CNSL - Consolidated Communications Stock Skyrockets: It Should Rise Even More

2023-07-13 09:00:00 ET

Summary

- Shares of Consolidated Communications spiked by 16.1% following a report by Wildcat Capital Management, which owns 2.6% of the company's shares, arguing that the company is undervalued.

- Wildcat's assessment suggests that CNSL stock should be worth at least $14 each, significantly higher than the $4 per share buyout offer made by Searchlight Capital Partners and British Columbia Investment Management in April.

- Wildcat's valuation is based on Consolidated Communications' ongoing upgrade from copper to fiber networks, which is expected to increase revenue and customer base.

Consolidated Communications Overview

July 12th proved to be a very wild day for shareholders of Consolidated Communications ( CNSL ). Shares of the company spiked, closing up 16.1% for the day. At issue was a letter that was written by Wildcat Capital Management in which the firm, an investor in Consolidated Communications that owns about 2.6% of all outstanding shares, argued that the business looks drastically undervalued and that management should not accept a buyout offer that came out in April. I am always skeptical when I see pronouncements of a company being drastically underpriced. But when you really dig into the arguments made by Wildcat, it's difficult to imagine the company not warranting significantly more upside than what its proposed suitors are offering. Even if we use assumptions that are significantly more conservative than what Wildcat has utilized, it becomes clear that investors would be wise to push for the company to remain independent and to continue along the path that it has found itself on.

An excellent assessment

Back in April of this year, Searchlight Capital Partners and British Columbia Investment Management issued a non-binding proposal that, if accepted, would result in the two firms collectively acquiring all of the outstanding stock of Consolidated Communications at $4 per share. That translates to a market capitalization of $452 million, with an enterprise value of roughly $2.86 billion. At that time, shares of the company spiked in response to the news. But since then, Wildcat has come up with its own assessment of what the firm might be worth.

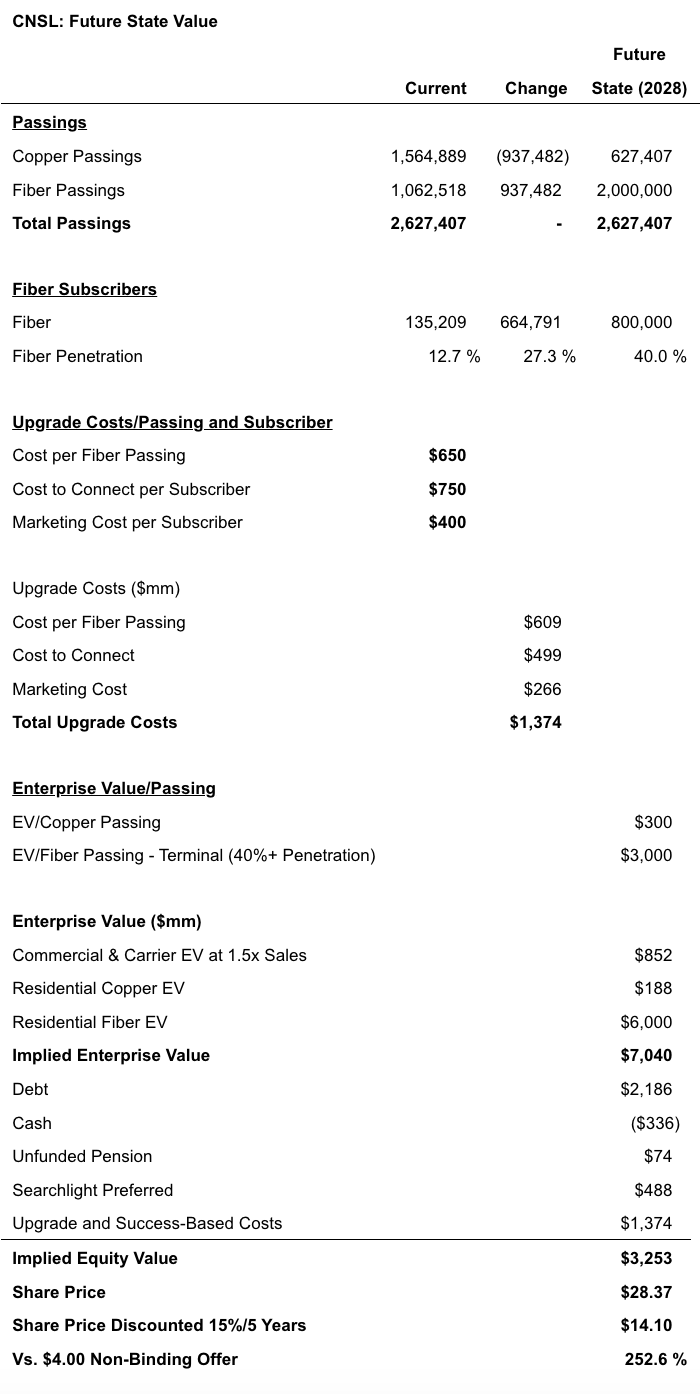

According to a letter written and made public by Wildcat, shares of Consolidated Communications should be worth at least $14 apiece. That is a massive disparity compared to the $4 per share that its suitors have offered to pay. This would translate to an enterprise value of roughly $7.04 billion and an equity value of $3.25 billion. But before we get into how Wildcat arrived at these numbers, we should first touch a bit on what the company does and what it is working on.

In the company's annual report, the management team describes the enterprise as a provider of communication solutions for consumers, both commercial and retail. As of the end of its most recent fiscal year , the company had 57,800 route miles that comprised its fiber network, touching on both rule and metro areas in the markets in which it is present. Through this network, the company provides high speed Internet, video, phone and home security services, data center services, security services, managed and IT services, and even a suite of cloud services. The firm's offerings extend to the wholesale category, with the firm offers data, voice, network connections, and custom fiber builds, to both wireless and wireline carriers. For full transparency, Searchlight, which is one of the two companies wanting to buy it up, is a strategic partner of the business that provides it funding for the upgrade of its network for the purpose of achieving more competitive broadband speeds for its users. At the time the buyout offer was issued, Searchlight held a 34.3% equity stake in Consolidated Communications.

{kind=link}

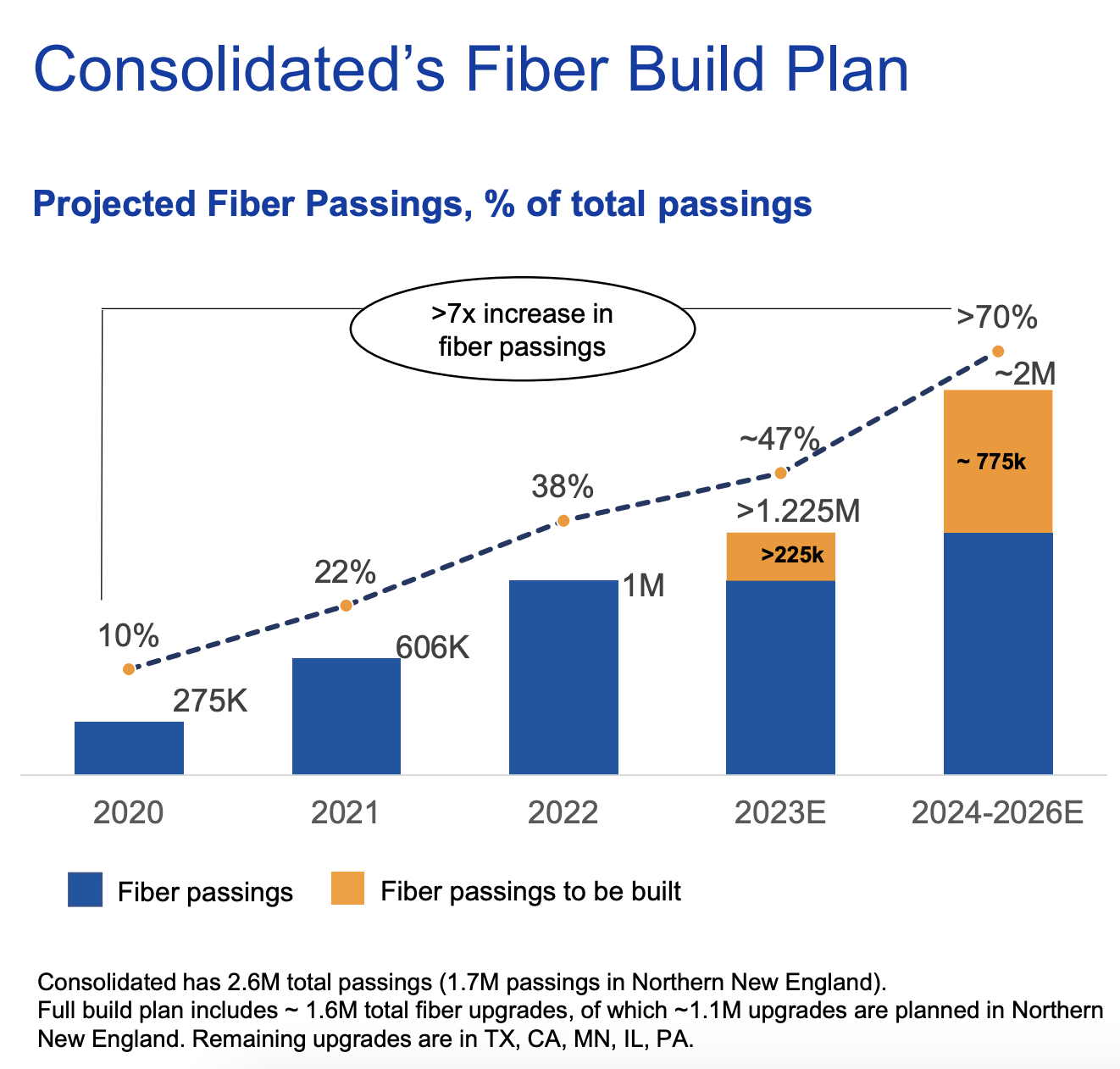

In an attempt to stay with the times, Consolidated Communications has been working diligently toward upgrading its network from copper to fiber. This is an incredibly expensive undertaking. In fact, already, the company has spent about $657 million on fiber in the ground that, according to Wildcat, the firm has yet to receive any significant cash flow from. In 2022 alone, the company achieved roughly 403,000 upgrades, taking its fiber locations, also known as passings, up to just over 1 million. That translated to about 38% of its service area as of the end of that year. The firm's goal , at this time, is to grow this number to roughly 2 million by the 2026 fiscal year end. Achieving this would allow the company to generate about $550 million worth of revenue associated with consumer broadband alone. Of that, $450 million would come from fiber, with the rest coming from its remaining copper network. That compares to $185 million worth of copper related revenue generated in 2022 and only $80 million of fiber revenue that year.

{kind=link}

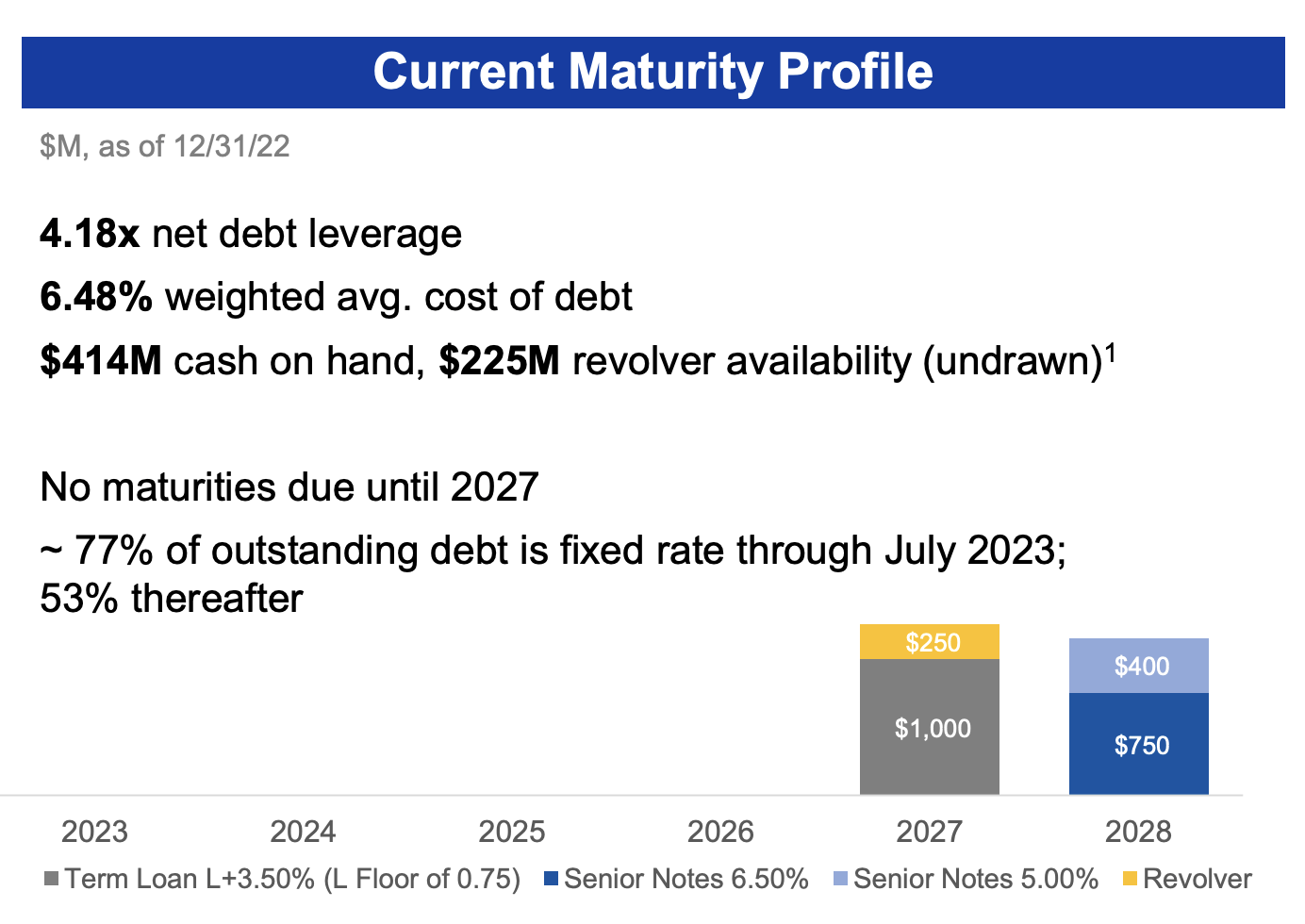

It is the opinion of Wildcat that investors should be focusing on a slightly longer-term time horizon. They looked out to what they believe is realistic for the 2028 fiscal year. Under this scenario, Consolidated Communications would keep its fiber passings at 2 million. By that point, only 627,400 of its passings would still be copper. That's down from 1.56 million at the end of the most recent quarter. But as I said already, this will not be a cheap initiative. The estimated cost per fiber passing is about $650 according to management. And the cost to connect a subscriber is about $750. There are other costs as well. For instance, Wildcat put an estimate of $400 in marketing costs per subscriber. All combined, achieving a 40% penetration rate, which management at Consolidated Communications stated is realistic, would bring a total cost to the company of $1.37 billion. For a business that already has net debt of $1.85 billion, that's quite a bit of additional spending that will be needed in order to accomplish their goal.

{kind=link}

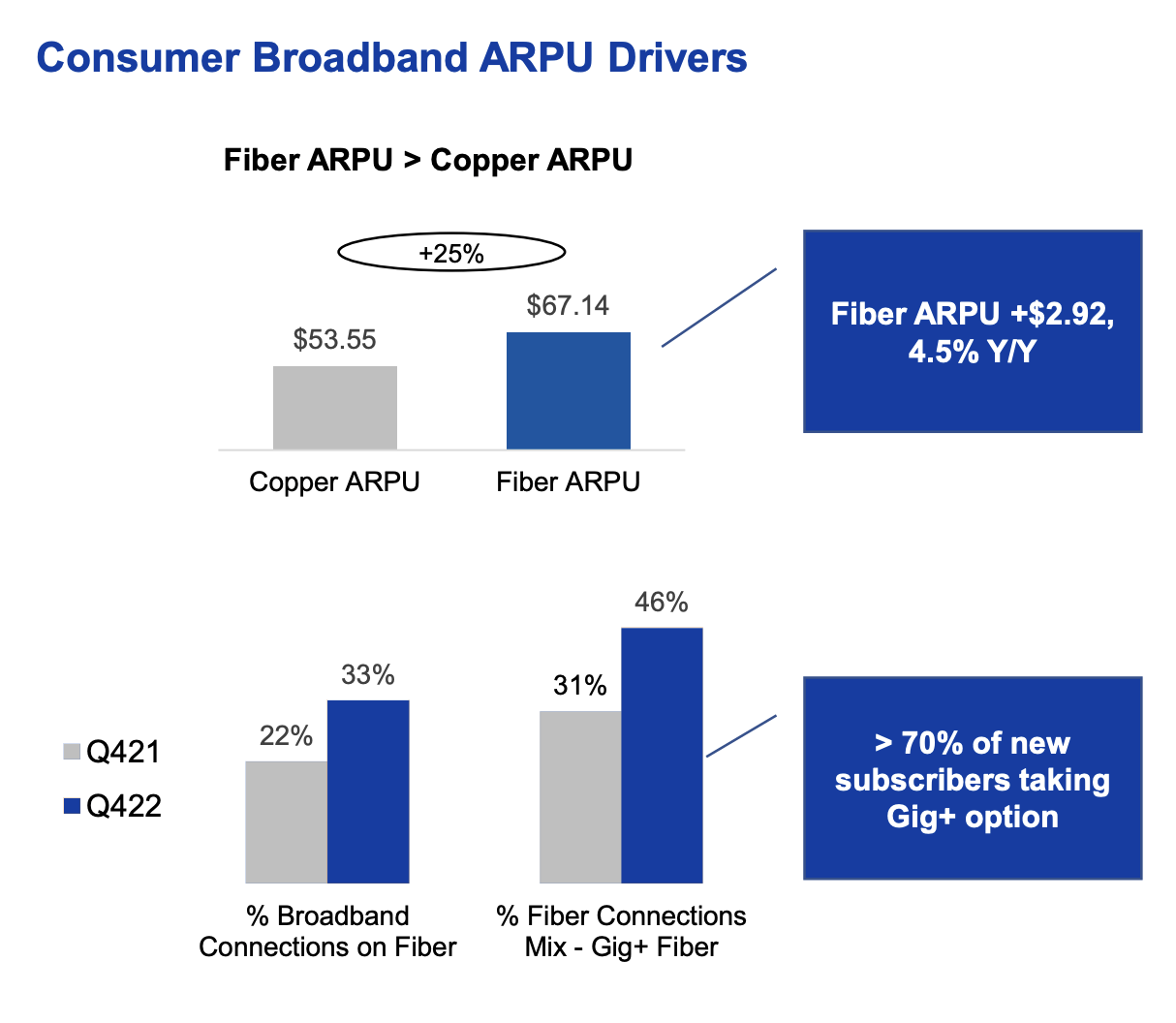

When it comes to valuing Consolidated Communications, Wildcat estimated that the implied enterprise value for a company in this space should be about $3,000 for each passing that it has. That's 10 times the implied enterprise value calculated for copper passings. There are some good reasons for this. For starters, monthly ARPU (average revenue per user) for fiber customers currently stands at about $67.14. That's 25% higher than the $53.55 for copper customers. Management's expectation is for monthly ARPU to grow to $75 by 2026. There's also some evidence based on the industry itself that $3,000 per passing is not unrealistic. At its analyst day in 2021, Frontier Communications Parent ( FYBR ) assigned a rough enterprise value per passing of between $3,000 and $4,000. And Charter Communications ( CHTR ) has been valued at about $2,800 per HFC passing. This type of passing is inferior compared to fiber because it involves higher operational costs and greater maintenance capital expenditures in order to remain viable. So using the lower end of the range provided by Frontier seems reasonable.

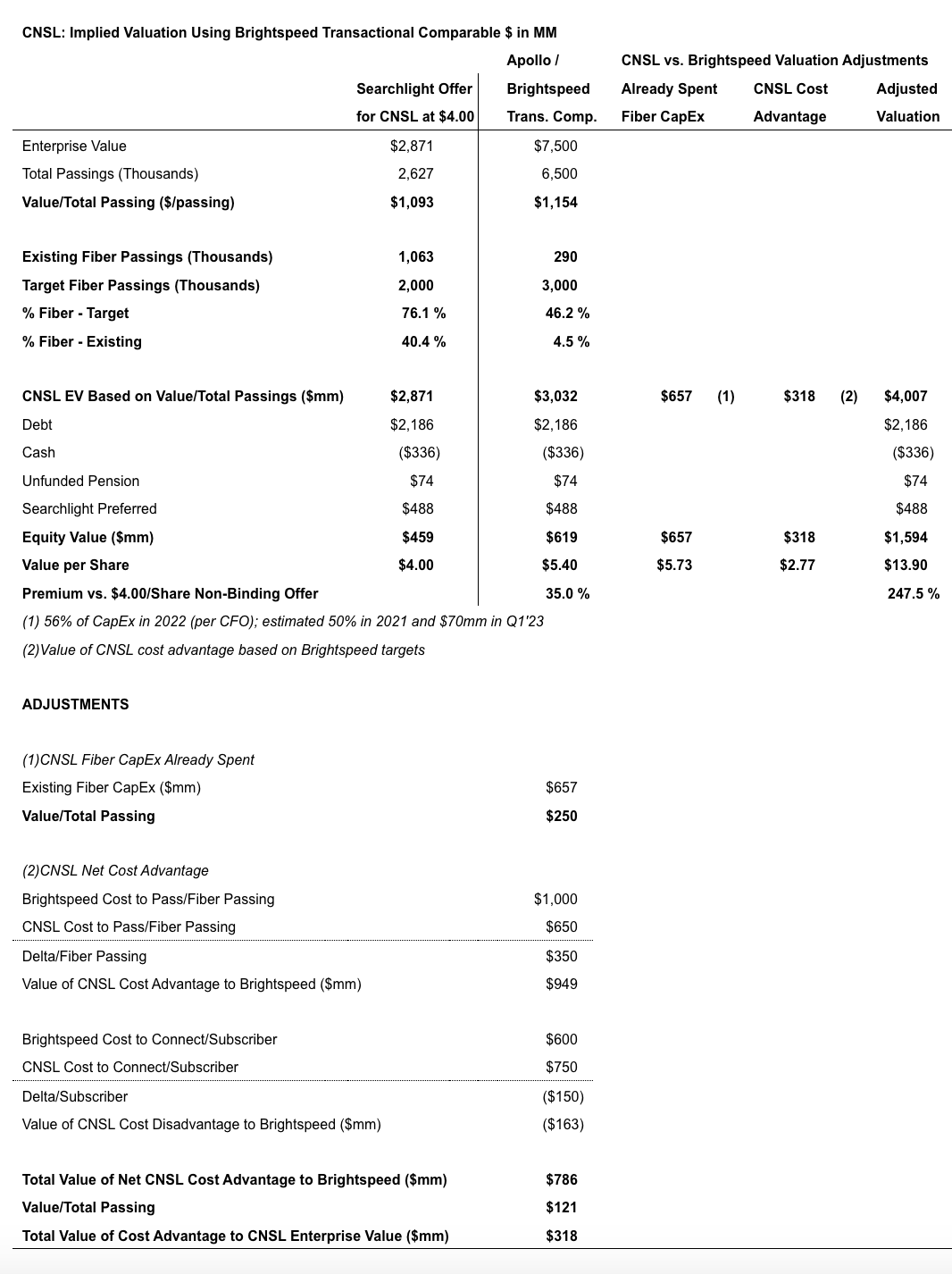

When we use these assumptions, we end up with a terminal enterprise value for Consolidated Communications of $7.04 billion. That translates to approximately $28.37 per share. To account for the risk and time value of money, Consolidated Communications even discounted that at a 15% rate per annum, getting us to $14.10 per share. But even if we discounted at a rate of 20%, you still end up with an implied value of $11.40 per unit. That's nearly triple where shares are trading today. In an alternative way of valuing the company, Wildcat looked at the price paid for Lumen Technologies (now known as Brightspeed) by Apollo Global Management ( APO ). But when you factor in the differences between the two companies and use the same, very conservative, valuation method applied to Lumen, you end up with a price per share for Consolidated Communications of $13.90.

{kind=link}

This is the kind of analysis that made me fall in love with finance. I performed many analyses similar to this in both undergrad and graduate school. I have obviously performed some since then as well, though none that were able to be applied to this industry. The logic used by Wildcat is solid, and I wouldn't make very many changes to their approach except perhaps to use the higher discount rate of 20% that I stated already. One thing that I did do though is to ask myself exactly what kind of enterprise value per passing the company would need to see for the stock to be worth even double what its suitors offered to buy it out for. Using the same methodology applied by Wildcat, I arrived at a value of roughly $1,835 per passing, which is well below any other numbers suggested for the purpose of valuing a company like this.

Even if Consolidated Communications is unable to continue on the path that it has, but still remains publicly traded, the stock is not necessarily priced at levels that wouldn't make sense. For the 2023 fiscal year, for instance, management is forecasting EBITDA of between $310 million and $330 million. At the midpoint, this would imply $320 million. If we strip out interest expense and taxes, this gives us operating cash flow of $160 million. The implied buyout price for the company right now would translate to a price to operating cash flow multiple of only 2.8 and an EV to EBITDA multiple of 9. If debt were coming due fairly soon, I would be perhaps more concerned. But the company does not have any maturities on its debt until $1.25 billion that must be either paid back or refinanced in 2027. Although it cannot cover anywhere near the full cost of the company’s continued growth, it has been estimated that the firm could be eligible for between $200 million and $450 million of additional government funding associated with fiber installation activities. And with Wildcat being of the opinion that EBITDA growth should be in the mid-teens starting next year and extending into future years, the picture should only improve from here.

{kind=link}

Takeaway

Based on the data provided, I must say that I find Consolidated Communications to be a fascinating prospect. I do worry that the significant ownership stake involving and the nature of the partnership with Searchlight could result in that company muscling the business into submission and selling off at what would be an incredibly low price. But beyond that, I think that the picture for shareholders is very favorable. I would go so far as to even rate the company a ‘strong buy’ to reflect my view that shares should drastically outperform the broader market for the foreseeable future. And while I have not made a commitment as of yet, I very likely will buy some shares in the near future.

For further details see:

Consolidated Communications Stock Skyrockets: It Should Rise Even More