CWCO - Consolidated Water: Being Careful With This Water Company

2023-03-06 12:05:56 ET

Summary

- I've been reviewing water utilities for some time, and my investments into York Water and other water companies have been covered.

- Consolidated Water Company is a business in water, specifically in Caribbean geographies, with a company in the Grand Caymans.

- This company has higher risk than other water utilities - but we can still invest in it, if we understand it and buy it at a cheap enough valuation.

Dear readers/followers,

In this article, I'll be taking a look at the Consolidated Water Co. ( CWCO ). This is a business in the water segment, with operating geographies in the Caribbean islands. What it does is finance, build, design, and operate seawater reverse osmosis or SWRO operations in its geographies. These operations turn seawater into potable water. The company also designs and operates distribution systems in the area.

In this article, we'll see if there is a valuation where the company is attractive, and more importantly where this valuation is and how "far" we're from it at this time, given the company's fundamentals.

Consolidated Water Company - The company from A to Z

So, the company's operations are found in the Caymans, the Bahamas, the US mainland, and the British Virgin Islands. Production plant locations are in Cayman, Bahamas, and the British Virgin Islands. The company operates 11 plants across these geographies, which have the capacity to produce 25.5 million gallons each day through SWRO operations. The company also has manufacturing operations, where it both produces and services specialized products and systems related to water operations on a commercial, municipal, and industrial level. The revenue split for the company is the following:

- 33% from Retail Water Operations

- 40% from Bulk Water Operations

- 21% from Service Operations

- 6% from Manufacturing Operations

What the company does is water services from A to Z in its operating geographies. CWCO also manages the treatment and reuse infrastructure. The company does seek to continually expand its operations, given that there is a continued demand for desalinated potable water, and its potential target areas include the US mainland.

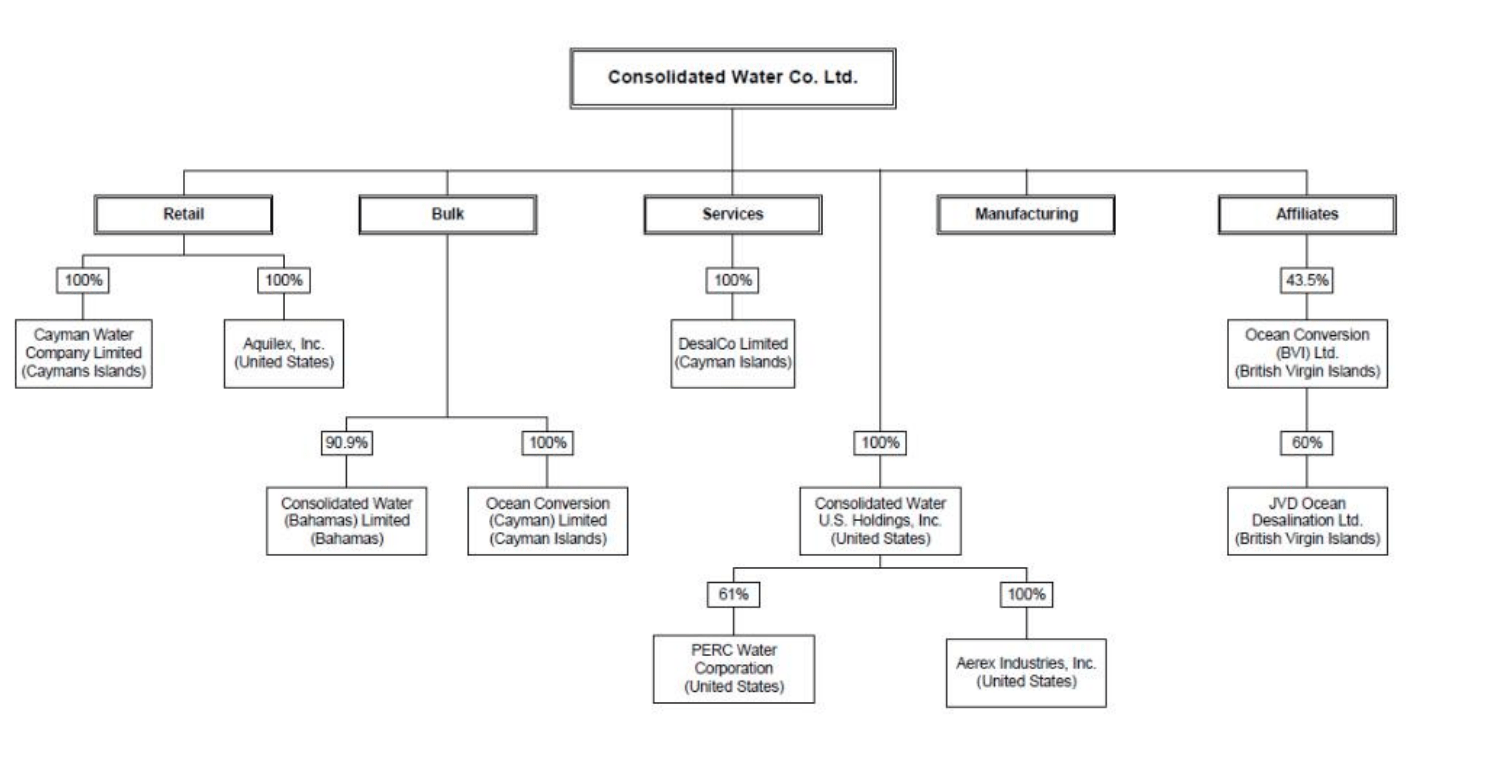

Here is the company's current organization. Like most companies in this segment, CWCO is a holding company with the following.

{kind=link}

In the Grand Cayman alone, the company manages 100 miles of potable water pipelines. Given the company's operating geographies, CWCO is somewhat cyclical depending on rainfall and tourism in the various areas it operates in. Obviously, and unlike many other water companies, CWCO saw some significant impact due to COVID-19 lowering the tourism numbers in the various operating geographies.

Manufacturing operations consist of Aerex. The manufacturing operations are headquartered in Florida, and all of the customers for these products are U.S. companies.

The company has similar margins to other water companies, managing an 8-12% operating margin, with some years seeing as high as 15% from non-recurring effects, with a net income margin around 2-3% lower than OM.

This company is small. It manages around $80-$90M worth of revenues, from which it manages around $7-$8M worth of operating income. The company has just below $180M worth of assets that it manages, less than $10M worth of long-term debt.

The most recent results showcase significant increases in company revenues both on a YoY basis and on the basis compared to the last 5 years - same with earnings, which are also growing. These increases represent growth in all of the company's 4 business segments.

However, being a smaller operator compared to its peers, CWCO is more impacted by the cost increases like G&A - though the company is clear in stating that they don't believe G&A will be as bad for the coming quarters. As far as tourism goes, this has already reversed, and the company has seen volume reversal - 14% in 3Q22 alone - due to the return of tourism.

The company is also expanding its US-based operations, with a contract for an advanced treatment plant in Goodyear, AZ. CWCO expects significant revenue and EPS impact from this In 4Q22 as well as 2023.

Traditionally speaking, this company's revenues and income have been more volatile than we'd typically expect out of water businesses, which tend to have extremely linear income and earnings trends, given their stable fundamental nature. CWCO, due to its size and specifics, breaks this mold.

A quick glance at the way the company has gone over the past 20 years because we do have a history this long, shows us that there has been some incredible volatility during that time. While long-term investors are up, they are not beating the market, and it's been a hell of a ride, to say the least.

CWCO Valuation/EPS (F.A.S.T graphs)

{kind=link}

I doubt this'll change going forward either. The company is likely to see some growth in revenue and earnings from its ongoing projects - as you can see in the current forecasts, but we'll see how long this lasts in the face of other pressures.

From a high level, and compared to other water businesses, CWCO is a pretty unique business model, because it combines retail water with desalination as well as wastewater contracting, of all things. In the short term, this stock can be an incredible play with great upside when it's bought at undervaluation, but the high-level long-term view on this stock is far more complicated.

Usually, with water businesses, we can point to solid trends delivering long-term slow-and-steady EPS growth. Not so for CWCO.

The following risks aren't non-trivial for this company:

1. Size risk. CWCO lacks the meaningful size to operate even close to a small business like York Water ( YORW ). Cost increases, G&A, inflation and macro do meaningful damage to the company's margins, as seen in the more recent reports. When you're a sub-$100M company, you really don't have the elbow room to do much, and the margin volatility we see on part of CWCO confirms this - as does the earnings volatility. There is a reason no other water company I review is this volatile - and part of that is size. CWCO lacks it , and that can be a very serious problem.

2. Geographical risk/climate risk. Usually, I consider this to be somewhat negligible. However, with the company's operating geographies centered around areas that are bound to be directly impacted by climate and weather changes, I don't believe it's wise to completely ignore the impacts this might have on a small business like this. The company is essentially a play to bring water to remote places with a tourist attraction. This can be a great idea - as long as those places continue to be "safe" and attractive to visit.

That's not even mentioning the tourism impacts on the company - meaning the volatility from having hotels and resorts as some of its primary customers, which are about as cyclical as the real estate itself - and if you're unfamiliar with how cyclical and how impacted resorts and tourist attractions can be, check out some of our work on Hotel/Resort REITs.

Don't get me wrong. This company is not "all bad" - I wouldn't be writing about it if there wasn't a case to be made to "BUY" it - but there are some key risks that are very difficult to get past - and this is especially true at today's valuation for the company.

Valuation for Consolidated Water - It's not attractive

While this company does come with theoretically attractive fundamentals, those fundamentals are currently unable to make up for the company's high valuation, despite estimated EPS growth and earnings growth. The company trades at a P/E of above 25x if we normalize it at lower levels, and consider for a moment that the analyst accuracy for this company is one of the worst I have ever seen.

Seeking Alpha FactSet analyst Accuracy (F.A.S.T Graphs)

Based on this accuracy, you could actually have shorted the company and come out on top during many of these forecasts - and that's bad. The company, while being a water utility (technically), also comes with a certain industrial and contracting component given its various arms. Couple industrial volatility with tourism volatility and climate volatility, and you may understand why I say that CWCO can be said to "take the safety out of a water utility". Only in name does the company really have these sorts of safeties, not in how the company actually operates.

Analysts following the company seem to ignore every single one of these risks. There are only two of them following the company for S&P Global, but both of them come in between $18-20/share, with an average of $19.5/share. 1 of them at a "BUY", one at a "HOLD". Not much to write home about there, even if we do see a 26.6% upside to that PT. However, I really wouldn't give any credence to that target.

The same is true with peers. I won't be comparing it to other water utilities like YORW, because it lacks what makes YORW and similar companies safer and that gives them the conservative argument for investing.

If you're willing to treat CWCO like a water utility, and you're willing to treat the estimated EPS growth as gospel, then you could see some returns in the triple digits here. However, with annual revenues below $100M, a market cap of less than $250M, and a yield of less than 2.3%, I consider CWCO to be a risky, mixed water/industrial/tourism play with a non-trivial climate risk component and a size disadvantage.

While the company has been around a long time, and I could see my way to treating it as a "spec" play at around 10-13x P/E, there is no way I would consider this company seriously above 20x.

There are too many good companies with credit ratings, better yields, larger sizes, and safer upsides out there, in any market situation that I have ever come across.

For that reason, I take a very conservative thesis on CWCO as I'm looking at it here.

Thesis

- While a water utility in name, CWCO comes with a number of segments and businesses run in volatile areas and with cyclical end-customers in leisure and tourism that makes this company's revenues and earnings have something like a YoYo character. This is the last thing I want to see in a conservative water investment that I make.

- For that reason, I'm giving this company a very conservative price target - I wouldn't be interested in investing at anything more expensive than a 10-15x P/E, which even at future normalized levels with the revenue and earnings increases considered, comes to around $11-$12/share, discounted around 15-20% for the size risk.

- That means I'm a "HOLD" here, and I wouldn't buy CWCO at this time.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic and conservative upside based on earnings growth or multiple expansion/reversion.

CWCO fulfills 2 out of 5 of my criteria, which is low, and warrants the conservative "HOLD" rating I give it.

For further details see:

Consolidated Water: Being Careful With This Water Company