CNSL - Consolidated Communications: The Buyout Offer Is Too Low

2023-04-13 14:38:17 ET

Summary

- The company should reject the $4 buy-out offer as the company has plenty of potential for the upcoming years.

- The company pivoted from a low margin copper-based communications business into a strong fiber business.

- The company operates in a market with a lack of competition, which gives them significant pricing power.

- We believe the company is a strong buy at this moment in time as we now have a margin of safety and we expect a higher bid in the future.

Introduction

Consolidated Communications Holdings ( CNSL ) is a company I started buying after its most recent earnings. My friend Jacob Rowe, Founder and CIO of Rogue Funds, a value-oriented hedge fund, talked me through the thesis surrounding this company and intrigued me. I decided to do some more DD and we discussed the investment thesis around this multiple times, which is why I'm now writing this article as I believe the current buy-out offer of $4 per share by Searchlight Capital Partners and British Columbia Investment Management is too low.

The Strategy Pivot

Consolidated Communication Holdings is a copper-based telecommunications company with operations all across the United States. The company struggled over the last few years as the share price tumbled from $30 per share back in 2016 to an all-time low of $2.11 per share on March 27th of 2023.

We believe the company is currently at an inflection point and is just too cheap to ignore. While this isn't a sexy big tech company such as Microsoft ( MSFT ) or Tesla ( TSLA ), this company can be a wonderful investment.

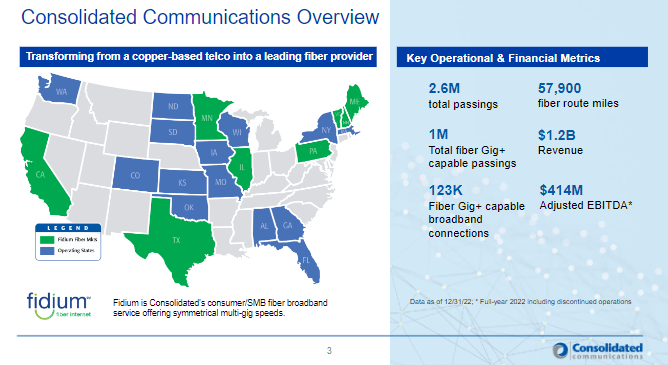

CNSL decided to pivot from a declining, low-margin telecommunications company into a strong fiber business all over the United States. Why fiber you may ask yourself. Fiber-optic technology is the way to go for faster and more reliable connectivity in today's world. It's time to leave behind the limitations of copper wiring and embrace the future of digital communication.

Consolidated Communications Q1 2023 earnings presentation

{kind=link}

So, what makes fiber-optic cables superior? Well, for starters, they use photons to transmit data, which travel at the speed of light! Compare that to copper, which relies on electrons and is simply no match for fiber's lightning-fast speeds. Additionally, fiber-optic cables boast higher bandwidth and lower latency, resulting in a smoother, more efficient user experience.

Not only that, but fiber-optic cables also experience far less signal degradation than copper over long distances. At 100m, copper loses up to 94% of its signal, while fiber-optic cables only experience a 3% loss. That's a massive difference!

Fiber-optic cables are also more durable, lighter, and smaller than traditional copper wiring. This translates to lower maintenance costs and a longer lifespan.

It's no wonder that CNSL is switching to fiber. It's considered "future-proof" and offers unbeatable connectivity advantages. With the government investing over $170 million in funding opportunities for broadband infrastructure, it's clear that the future of digital communication lies in fiber-optic technology.

Lack of Competition

"CNSL basically operates in a monopoly or duopoly in just about every market that they operate in. 11% of CNSL’s footprint is monopolistic with zero competitors. Another 83% of CNSL’s footprint is a duopoly with just a single competitor. The remaining 6% is an “oligopoly” with two competitors. Thus 94% of its markets are either in a monopoly or a duopoly", according to Rogue Funds.

Their competitive standpoint allows them to enjoy stronger pricing advantages, which leads to greater margin expansion, with most fiber companies having EBITDA margins of around 50%.

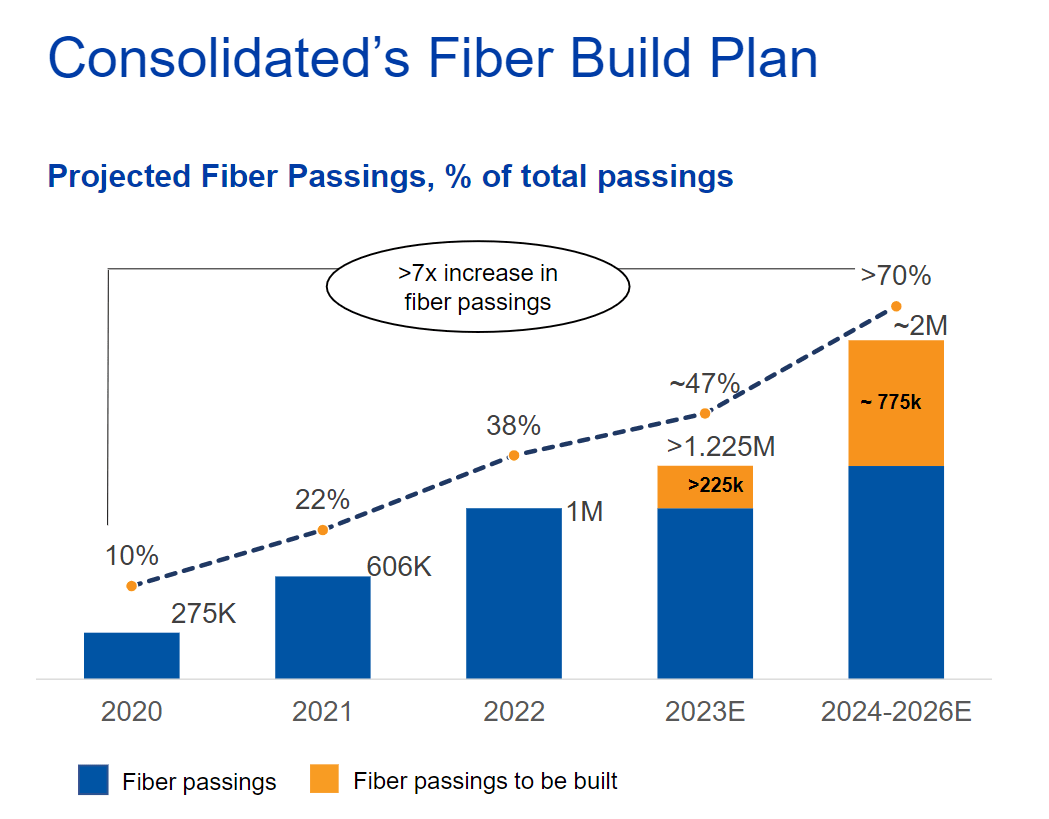

As can be seen in the slide below, the company expects to reach 70% of total passings to be fiber passings by 2026. This is a significant increase from their current 38% of total passings. We believe this will continue, which would increase their revenue per user by around 20%. In addition, we believe this % increase in revenue per user will continue to grow as well.

Consolidated Communications Q1 2023 earnings presentation

{kind=link}

Debt Situation

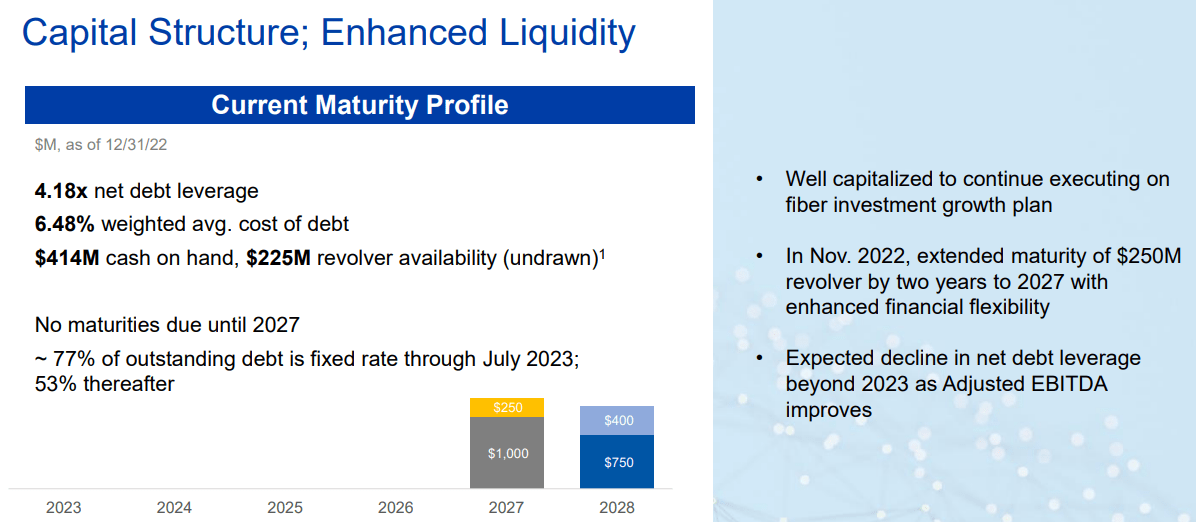

We are not going to sugarcoat this, CNSL has a lot of debt. Mainly due to the fact that they have to front-run a lot of their capital expenditure, which will affect their balance sheet in the upcoming years. In the slide below, you can see the capital structure.

{kind=link}

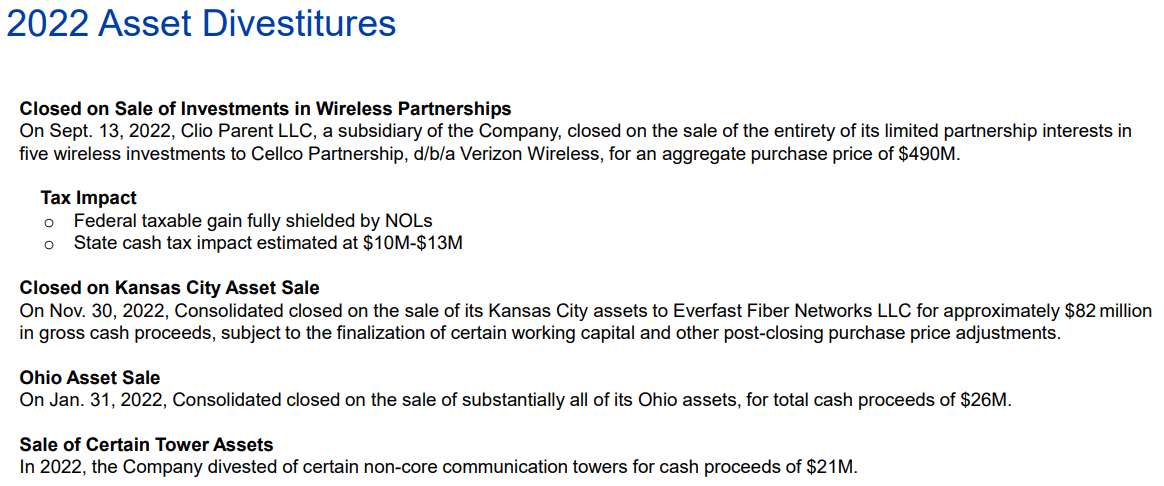

Their loans are made at great terms. The company was able to take advantage of the low rates in 2021. The biggest part of their debt matures in 2027 ($1b at 4.25%) and 2028 ($1.15B at 5% and 6%). In addition, the company is also divesting assets to continue paying for the capital expenditure that is needed. In other following slide you can see the most recent asset divestitures the company made.

{kind=link}

As most of their unneeded assets are now sold off. It is time to start focusing on acquiring customers and executing the plan until they are able to start increasing their revenue from their customers.

Insiders and the Buy-Out Offer

The CEO owns around 1% of the shares and the CFO owns around 0.5% of the shares. But, more importantly, there hasn't been a single insider that has sold shares since 2016. This shows that even though the share price plummeted, the insiders remain confident in the business. CNSL has one significant insider namely Searchlight Capital Partners. This name might sound familiar as this is the insider who has submitted the take-over bid.

Searchlight Capital Partners owns 34.3% or 39,338,753 shares of CNSL according to their latest 13D filing . The buy-out offer is no surprise as the company has just become too cheap to ignore as we mentioned at the beginning of this article. While shareholders who bought in the low $2's might be happy with this quick 80%+ gains, we believe the buy-out offer is simply too low. We believe this due to our expectations of a $16 to $20 share price in 2026-2027 (if the company is able to execute), that a buy-out between $6-$7 is fair at this moment in time. We will go more in-depth on the valuation of the company in the next paragraph.

In all honesty, we would rather see this company execute its plan and get this sweet long-term share appreciation. Nonetheless, I'll take $6 per share if the deal closes in 2023. It is fairly likely that the company declines the bid (as they should), but, we believe Searchlight won't give up so easily. I expect them to raise their offer in the next few months and eventually a buy-out will more than likely follow. We expect a price between $5.50 and $6 to be the final price.

The current buy-out offer will put a cushion below the share price and the shares will more than likely find solid support between $3.50 and $4.

Valuation

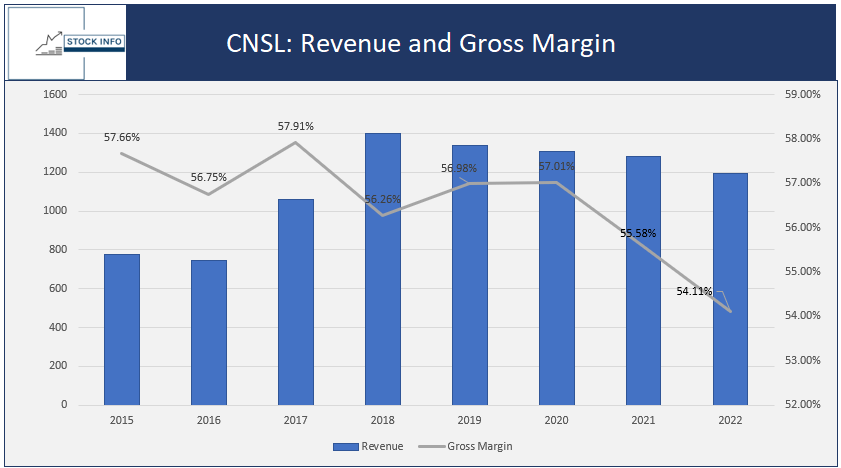

In the case of CNSL, we believe debt is a good thing. Especially, since the company has relatively cheap debt. We believe the market is undervaluing CNSL significantly. Even after today's close to 40% jump in share price, the company is still only sitting at a market cap of $317M. The enterprise value is around $2.5B, this will more than likely increase further as the company burns cash by expanding its business. In the chart below, you can see the historical financials of CNSL.

{kind=link}

The company currently has $414M cash on hand, which is almost $100M more than its current market cap. The market tends to undervalue companies like CNSL significantly due to the high debt, and we can't blame the market for that. Often businesses with such a high amount of debt will eventually default, but this shouldn't be the case for CNSL as they will generate plenty of money down the line if they are able to execute.

CNSL is a growth company and should be seen as such. CNSL isn't planning on taking on more debt like other growth companies. It seems like CNSL has a solid plan in place to pay off its debt. By 2025, we expect that the company has been able to reduce its capex significantly.

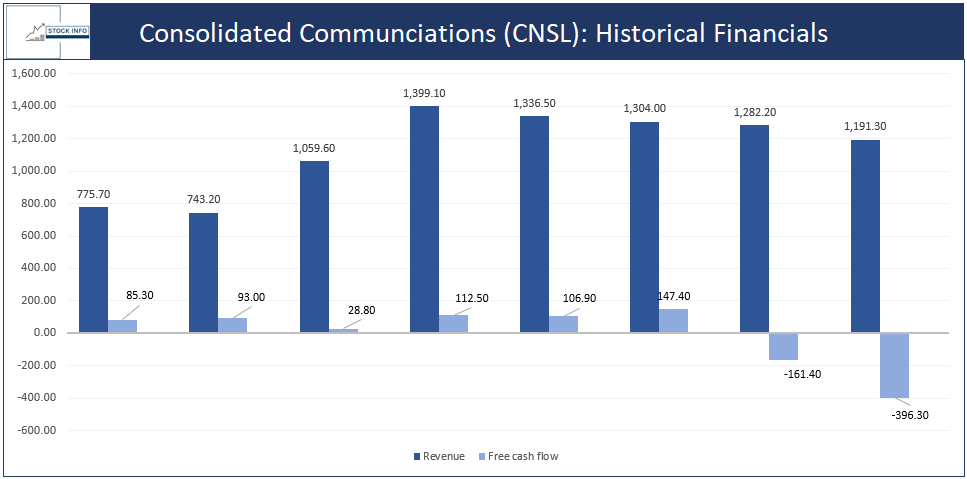

In addition, we expect the company to be operating with an EBITDA in the range of $600 to $800M in 2026-2028. In addition, Fiber is much cheaper to maintain than their current passing, this will reduce maintenance capex significantly. In the figure below, you can see the historical revenue and FCF of CNSL.

Nonetheless, we expect the company to perform and turn their business around. Currently, the management seems on track to accomplish its goals and they are reaching their goals earlier than expected.

{kind=link}

We believe this should give them plenty of cash flow to pay off their debt and additionally significantly improve their balance sheet. If all goes well, that would mean the company pays off its debt and reaches its revenue and cash flow numbers they are currently valued at 0.5x the EBITDA of 2025, which we consider too low.

Conclusion

We believe CNSL is a strong buy for long-term investors as the company tries to execute its plan and seems to be undervalued. In addition, the takeover bid by Searchlight Capital that was announced today will provide a cushion for the share price in the upcoming months.

The biggest risk to the thesis is that a lowball offer, such as the current one will be accepted. We believe this is highly unlikely as the management seems to be aware of what they own and no insider sells occurred since 2016. In addition, Searchlight seems to be aware of the fact that the company is currently undervalued, which is why it made a bid for the remaining shares.

Furthermore, there is obviously a risk that the company isn't able to execute as planned, but even if they only partially achieve their goals, the company remains undervalued in our opinion. We expect the current $4 bid to be rejected by the company and expect a new bid to come in the next few months in the $5-$6 range, which the company should consider at this moment in time. Nonetheless, we would rather not see the company go private.

For further details see:

Consolidated Communications: The Buyout Offer Is Too Low