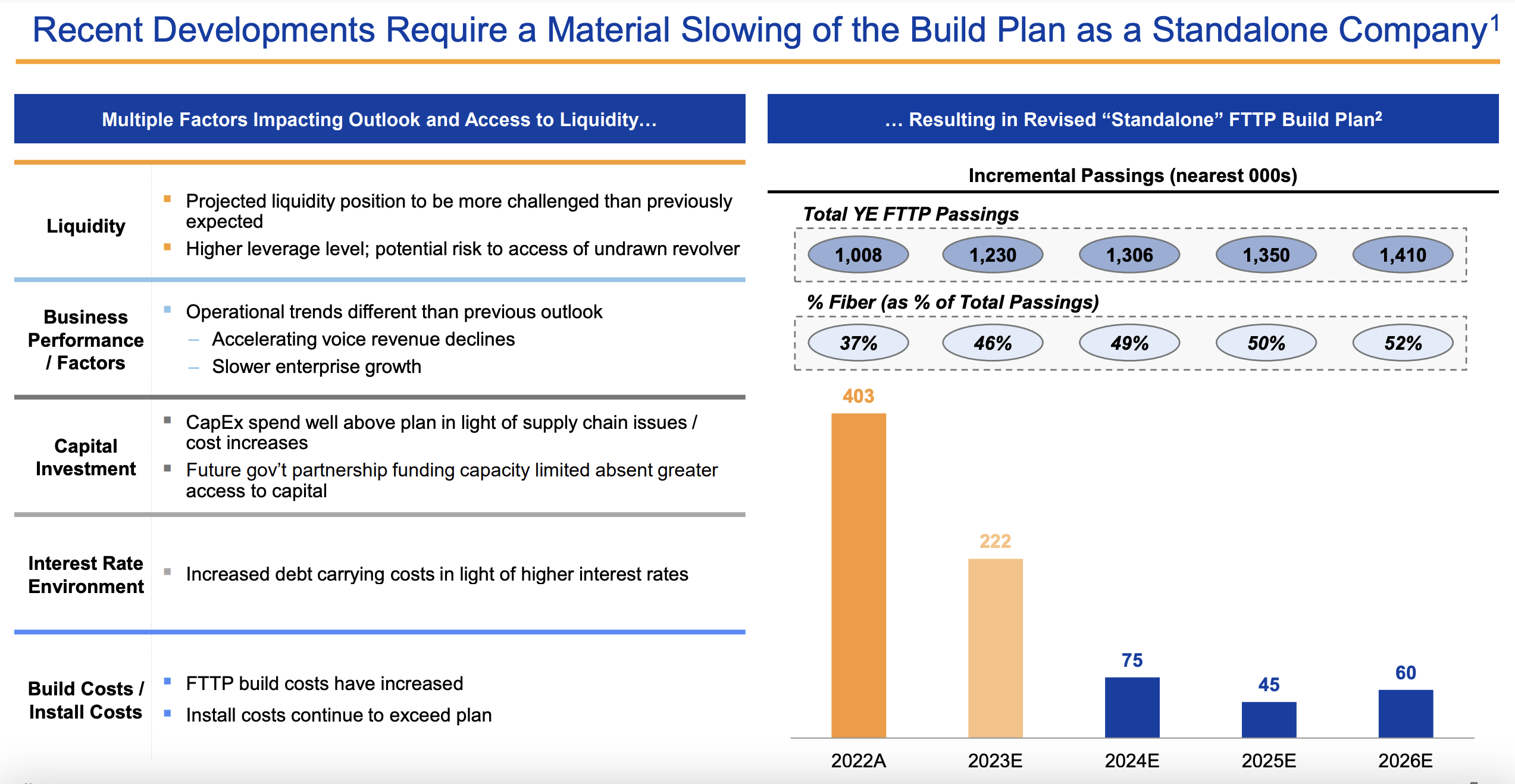

Citing higher interest expense caused by higher interest rates, as well as other issues like supply chain problems, accelerating voice revenue declines, slower enterprise growth, elevated costs, etc…, management is of the opinion that, after this year, the growth rate of total fiber Gig+ capable passings will grind to a halt, climbing from just 1.23 million at the end of 2023 to 1.306 million at the end of 2024. Growth is expected to be slowest in 2025, with expansion of only 45,000 passings. And by 2026, they are forecasting 1.41 million. By comparison, Wildcat was calling for the company to hit two million passings by 2028. This would imply a 19.9% annual growth rate from 2026 through 2028, which is frankly unrealistic.

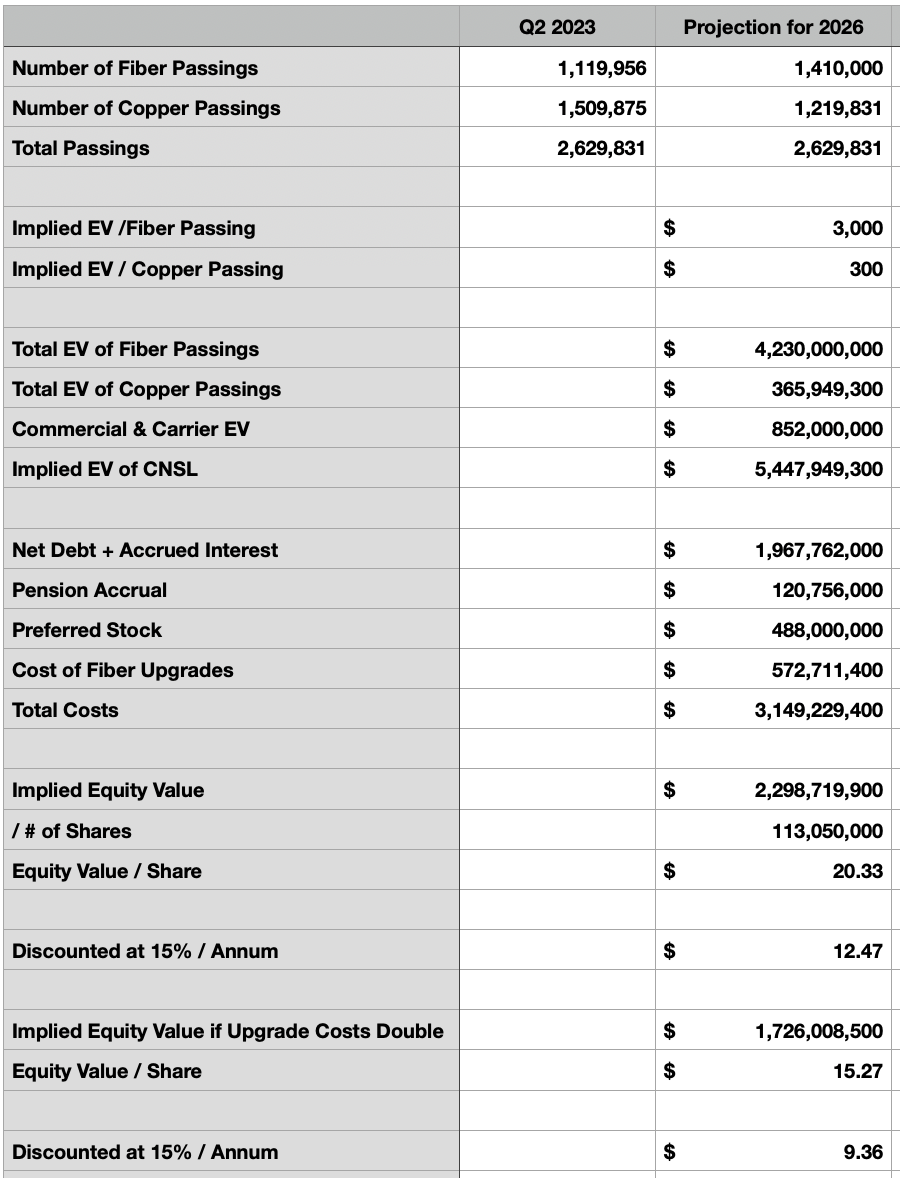

While all of this might be true, it still does not explain the significant gap in value between what the company probably should be worth and what management is selling it off for. As you can see in the table below, I repeated the same type of analysis done by Wildcat, ending instead in 2026 and assuming that managements passings turn out to be accurate. If costs remain the same per passing, the company would still be worth $12.47 per share today. That's after discounting it by 15% per annum between the second-half of this year and the end of 2026. Even if we assume that costs double per fiber passing, we would get $9.36 in value today. You have to run some really ridiculous assumptions to get anything remotely close to $4.70.

{kind=link}

Author

Takeaway

Based on the data provided, I believe that investors would be right to be frustrated about what management has decided to do. Wildcat has not, unfortunately, come out with its own public statement as of this writing. But I assume that they will feel the same way. The good news is that if management does fail to complete this deal, the termination fee is only $15.9 million. So there is some hope that perhaps something will change. As for me, I likely will hold on to my stock for now. As I mentioned already, the spread between the current price of the stock and the $4.70 buyout price is about 14.4%. When you consider this covers a span of about 14.5 months, it's not exactly a great return, but it's not an awful one either. And when you add in to this how volatile the market could be over the next several months and consider the prospect of this deal changing or being canceled for something more favorable, I find holding my stake in the company for the moment a better decision than keeping it in the bank.

For further details see:

Consolidated Communications Holdings Skyrockets: I'm Angry And You Should Be Too